FINS3616 International Business Finance

1/96

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

97 Terms

Globalised Economy

Financial investments abroad are on the rise as:

Diversification needs

Chasing higher returns in more mature markets

Ease of access (rise of ETFs, app brokers etc)

World economy also becoming more globalised:

MNCs dominate our environment

International production

Import of intermediate goods

Export of the final product

Even domestic firms will have significant international components

Rise of MNCs

The raw material seekers go abroad to explore raw materials

multinational oil and mining companies (BHP, Exxon)

The market seekers go overseas to produce and sell in foreign markets

Unilever, Proctor&Gamble, Nestle, Maccas, Coke

The cost minimisers invest in lower cost production or production technologies overseas to remain cost competitive

Apple, SHEIN, Uniqlo, H&M, Zara (Countries like India, Bangladesh, China, etc)

The knowledge seekers enter foreign markets to gain information

Production processes in terms of technology, foreign innovation

The domestic customer followers try to deliver services to customers abroad

banks, law, consulting firms that set foreign practices following their MNC clients (KPMG, PwC, Deloitte)

Financial market imperfection exploiters reduce taxes and benefit from diversification

American companies relocating their corporate HQ to ireland due to tax benefits

BHP moving HQ to SGP

International Markets

Classified by asset class

Stocks

Bonds

Currencies

Derivatives

Many more but not covered in course

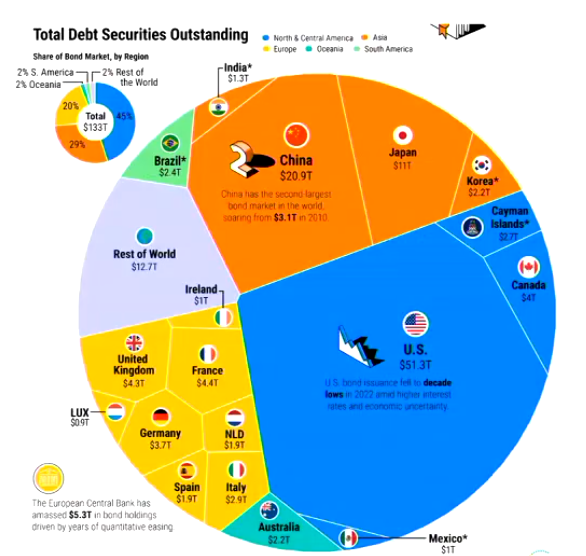

Bond Market

The bond market is as large as the stock market

International bonds: US$32 Trillion

Domestic bonds: US$101 Trillion (US?)

By sector

Governments: US$60 Trillion

Financial institutions: US$42 Trillion

Non-financial corporations: US$17 Trillion

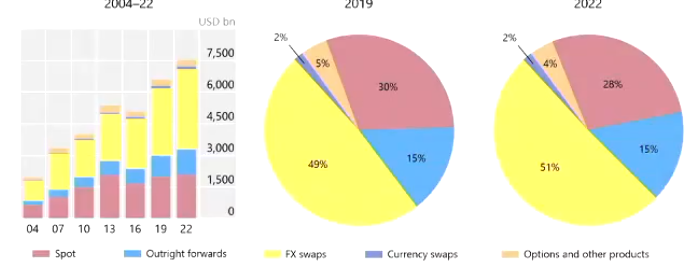

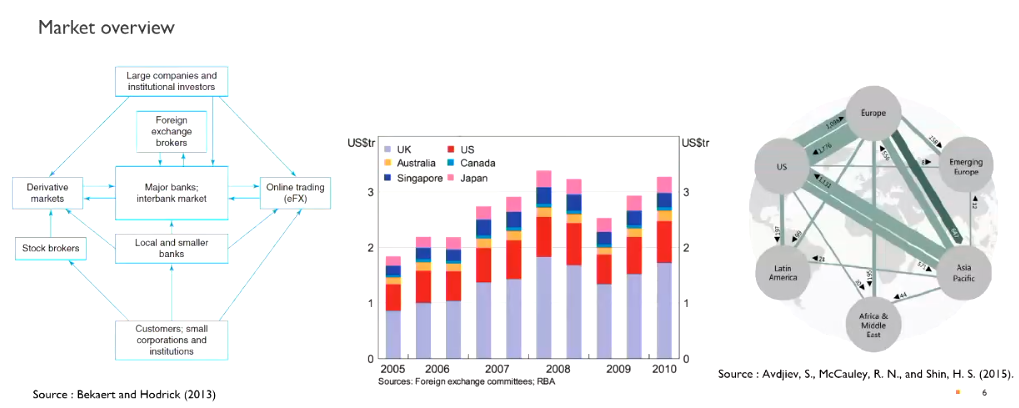

FX Market

largest market in the world in terms of activity

growing exponentionally since the 1980s

daily volume of US$ 7.5 Trillion

Instrument wise:

Exchange rate quotations

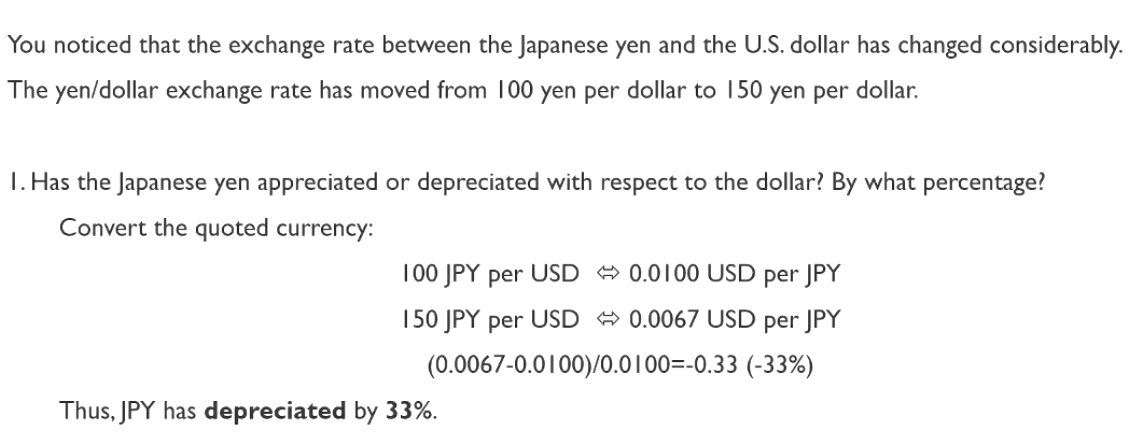

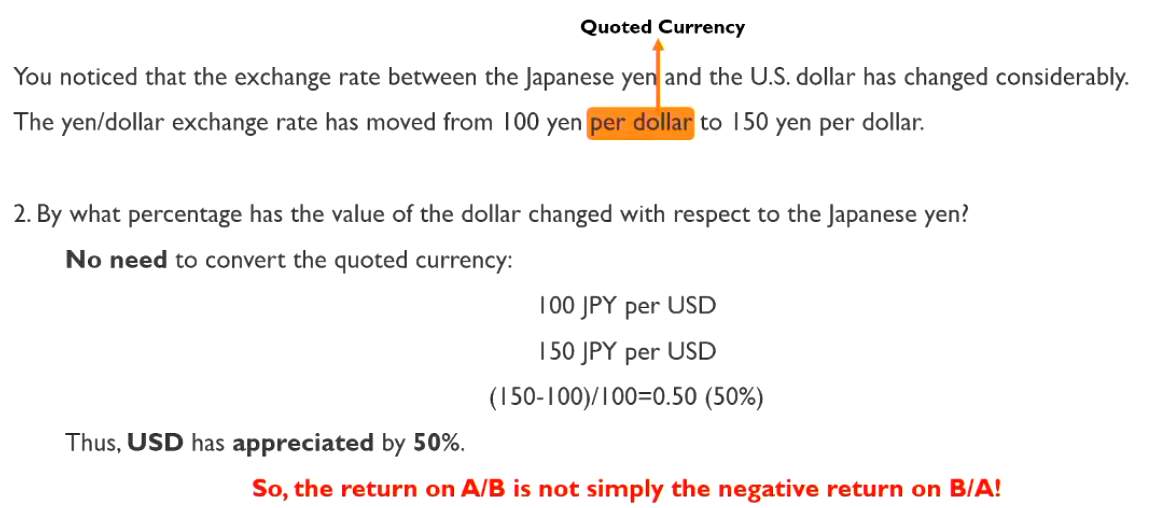

A/B (in this course)

USD/EUR

EUR is the quoted currency

USD is the base

1 USD to 1.20 Euros

If say 1 USD is now worth 1.3 Euros

we say that the USD has depreciated and that the Euro has appreciated

and vice versa if the other way around

Percentage as a measure of depreciation / appreciationm

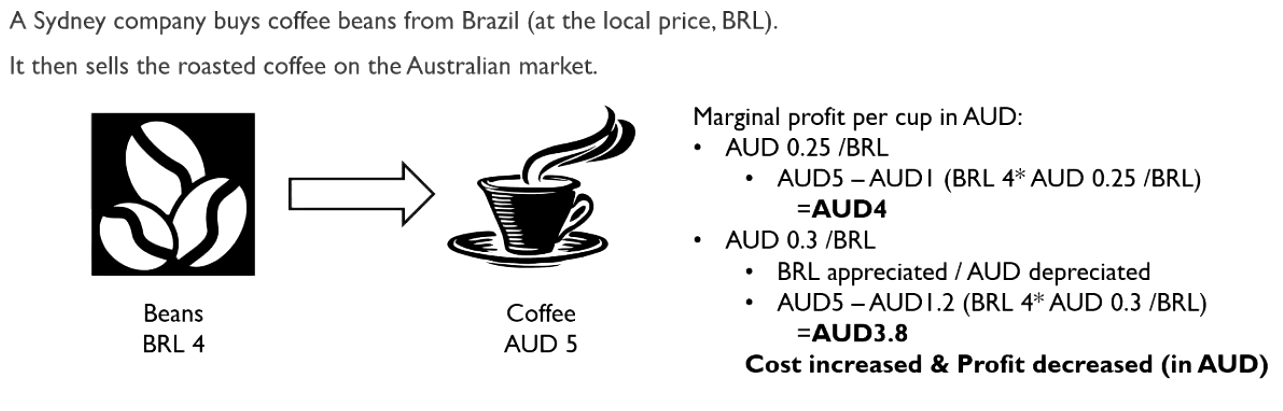

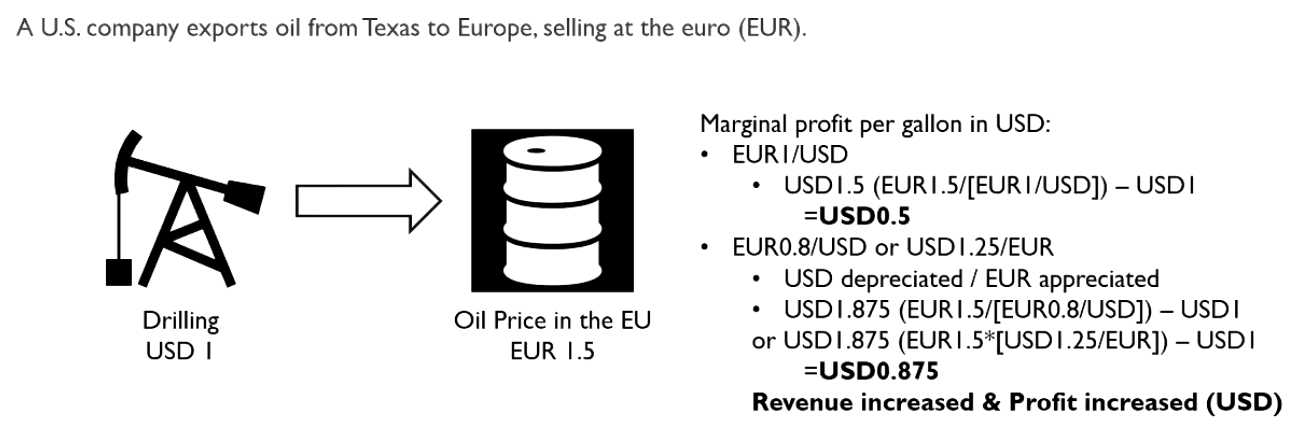

Examples of FX effects for importers vs exporters

Multiply when the rate is expressed as domestic currency per unit of foreign currency (AUD/BRL) — this converts foreign currency costs into domestic currency terms, where a stronger foreign currency means higher costs and lower profit.

