D104 - OA #1 Intermediate Accounting II

1/81

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

82 Terms

Property, Plant, and Equipment

Plant and fixed assets

Used in operations and not for resale

Long-term and usually depreciated except for land (unless a decrease in value occurs like soil erosion)

Possess physical substance

Historical Cost

Measures the cash or cash equivalent price of obtaining the asset and bringing it to the location and condition necessary for its intended use

Purchase price

Used to value PP&E

Fair Value

It is current and market-based

Carrying amount

It is the asset’s worth after subtracting depreciation from its original cost

Cost of Land

All expenditures made to acquire land and ready it for use

Includes:

Purchase price

Legal fees (title, attorney)

Costs incurred in getting the land in condition for its intended use, such as grading, filling, draining, and clearing (such as demolition/removal of buildings)

(Cost of demolition - Salvage value)

Any additional land improvements that have an indefinite life

Any taxes or liens

Land as PP&E

Land is generally PP&E unless it is an investment or held of resale (inventory)

Cost of Buildings

Includes all expenditures related directly to their acquisition or construction. These costs include:

Materials, labor, and overhead costs incurred during construction

Professional fees and building permits

Architect’s Fee

Blueprints

Capitalized interest

Cost of Equipment

Includes all expenditures incurred in acquiring the equipment and preparing it for use

Such as:

Purchase price

Freight and handling charges incurred

Insurance on the equipment while in transit

Assembling and installation costs

Costs of conducting trial runs

Self-Constructed Assets - Indirect/Overhead Costs

Companies should assign to the asset a pro rata portion of the fixed overhead to determine its cost

Pro Rata: Proportional

Interests Costs During Construction

GAAP requires capitalizing (deferring) actual interest

This method follows the concept that the historical cost of acquiring an asset includes all costs (including interest) incurred to bring the asset to the condition and location necessary for its intended use

Once construction is complete, the company should report interest as an expense in future periods, when the asset contributes to these revenues

2 Items to Capitalize Actual Interest

To implement this general approach, companies consider three items:

Qualifying assets

Capitalization period

Amount to capitalize

Qualifying Assets

To qualify for interest capitalization, assets must require a period of time to get them ready for their intended use

Ex.: assets under construction for a company’s own use (including buildings, plants, and large machinery) and assets intended for sale or lease that are constructed or otherwise produced as discrete projects (e.g., ships or real estate developments)

Capitalization Period

It is the period of time during which a company must capitalize interest

It begins with the presence of three conditions:

Expenditures for the asset have been made

Activities that are necessary to get the asset ready for its intended use are in progress

Interest cost is being incurred

The capitalization period ends when the asset is substantially complete and ready for its intended use

Avoidable Interest

The amount of interest cost that a company could theoretically avoid if it had not made expenditures for the asset

To apply the avoidable interest concept, a company determines the potential amount of interest that it may capitalize during an accounting period by multiplying the interest rate(s) by the weighted-average accumulated expenditures for qualifying assets during the period

Amount to Capitalize

The amount of interest to capitalize is limited to the lower of actual interest cost incurred during the period or avoidable interest

GAAP requires interest capitalization for a qualifying asset only if its effect, compared with the effect of expensing interest, is material

Weighted-Average Accumulated Expenditures

In computing the weighted-average accumulated expenditures, a company weights the construction expenditures by the amount of time (fraction of a year or accounting period) that it can incur interest cost on the expenditure

Expenditure = Amount x Capitalization Period

Ex.: 6/12 = Six months

Weighted-Average Interest Rate

Total Interest / Total Principal

Interest rate Incurred on Specific Borrowings

For the portion of weighted-average accumulated expenditures that is less than or equal to any amounts borrowed specifically to finance construction of the assets, use the interest rate incurred on the specific borrowings

Weighted Average of Interest Rates Incurred

For the portion of weighted-average accumulated expenditures that is greater than any debt incurred specifically to finance construction of the assets, use a weighted average of interest rates incurred on all other outstanding debt during the period

Expenditures for Land

If land is purchased to develop it for a particular use, interest costs qualify for interest capitalization

If land is purchased as a site for a structure (plant site), interest costs are not capitalized as land, but as part of the plant

If a company develops land for lot sales, it includes any capitalized interest cost as part of the acquisition cost of the developed land. However, it should not capitalize interest costs involved in purchasing land held for speculation because the asset is ready for its intended use

Interest Revenue

Companies should capitalize the interest incurred on qualifying assets whether or not they temporarily invest excess funds in short-term securities

Valuation of PP&E - Cash Discounts

Companies should record property, plant, and equipment at the fair value of what they give up or at the fair value of the asset received, whichever is more clearly evident

Deferred-Payment Contracts

To properly reflect cost, companies account for assets purchased on long-term credit contracts at the present value of the consideration exchanged between the contracting parties at the date of the transaction

Lump-Sum Purchases

When this common situation occurs, the company allocates the total cost among the various assets on the basis of their relative fair values. The assumption is that costs will vary in direct proportion to fair value

When should costs be capitalized?

