5.5 Break-even analysis

1/47

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

48 Terms

Contribution

The sum of money that remains after all direct / variable costs have been deducted from sales revenue of a product

The surplus contributs to paing fixed costs

Contribution per unit

Difference betw selling price of a product and its variable costs of production

Aka proportion of SP per unit that goes towards paying FC

Contribution per unit formula

P - AVC

Total contribution

Surplus after all VC have been deduced from revenue, that is used to cover fixed costs

FC / unit contribution (double check)

Quantity of output needed to go towards paying off total fixed costs

Total contribution formula

(P-AVC) X Q

Aka GP for a product

Formula for contribution per unit vs added value

CPU = P - AVC

VA PU = P - ATC

What is used to pay a firms fixed costs?

Positive difference betw SP - AVC

Profit

Positive difference betw TR - TC

On BE chart: all levels of output beyond BEQ

Profit formula

Total contribution - TFC

TR - total costs

Simple- how to increase profit?

Increase revenue (via sales volume or price) → raises total contribution

Reduce VC

Reduce FC

Break-even analysis

Quantitative decision making-tool

Used to calc the level of sales needed to cover all COP

Any sales beyond BEP generate a positive safety margin, hence profit for the business

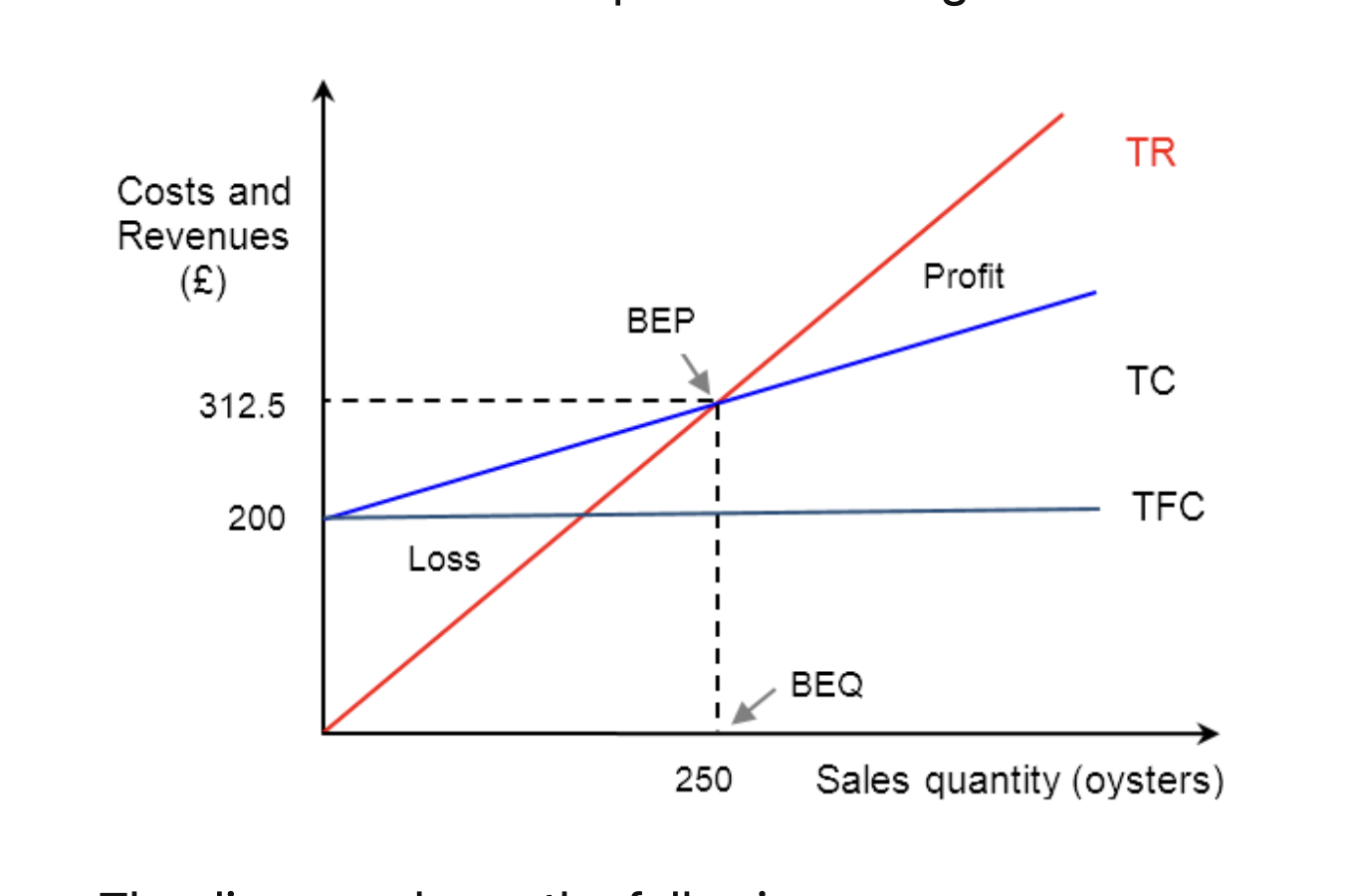

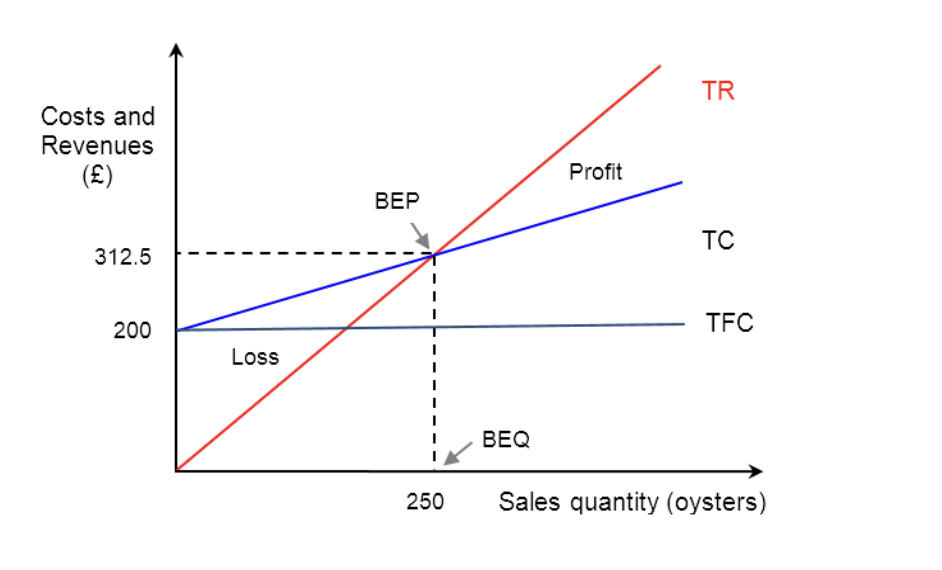

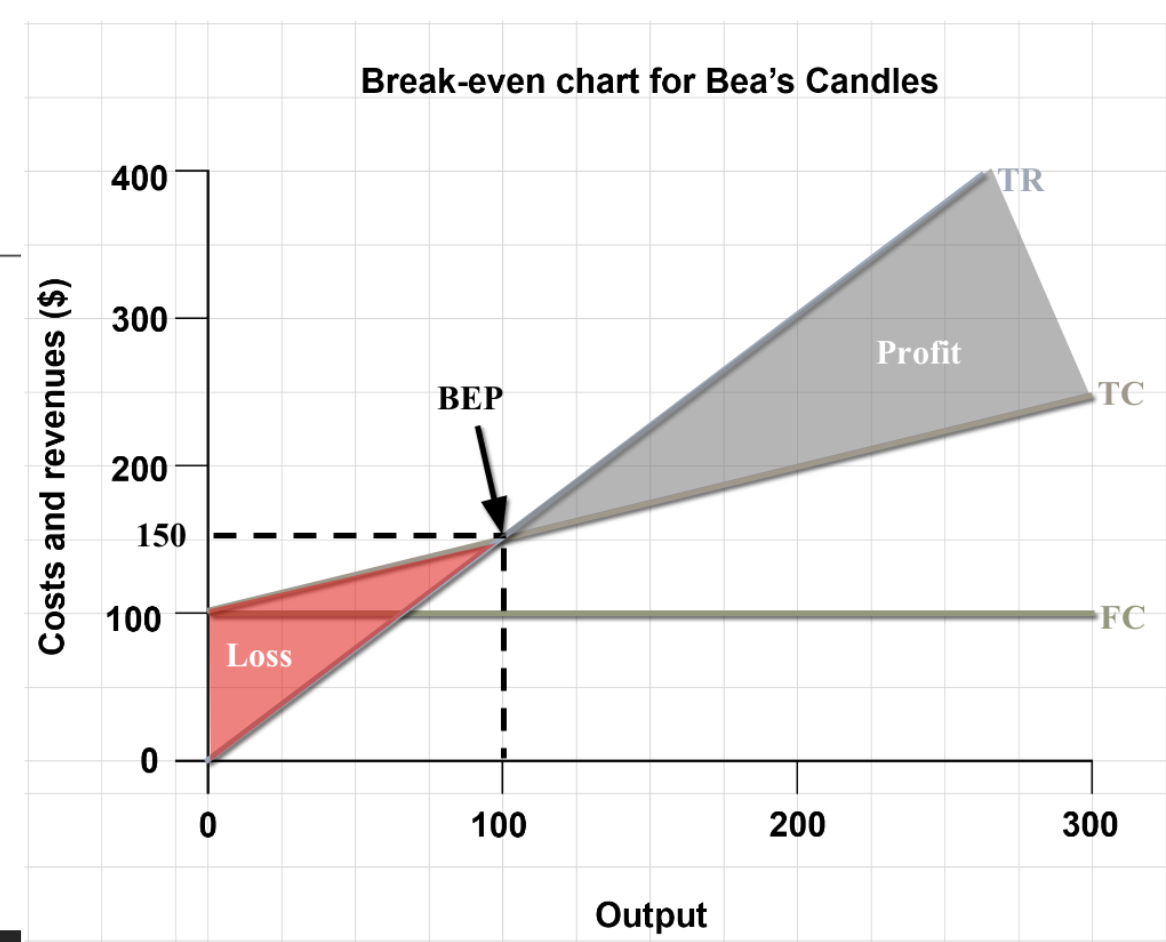

Break-even chart

Represents firms costs, revenues, profits (or loss) at various levels of output

3 diff financial situations a firm can be in (relating to BE)

Loss- TC > TR

Break-even- TR = TC

Profit- TR > TC

Purpose of contribution analysis

Determine pricing strategies

Prioritise products in their portfolio

Decide whether to make / buy in products

Perform BE analysis

Break even

When a firm’s sales revenues cover all of its production costs

When a firm makes neither a profit nor a loss

TR = TC

Break-even point

Position of BE chart where TC line intersects TR line

TR = TC

Break-even quantity

Sales vol needed for a firm to reach

BEQ = FC / (P – AVC)

What does BE analysis inform managers?

hether a product is financially worthwhile to produce.

How much profit can be earned if the business idea goes to plan.