Divide when the rate is expressed as foreign currency per unit of domestic currency (EUR/USD); multiply when the rate is expressed as domestic currency per unit of foreign currency (USD/EUR) — both convert foreign currency revenue into domestic currency terms

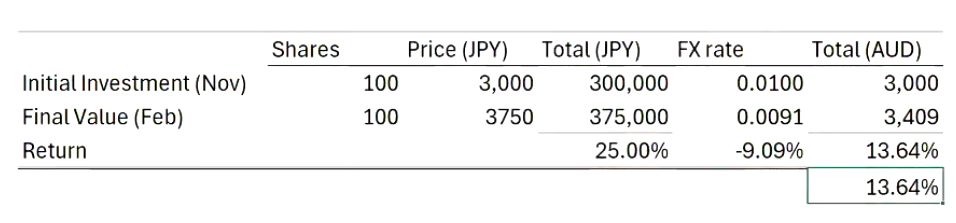

Finding the return of an invesment in a foreign currency

The total return in domestic currency (AUD) reflects both the asset's price return in foreign currency (JPY) and the FX rate change — multiply the foreign currency total by the FX rate (AUD/JPY) to convert to AUD, then calculate the return as (Final AUD Value − Initial AUD Value) / Initial AUD Value

Exchange rate risk

Companies and investors pay risk if they hvae to receive and pay an amount in foreign currency

The future exchange rate is uncertain

And unfavourable exchange rate movements may result in a loss

Important exchange rates in the FX market

Spot rates

quoted for immediate currency transactions

Forward exchange rates

contracted today but with delivery and settlement in the future

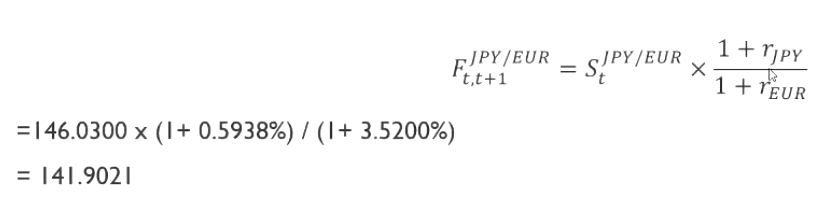

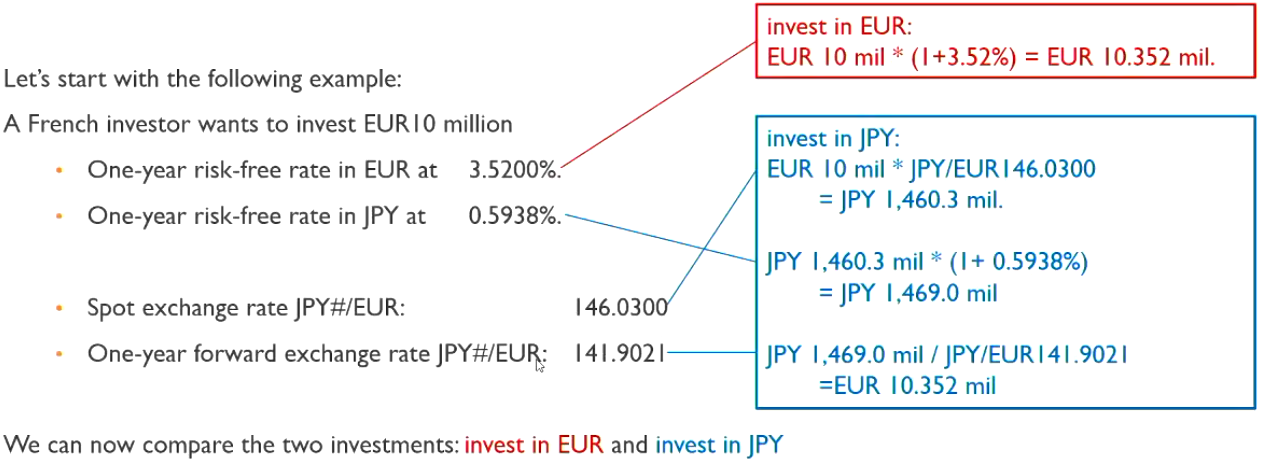

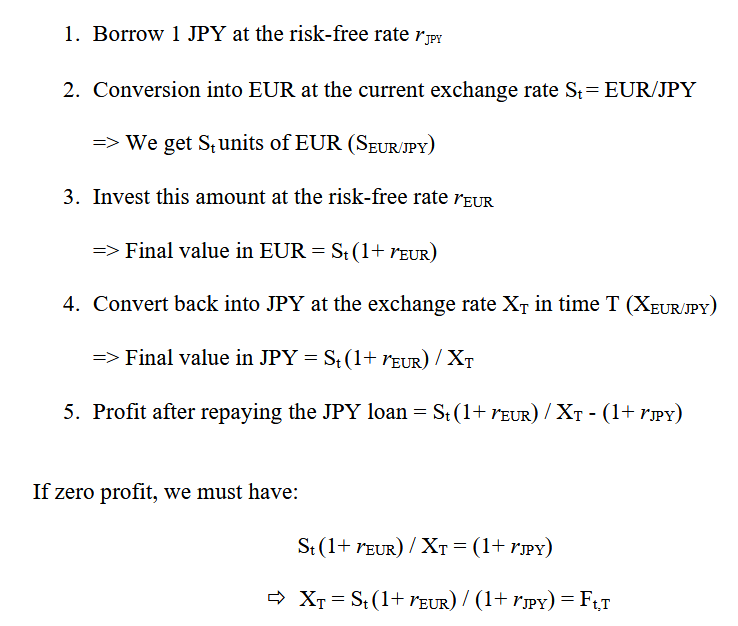

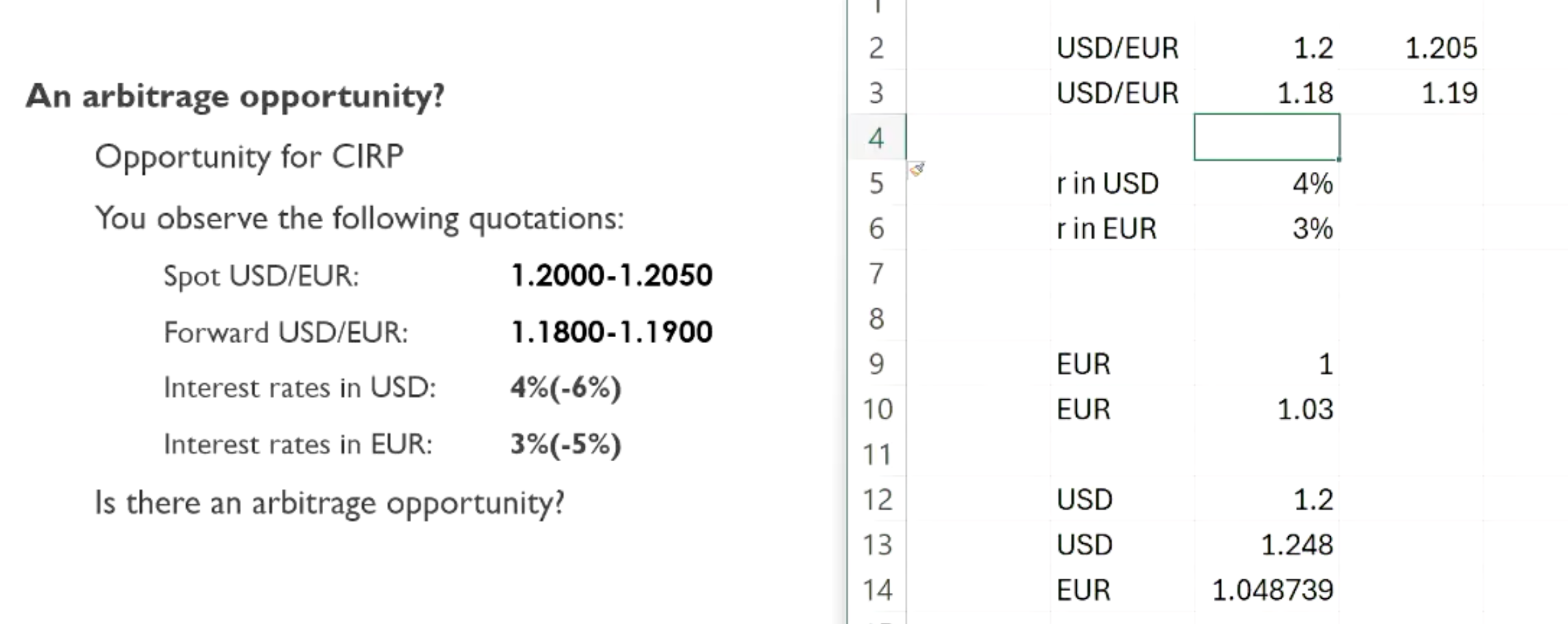

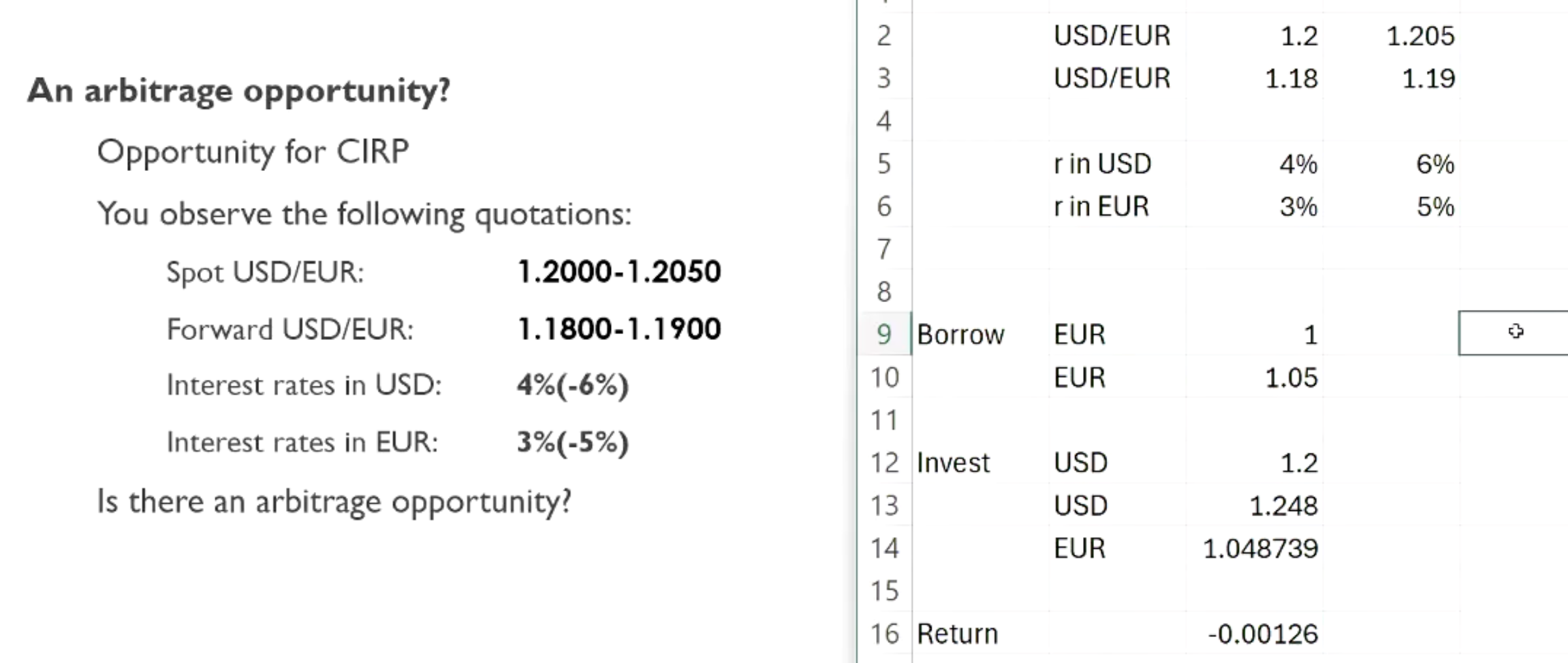

Covered Interest Rate Parity

The forward rate that makes the two investments equal must be given by (F = future.S = spot,r = interest rate)

assumes that there is a non-arbitrage relationship (no difference between investing in two markets)

Premium of the forwards contract

Premium is dependant on the interest rate differential (F = future.S = spot,r = interest rate)'

Covered Interest Rate Parity in practice

In practice it is generally empirically verified

However in the GFC it was violated, as trust in financial institutions faltered and the term “risk-free’ was threatened

Factors that may prevent a potential arbitrage

Counterparty default risk on:

the loan leading to higher interest rates as banks want to prevent bank runs (technically not arbitrage but the risk premium)

the forward contracts (people do not have faith in the next year leading to the rates changing)

Exchange rate controls and tax differences

Countries may limit the ability to exchange currencies

Taxes may be higher than expected and erode profits

Transaction costs

Transaction costs which may seem minute can add up

Forward rate replication

Forex (Foreign Exchange, FX) Market

main exchange rate market

OTC market (no one specific exchange during transaction)

Exchanges by phone or an electronic platform

24 hours a day on weekdays

Inter-bank market: 80% of transactions

Daily volume: $6.6 Trillion in 2024

Largest market in the world by volume traded

Daily volume of US stocks for example is only $1 Trillion in 2024

Main participants in the forex market

Commercial and investment banks

Dealer and market makers

Offering liquidity in the market

FX brokers

financial intermediaries (link between buyers and sellers)

Central banks, mutual funds and hedge funds

Growing players

Transactions in the FX market

Interbank spot market, payment / receipt of FX requires 2 business days

One day for admin, another for time zone differences

Exception is USD/CAD (done in one day)

Electronic exchange rate trading platforms

Thomson Retuers

Electronic Brokering Service (EBS)

More than 50% of transactions route through these services

Anonymous transactions

Trading in the FX Market

Trading is done via the Society for Worldwide Interbank Financial Telecommunications (SWIFT) system

SWIFT links 11000 banks and institutions in more than 200 countries

Operates by sending messages containing transaction information and instructions between FIs

Messages are exchanged in a standardised format, ensuring compatibility between different systems and FIs

Quotations

No exchanges for all exchange rates

However all currencies are exchanged against the USD

Use of cross rates

AUD/BRL = AUD/USD * USD/BRL

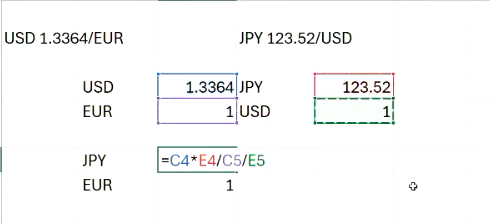

Cross Rates

A cross rate is the exchange rate between two countries inferred from each country’s exchange rate with a third country

For example:

USD 1.3364 / Euro

JPY 123.52 / USD

JPY/EUR = USD/EURO x JPY USD = 1.3364 × 123.52 =165.07

Therefore one euro is worth 165.07 or JPY 165.07/EURO

Order of operations

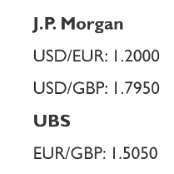

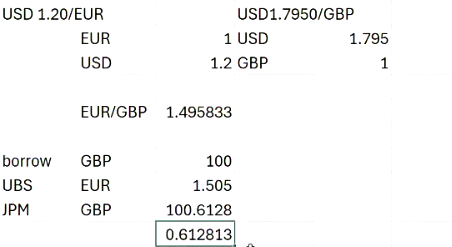

Cross rate arbitrage

Attempting to leverage mispricing between 2 different FX institutions

Ideally borrow money Buy EUR using JPM and sell GBP via UBS

Bid-ask spread

Bid price: amount purchased by the bank / seller

Bank buys EUR at USD 1.24969 / EUR

Ask price: amount sold by the bank / seller

Bank sells EUR at USD 1.5 / EUR

Equavilent quotations

USD / EUR: 1.24969-1.25000

EUR / USD: 0.80000-0.80020

EUR/ USD: 0.80000-20

Bid-ask spread size

Bid ask spread rating for USD / EUR: 1.24969-1.25

3.1 pips (price interest point = unit of change)

One pip = one unit to the 4th decimal place (e.g. USD 0.0001 except for JPY where JPY 0.01)

Can be expressed in relative terms

Spread = round-trip transaction costs

Spread size for major international currencies

Spread size for physical currency exchange

The difference is opportunity costs (no interest)

Spread at the airport: 20-30%

Historically bid ask spread for emerging and advanced markets was quite different, not the case anymore as globalisation and the rise of fintech has allowed converence in liquidity for the currencies of AE and EMs

bid-ask spread size

Size varies according to market conditions

Allows traders (dealers) to manage inventory risks

exchange rate volatility as a determinant on the bid-ask spread size

The bid ask spread increases with exchange rate volatility (connected with uncertainty)

An example is the GFC, august 2024 where there was high uncertainty

forward contracts as a determinant of the bid-ask spread size

Bid ask spread increases with the maturity of the forward contracts

A bank’s default risk increases with the horizon

More difficult to find counterparty willing to do such a transaction

Increases the bank’s inventory riosk

Higher bid ask spread for forward contracts than for spot rates

Real world example:

Very significant counterparty risk in 2008-2009

Following bankruptcy of Lehman Brothers in 2008, bid ask spreads for 3 month forwards were double the spread for spot contracts

IF FORWARD BID ASK SPREAD IS NARROWER THAN SPOT IT IS A WRONG CALCULATION

Liquidity as a determinant of bid ask spread size

Forward market less liquid than the spot market

Especially for long-term contacts

Banks often impose an order limit or ask for collateral

If there is high liquidity, there will be pressure narrowing down the bid ask spread

High transaction costs for long term forward contracts encouraged the development of another market

long term currency swap

Intra-day variations of the bid ask spread

Generally higher spread at the beginning of the market and at the end of the day

less news less trading

Economic statistics announcements during the day can significantly move prices

Calculating cross rate calculation with bid ask spreads

As a general rule of thumb, the bid ask spread should be maximised (take the worst)

Bid rate (buying price) should be as small as possible

Ask rate (selling price) should be as high as possible

Formula

(A/B) bid = (A/C) bid / (B/C) ask = (A/C) bid * (C/B) bid; given that (C/B) bid = 1 (B/C) bid

(A/B) ask = (A/C) ask / (B/C) bid = (A/C) ask * (C/B) ask; given that (C/B) ask = 1 (B/C) ask

Examples:

Note to keep the bid as low as possible and ask as high as possible

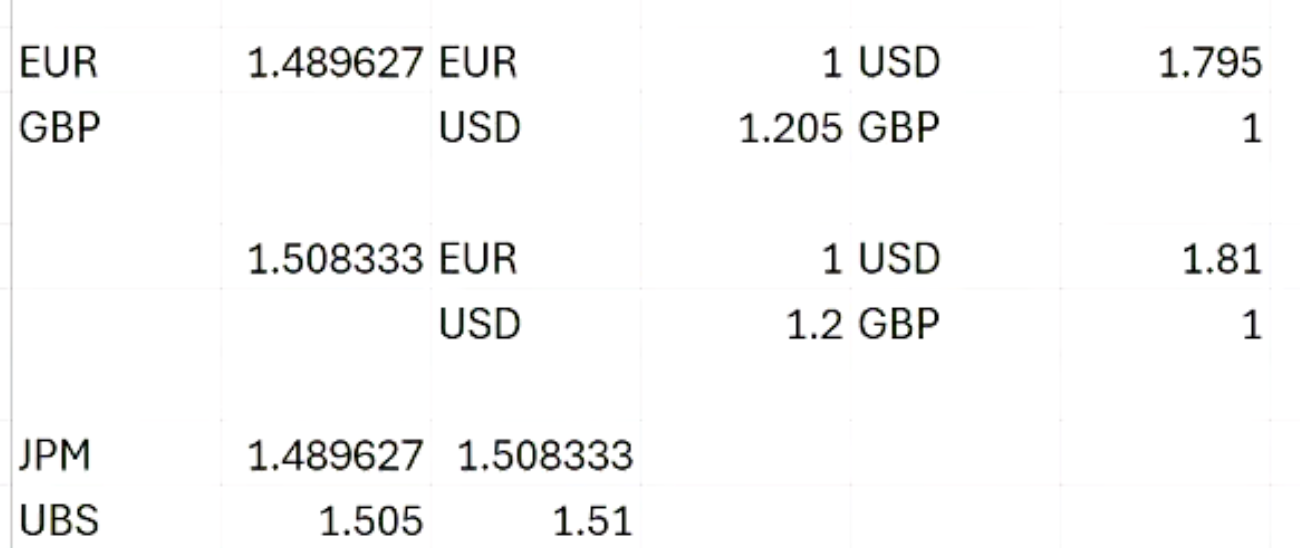

J.P. Morgan

USD/EUR: 1.2000-1.2050

USD/GBP: 1.7950-1.8100

UBS

EUR/GBP: 1.5050-1.5100

Multiply top with top and bottom with bottom

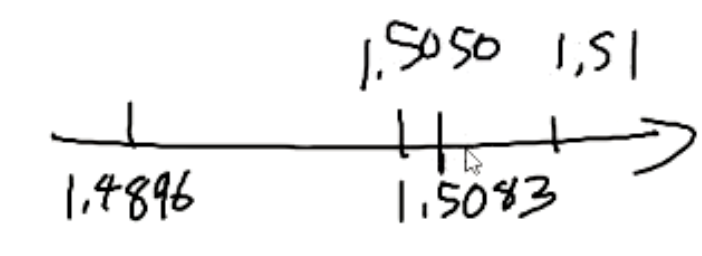

There is no arbitrage in this sense as we buy at 1.5083 from JPM and sell to UBS at a price of 1.505

easy way to determine arbitrage is to construct a diagram showing both bid ask spreads:

Covered Interest Rate Parity in the context of a bid ask spread

Theoretically nothing much changes in regards to the currency that is invested in the home country’s bank, however the only difference is that when converting pay the bid spread (which will be lower than the market value), and when converting back to original currency pay the ask spread (which will be higher than the market value)

Covered Interest Rate Parity in the context of a bid ask spread with different borrowing rates

Different borrowing rates may exist for each country’s FI, after all banks will charge higher for borrowing money and will often pay less for the guarantee of a riskless investment return

Therefore the rate differences may actually eliminate the ability to conduct an arbitrage

As we see in the example: the borrowing rate for the EURO is 5% making the arbitrage unprofitable as the cost of capital is too high

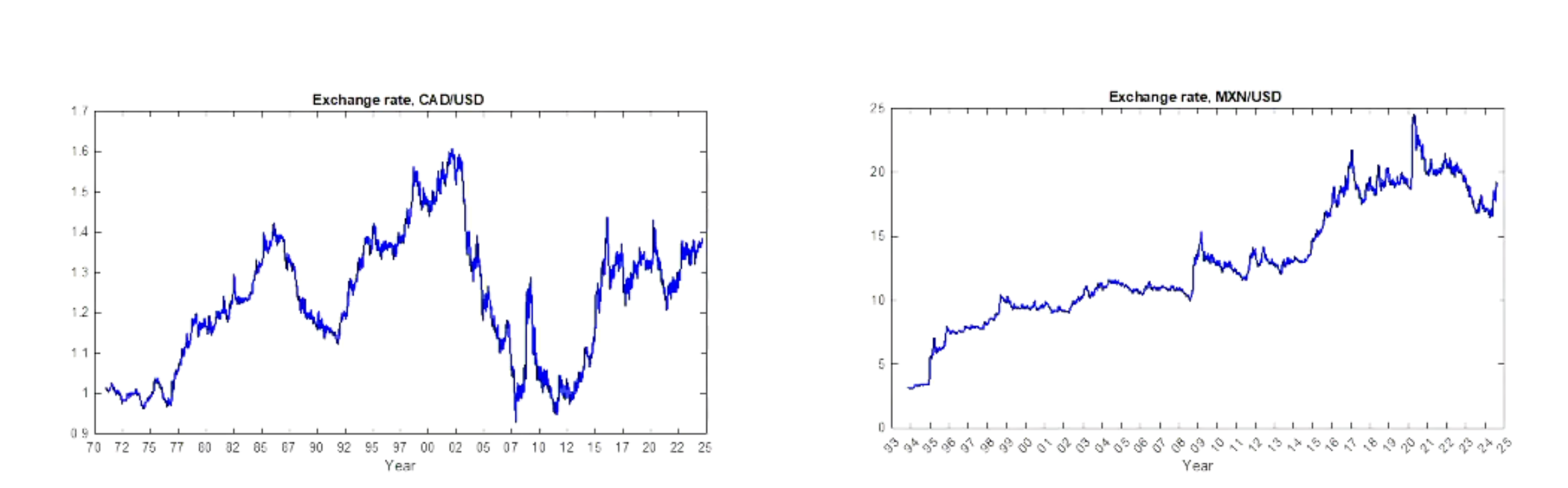

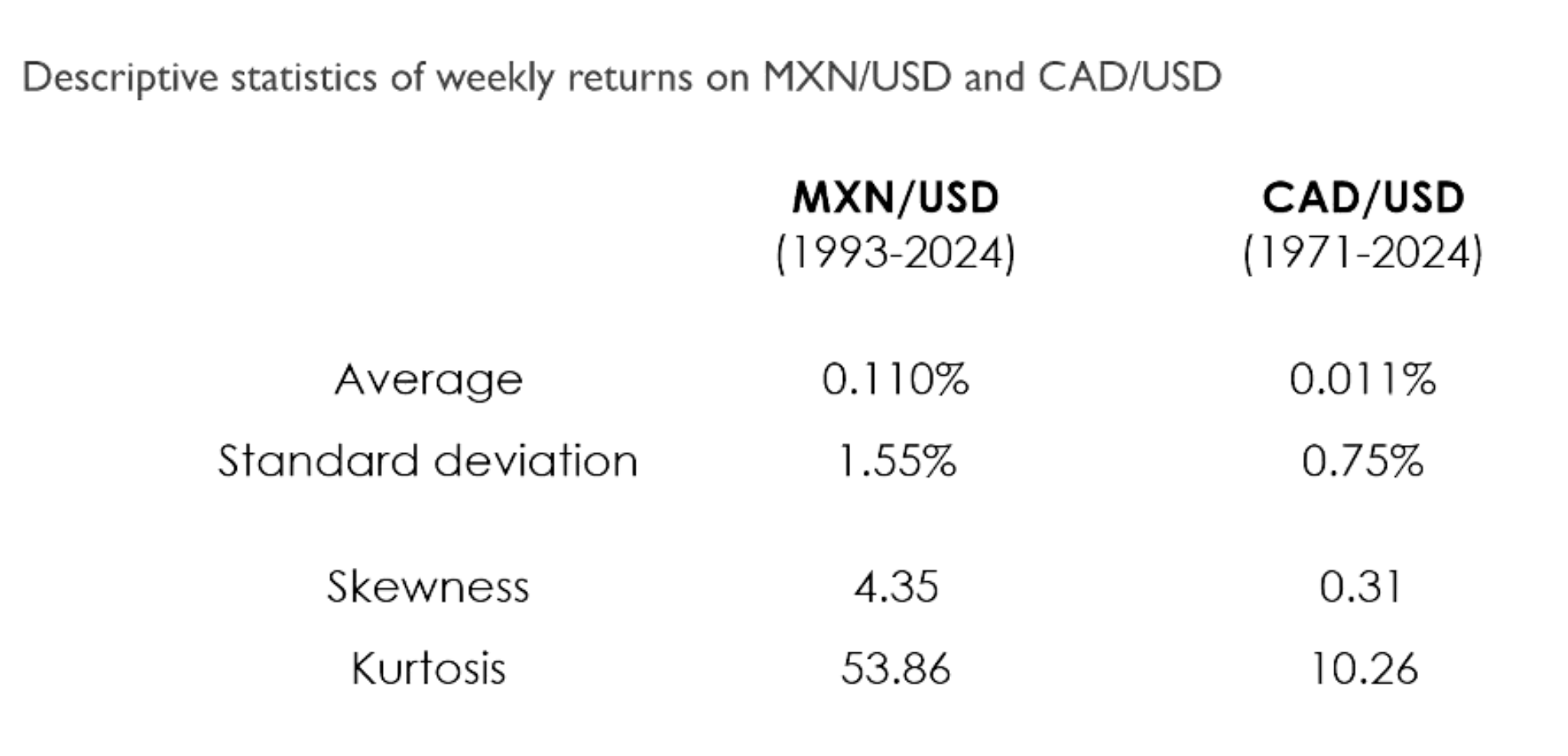

Exchange rate risk

CAD / USD has a range of 1-1.6 / USD over the past 50 years indicating the USD has appreciated and CAD has depreciated

MXN / USD has a range of 3-25 / USD over the past 30 years indicating the USD has appreciated and MXN has depreciated

Quantification of losses / gains require a description of the uncertainty related to exchange rate fluctuations

Using historical data to determine the distribution of exchange rate changes (returns)

Take the return of the exchange rate per a certain interval (daily, monthly, yearly whatever period)

