FBLA Economics Study Guide: Key Concepts and Definitions

1/59

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

60 Terms

comparative advantage

the ability to produce a good at a lower opportunity cost than another producer

absolute advantage

the producer can produce the most output/requires the least amount of inputs

tons of trade

how many units of one product would they benefit from another product

private sector

part of the economy that is run by individuals and businesses

public sector

the part of an economy that is controlled by the government.

factor payments

payments for the factors of production, namely rent, wages, interest, and profit

transfer payments

When the government redistributes income (ex: welfare, social security)

subsidies

government payments to businesses

Law of Demand

there is an inverse relationship between price and quantity demanded

substitution effect

customers switching to cheaper products as prices increases

income effect

the change in consumption resulting from a change in real income

law of diminishing marginal utility

the principle that consumers experience diminishing additional satisfaction as they consume more of a good or service during a given period of time

substitute

increase in price of one good, increases demand for another good

complements

increase in price of one good, decreases demand for other

normal goods

as income increases, demand decreases

inferior goods

as income increases, demand decreases

total revenue test

Total revenue rises with a price increase if demand is price inelastic and falls with a price increase if demand is price elastic

price ceiling

A legal maximum on the price at which a good can be sold

trade

- if we can buy something at a cheaper world price, that means that price will fall, producer surplus will get smaller, but consumer surplus will get bigger

consumer surplus

the amount a buyer is willing to pay for a good minus the amount the buyer actually pays for it

producer surplus

the amount a seller is paid for a good minus the seller's cost of providing it

Utility Maximization

The proposal that people make decisions by selecting the option that has the greatest utility.

law of diminishing marginal resources

as variable resources are added to fixed resources the additional output produced by each additional worker will eventually fall

fixed costs

Costs that do not vary with the quantity of output produced Ex: rent, insurance, Managers Salaries

variable costs

costs that vary with the quantity of output produced ex: raw materials, electricity, labor

