Chapter 8 - Perfect Competition

1/43

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

Market Structures

Economists categorize industries based on their market structure, which influences firm behavior regarding pricing and sales

Key characteristics used for market structure analysis

Number of firms in the industry

Nature of the industry’s product

Barriers to entry

Extent of individual firm control over prices

Potential for long-run economic profit

Primary Market Structures: Based on these characteristics, economists identify four main market structures:

Perfect Competition

Monopolistic Competition

Oligopoly

Monopoly

Perfect Competition

Many small firms selling homogeneous products with no barriers to entry or exit and no control over price (price takers). No long-run economic profit.

Monopolistic Competition

Many sellers offering differentiated products with little to no barriers to entry or exit and some control over price (limited market power). No long-run economic profit.

Oligopoly

Few large firms making mutually interdependent decisions with substantial barriers to market entry and shared market power (considerable control over price). Potential for long-run economic profit.

Monopoly

One firm with no close substitutes for its product, nearly insurmountable barriers to entry, and substantial market power (control over price). Potential for long-run economic profit.

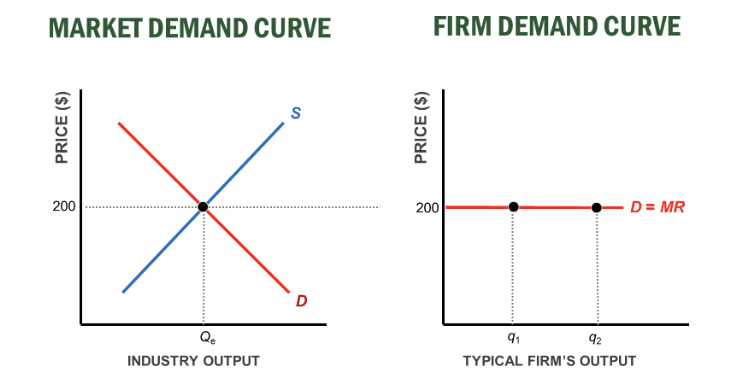

Defining Perfectly Competitive Markets

Many Buyers and Sellers

Each individual buyer and seller is too small to influence the market-determined price. Actions of one firm do not affect another.

Homogeneous (Nearly Identical) Products

Products offered by different firms are virtually the same, making quality mostly indistinguishable. Consumers see no difference and will always choose the lowest price.

No Barriers to Market Entry or Exit

New firms can freely enter the industry if it appears profitable, and existing firms can leave if they are incurring losses in the long run.

Perfect Information

Buyers and sellers have complete information about prices and product quality to make informed decisions.

Price Takers

Individual firms have no market power to set prices; they must accept the prevailing market price determined by overall market demand and supply. The firm's demand curve is perfectly elastic (horizontal) at the market price.

Perfect Competition: Short-Run Decisions

Profit-Maximizing Output

Firms aim to maximize economic profit (Total Revenue - Total Cost)

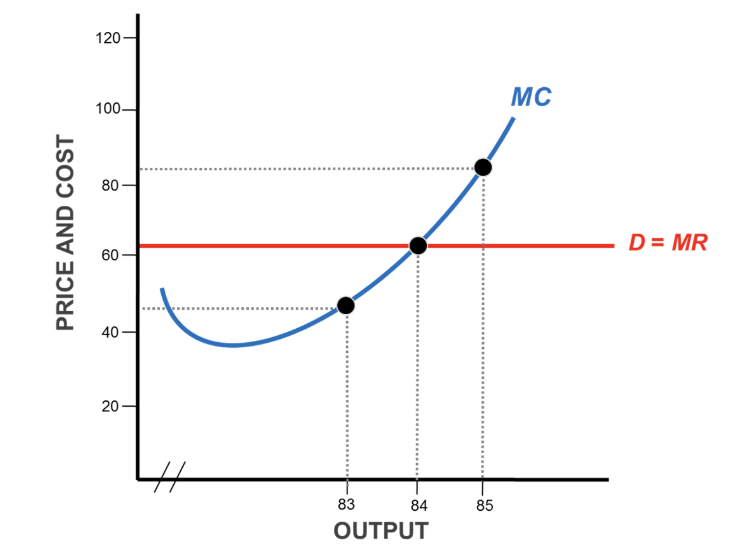

Profit-Maximizing Rule

A firm maximizes profit by producing the quantity of output where Marginal Revenue (MR) equals Marginal Cost (MC).

Producing below this level means forgoing potential profit because MR > MC.

Producing above this level reduces profit because MC > MR.