Calculate the mean and volatility of the exchange rate returns

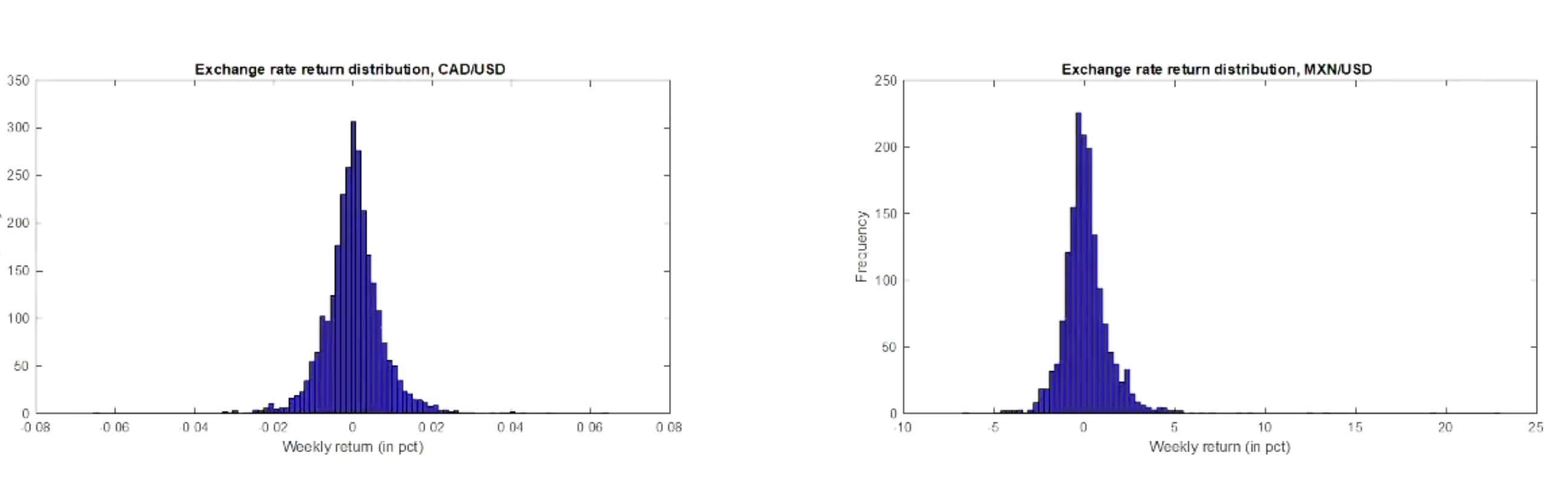

Assume a normal distribution (bell curve, no extreme returns)

Include skewness (asymmetric shape) and kurtosis (extreme returns) if the distribution is not normal

Example:

Skewness indicates that there are more positive outliers in the distribution indicating a high volume of change in MXN / USD (depreciation)

Kurtosis measures the fatness of tails, the MXN / USD has a fat right tail indicating that there are more extreme depreciation events that are likely to happen in the future

Missing the 95% confidence interval which measures (Clarify on this)

Currencies of Advanced vs Emerging Markets

Currencies of advanced countries

Reasonable to consider symmetrical distribution in view of the symmetry of the returns

More appropriate to consider a distribution that takes into account of fat tails, extreme values

Currencies of emerging markets

Symmetrical distribution is not appropriate

Historical distribution is generally very skewed and shows large magnitude changes

Mainly due to significant depreciation / devaluation of these currencies that have occured

Exchange rate volatility changing

Time-varying volatility can be estimated with different approaches:

Rolling standard deviation of the returns

Autoregressive (GARCH) model on returns

Important to use recent data to get more realistic, more accurate results from more complicated models as complicated models are easier to break

Statistical models may determine how exchange rate returns (and their volatility) vary over time. However, they do not help us understand why exchange rates fluctuate in such a way. Therefore it is key to remember the fundamentals (interest rates, macroeconomics)

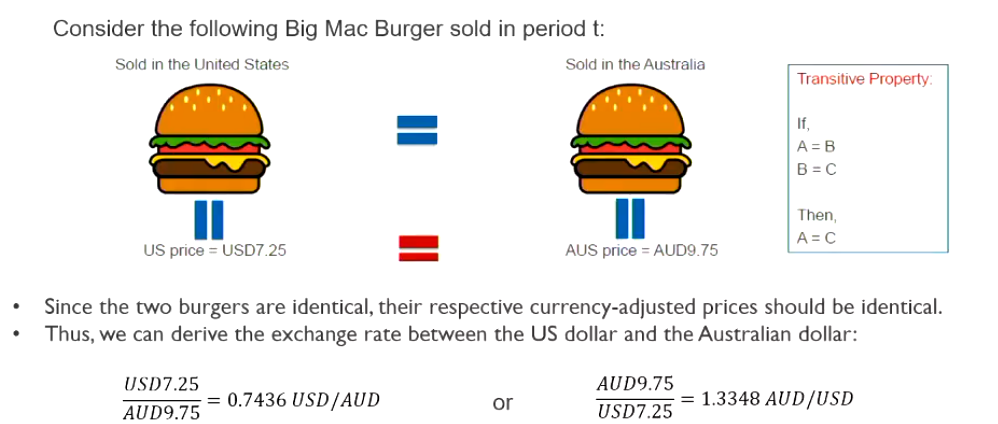

Absolute Purchasing Power Parity (PPP)

The same good is at the same price everywhere (law of one price)

The exchange rate equals the consumer price ratio

Assumes:

No transaction costs

Same basket of goods in all countries

Example:

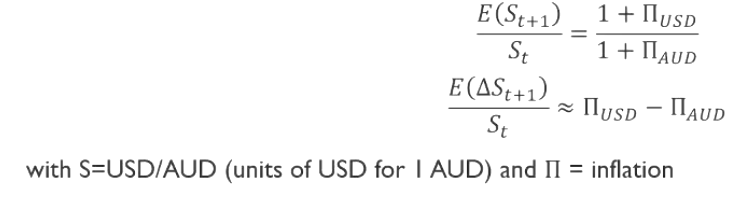

IF APPP holds RPPP will hold

Relative PPP

Considers price growth (rate of inflation) rather than price levels

Expected exchange rate growth = inflation differential

Same simplifying assumptions as absolute PPP

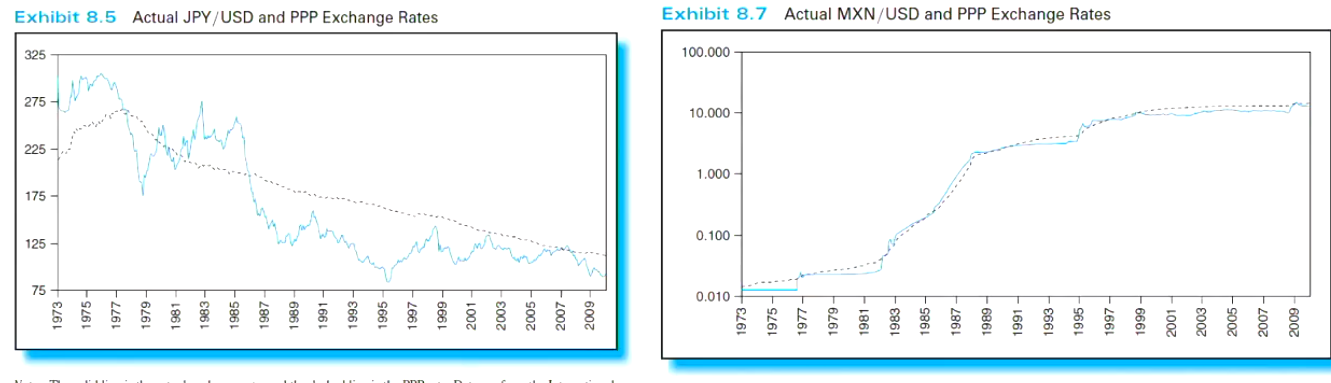

PPP in the real world

PPP gives a framework as to where currencies are trading in the bigger picture

Long-term fundamental valuation

Useful in the long term

Not very effective in the short term

Common CPI alternatives

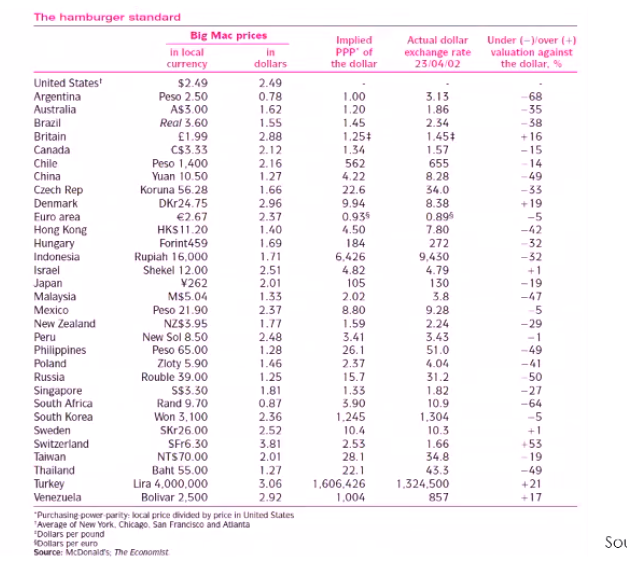

Big Mac Index (used to predict exchange rate index)

IKEA Billy Bookshelf Index (produced in one area and shipped to other countries, better index)

PPP investment application

Sort currencies into portfolios based on 5 year change of PPP

Portfolio 1: 25% of currencies that are most overvalued

Portfolio 4: 25% of currencies that are most undervalued

Result:

Find predictive power for the cross-section of currency excess returns

Buy P4 and Sell P1, Long-short

Theoretically will hold but there may be difficulties finding some currencies (CFA franc for example)

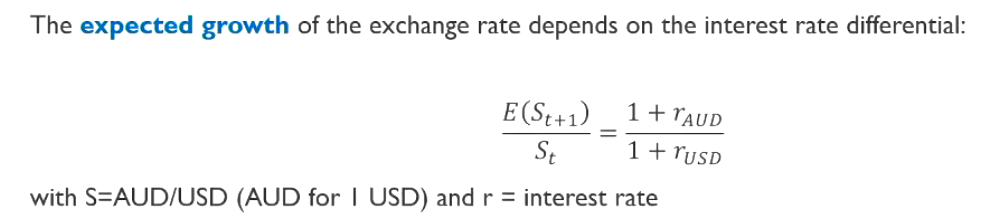

Uncovered Interest Rate Parity

Hypothesis that the expected return on the uncovered (unhedged) foreign money market investment equals the known return from investing in risk free rates internationally

Idea:

The expected growth of the exchange rate depends on the interest rate differential

We are not hedging anything we are just using the spot rate

Explanation for parity:

Interest rate differential across countries on bonds of similar credit risk should reveal the expectation of depreciation

Initially, attractive interest rates (say australian rates are higher) should be met by an FX move (AUD depreciates by the same amount, cancelling the effect of rates), resulting in the same return

The ex post realised exchange rate will not necessarily equal the rate expected on average

Basically the same as CIRP, but now even in uncovered transactions, there is nothing to earn

Formally”

Assumes free capital mobility and the absence of taxes on capital transfers

The zero investment (zero-cost) portfolio of money market instruments should yield 0 in expectation if investors are rational and risk neutral

Current exchange ratre formula UIP

Implications of UIP

Interest rate differential, CP = expectation of exchange rate return

The USD Return on a risk free investment must be the same for all countries

Not interesting in a country with higher rates

Expected depreciation is expected to offset the higher rate

Exchange rate coverage without cost

forwards contract price = expected exchange price

Essentially we dont need the forward rate

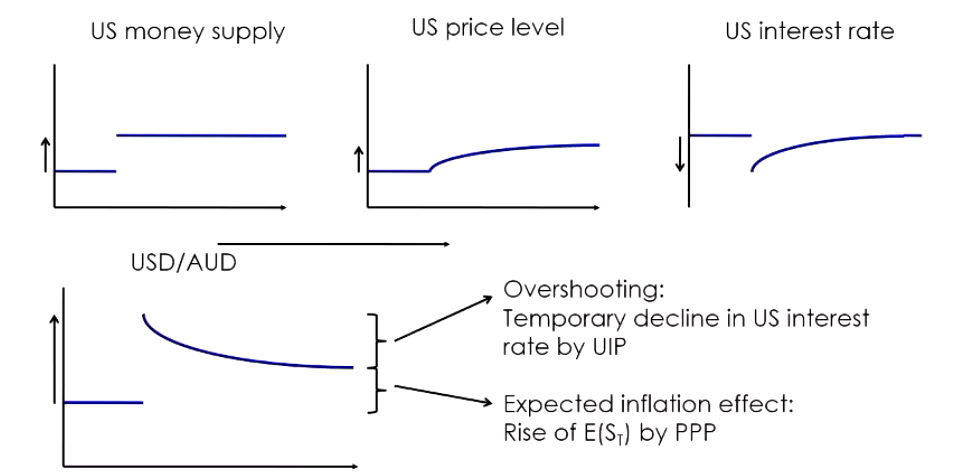

Valuation model with monetary shock

Impact of a money supply shock (one time and permanent shock) in the USA (QE)

American consumers are endowed with more money

Initially all invested in risk free bonds (banks) so bond yield / interest rate (R usd) will fall

Then consumers will gradually buy goods

Interest rates increases again and inflation slowly picks up

In the long run all money invested has been spent on goods

Therefore higher consumer prices while interest rate goes back to the initial value

Represented by:

Overshooting is the phenonmenon where the exchange rate is temporarily higher than it should be, and takes time before settling

