economic AOS 2 sac 2

1/61

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

62 Terms

market

a place where buyers and sellers come together to exchange goods and services for money

demand

buyers have a willingness to purchase a product

supply

sellers willingness to produce a product

price

the rate of exchange

to understand the relationship between demand and supply, economists have created a concept called

perfectly competitive market to demonstrate a “pure market” economy

characteristic of a Perfectly Competitive Market

1st characteristic: There are many buyers and sellers which causes lots of competition

2nd characteristic: No barriers to entry or exit for suppliers which means it’s easy to reallocate resources

3rd characteristic: Identical product

Perfectly Competitive Market

1st characteristic: There are many buyers and sellers which causes lots of competition

this means that no one company or buyer can set the price of something

Perfectly Competitive Market

2nd characteristic: No barriers to entry or exit for suppliers which means it’s easy to reallocate resources

if firms are making high profit, new businesses can enter the market

if firms are making losses, businesses can leave the market

This movement helps maintain strong competition over time

Perfectly Competitive Market

3rd characteristic: Identical product

all firms sell identical or very similar goods and services

consumers see no difference between products from different sellers

because the goods are identical, firms must compete on price, not quality or branding

perfectly competitive markets characteristics

sellers try to maximize profit

producers surplus occurs when producers sell something for more than the market price

Buyers try to maximize their utility (satisfaction)

consumers surplus occurs when a buyer can purchase something for less than the maximum they are willing to pay for it

not much government intervention

if the government intervention it changes the pricing and how resources are allocated

