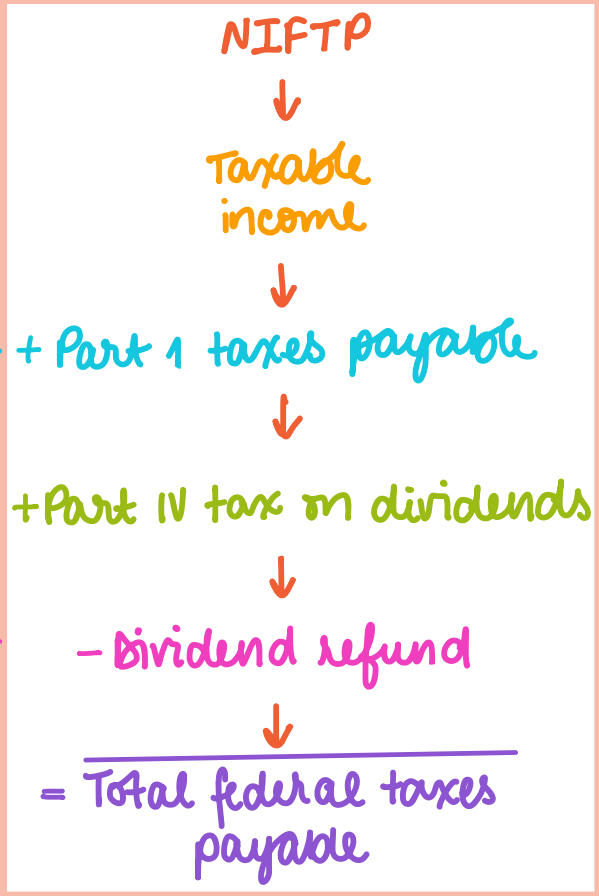

Corporate Taxes Payable - Steps

Corporate Tax Calculations Rates

Part I

Business income - Public company/large CCPC —> 15%

Business income - small CCPC (<500k) —> 9%

Investment income —> 38.67%

Part IV

Dividends from non-connected CDN companies —>38.33%

Dividends from connected CDN companies —> % ownership x dividend refund by corporation

Class 1

Buildings

4% for residential

6% for non residential

10% for manufacturing

Class 8

Machinery, equipment, furniture

20%

Class 10

Vehicles

30%

Class 10.1

Luxury vehicles

30% limit to prescribed amount

Class 12

Computer software (NOT systems software), uniforms, tools <$500

100%

Class 13

Leasehold Improvements

Max CCA - Lesser of:

1/5 of capital cost

Capital cost of leasehold improvement/lease term remaining + one renewal option

Class 14

Definite Life Intangibles (patents, franchises, concessions, licenses)

Straight line over legal life

Class 14.1

Goodwill and Indefinite life Intangibles (incorporation costs, customer lists)

5%

Class 16

Taxis, vehicles used in daily car rental business

40%

Class 17

Roads, Parking Lots, other surface constructions

8%

Class 29

Machinery and equipment purchased between 2007-2016

Class 44

Patents

25%

Class 50

Computer hardware (computers, laptops, smartphones) and systems software

55%

Class 53

Manufacturing Equipment

50%

Class 54

Zero Emission Vehicles

30%

Advantages of Incorporation

Potential for income splitting

Limited liability

Lifetime capital gains deduction

Estate planning

Flexibility as to how/when the income is distributed

Disadvantages of Incorporation

Cannot use business losses against other types of income for the individual

Maintenance costs (ex. Incorporation/filling fees)

Not eligible for tax credits & charitable donations available to individuals

Cost of winding up corporation

Double taxation

Advantages of Salaries

RRSP contributions: RRSP contribution limit is based on earned income. Earned income includes income from salaries but NOT dividends.

Child care costs: similar to RRSP, child care expense deduction is calculated based on earned income.

CPP/Canada Employment Credits: these tax credits are only available if an individual receives a salary.

A salary will be deductible to the corporation, as opposed to a dividend which is paid out of after-tax income.

Disadvantages of salaries

Income splitting: paying dividends offers the opportunity to split income if some shares are held by family members. In order to pay a salary to a family member, they need to be employed in the company

CPP and EI contributions: when a salary is paid, CPP and EI contributions must be made, by both the employee and employer. The same could apply for certain provinces with additional payroll taxes.

Instalments?

If large balance owing in two consecutive years, must start making instalment payments (quarterly).

If instalments are not paid —> interest and penalties

Who is eligible to claim the LCGE deduction?

Any resident of Canada

What gains are eligible for the LCGE deduction?

Gains from disposition of qualified property (QSBC shares)

Requirements for Qualified Small Business Corporation (QSBC)

The corporation must be a CCPC

90% of assets invested in active business carried on in Canada on the day of sale

50% of assets invested in active business carried on in Canada throughout 24 months

Shares must have been held for 24 months

Requirements for a CCPC

Private company, incorporated & resident in Canada

Cannot be controlled by a public corporation or by non-residents

CCPC shares cannot be listed on a designated stock exchange in Canada or certain designated foreign stock exchanges

How much is the LCGE deduction?

1,016,863 (limit at 50%, so 508,431)

How do you claim the LCGE?

Need to calculate the gain from disposition and fill out the form T657