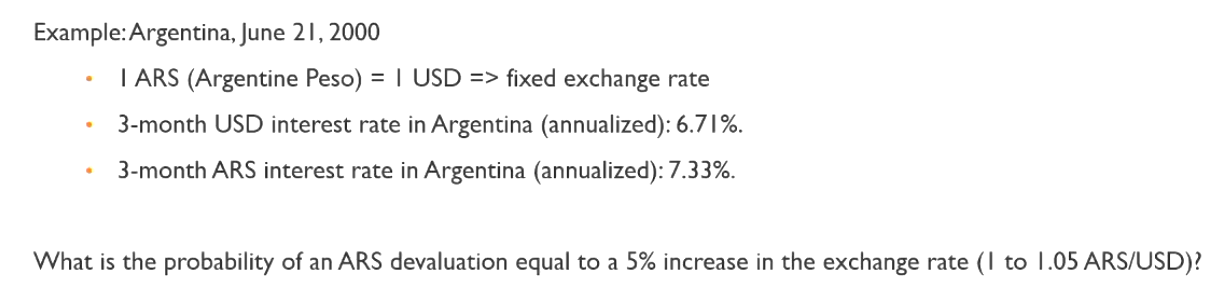

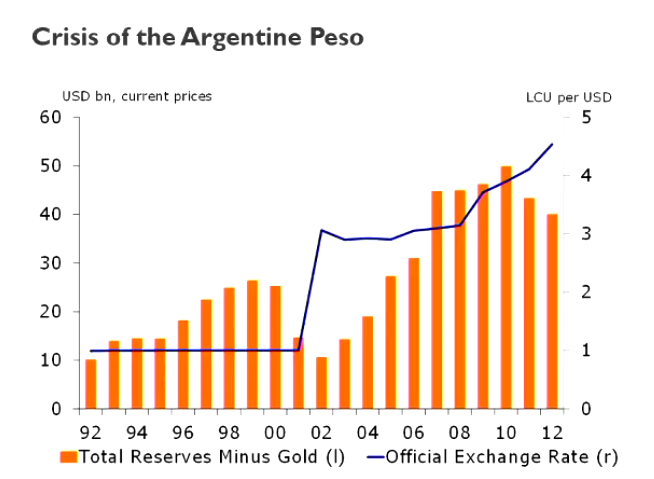

Forecast of exchange rate devaluation

Majority of currencies are not floating

Devaluation can be forecasted using:

Balance of the current account (trade + financial balance)

Monetary growth

Interest rate and inflation differential

Measures of overvaluation using PPP

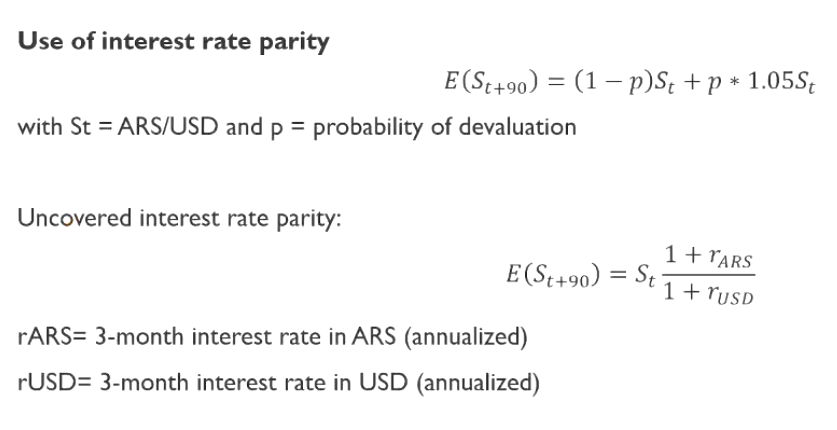

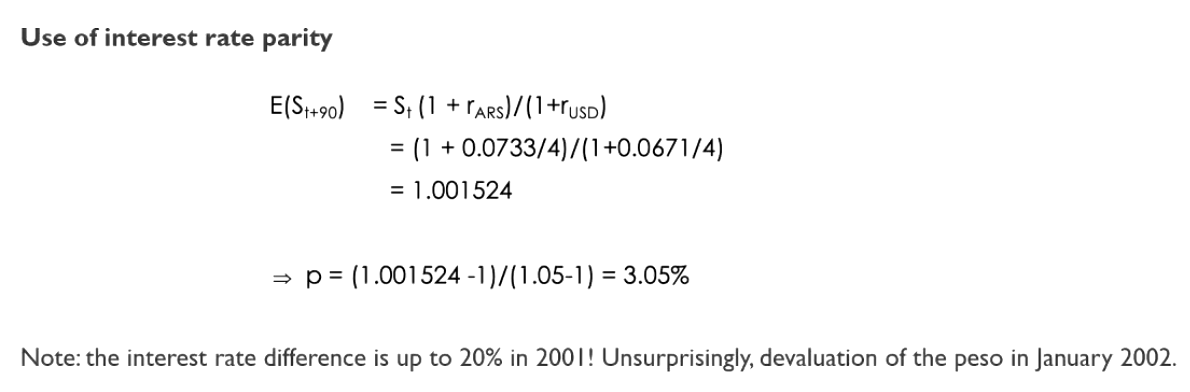

Use of interest rate parity for predicting devaluation

ARS interest rate is higher than USD indicating that ARS is expected to depreciated by the market

Using expectation spot rate formula:

Floating exchange rate system

Free float (clean): determined solely by supply and demand

Dirty float: market forces with some central bank intervention

Managed float: more central bank intervention than a dirty float

Assume in this course that otherwise mentioned all currencies are using the floating exchange rate system

Fixed / Pegged exchange rate system

Target exchange rate set by the government with the central bank intervening to prevent significant deviation

Requires coordinated monetary policies and commitment to the target rate

Target zone agreement

allows market forces but only within a margin around agreed upon fixed exchange rate

Crawling Peg

Currency deprecation against a reference currency on a regular controlled basis, used to ease transition from fixed to fluctuating exchange rate

What is money?

Serves as a store of value, medium of exchange, and unit of account

Managed by different institutions (Federal Reserve, RBA for USD and AUD)

Previous exchange rate systems

Gold / Silver

1 Pound Sterling = 1 Pound of Sterling Silver

$35 = 1 Oz of Gold (US Bretton Woods)

Features

Exchange rate based on the law of one price

Extremely stable inflation

Rigid supply restrictions

Bretton Woods (1944-1971)

US held 2/3 of all gold reserves in the entire world

Gold was pegged to the dollar at a fixed rate, other currencies were pegged to USD

IMF was introduced to provide liquidity to nations in crisis

Nixon Shocks (1971)

Ended the convertibility of USD to Gold

Huge US deficits (due to the vietnam war, foreign banks demanding gold redemptions)

Marked the shift to fiat currencies

The dollar retained the status of the premier currency despite no gold backing

Floating exchange rate

Exchange rate between two freely traded currencies

Exchange rate fluctuations are determined by supply and demand:

Market equilibrium

High exchange rate volatility

Limited central bank intervention

Temporary stabilisation only

Exchange rate risk:

Can be determined by historical FX volatility

Historical return distribution is useful for predicting up/down movements

Possible intervention by monetary authorities

Determines some ceiling or treshold

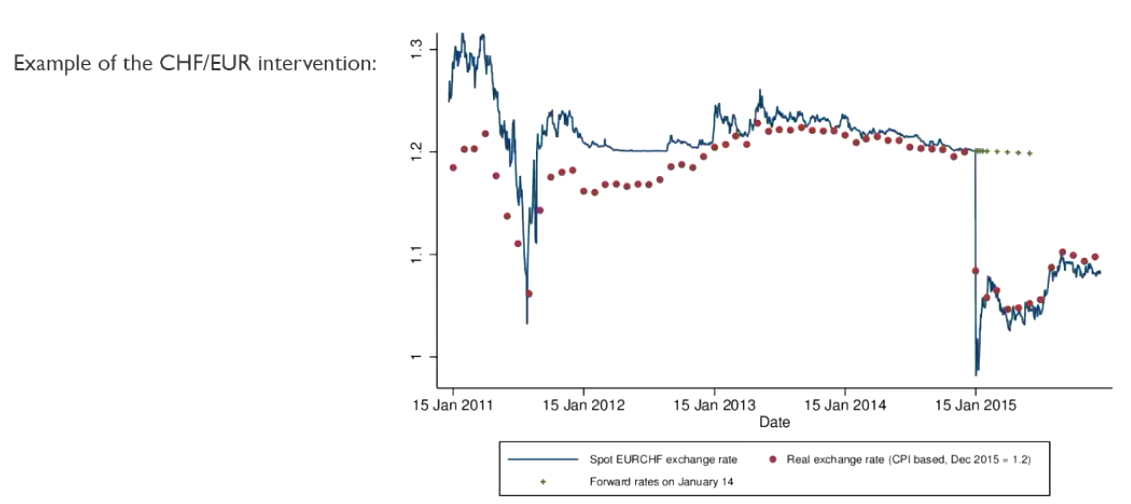

SNB sets a floor at 1.21/1 CHF / EUR in 2011

Fixed exchange rate

Predetermined exchange rate at a fixed level

Determined in advance by the central bank

There is still some exchange rate risk

Collapse of the fixed regime (IDR, ARP)

Abrupt and substantial devaluations of currency (GBP post suez)

Arrangement is not credible in the long term

Devaluation incentive in case of economic crisis

Subject to speculative attacks (George Soros GBP)

Pegged exchange rate

Predetermined exchange rate with authorised adjustment

Compromise between fixed and floating regimes

Free fluctuations within a certain range

Adjustments are based on economic fundamentals

inflation, growth, current accounts

Low short-term volatility

Exchange rate risk

low daily volatility is not real risk

latent volatiliy is the real risk (political risk esp if developing countries)

Difficult to quantify as there is no historical data

Called the “Peso” problem

Agreement not very credible in the long term

Devaluation incentive in case of economic crisis

Subject to speculative attacks

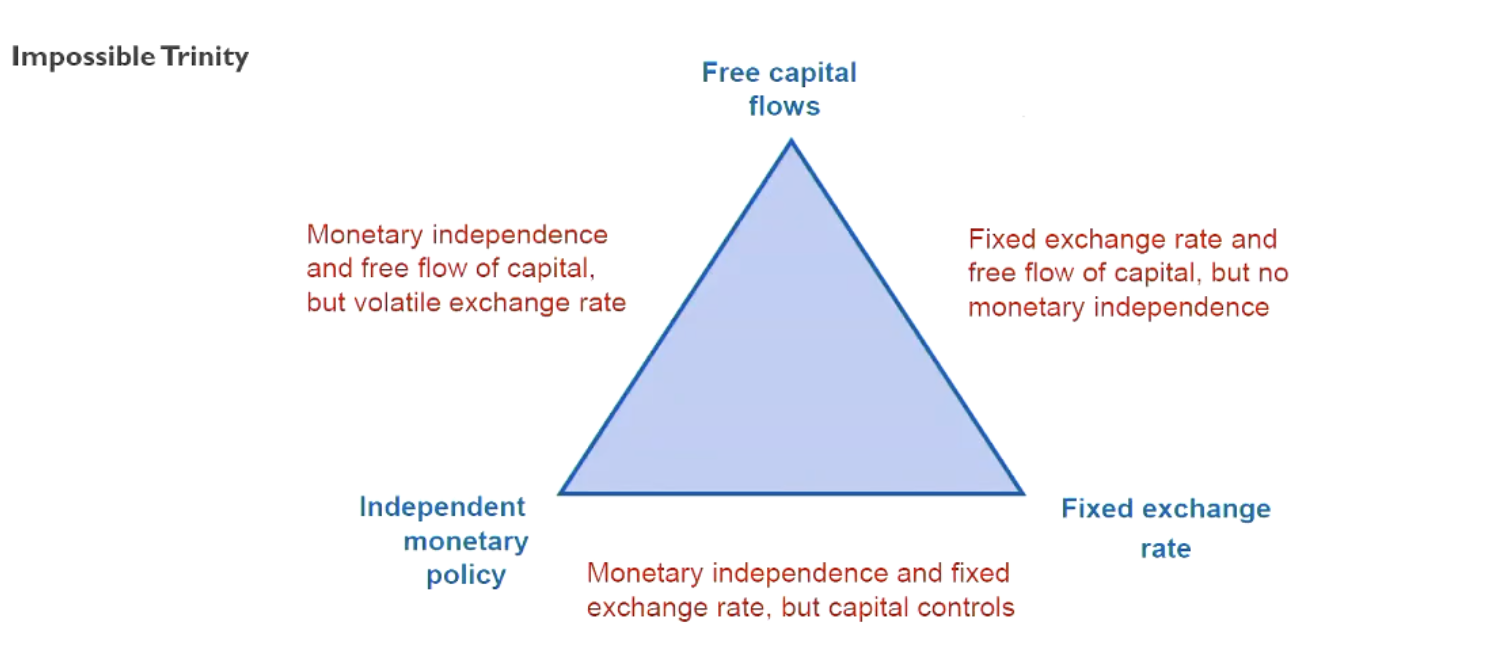

Impossible trinity

one currency can only have 2 of these charactheristics but not all three

Factors that determine exchange rates

Balance of payments

international trade and capital flows

Economic fundamentals

inflation, growth, commodities

Financial conditions

interest rates, stock market performances, level of uncertainty

Balance of Payments

Synthesis of international financial flows observed during a given period

accounting identity

Each flow is associated with currency demand or supply

Significant edia, analyst, investor, media attention

main source: IMF open source data, easy to access / public

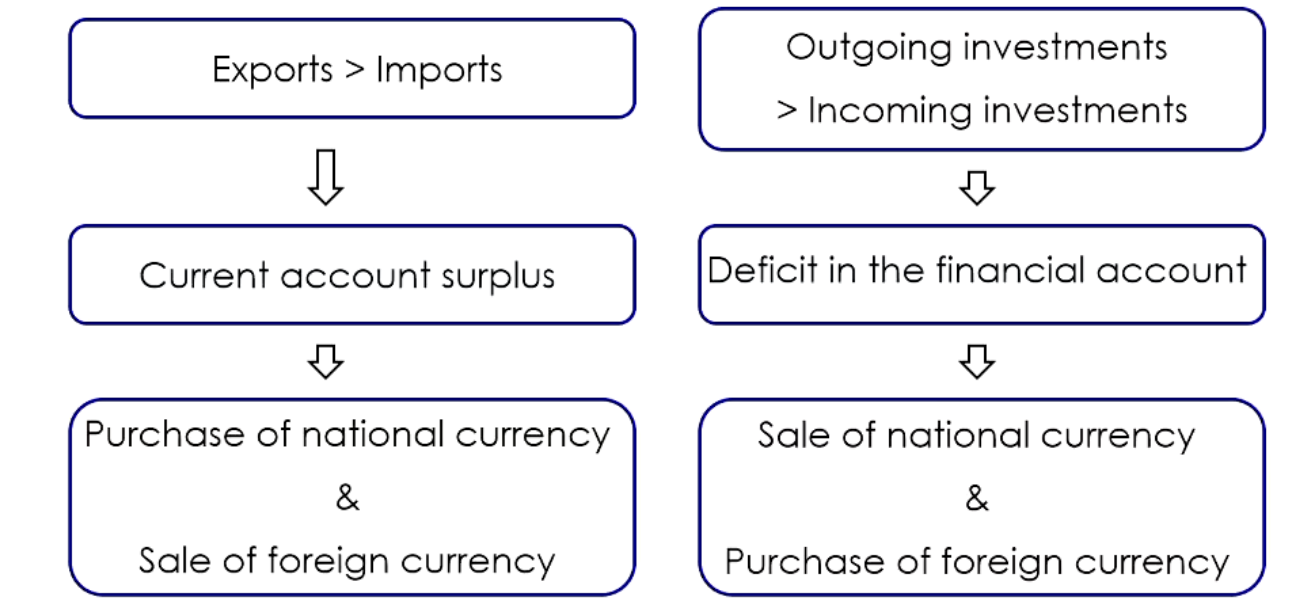

Balance between trade and financial flows

Current + Financial accounts = 0

Accounting balance due to changes in the foreign currency reserves of the central bank