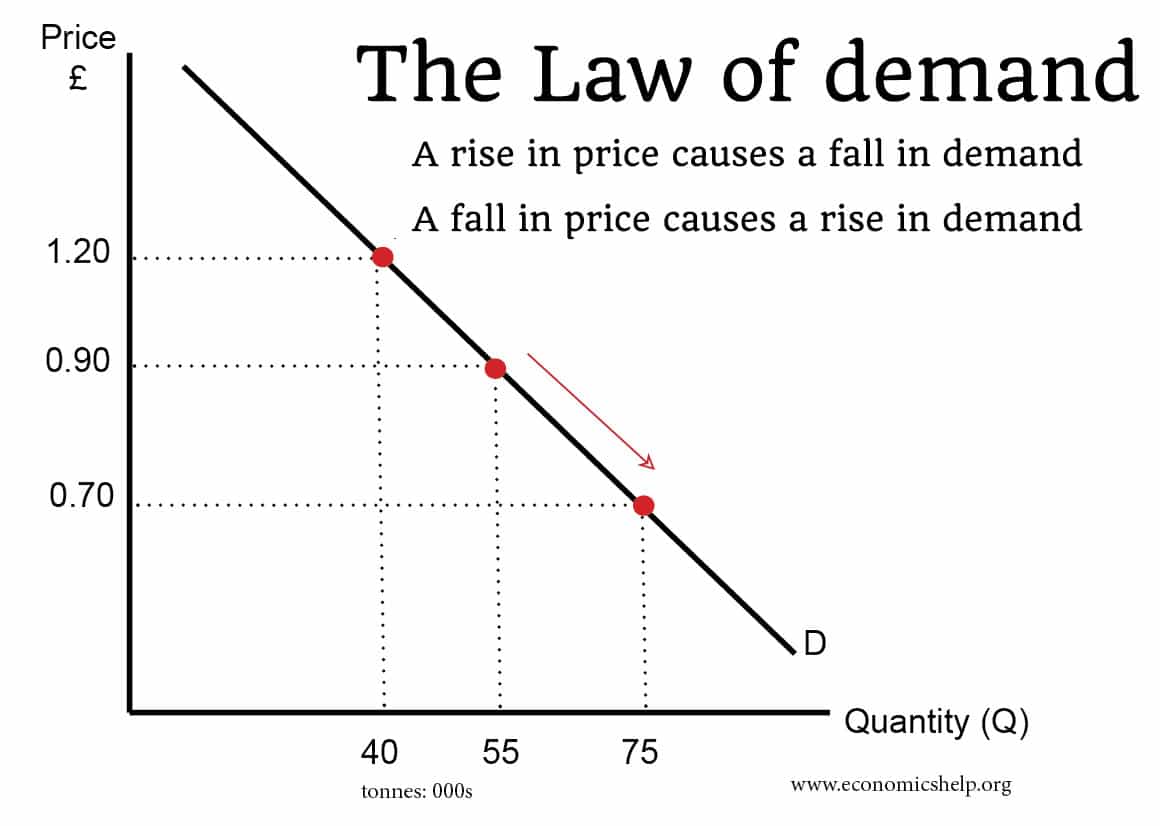

The theory of the law of demand

as the Price (P) of a product decrease, the Quantity Demanded (Qd) for that product increases

As the Price (P) increase, The Quantity Demanded (Qd) decreases

Quantity Demanded is how much a good of people are willing and able to buy at a certain price

some exceptions to this rule (i.e luxury goods) which is why we call it a theory

Graph the law of demand

upward slope area is contraction

downward slope area is expansion

The Demand Curve

a graphical representation of the theory of the Law of Demand

downward slopping

moving up the demand curve is called contraction (people demand less) and moving down the demand curve is an expansion (people demand more)

Th Income Effect

assumes we have a fixed level of (disposable) income

as the prince of a good increase we have less income to afford it. (vice versa) therefore as the price rises the Qd decreases

example: The price of Matcha decreases, now it won’t take up as much of my income to buy so I can buy more matcha

The Substitution Effect

as the price rises consumer will ‘substitute’ away other more (relatively) affordable goods

and vice versa

example: If matcha becomes less expensive then people who normally buy coffee may switch to matcha as a substitute for coffee

Non-price factors that SHIFT the demand curve

if the price of a product changes, it will cause an expansion or contraction

non-price factors shift the whole demand curve e.g ‘affect the position’

they will increase or decrease quantity demanded (Qd) at each and every price

if Demand shifted to the left it would decrease in Demand

Non-price FACTORS that SHIFT the demand curve

Changes in Disposable Income

The price of substitute goods and services

The price of complementary goods and services

Consumer preferences and tastes

Interest Rates

Population Demographics

Consumer Confidence

changes in disposable income

Disposable income is the money earned from wages and transfers (like centrelink payments) minus taxes paid

Increase in disposable income =

Decrease in disposable increase =

Demand shifts to the right (increase)

Demand shifts to the left (decrease)

Changes in the price of complementary products

Complementary products are sold separately but consumed together.

Increase in price of complement =

Decrease in price of complement =

Demand shifts left (decreases)

Demand shifts right (increases)

Changes in the price of substitute products

Substitutes are different goods and services which satisfy the same needs and wants.

Increase in price of a substitute =

Decrease in the price of a substitute =

Demand shifts right (increases)

Demand shifts left (decreases)

Changes to preferences and tastes

Consumers preferences and tastes are constantly changing

When they do, so does the demand for certain goods and services

When consumers want something more =

When they don’t =

Demand shifts right (Increases)

Demand shifts left (Decreases)

Changes in population

Change in population or demographics will change demand for certain goods or services

Increase in population/ population demographic =

Decrease in population =

Demand shifts right (increases)

Demand shifts left (decreases)

Changes in interest rates

Interest rates = cost of borrowing and reward for saving (e.g. 4%)

An increase interest rates =

A decrease in interest rates =

Demand shifts left (decreases)

Demand shifts right (increases)

Consumer confidence (sentiment)

An index that measures how consumers feel about the future state of the economy, their household finances and how likely they are to make a major household purchase

An increase in confidence =

A decrease in confidence =

Demand shifts right (increases)

Demand shifts left (decreases)

The Theory of the Law of Supply

As the Price (P) of a product increases, Quantity Supplied (Qs) increases

As the Price (P) of a product decreases, Quantity Supplied (Qs) decreases

Quantity Supplied is

how much of a good or service producers are willing and able to make at a given price