In general, costs incurred to achieve greater future benefits should be capitalized, whereas expenditures that simply maintain a given level of services should be expensed

What three conditions must be present to capitalize costs?

The useful life of the asset must be increased

The quantity of units produced from the asset must be increased

The quality of the units produced must be enhanced

4 Major Types of Expenditures Relative to Existing Assets

Additions: Increase or extension of existing assets

Improvements and Replacements: An improvement (betterment) is the substitution of a better asset for the one currently used and a replacement is the substitution of a similar asset

Rearrangement and Reinstallation: Movement of assets from one location to another

Repairs: Expenditures that maintain assets in condition for operation

Additions

Companies capitalize any addition to plant assets because a new asset is created

If the company had anticipated an addition later, then this cost of removal is a proper cost of the addition

If the company had not anticipated this development, it should properly report the removal as a loss in the current period

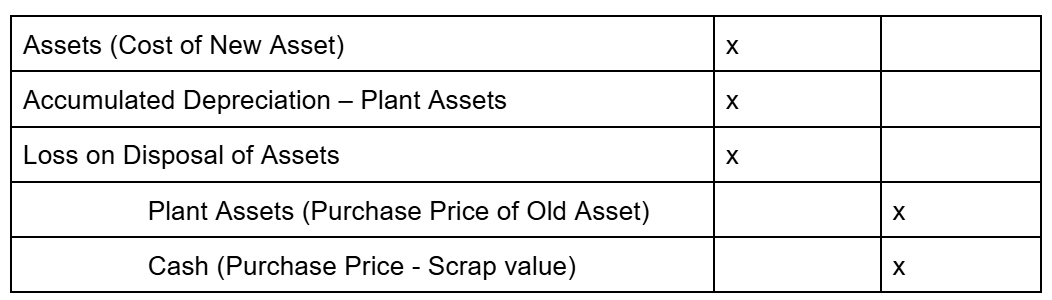

Improvements and Replacements

If the expenditure increases the future service potential of the asset, a company should capitalize it

3 Methods to Account for Improvements and Replacements

Use the substitution approach

Remove the cost of the old asset and replace it with the cost of the new asset

Capitalize the new cost

Capitalizes the improvement and keeps the carrying amount of the old asset on the books

Companies usually handle improvements in this manner

Charge to accumulated depreciation

In cases when a company does not improve the quantity or quality of the asset itself but instead extends its useful life, the company debits the expenditure to Accumulated Depreciation rather than to an asset account

Substitution Approach - Journal Entry

Rearrangement and Reinstallation

If a company can determine or estimate the original installation cost and the accumulated depreciation to date, it handles the rearrangement and reinstallation cost as a replacement

If not, they should capitalize the new costs (if material in amount) as an asset to be amortized over future periods expected to benefit

If these costs are immaterial, if they cannot be separated from other operating expenses, or if their future benefit is questionable, the company should immediately expense them

Repairs

A company makes ordinary repairs to maintain plant assets in operating condition

Maintenance charges that occur regularly include replacing minor parts, lubricating and adjusting equipment, repainting, and cleaning

A company treats these as ordinary operating expenses

Repairs vs Improvement & Replacement

The major consideration is whether the expenditure benefits more than one year or one operating cycle, whichever is longer

If a major repair (such as an overhaul) occurs, several periods will benefit. A company should handle the cost as an addition, improvement, or replacement

Disposition of PP&E

Sale of Plant Assets

Involuntary Conversion

Miscellaneous Problems

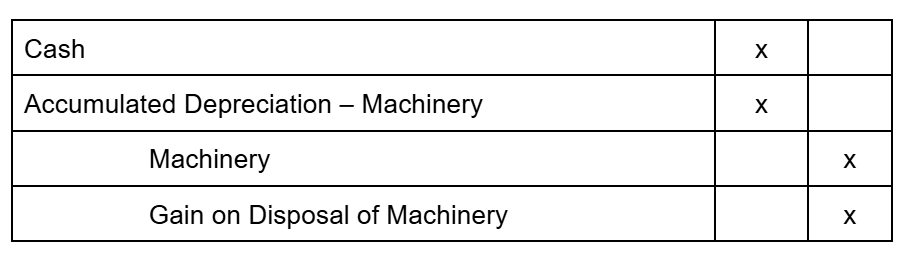

Sale of Plant Assets

Companies record depreciation for the period of time between the date of the last depreciation entry and the date of sale