Current account + financial account = Delta reserve

Example: decrease in reserves if total balance < 0

Economically in a floating exchange rate system, the exchange rate would appreciate / depreciate to keep the system balanced

trade deficit

Trade balance = not informative per se about the direction of the exchange rate, if

current account deficit = financial account surplus

it is important to analyse the entire balance of payments as trade deficit leads to financial surplus (generally)

Financial account

main aspect to be analysed

if foreign investors want to finannce a trade deficit = no problem

balance between depreciation (trade deficit) and appreciation (financial surplus) of the currency

natural situation in the case of strong economic growth

Consumption > production: trade deficit

High profitability = high returns on investment: financial surplus

if foreign investors no longer want to finance a trade deficit it could lead to

liquidiation of financial investments (capital flight)

currency depreciation (no one wants the currency, no demand)

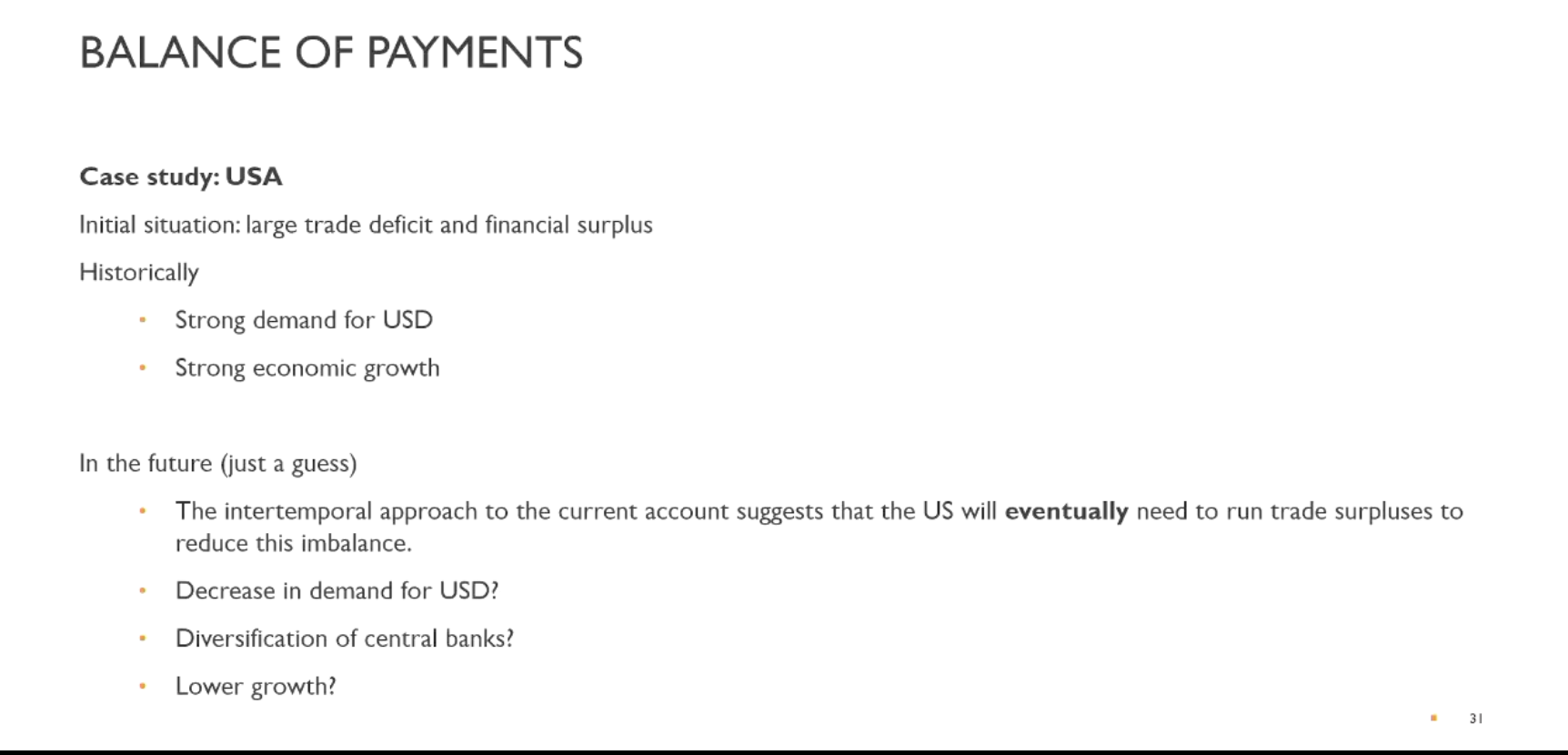

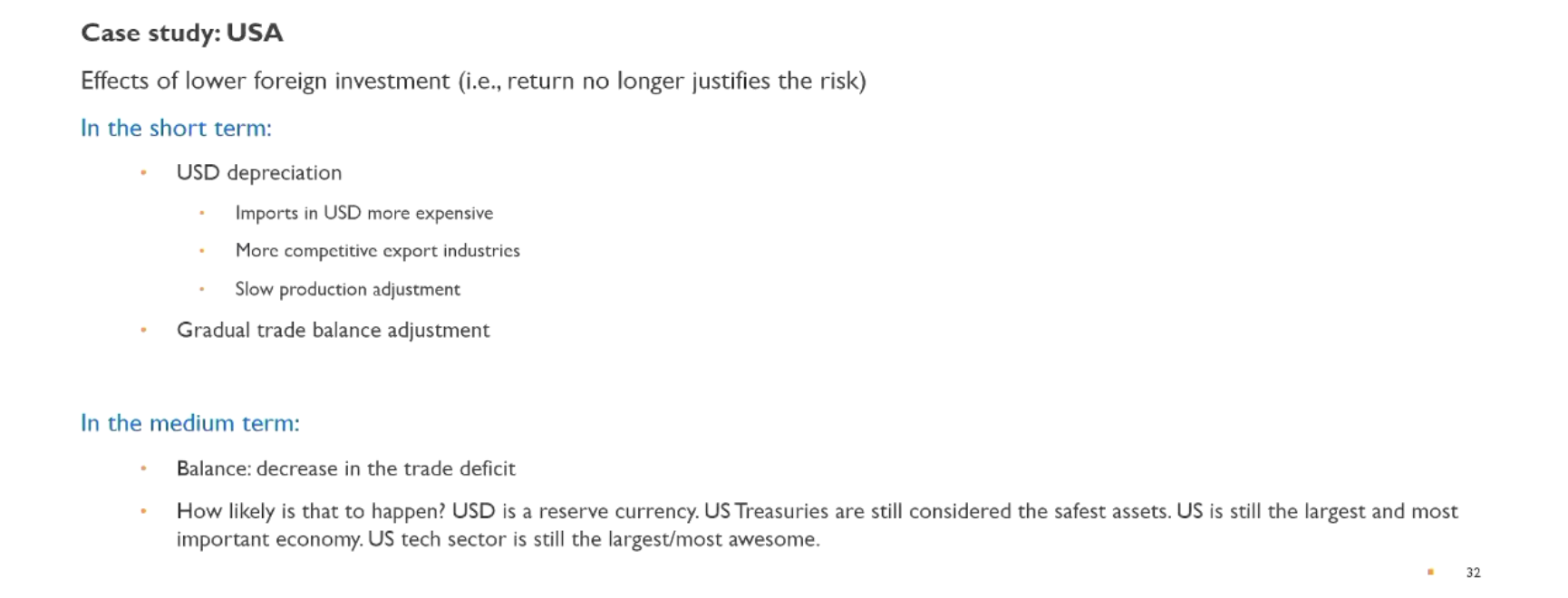

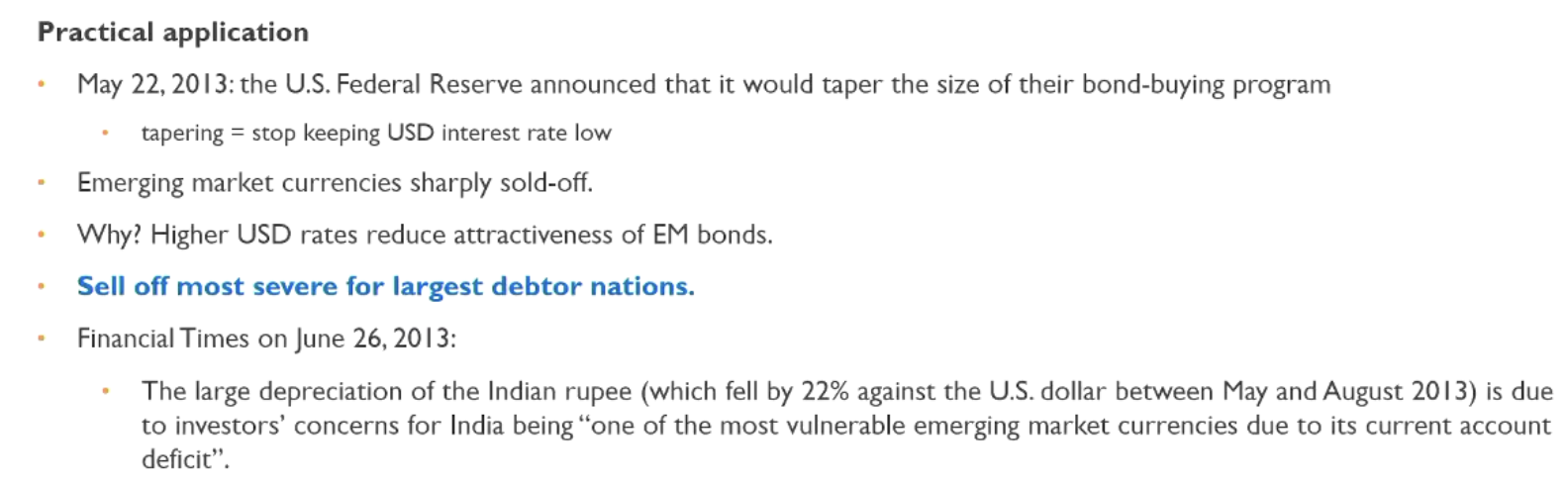

Case study for BOP (USA)

Scenarios are unlikely as US has a lot of economic power (innovating companies, leading products that are exported)

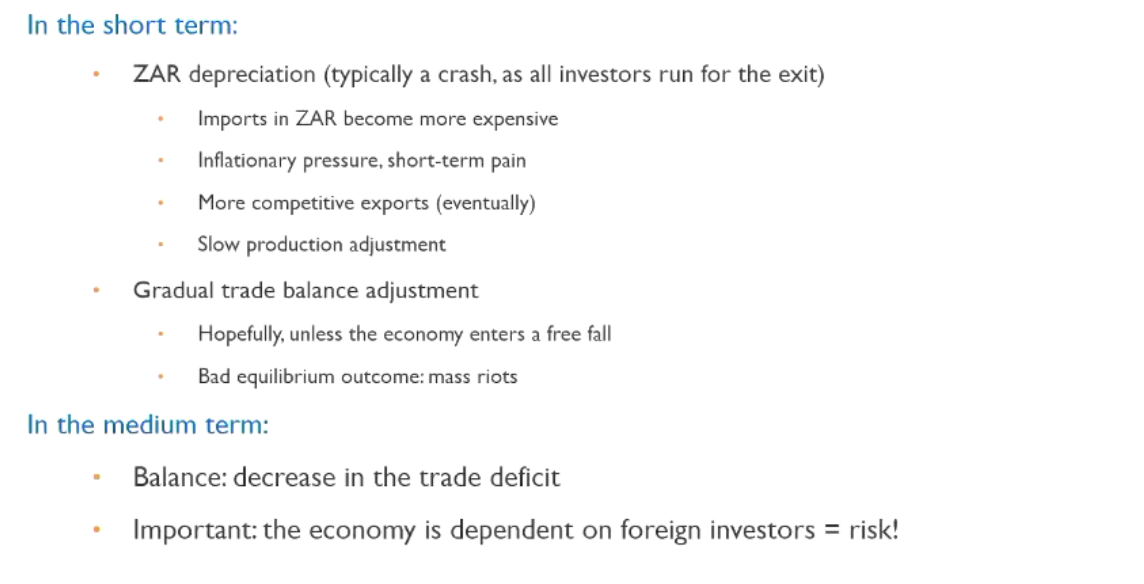

Case study for BOP (Emerging Market)