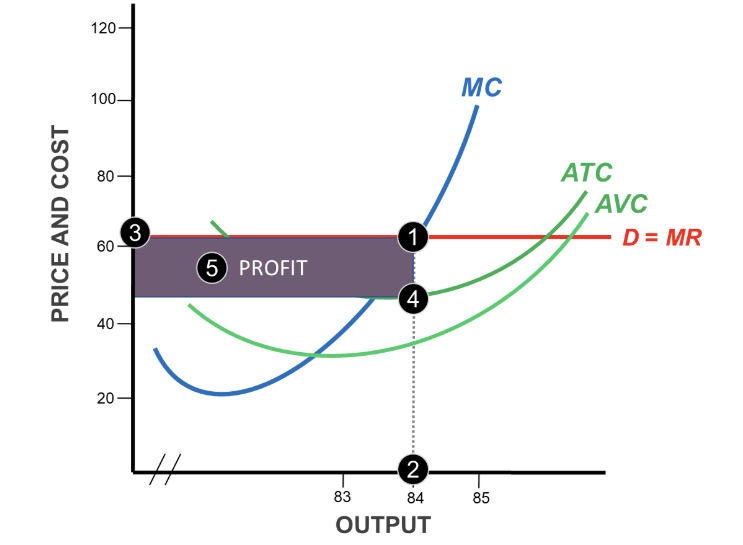

Economic Profit

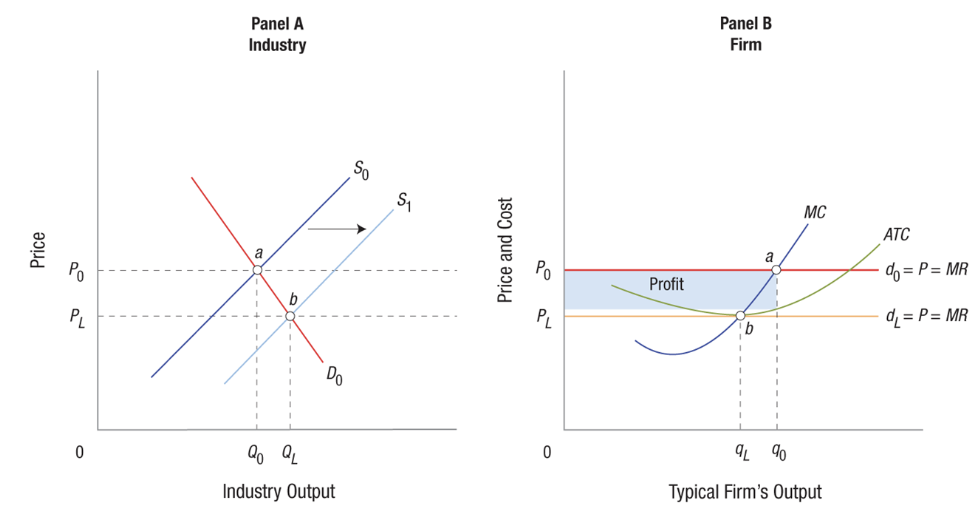

Occurs when price (P) > Average Total Cost (ATC) at the profit-maximizing quantity.

Total profit is (P - ATC) * Quantity.

Normal Profit (Zero Economic Profit)

Occurs when price (P) = minimum ATC. The firm earns enough revenue to cover all costs, including the opportunity cost of capital.

There is no incentive for entry or exit.

This is the break-even point.

Total revenue (TR)

is equal to price per unit (p) times quantity sold (q).

Profit

is equal to total revenue minus total cost.

Average total cost (ATC)

the total cost divided by the quantity of output.

Average variable cost (AVC)

the total variable cost divided by the quantity of output.

Marginal cost (MC)

the additional cost of producing one more unit of output.

Marginal revenue (MR)

the change in total revenue that results from the sale of one additional unit of a product.

It is calculated as the change in total revenue divided by the change in quantity sold.

In a perfectly competitive market, marginal revenue is simply equal to the market price.

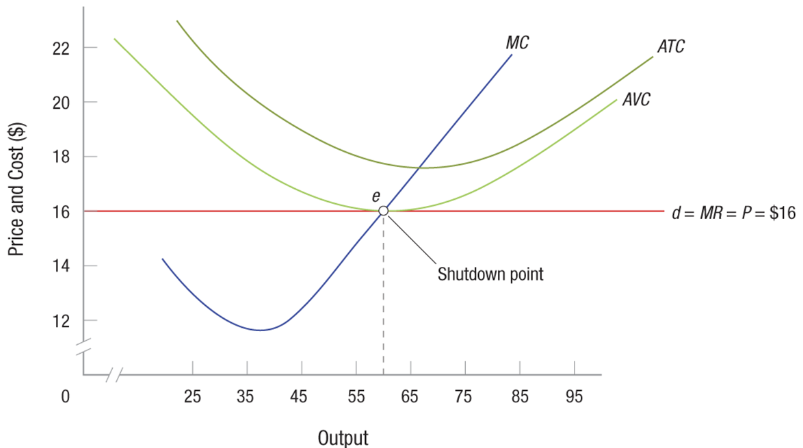

Loss Minimization

If price (P) < ATC, the firm is making a loss. However, it should continue to produce in the short run if Price (P) ≥ Average Variable Cost (AVC).