3 methods to determine BE point

Unit contribution method

TR = TC method

Draw + interpret BE chart

Unit contribution method to calculate BE point

BEQ = TFC / contribution per unit

TR = TC method to calculate BE point

Work out TR and TC

Equate them

Sub in values

Solve for Q

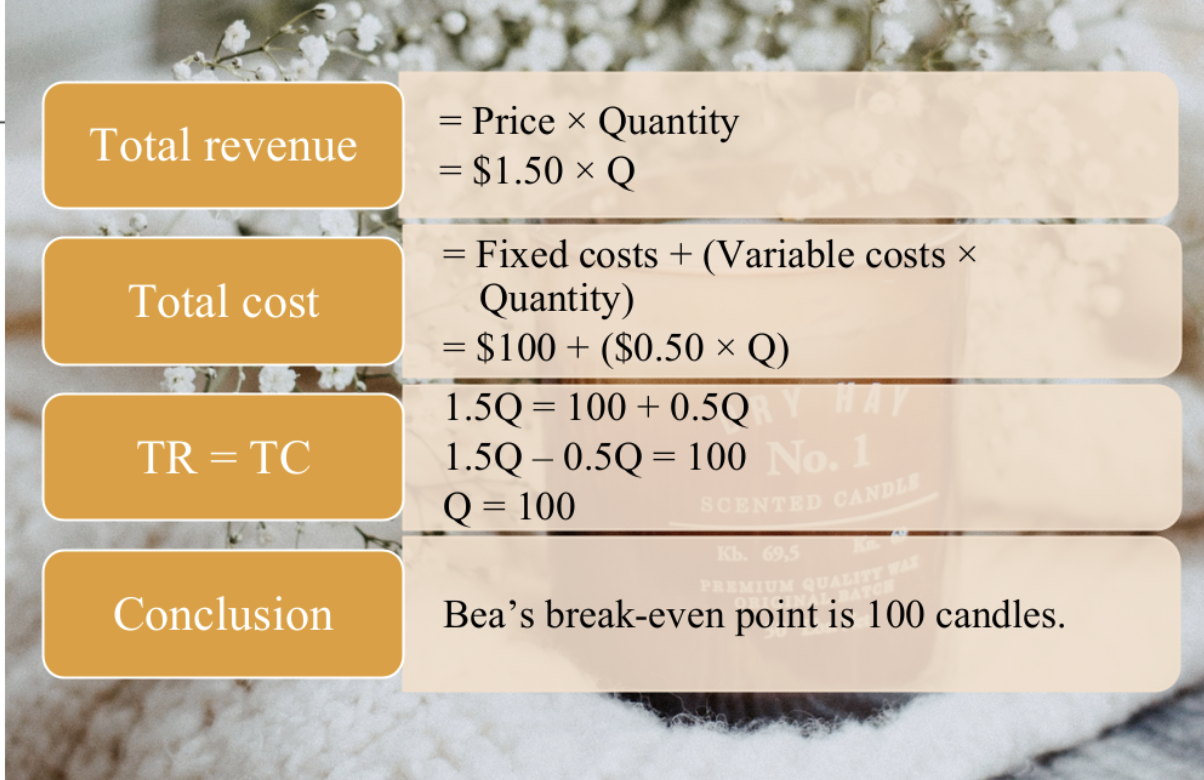

TR = TC

P x Q = TFC + TVC

30Q = 3500 + 10Q

20Q = 3500

BEQ = 175 jeans

BE chart method to calculate BE point

Draw BEC

Level of output on x axis at BEP

Loss

When firms TC > TR

At all levels of output below BEQ

Break even chart

Which businesses is BE analysis especially useful for?

Business that:

Produce / sell 1, standardized product

Operate in 1 market

Make products to order → all output sold

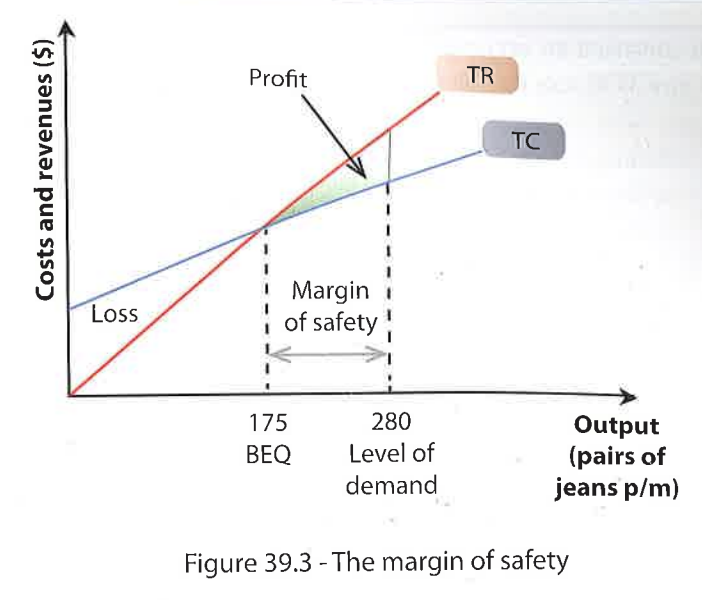

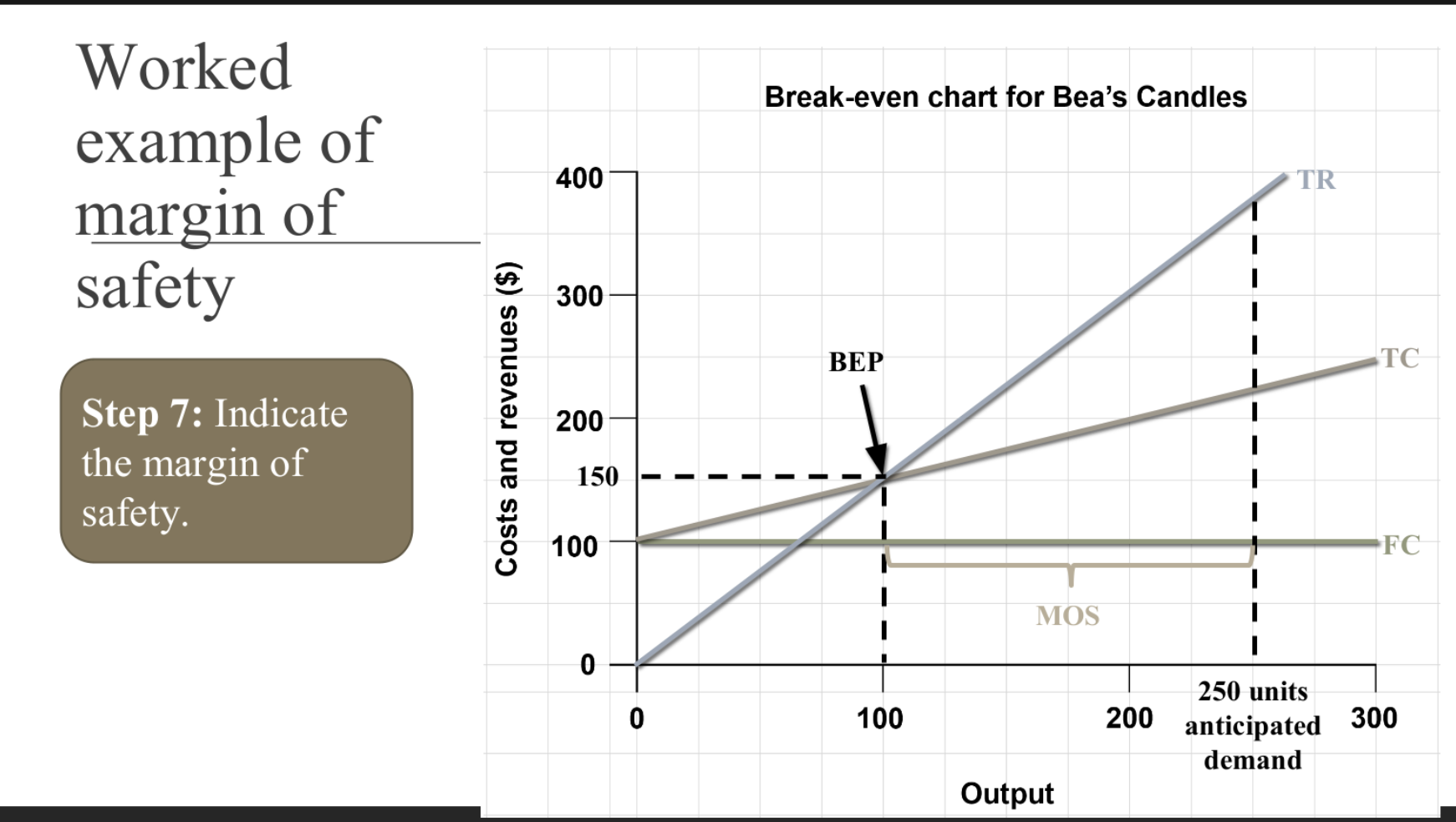

Margin of safety (MOS)

Numerical difference betw firms actual sales quantity and its BE quantity

Positive MOS → firms can reduce output by that amt w/o making a loss

V high positive MOS → reduce risk if adverse conditions

Margin of safety formula

Actual sales quantity - BE quantity

MOS units

The unit of output (ie jeans)

NOT monetary

How to draw a BE chart?

Optional- draw TFC line (horizontal)

Draw TC line (starts at same level as TFC)

Draw TR line (starts at 0)

Label x axis- output (rings per month)

Label y axis- costs AND revenue (give specific currency)

Title

What happens if BE quantity is a decimal?

Always round up

Target profit

Amt of profit (surplus) a firm intends to achieve, in a given time period

Expected SR = TC

Target profit output

The quantity of sales required to reach the firm’s target profit

Target profit output formula

(FC + Target profit) / contribution per unit

How to manually work out target profit output?