Practical application of the above concepts for emerging markets

net foreign position (asset - liabilities at a country level) relates to currency returns

the intuition is that investors demand a risk premium to hold debtor nations currencies due to the risks, this is especially true if the currency is held in a foreign currency

Observed effects of economic fundamentals

Appreciation of a currency occurs ceteris paribus if there is:

1.) Strong economic growth

Increase in investment returns

Increased foreign investment

Interest rates with expected economic growth

taylors rule

also interest rates hike from the central bank to reduce inflation from the increase in economic growth

Note that the effect is partially offset if import > export growth

2.) Higher commodity prices for exporting countries (Australia, Canada, NZ)

more corporate profits and equity prices (BHP, Rio Tinto)

improve the country’s economic conditions

speculative component for FX investors

3.) Rise in domestic interest rates

increase in demand for domestic bonds (carry trades)

can signal stronger economic growth and higher stock prices

not necessary due to higher economic growth and higher inflation

4.) Foreign interest rate cut

decline in demand for foreign bonds → depreciates foreign currency relative to domestic currency therefore domestic currency appreciates

5.) Good times for cyclical countries

Ex: emerging market countries

Currency “speculative” growth and periods of calm (low volatility)

6.) Times of crisis for non-cyclical countries

Ex: USA, Japan, Switzerland

safe haven currencies in recessions and period of uncertainty

Central Bank and Exchnage Rates

Purpose of intervention

Influence exchange rates to influence a currency

In general, to limit the appreciation/depreciation of the currency

Appreciation: Loss of competitiveness of exporters

Depreciation: Rising “imported” inflation

Interventions can be:

Sterilised

Unsterilised

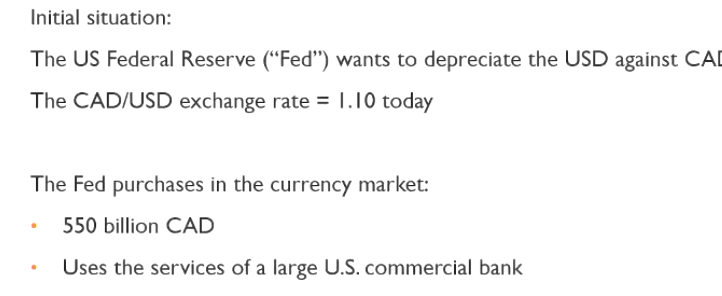

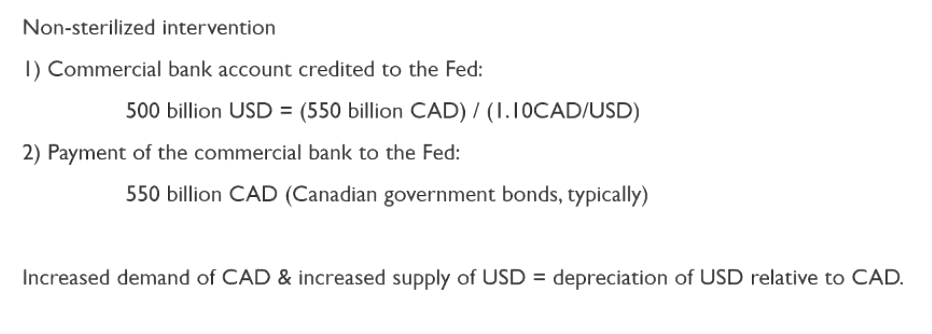

Unsterilised Intervention

There are downsides:

Increased money supply (500 Billion USD more circulating in the economy)

Medium / long term inflation effects

Therefore there is a potential conflict when seeking price stability

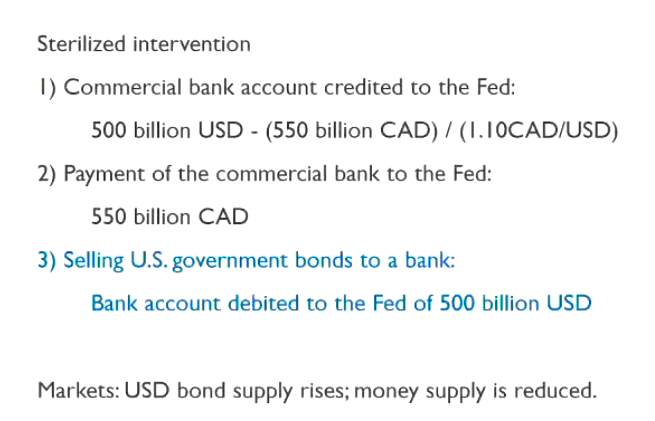

Sterilisation can solve this

Sterilised Intervention

Example of intervention

Intervention Success depends on

Size of intervention relative to daily volume

Size of the available foreign exchange reserves

Current market trends

Coordination between nations (Plaza Accords 1985 took Japan, Germany and USA to depreciate USD)

Number of interventions

Sterilised or Non-Sterilised intervention

It is often easier to prevent appreciation than a depreciation

Markets are also typically pessimistic about the success of an intervention

Forecasting exchange rate

still a prevailing view that exchange rate changes are difficult to predict in the short term

A random walk model performs just as well as any estimated model in the short term (1-12 month time horizon)

exchange rates are asset prices like stock prices and therefore we should expect they behave like other assets which are also hard to predict

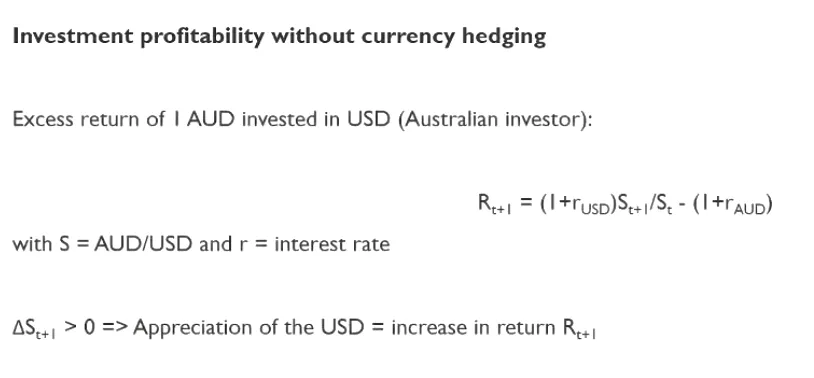

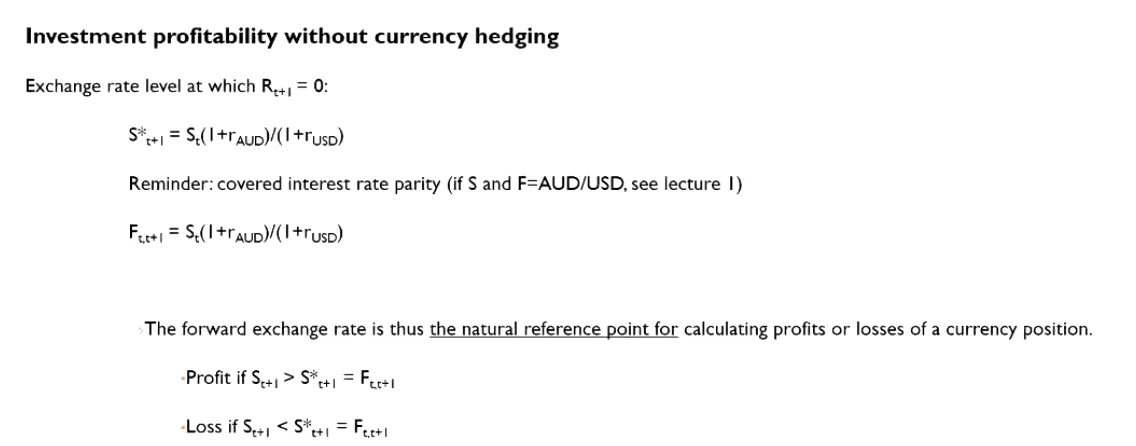

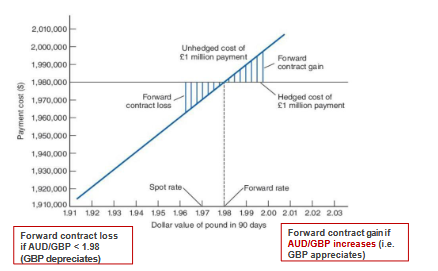

Investment profitability without currency hedging

The return has two drivers: the interest rate differential and the currency movement. USD appreciation boosts returns; depreciation hurts them.

Interest rate differential: When converting, one earns the USD interest rate instead of the AUD rate. If R_usd > R_aud, already profitable before currency moves

Profit if the USD ends up stronger than the forward rate predicted as converting back to AUD at a better rate than expected.

The break-even rate is the future exchange rate at which these two effects exactly cancel out — where what you gained from the interest rate differential is precisely wiped out (or matched) by the currency move, leaving you with zero excess return. That break-even point turns out to equal the forward exchange rate.

Loss if the USD ends up weaker than the forward rate predicted getting less AUD when converting back than the forward rate implied.

Real return always compared against the forward rate

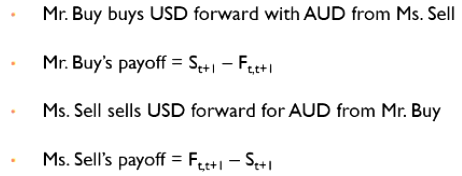

Forward Contracts

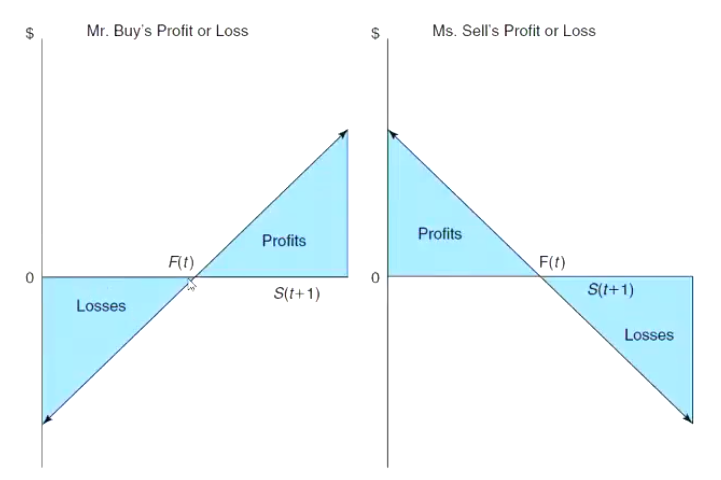

Is an agreement between two parties to buy or sell a security (or currency) at a pre-specified price on a pre-specified date T.

Party agreeing to buy (sell) the underlying currency in the future is said to “buy (sell) a forward” and will have a long (short) position in that currency

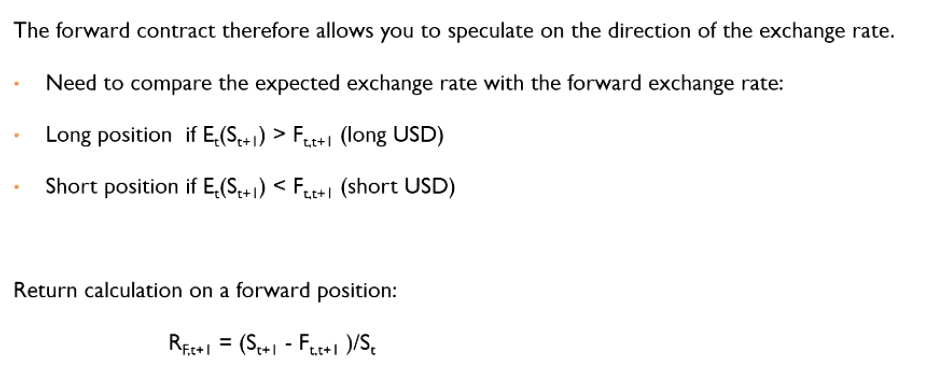

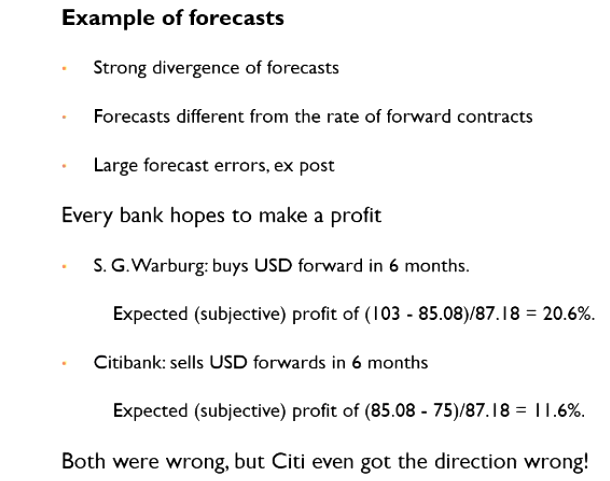

Speculation Strategy based on the direction of exchange rate

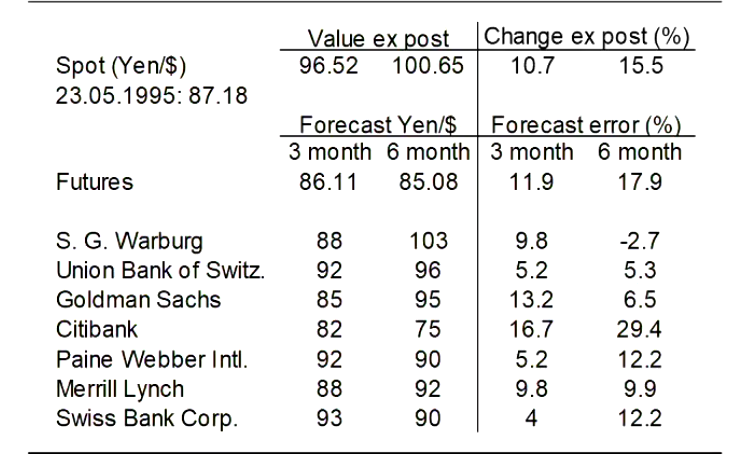

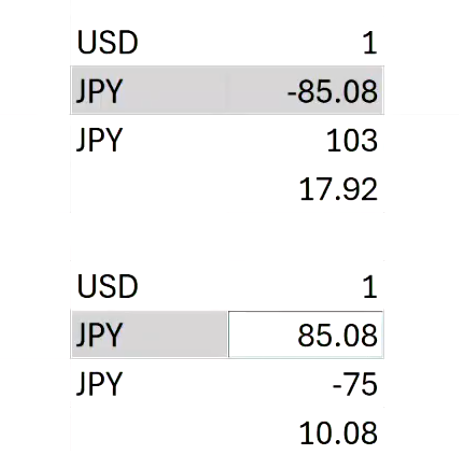

Example of Forecasts and speculation transaction

Note: Example evaluates Warburg and Citi predictions

Usefulness of professional forecasts

Generally there is some ability to predict future movements in the exchange rate (and in the right direction)

Forecasters do this by:

Extrapolating recent trends (technical analysis), while at longer horizons they tend to forecast a return to a long term equilibrium, such as PPP.

