AP Economy

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

40 Terms

Profit

Total Revenue - Total Cost

Total Revenue

All the money the firm takes in from its sales

OR

P * Q

Total Cost

Comprises of two type of costs, explicit + implicit

EXPLICIT: cost that involves laying out money

IMPLICIT: doesn’t require outlay of money; measured by the value in terms of benefits that are forgone

Economic Profit

TOTAL REVENUE - OPPORTUNITY - EXPLICIT DEPREICFATION

Accounting Profit

TOTAL REVENUE - EXPLICIT COSTS/DEPRICATION

Implicit Cost of Capital

The opportunity cost of the capital used by a business — the income the owner could have realized from that capital if it had been used in its next best alternative WAY

Accounting Profit indicators

+ - best current use of resources

- : there is a better alternative use for resources

0: couldn’t be better or worse off

Principal of Marginal Analysis

every activity should continue until MARGINAL BENEFIT EQUALS MARGINAL COST

Marginal Revenue

The change in total revenue generated by an additional unit of output

Optimum output rule

Profit is maximized by producing the quantity of output at which the marginal revenue of the last unit produced is equal to its marginal cost

CHARTS FOR OUTPUT

MC - Total Cost Change

(EX: P1: 30

P2: 35

P2 - P1 = MC)

MR - CONSTANT COST OF A PRODUCT

Profit: Total Revenue - Total Cost

KEEP PRODUCING UNTIL PROFIT drops (highest possible profit)

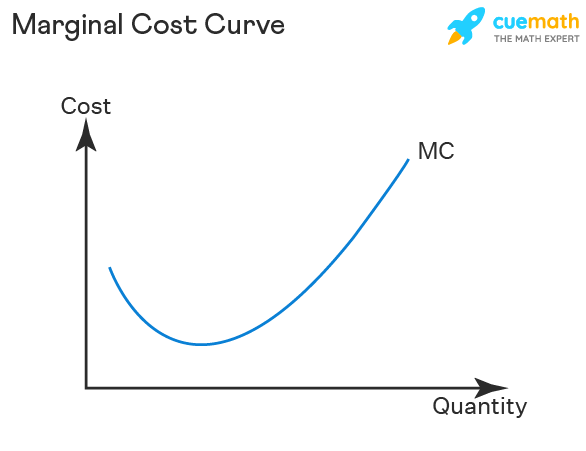

Marginal Cost Curve

shows how the cost of producing one more unit depends on the quantity that has already been produced

Profit Maximizing Quantity

Keep producing until you reach negative/make more revenue than costs

Marginal Revenue Curve

Shows how the marginal revenue varies as output varies

Production Function

The relationship between the quantity of inputs a firm uses and the quantity of outputs it produces

Fixed

an input whose quantity cannot be varied for a period of time

Variable input

An input whose quantity the firm can vary at any time

LONG RUN

period in which ALL inputs can be varies

SHORT RUN

period in which AT LEAST ONE input is varied

Production Function

The relationship between the quantity of the variable input and the quantity of output for a given quantity of a fixed input

Total product curve

increases at a decreasing rate, shows how the quantity of output depends on the quantity of variable input for any given quantity of fixed input

EX: too many people in the kitchen, becomes counter productive

Marginal Product Curve

when an increase in the quantity of that input, holding the levels of all other inputs fixed, leads to a decrease in the marginal product of that input

same as original curve, but reflecting CHANGE instead of overall

Law of Diminishing returns

When an increase in the quantity of that input PRODUCED, holding the levels of all other inputs fixed, leads to a decrease in the marginal product of that input

Fixed costs

Does not depend on the quantity of output produced EX: oven

Variable Costs

A cost that depends on the quantity of output produced EX: ingredients, pay for workers