Target profit = TR - TC

Target profit = (target price x Q) - TFC - TVC

Solve for Q

Target price

Price set by a firm in order to reach BE Q or certain target profit

Amt customers need to pay per unit, in order for firm to BE or reach target profit

BE revenue

Value of the output needed to break-even

When does a firm generate a profit / loss on BE chart?

Profit- output beyond BEP

Loss- output below BEP

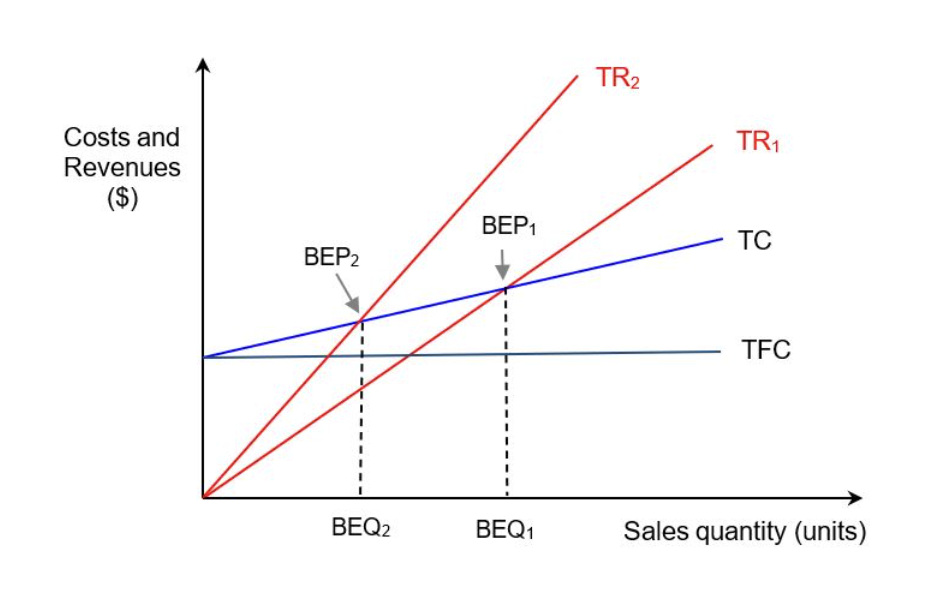

Effect of increase in selling price on firms BE quantity + on chart

Reduces firms BEQ

Greater gradient (steeper) of TR line (1 → 2)

Effect of higher selling price on MOS

Increases MOS (because the firm BEs earlier)

Assumption: inelastic demand

Whether a higher price generates a greater or smaller MOS, depends on what?

PED

Effect of higher cost of production on firms BE quantity + on chart

Increase BEQ

If VC increase → TC line is steeper

If FC increase → TC line shifted upwards

Summary: effect of increase in price on BEQ, profit, MOS

BEQ decreases

Profit increases

MOS increases

Summary: effect of increase in cost on BEQ, profit, MOS

BEQ increases

Profit decreases

MOS decreases

What formulas to use to quantitatively show effect of change in price and cost on BE

BE = FC / CPU

CPU = SP - AVC

Why are actual BE, profits / losses, MOS going to be diff from the predicted ones in BE analysis? (not in spec)

Non price determinants of demand → affects BEQ → affects MOS

fashion tastes change → demand ↑ → profit ↑, MOS ↑, BEQ reached sooner

Innovation / new tech → demand ↑ → revenue ↑ → profit ↑, MOS ↑, BEQ reached faster

ST vs LT pricing

SR- low price to attract customers: contribution ↓ → BEQ ↑, profit ↓, MOS ↓

LR- opposite (once customers are loyal)

External factors (costs, interest, exchange rates)

Increase costs → decrease contribution → BEQ ↑, profit ↓, MOS ↓

Risk level

High risk project → high FC → BEQ ↑, MOS ↓ (but potential profit ↑ if successful)

Assumptions of BE analysis / charts

Costs are constant (linear)

Sales revenue is constant (linear)