Capture information like:

real exchange rate

ratio of current account balance to GDP

currency risk premium

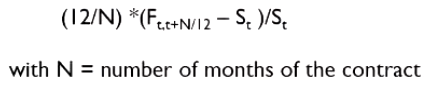

Forward rate premium and discounts

USD is quoted at a forward premium if forward rate is higher than spot rate

USD is quoted at a forward discount if forward rate is lower than spot rate

Basically pay more AUD for one USD in the future if there is a premium

The forward rate is typically annualised and in %

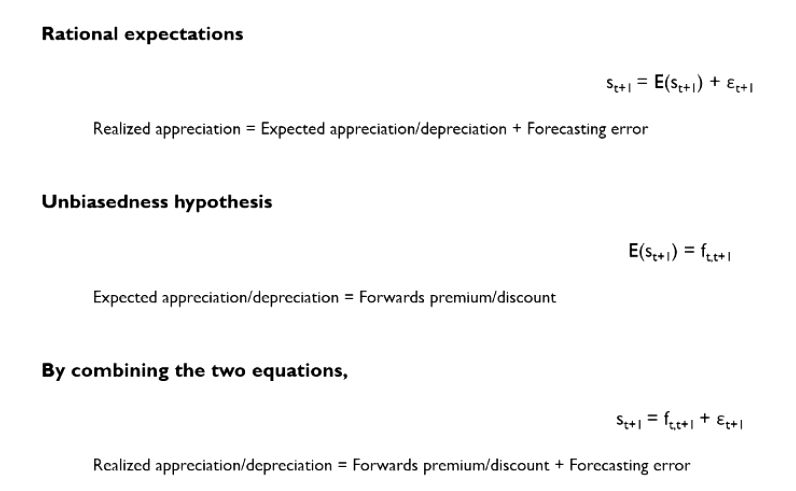

Forward exchange rate as a predictor of the future spot rate

Recall

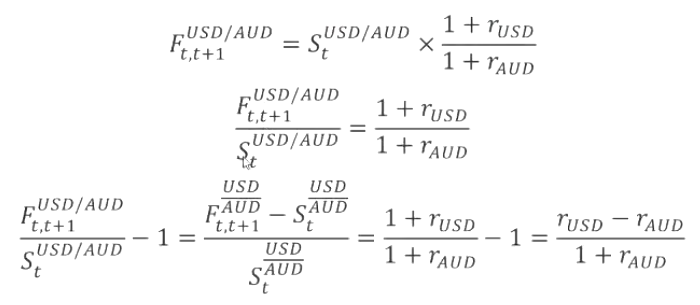

CIP: Ft,t+1 = St (1+raud) / (1+rusd)

UIP: Et (St+1) = St (1+raud) / (1+rusd)

with S and F expressed as AUD/USD (AUD for 1 USD)

Combine UIP with CIP: Et (St+1) = Ft,t+1

Et (St+1) - St = Ft,t+1 - St

Expected currency return: Et (St+1) - St / St

Forward premium: Ft,t+1 - St / St

Et (St+1) = ft,t+1

rtAUD - rtUSD, S = AUD/USD

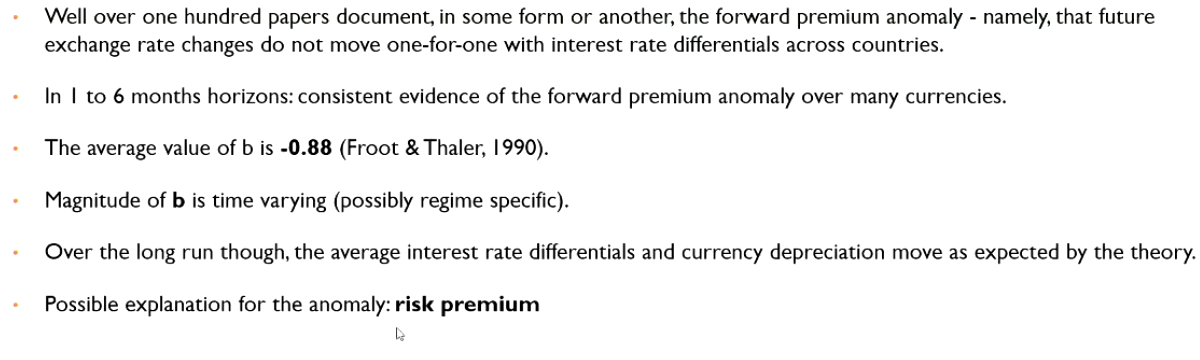

UIP (together with CIP) implies that forward exchange rate is an unbiased predictor of the future spot exchange rate

Forecast error = 0 on average

Economic background behind the forward exchange rate

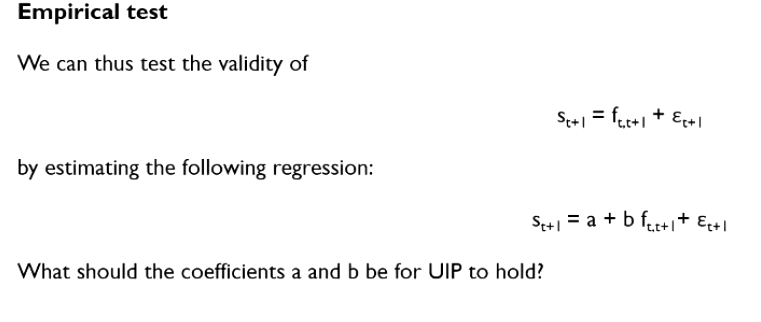

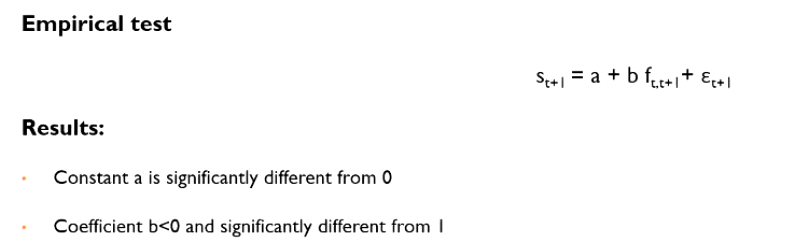

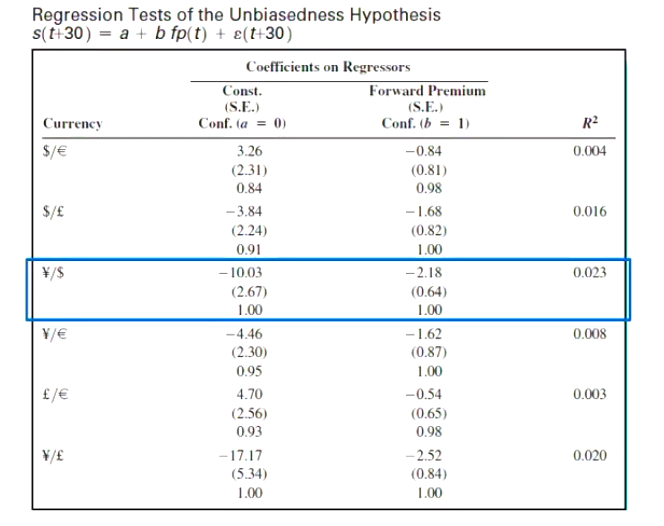

Empirical Test behind forward premium theory

Interpretations:

a = -10.03 USD at a discount because RJPY < RUSD, therefore USD depreciates on average

b = -2.18 if USD becomes more at a discouint because RJPY - RUSD is more than < 0, USD should depreicate but it appreciates

Implications:

the constant (a) is in the right direction (higher interestr rate currencies depreciate on average in the long run)

the slope (b) suggests that UIP does not hold in short-term: countries with higher interest rates = future currency appreciation

This may be due to the risk premium

Risk Premiums

Assumes that the true model of exchange rate changes is

Et (St+1) = Ft,t+1 + RPt

where RPt is a risk premium adjustment

if risk premium is always 0, UIP Holds

But we have seen it fail empirically

In practice RPt is often positive when ft,t+1 is negative

AUD depreicates in bad times against JPY so RPt > 0

Domestic inteest rates (AUD) are higher than foregin interest rates (JPY) So ft,t+1 < 0

Forecasting techniques

Fundamental Analysis

Econometric / Statistical models

Economic and financial fundamentals

Technical Analysis

Chartists (patterns)

Statistical analysis (filters, momentum, regressions)

Technical Analysis

The idea that currencies follow trends and reversals

The majority of strategies are based on the temporal evolution of a currency

Filter-based strategies

to distinguish trrends and reversals from noise

Typically economists have a negative view of this method as it is inconsistent with the efficient market hypothesis

Typically short term and used by retail traders

In the long term fundamental analysis is always favoured

Hedging with Forward Contracts vs Money Market — Which to Choose?

Forward Contract = (Amount × Forward rate) / Domestic interest rate

Forward contract → use forward rate and domestic interest rate

Money Market = (Amount / Foreign interest rate) × Spot rate

Money market → use foreign interest rate and spot rate

Never mix rates between the two methods

Foreign Currency Risk Premium & Domestic Currency Return

Risk Premium (approximation):

Expected exchange rate appreciation − Interest rate differential = Expected appreciation − (r_domestic − r_foreign)

UIP holds if: risk premium = 0 (expected appreciation = interest rate differential) UIP does not hold if: risk premium ≠ 0

Domestic Currency Return on Foreign Bond (two methods):

Method 1: Domestic rate + Risk premium Method 2: Foreign rate + Expected appreciation

Method 2: Foreign rate + Expected appreciation

Both give the same answer

Example:

UK rate 5%, Swiss rate 3.75%, expected CHF appreciation 2%

Risk premium = 2% − (5% − 3.75%) = 0.75%

UIP does not hold

Domestic return = 3.75% + 2% = 5% + 0.75% = 5.75%

Forward and Future contract

A promise to buy or sell a specific quantity of a currency on a specific date

Characteristics of Forward Contracts

Private agreement between two parties (OTC)

Terms of the contract specific to the needs

Fixed maturities: 1,2,3,6, or 12 months

Large contracts

Significant credit (counterparty risk)

As it is only between two parties, there is always a risk that the other party may go bankrupt, hence not be able to pay

Main actors are typically large institutions

Banks, Hedge funds, MNCs

No quotes → no secondary market

Fixed and non-reversible position unless there is mutual agreement between parties

No action until contract expiry

No margin call but a large initial deposit is required

Its main use is to receive currency at a predetermined price

Prices are derived from the CIRP (see flashcard)

Characteristics of Future Contracts

Contracts are traded on a organised exchange (CME)

Standardised contracts

Small sizes

Fixed expiry date

4x per year: Mar, Jun, Sep, Dec: IMM Dates (3rd Wed of the month)

High daily liquidity but not enough for a large player (>100 Million USD position)

Price is quoted around the clock as positions are marked to market

Easy to close position even before maturity

No credit risk but maintain a margin account

Guarantees the counterparty the payment of future losses and risk of possible margin calls

Mainly used for heading and short term speculators

Currency is rarely physically received or delivered

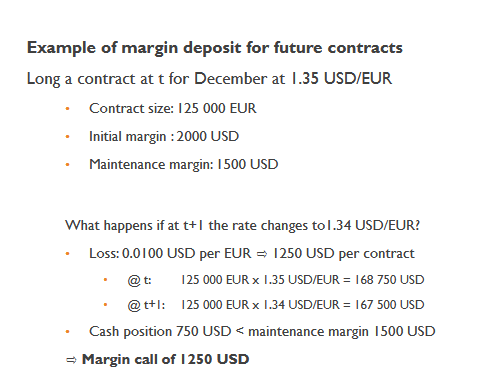

Betting on the uncertainty of timing and amount

Initial margin

Amount to be deposited when the contract is bought / sold

Depends on exchange rate volatility

USD 1000 to 4000 per contract on CME

Typically cash or collateral (gov bonds)

Shares listed at NYSE or physical gold can also be margin

Valued only at 70% of current value though

There is an oppoiortnity cost if the initla margin did not come from colateral (foregone interest)

Maintenance margin

Minimum margin level required each day

70 to 100% of the initial deposit level

The client must cover his / her loss

the contract can be closed if necessary

Example:

Main participants

Arbitragers

Seek to earn risk free profits by taking advantage of differences in interest rates amongst countries

Use forward contrats to eliminate the exchange rate risk

Commercial traders / hedgers

use forward contracts to elimintate or cover the risk of loss on export / import orders

Mostly MNCs

Speculators

Make profits from FX fluctuations

Currency Swaps

Fixed for fixed currency swap

Exchange of interest payments and capital in one currency to interest payment sand capital into another currency

Characteristics:

Private agreement between a client and a bank (OTC)

Appear off balance sheet

No secondary market

Reversible position only by mutual agreement