Total Cost Curve

Becomes steeper as more output is produced due to diminishing returns

COST DEPENDS ON QUANTITY OUTPUT

could be bent based on FIXED COSTS

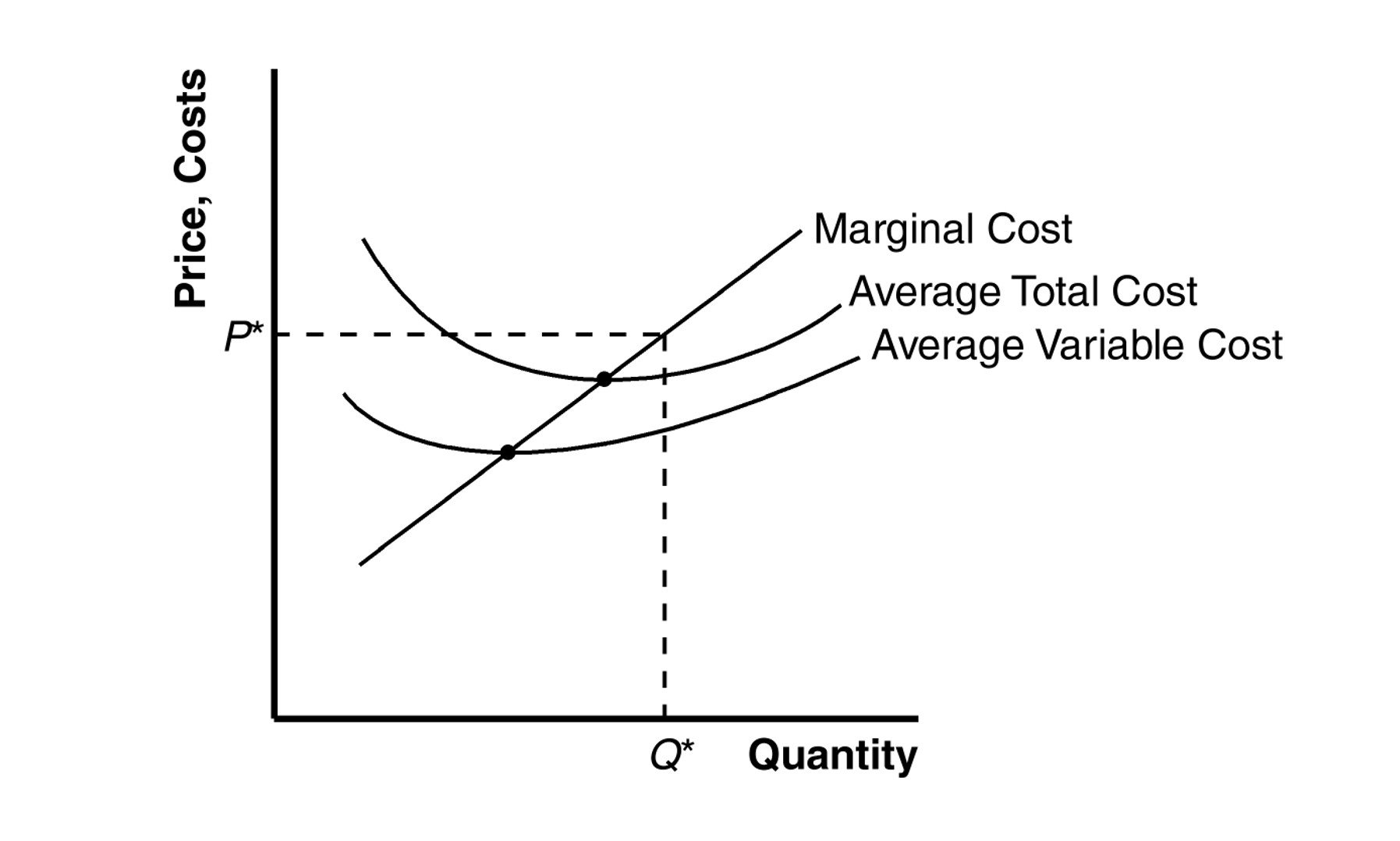

Marginal Cost

Change in total cost by producing 1 more unit

Average Total Cost

total cost divided by quantity of output produced, minimum costs can be MC = MR

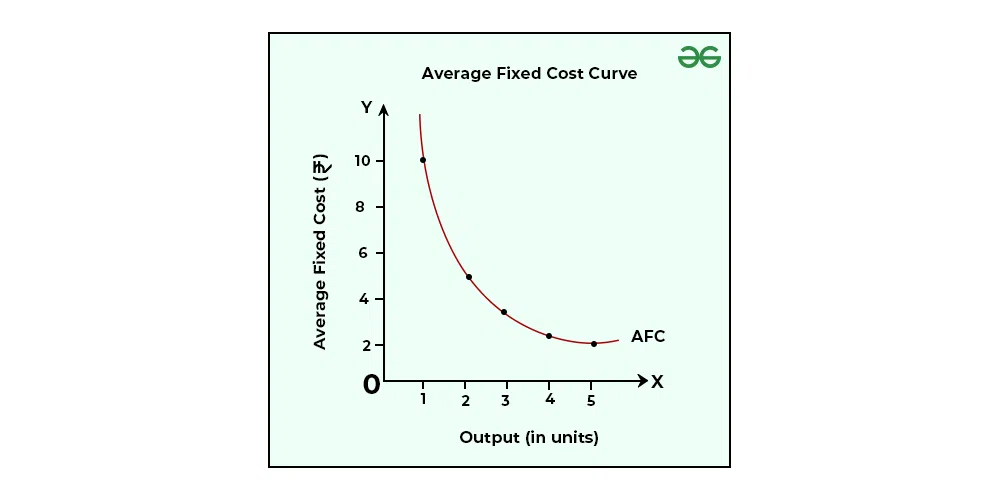

Average Fixed Cost

Fixed cost per unit of output

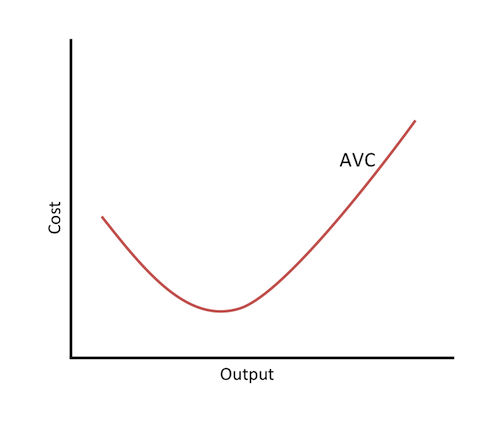

Average Variable

variable cost per unit of output

WHY IS ATC U-SHAPED

I. The spreading effect - the larger the output, the greater the quantity of output over which the fixed cost is spread, leading to a lower average fixed cost

II. The diminishing returns effect - the larger the output, the greater the amount of the variable input required to produce additional units, leading to a higher average variable cost

When output INCREASES,

average fixed costs decrease sooner average variable costs increase

Minimum Average Total Cost

Minimum cost Output: quantity of output at which your average total is lowest , The bottom of the TOTAL COST CURVE