All output will be sold

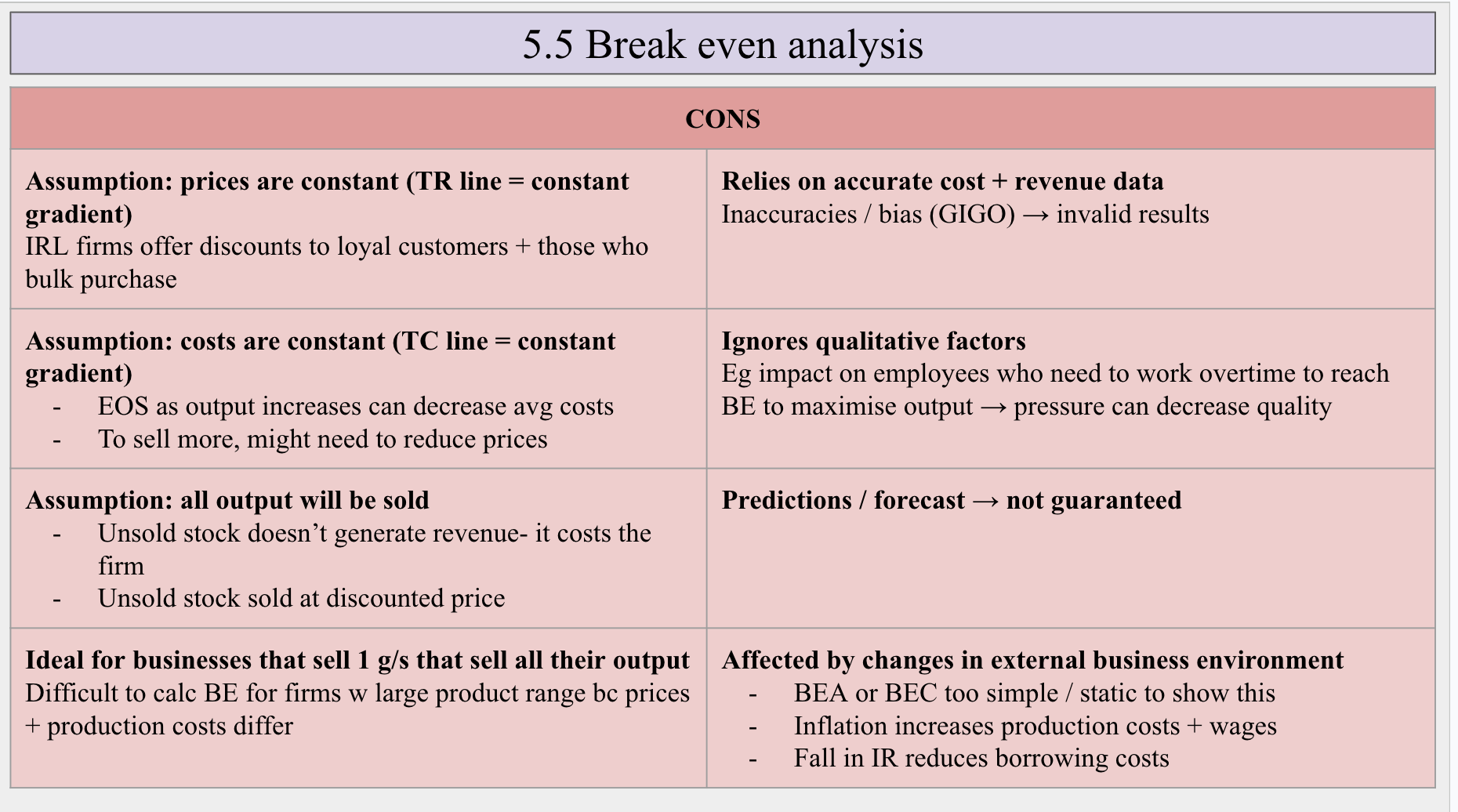

Cons of BE analysis

Assumption: prices are constant (TR line = constant gradient)

Assumption: costs are constant (TC line = constant gradient)

Affected by changes in external business environment

Ideal for businesses that sell 1 g/s that sell all their output

Relies on accurate cost + revenue data

Predictions / forecast → not guaranteed

Ignores qualitative factors

Assumption: all output will be sold

Pros of BE analysis as a planning + decision making tool

Product portfolio management

Helps to assess the expected BEQ prior to the launch of a new product.

Risk assessment

By calc MOS

Helps w make or buy decisions (CTM vs CTB)

Helps w special order decisions

If a one-off orderi s worth accepting