Sale of Plant Assets - Depreciation to Date of Sale Entry

Sale of Plant Assets - Sale of Asset Entry

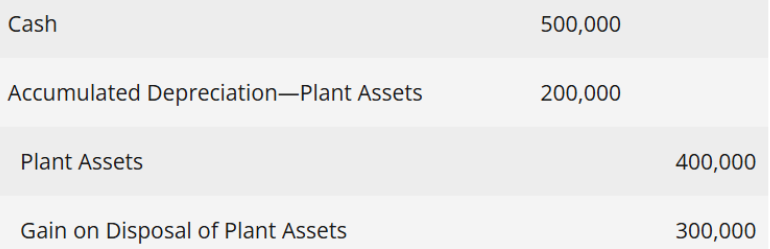

Involuntary Conversion

Sometimes an asset’s service is terminated through some type of involuntary conversion such as fire, flood, theft, or condemnation

Companies report the difference between the amount recovered, if any, and the asset’s book value as a gain or loss

Involuntary Conversion - Journal Entry

Intangible Asset Characteristics

They lack physical existence

They are not financial instruments

Ex.: AR, long-term investments

Valuation of Purchased Intangibles

Companies record at cost intangibles purchased from another party. Cost includes all acquisition costs plus expenditures to make the intangible asset ready for its intended use

Ex.: purchase price, legal fees, and other incidental expenses

Sometimes companies acquire intangibles in exchange for stock or other assets. In such cases, the cost of the intangible is the fair value of the consideration given or the fair value of the intangible received, whichever is more clearly evident

In such a “basket purchase,” the company should allocate the cost on the basis of fair values

Valuation of Internally Created Intangibles

Sometimes a company may incur substantial research and development (R&D) costs to create an intangible

Costs incurred internally to create intangibles are generally expensed

Companies capitalize only direct costs incurred in developing the intangible, such as legal costs, and expense the rest

Life of Intangibles

Intangibles have either a limited (finite) useful life or an indefinite useful life

Amortization of Limited-Life Intangibles

Companies amortize their limited-life intangibles by systematic charges to expense over their useful life

The useful life should reflect the periods over which these assets will contribute to cash flows

The residual value is assumed to be zero unless at the end of its useful life the intangible asset has value to another company

Companies should, on a regular basis, evaluate the limited-life intangibles for impairment

Amount to Amortize an Intangible Asset

Cost - Residual Value

Amortization of Indefinite-Life Intangibles

A company does not amortize an intangible asset with an indefinite life

Companies should test indefinite-life intangibles for impairment at least annually

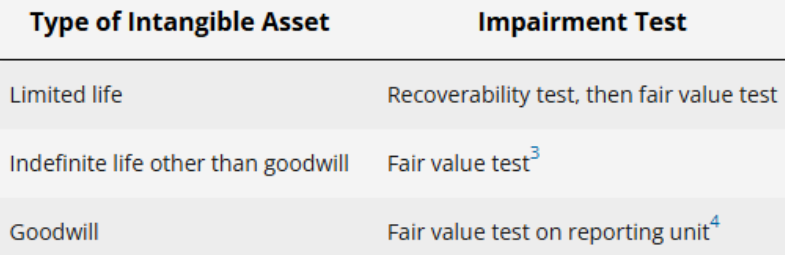

Impairment Test for Intangibles

For limited-life intangibles, you apply the recoverability test and then the fair value test

For indefinite-life intangibles, you only use the fair value test

Types of Intangible Assets

Marketing

Customer

Artistic

Contract

Technology

Marketing-Related Intangible Assets

Marketing or promotion of products or services (ex.: trademarks, internet domain, etc)

If a company buys a trademark or trade name, it capitalizes the purchase price as the cost of the asset

If a company develops a trademark or trade name, it capitalizes costs related to securing it, such as attorney fees, registration fees, design costs, consulting fees, and successful legal defense costs. However, it excludes research and development costs

When the total cost of a trademark or trade name is insignificant, a company simply expenses it