total costs

fixed costs + variable costs

marginal cost

the cost of producing one more unit of a good

average total costs

total cost divided by the quantity of output

average variable cost

variable cost divided by the quantity of output

economies of scale

factors that cause a producer's average cost per unit to fall as output rises

Characteristics of Perfect Competition

- many small firms

- identitcal products

- low barriers: easy to enter and exit

- seller has no need to advertise

- Firms are "price takers": got to take price that is set by market

- seller has NO control of price

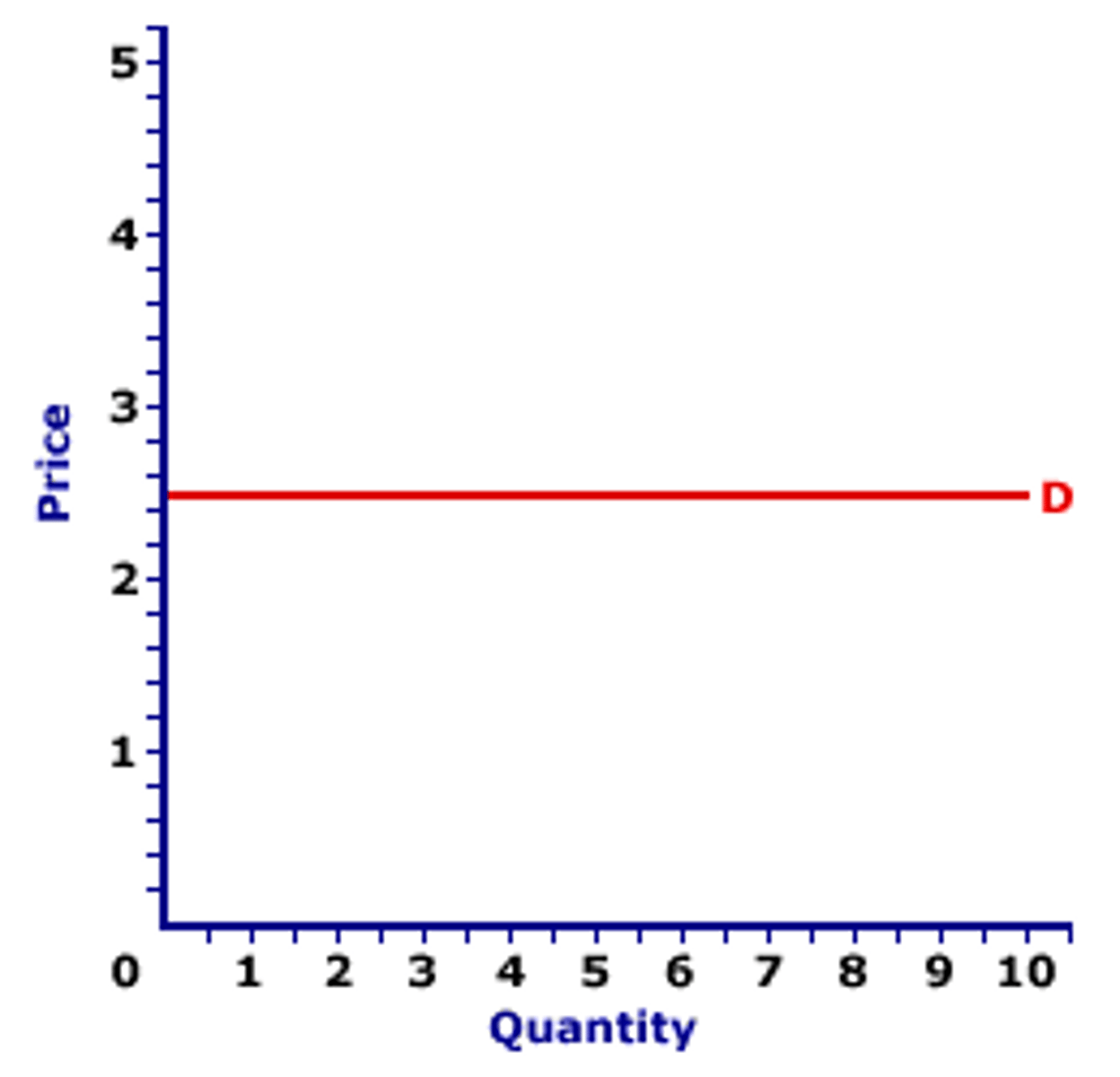

horizontal demand curve

perfectly elastic demand

Profit Maximizing Rule

MR=MC

shut down rule

a firm should shut down if the price falls below the minimum AVC

Accounting v Economic Profit

- accountants look at only explicit costs

- economists examine both explicit, and implicit costs

Perfect Competitive Firms earn zero Economic Profit and positive Accounting profit , supply shifts to right

productive efficiency

where price=min ATC, producing at lowest possible cost

allocative efficiency

producing at the amount most desired for society

price=mariginal cost

Monopoly

- one large firm

-unique product

- high barriers: firms cannot enter the industry

- price makers

- require some advertising

Natural Monopoly

a market that runs most efficiently when one large firm supplies all of the output

price discrimination

the business practice of selling the same good at different prices to different customers

Oligopoly

-A market structure in which a few large firms dominate a market

- identical or differentiated products

- high barriers to entry

- control over price(price maker)

- mutual interdependence

dominant strategy

a strategy that is best for a player in a game regardless of the strategies chosen by the other players

Nash Equilibrium

a situation in which economic actors interacting with one another each choose their best strategy given the strategies that all the other actors have chosen

monopolistic competition

- relatively large number of sellers

- differentiated products

- same control over price

- easy entry and exit

- a lot of advertising

derived demand

Business demand that ultimately comes from (derives from) the demand for consumer goods.

if the demand goes up for pizza, demand for pizza drivers will go up

minimum wage

- quantity demanded falls

- quantity supplied increases

Marginal Revenue Product

The additional revenue generated by an additional worker

MRC

the additional cost of an additional worker

Least Cost Rule

The combination of labor and capital that minimizes total costs for a given production rate. Hire L and K so that MPL / PL = MPK / PK or MPL/MPK = PL/PK

Market Failure

a situation in which the market does not distribute resources efficiently

public goods

Goods, such as clean air and clean water, that everyone must share.

shared consumption

A good or service where more than one person can simultaneously enjoy it.

non exclusion

the idea that you cannot exclude people that don't pay

negative externalities

by-products of production or consumption that impose costs on third parties

positive externalities

benefits created by a public good that are shared by the primary consumer of the good and by society more generally

dead weight loss

the reduction in economic surplus resulting from a market not being in competitive equilibrium

the lorenz curve

the curve that illustrates income distribution

progressive taxes

-takes more from rich ppl (current federal income tax system)

proportional (flat)

- takes the same amount of taxes from rich and poor (20% of income)

regressive tax

A tax for which the percentage of income paid in taxes decreases as income increases (sales tax, consumption tax)