If output < minimum-cost output, marginal cost is less than average total cost, and average total cost is falling (MC below ATC)

If output > minimum-cost output, marginal cost exceeds average total cost, and average total cost is rising (MC above ATC)

Average Product

the total product divided by the quantity of the input

Average Product Curve

shows the relationship between the average product and quantity of input

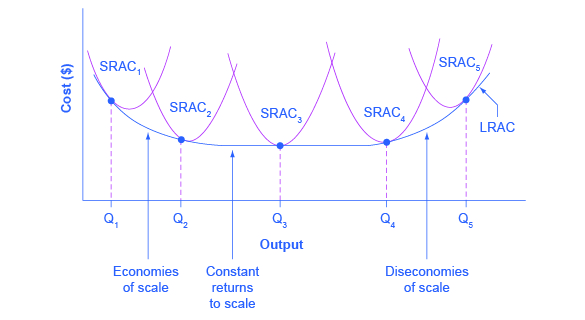

Long-Run Costs of Economies of Scale

shows the relationship between output and ATC, when fixed cost has been chosen to minimize average total cost for each level of output

LOWEST POINT IS WHERE YOU WANT TO BE AT, lowest costs

Economies of scale

when long-run average total cost decreasing as output increases

Diseconomies of scale

When long-run average total cost increases as output decreases

Constant returns to scale

When output increases directly in proportion to an increase in inputs

Sunk Costs

A cost that has already been incurred and is non-recoverable, should be ignored in future transactions