CHAPTER 2: Process of Assurance - Obtaining an Engagement

1/27

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

28 Terms

Advertising for Clients

certain professional guidelines exist for accountants that which to advertise

Accountants and Tendering

tendering - when the client requests a presentation on why they should work with them

Accepting an Engagement

the auditors must undertake to ensure that their appointment is valid and that they are clear to act.

Audit Acceptance Procedures

Ensure they are professionally qualified to act

Ensure existing resources adequate

Obtain references

Communicate with present auditors

Consider the integrity of those managing the company.

Procedures: Professionally qualified to act

consider whether it should be disqualified on legal or ethical grounds e.g. conflict of interest

Procedures: Existing resources are adequate

consider the available time, staff and technical expertise

Procedures: obtain references

make independent enquiries if directors are unknown

Procedures: communicate with present auditors

enquire whether there are reasons behind the change which the new auditors should know

Procedures: consider the integrity of those managing the company

management could mislead the auditor into giving the wrong opinion

Risk of Firm

the audit firm will also consider whether the client is high/low risk

high risk = more time spent and more experienced staff

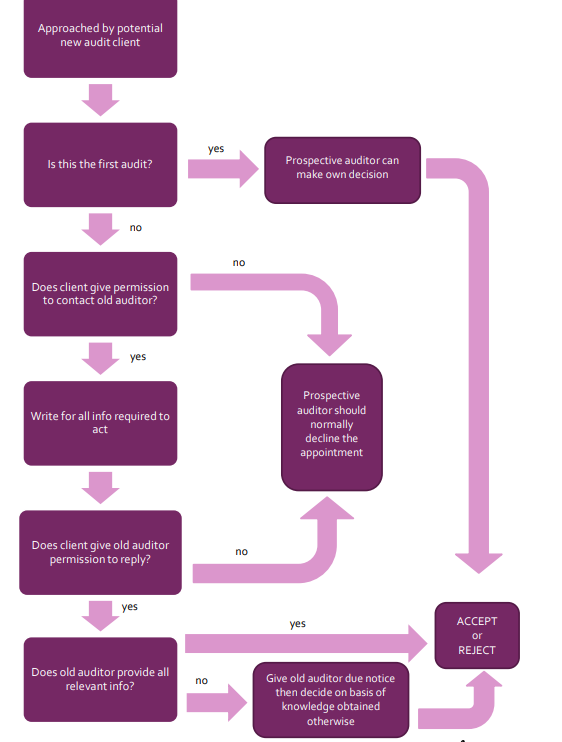

Contacting Previous Auditors

Auditors should seek prospective clients’ permission before engaging with the previous auditor.

If they refuse, this is a red flag and they should decline the proposal.

Appointment Decision Chart

After Acceptance

Ensure the outgoing auditors’ removal should be properly conducted in accordance with the national legislation

Ensure that the appointments is valid

Submit a letter of engagement

Do Money Laundering Checks

Money Laundering Regulations

Assurance firms must keep documents about clients and undertake client due diligence

When it is mandatory for identity checks on clients:

when an ongoing relationship is envisaged

when a one-off transaction greater than £15,000 will take place.

Identification Checks on Individuals

Photograph

Full name

Permanent Address

e.g. passport and utility bill

Identification Checks for Companies

Certificate of Incorporation

Registered Address

Confirmation Statement (Annual Return) for Directors and Shareholders

Previous Financial Statements

ISA 210 - Agreeing the Terms of Audit Engagements

requires that the auditor and the client agree on the terms of the engagement letter.

Features of an Engagement Letter

MCSOOAR

MCSOOAR

Management Responsibility

Confirmation of Audit

Scope of the Audit

Objective of the Audit

Opinion

Audit Responsibility

Report

MCSOOAR - Management Responsibility

to prepare the financial statements and to provide the auditor to unrestricted access to whatever records, documentation that is required

MCSOOAR - Confirmation of Audit

the confirmation of the audit’s output and form of any report

MCSOOAR - Scope of the Audit

the scope of the audit, could include reference to the applicable legislation and regulations.

MCSOOAR - Objective of the Audit

the objective of the financial statements

MCSOOAR - Opinion

the auditor’s opinion

MCSOOAR - Audit Responsibility

the auditor’s responsibilities and their duties

MCSOOAR - Report

report to be included

Potential points to be included:

arrangements regarding the planning of the audit

expectation of receiving from management written confirmation of representations made in connection with the audit

basis on which fees are computed and any billing arrangements

arrangements concerning and the involvement of other auditors and experts in some aspects of the audit

arrangements concerning the involvement of internal auditors