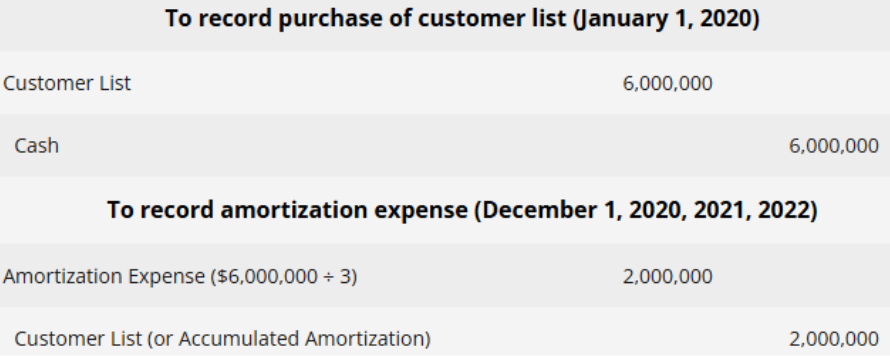

Customer-Related Intangible Assets

Results from interactions with outside parties (ex.: customer lists, order or production backlogs, and both contractual and noncontractual customer relationships)

Companies should assume a zero residual value unless the asset’s useful life is less than the economic life and reliable evidence is available concerning the residual value

Customer-Related Intangible Assets Journal Entry

Artistic-Related Intangible Assets

Involves ownership rights to plays, literary works, musical works, pictures, photographs, and video and audiovisual material

Companies capitalize the costs of acquiring and defending a copyright. They amortize any capitalized costs over the useful life of the copyright if less than its legal life (life of the creator plus 70 years)

Contract-Related Intangible Assets

Represent the value of rights that arise from contractual arrangements

Ex.: franchise and licensing agreements, construction permits, broadcast rights, and service or supply contracts

A company should amortize the cost of a franchise (or license) with a limited life as an operating expense over the life of the franchise

It should not amortize a franchise with an indefinite life nor a perpetual franchise; the company should instead carry such franchises at cost

Technology-Related Intangible Assets

Relate to innovations or technological advances

Ex.: patented technology and trade secrets granted by the U.S. Patent and Trademark Office

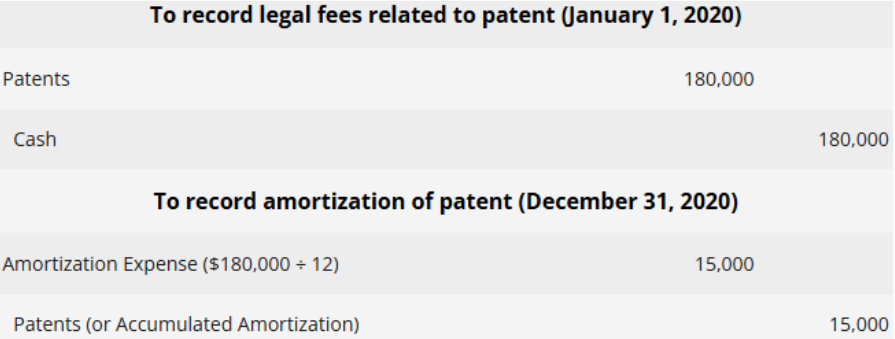

Companies should amortize the cost of a patent over its legal life or its useful life (the period in which benefits are received), whichever is shorter

Technology-Related Intangible Assets Journal Entry

Goodwill

Goodwill = Purchase price - Fair Value

It is measured as the excess of the cost of the purchase over the fair value of the identifiable net assets (assets less liabilities) purchased

Represents the future economic benefits arising from the other assets acquired in a business combination that are not individually identified and separately recognized

The only way to sell goodwill is to sell the business

Internally Created Goodwill

Goodwill generated internally should not be capitalized in the accounts

Impairment

It is a write-off done when the carrying amount of a long-lived asset (property, plant, and equipment or intangible asset) is not recoverable

Recoverability Test

A company should review PP&E for impairment at certain points—whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable. In performing this recoverability test the company estimates the future cash flows expected from use of the asset and its eventual disposal

Fair Value Test for Limited-Life Intangibles

To measure the impairment, the company uses the fair value test

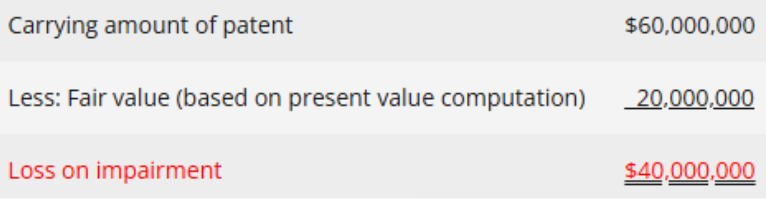

This test measures the impairment loss by comparing the asset’s fair value with its carrying amount

