Standard Costing and Variance Analysis

1/14

Earn XP

Description and Tags

Flashcards for vocabulary related to standard costing.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

15 Terms

Standard Costing

A system of accounting based on predetermined costs and revenue per unit.

Variances

Differences between standard and actual costs

Variance Analysis

The process of analysing differences between actual and standard costs.

Ideal Standards

What should be achieved if there is no wastage or loss and the whole production process functions perfectly.

Basic Standard

A standard that was set some time ago and has not been updated.

Variances

Difference between a planned, budgeted or standard cost and the actual cost incurred.

Favourable Variances

Occur when actual results are better than expected, thereby producing higher than expected profits.

Adverse Variances

Occur when actual results are worse than expected, which leads to producing lower than expected profits.

Material Price Variance

(Actual cost per unit –standard cost per unit) * actual quantity

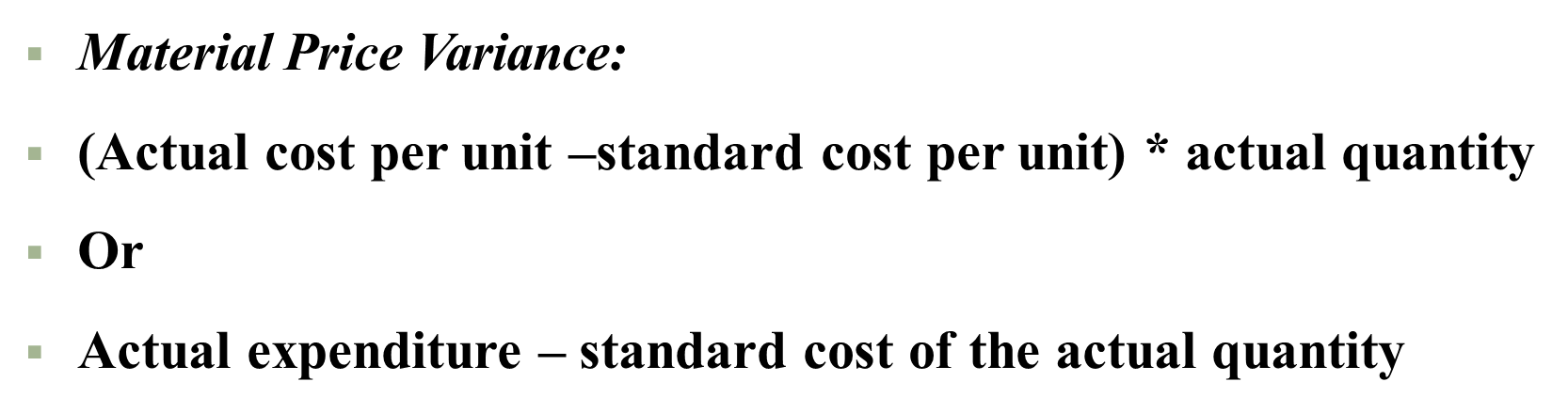

§Material Price Variance:

§(Actual cost per unit –standard cost per unit) * actual quantity

§Or

§Actual expenditure – standard cost of the actual quantity

§Material Usage Variance:

§(Actual quantity –standard quantity produced) * standard cost

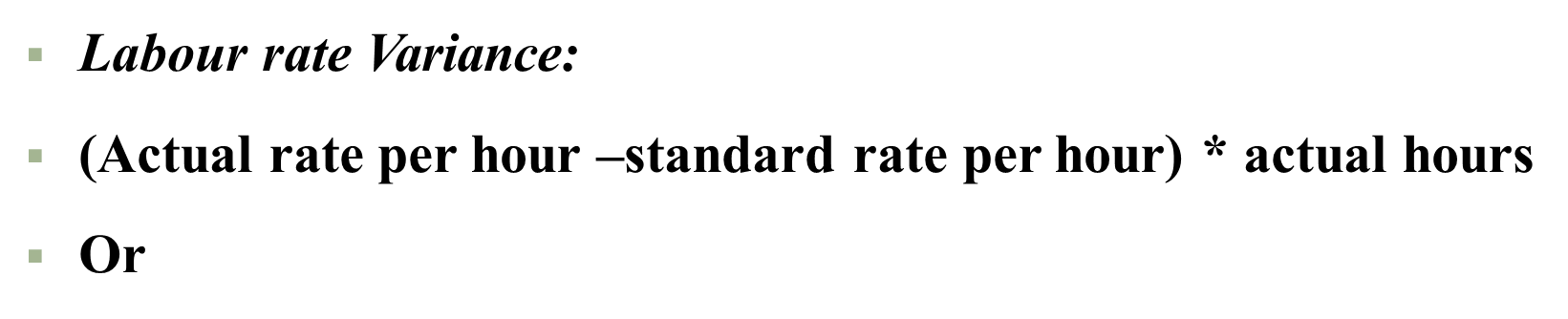

§Labour rate Variance:

§(Actual rate per hour –standard rate per hour) * actual hours

§Or

§Labour efficiency Variance:

§(Actual hours –standard hours for actual production) * std rate/hour

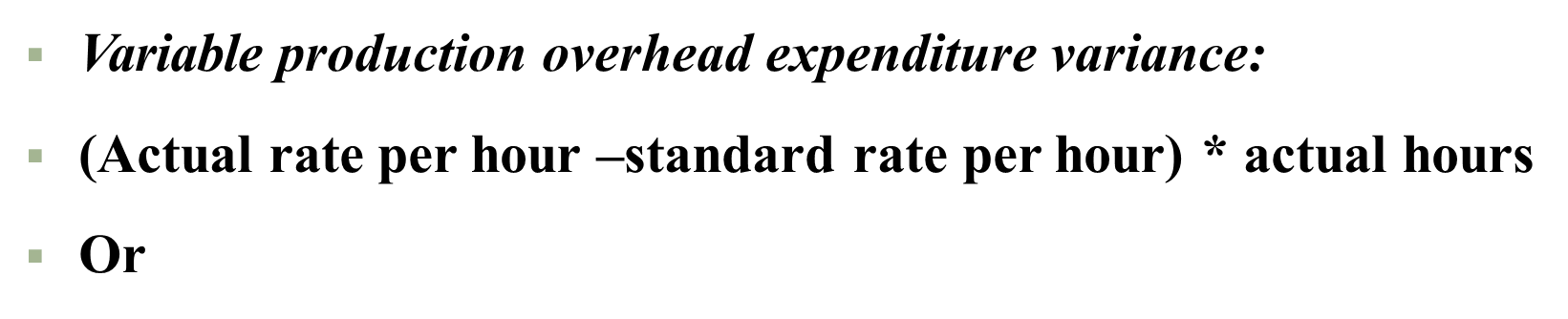

§Variable production overhead expenditure variance:

§(Actual rate per hour –standard rate per hour) * actual hours

§Or

§Variable production overhead efficiency Variance:

§(Actual hours –standard hours for actual production) * std rate/hour