The Supply Curve

The Supply Curve is a graphical representation of the Law of Supply

It is upward sloping because Suppliers are profit motivated

An increase in quantity supplied because of price

A decrease in quantity supplied because of price

is an expansion

is a contraction

Non-Price Factors that Shift Supply Left and Right

Cost of production

Exchange Rates

Technological change

Productivity growth

Climatic conditions

Government intervention

Disruptions in the world economy – Such as the war in the Middle East

If any of the Factors of Production increase, then it is more

expensive to make Goods and Services and will Shift Supply to the Left

Cost of factors of production (natural, labour and capital) will influence

the price that the producer is willing to accept for their G/S.

Shortages of inputs (eg. fruits/vegetables used as inputs in markets such as fast food)

the exchange rate and other factors can affect cost.

An increase in the cost of production will likely

decrease supply as firms as less willing to produce the good due to reduced profit opportunities.

The Exchange Rate

is the price of one currency in terms of another, determining how much of one currency is needed to purchase another

If the Exchange Rate is high like AUD to USD, then the

cost of production increase because imports are now more expensive

If the Exchange Rate is low like AUD to Indonesian Rupiah then imports

are cheaper and cost of production is cheaper

Technological Change

New technology tends to improve efficiency/productivity in production.

Remember that productivity measures input relative to output.

An increase in productivity will increase output per unit of input.

Technology makes both labour and capital more efficient

Productivity Change

Productivity is measured as input per unit of output.

Types of productivity:

Labour productivity (output per hour worked)

Capital productivity (output per capital input used)

Multi-factor productivity - a combination of labour and capital productivity.

Innovative work practices, labour market reform and technology can all increase productivity, leading to an increase in S.

Climatic Conditions and External Shocks

Favorable Climatic Conditions will cause Supply to increase because there is an increase in Natural Resources

Bad climatic conditions will cause supply to decrease because there is a decrease in natural resources

Global events like War, Pandemics, and Global Economic recessions can also impact suppliers ability to provide because their access to resources will decrease

Government Interventions

Policies such as laws, taxation reform and changes to subsidies can impact the ability and/or willingness of a business to produce.

New Law saying minimum wage is increased, would make the cost of labour more expensive and decrease supply

price mechanism

the price mechanism is the system that determines how scarce resources are allocated to the production of goods and services in the Australian economy

features of price mechanism

changes in non-price factors that would shift the S or D curve

this causes a shortage/surplus

relative prices is likely to change

as firms motivated by profit, resources allocated into production of G/S with higher relative price

relative prices

a relative price is the piece of one good or service compared to another

changes in relative prices can how

resources are allocated to particular markets

Businesses will allocate more natural, capital and labour resources towards

markets experiencing a shortage where the relative price is higher as they are motivated by prices

Businesses will allocate natural, capital and labour resources away

from markets experiencing a surplus where the relative price is lower

what is resource allocation?

In Australia, free markets (without government intervention) operates with the force of supply and demand determining prices

changes in supply and demand factors (eg. income. taxes, climate conditions, productivity) can

shift the curves and causes shortage/surpluses and result in changes in price

Businesses will allocate scarce natural, labour and capital resources to markets with the highest

relative price (ie. price of one good compared to another) due to the profit motive

equilibrium

a point in a market where quantity demanded is equal to quantity supplied the market the market is cleared of any shortage or surplus

EQUILibirum is like equal, finding the point where the supply equals demand

moving away from Equilibrium

anything that causes EITHER Supply or Demand to change will cause disequilibrium

Disequilibrium when Supply and Demand are not equal

shortage

when Price is too low and Qd > Qs

surplus

when Price is too high and Qd < Qs

Disequilibrium in Markets when price too low = shortage

if Demand shifts to the right, then they market will experience a shortage

a shortage occurs when quantity demanded exceeds quantity supplied

a shortage implies the market price is too low

The Shortage will only go away when

prices increase causing a contraction along the demand curve to the new equilibrium point