Impairment Loss = Carrying Amount of Asset - Fair Value of Impaired Asset

As with other impairments, the loss on the limited-life intangible is reported as part of income from continuing operations

The loss is generally reported in the “Other expenses and losses” section of the income statement

Impairment Loss

Impairment Loss = Carrying Amount of Asset - Fair Value of Impaired Asset

Impairment Loss Journal Entry

Impairment of Indefinite-Life Intangibles Other Than Goodwill

Companies should test indefinite-life intangibles other than goodwill for impairment at least annually

Companies do not use the recoverability test, just the fair value test

Fair Value Test for Indefinite-Life Intangibles

The impairment test for an indefinite-life intangible asset other than goodwill is a fair value test

This test compares the fair value of the intangible asset with the asset’s carrying amount

If the fair value is less than the carrying amount, the company recognizes an impairment

Companies use this one-step test because many indefinite-life assets easily meet the recoverability test (because cash flows may extend many years into the future)

Optional Qualitative Assessment - Indefinite-Life Intangibles

Companies have the option to perform a qualitative assessment (optional qualitative assessment) to determine whether it is more likely than not (i.e., a likelihood of more than 50 percent) that an indefinite-life intangible asset is impaired

If the optional qualitative assessment indicates that the fair value of the reporting unit is more likely than not to be greater than the carrying value (i.e., the asset is not impaired), the company need not continue with the fair value test

Impairment of Goodwill

Goodwill must be tested for impairment at least annually

The impairment rule for goodwill is a fair value (quantitative) test

A company compares the fair value of the reporting unit to its carrying amount, including goodwill

If the fair value of the reporting unit exceeds the carrying amount, goodwill is not impaired. The company does not have to do anything else

Impairment Summary

Balance Sheet - Presentation of Intangible Assets

Companies should report all intangible assets as a separate item other than goodwill on the balance sheet

If goodwill is present, companies should report it separately

Income Statement - Presentation of Intangible Assets

Companies should present amortization expense and impairment losses for intangible assets other than goodwill separately and as part of continuing operations

Goodwill impairment losses should also be presented as a separate line item in the continuing operations section, unless the goodwill impairment is associated with a discontinued operation

Financial Statement - Presentation of Intangible Assets

The notes to the financial statements should include information about acquired intangible assets, including the aggregate amortization expense for each of the succeeding five years

If separate accumulated amortization accounts are not used, accumulated amortization should be disclosed in the notes

The notes should include information about changes in the carrying amount of goodwill during the period

Research & Development Costs

R&D activities frequently result in the development of patents or copyrights (such as a new product, process, idea, formula, composition, or literary work) that may provide future value

Identifying R&D Activities

Research activities: planned search or critical investigation aimed at discovery of new knowledge

Development activities: translation of research findings or other knowledge into a plan or design for a new product or process or for a significant improvement to an existing product or process whether intended for sale or use

R&D activities do not include routine or periodic alterations to existing products, production lines, manufacturing processes, and other ongoing operations, even though these alterations may represent improvements

Accounting for R&D Activities - Materials, Equipment, and Facilities

Expense the entire costs, unless the items have alternative future uses (in other R&D projects or otherwise)

If there are alternative future uses, carry the items as inventory and allocate as consumed, or capitalize and depreciate as used

Accounting for R&D Activities - Personnel

Expense as incurred salaries, wages, and other related costs of personnel engaged in R&D

Accounting for R&D Activities - Purchased Intangibles

Recognize and measure at fair value

After initial recognition, account for in accordance with their nature (as either limited-life or indefinite-life intangibles)

Accounting for R&D Activities - Contract Services

Expense the costs of services performed by others in connection with the R&D as incurred

Accounting for R&D Activities - Indirect Costs

Include a reasonable allocation of indirect costs in R&D costs, except for general and administrative costs, which must be clearly related in order to be included in R&D

R&D Facility

If a company owns a research facility that conducts R&D activities and that has alternative future uses (in other R&D projects or otherwise), it should capitalize the facility as an operational asset

The company accounts for depreciation and other costs related to such research facilities as R&D expenses

Costs Similar to R&D Costs

Examples are:

Start-up costs for a new operation

Expense as incurred

Initial operating losses

Do not capitalize

Advertising costs

Expense as incurred

Computer software costs

Exclude from R&D

For the most part, these costs are expensed as incurred, similar to the accounting for R&D costs

Presentation of R&D Costs

Companies should disclose in the financial statements (generally in the notes) the total R&D costs charged to expense each period for which they present an income statement

Recoverability Test

If the sum of the expected future net cash flows (undiscounted) is less than the carrying amount of the asset, the company measures and recognizes an impairment loss