By producing where MR = MC, the firm covers all its variable costs and some of its fixed costs, thus minimizing its losses. The loss will be less than the fixed costs it would incur if it shut down.

Plant Shutdown

If price (P) < minimum AVC, the firm should shut down production in the short run.

At this point, revenue is not even covering the variable costs, and losses would exceed fixed costs if the firm continued to operate.

The greatest loss a firm is willing to endure in the short run is equal to its fixed costs.

Five-Step Process to Calculate Maximum Profit: A consistent approach applicable to all market structures

Find the output where MR = MC.

Determine the corresponding profit-maximizing quantity on the horizontal axis.

Go up to the demand curve (MR) and left to find the profit-maximizing price (which is given in perfect competition).

Go up to the ATC curve and left to find the average total cost per unit at that quantity.

Calculate profit as (Price - ATC) * Quantity, represented by the area of a rectangle.

The Short-Run Supply Curve

The portion of the firm's Marginal Cost (MC) curve that lies above the minimum point of the Average Variable Cost (AVC) curve. It shows how much the firm will supply at various prices above the shutdown point. Below the minimum AVC, the firm will supply zero output.

Perfect Competition: Long-Run Adjustments

Factors in the long run

In the long run, all factors are variable, and firms can enter or exit the industry.

Adjustment to Short-Run Economic Profit

If firms are earning short-run economic profit (P > ATC), this attracts new firms to enter the industry because there are no barriers.

Increased entry shifts the industry supply curve to the right, causing the market price to fall.

This process continues until economic profits are driven to zero (P = minimum ATC).

In the long-run equilibrium, firms earn only a normal profit.

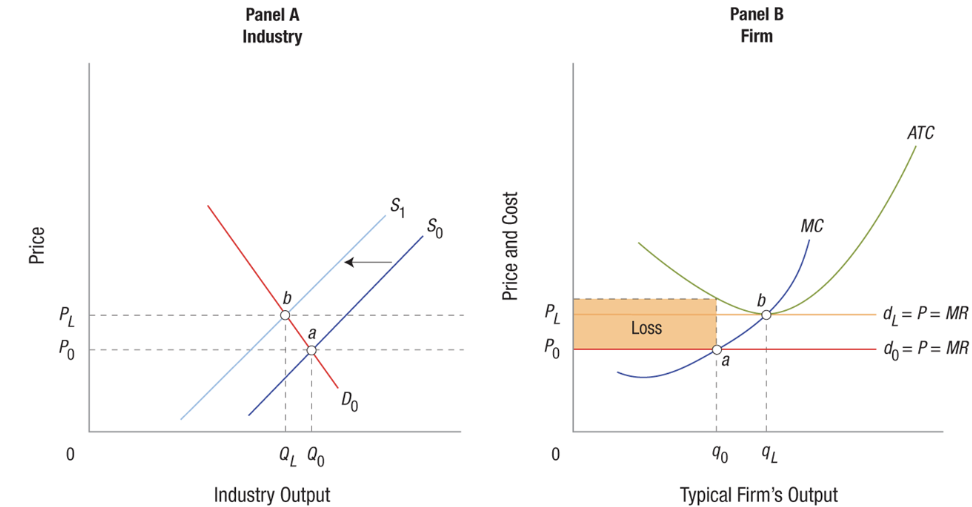

Adjustment to Short-Run Economic Losses

If firms are incurring short-run economic losses (P < ATC), some firms will exit the industry.

Decreased supply shifts the industry supply curve to the left, causing the market price to rise.

This continues until the losses are eliminated, and firms earn only a normal profit (P = minimum ATC).

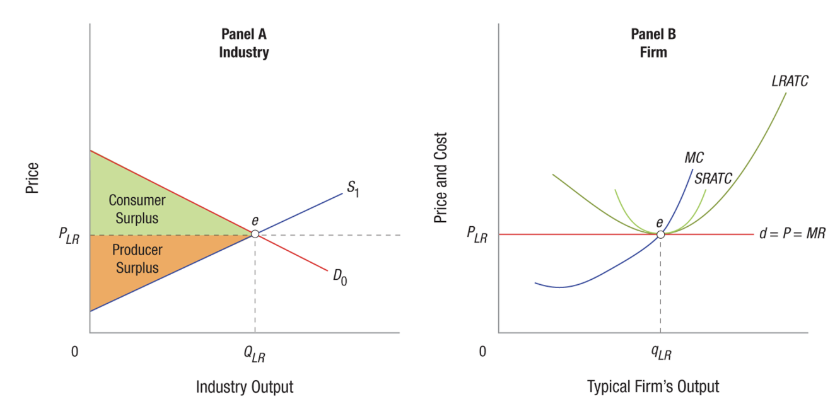

Long-Run Equilibrium

In a perfectly competitive market with free entry and exit, the long-run equilibrium occurs when price (P) equals the minimum of the long-run average total cost (LRATC) curve.

At this point, firms earn zero economic profit, and there is no incentive for entry or exit.

Elimination Principle

In the long run, profit is eliminated by firm entry, and losses are eliminated by firm exit in competitive industries with easy entry and exit.

Competition and the Public Interest

Production Efficiency

Products are produced at their lowest possible opportunity cost because, in the long run, price (P) equals the minimum LRATC.

Consumers pay no more than the minimum production costs plus a normal profit.

Allocative Efficiency

The price (P) that consumers pay is equal to the marginal cost (MC) of producing the good. This means society's resources are used to produce the exact quantity of the good desired by consumers.

Total surplus (consumer surplus + producer surplus) is maximized.

If P > MC, society would benefit from producing more.

If P < MC, resources could be better used to produce other goods.

Long-Run Industry Supply

The relationship between the price and the total quantity supplied by all firms in the industry in the long run. Its shape depends on how changes in industry output affect the prices firms pay for resources and their costs.

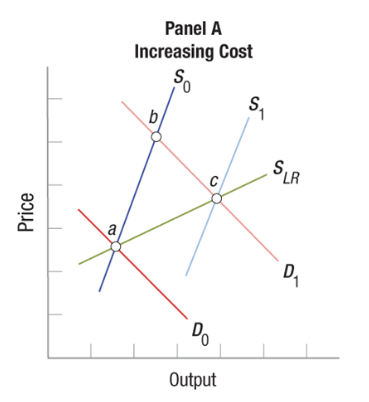

Increasing Cost Industry

An industry where the entry of new firms or the expansion of existing firms leads to an increase in the prices of inputs (e.g., raw materials, labor), causing the LRATC to shift upward and resulting in a higher long-run equilibrium price.

The long-run industry supply curve is upward sloping.

Example: Increased demand for pizza workers as more pizzerias open, leading to higher wages and pizza prices.

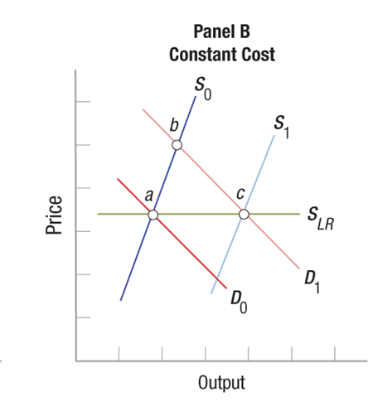

Constant Cost Industry

An industry where the entry of new firms or the expansion of existing firms has no significant impact on input prices, and the LRATC remains constant.

The long-run industry supply curve is horizontal (perfectly elastic) at the level of minimum LRATC.

Example: Some fast-food restaurants and retail stores that can easily replicate their operations without cost increases.

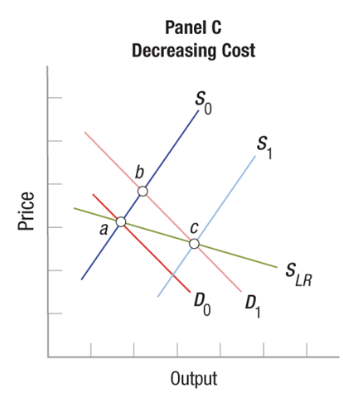

Decreasing Cost Industry

An industry where the entry of new firms or the expansion of existing firms leads to a decrease in input prices or technological advancements, causing the LRATC to shift downward and resulting in a lower long-run equilibrium price.

The long-run industry supply curve is downward sloping.

Example: The personal computer industry, where increased demand led to economies of scale in component production and technological innovation, lowering prices.

Globalization and Perfect Competition

The development of technologies like the standardized shipping container ("the box") has drastically reduced shipping costs, increasing the competitiveness of many industries and facilitating globalization. This can lead to market adjustments consistent with perfectly competitive models.

Why Do Firms Stay in Business with Zero Long-Run Economic Profit?

While they don't earn economic profit in the long run, they do earn normal profit, which is sufficient to cover the opportunity cost of their investment and labor. This keeps investors satisfied and the business viable. They are earning as much as they would in their next best alternative.

Firms Generally Do Not Seek Perfect Competition

Because in the long run, economic profit is zero. Most firms aim for some degree of market power to achieve and sustain long-run economic profit. This is why they may try to differentiate their products or create barriers to entry.