Unit 2 - AP Microeconomics Vocabulary

1/115

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

116 Terms

Demand

consumers’ ability and willingness to pay for a good or service

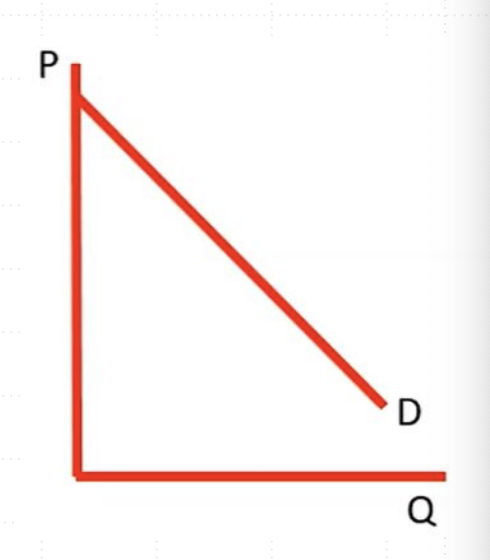

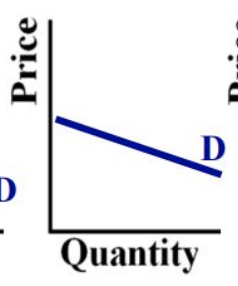

Law of Demand

a decrease in the price of a good causes an increase in the quantity demanded

Law of Demand: As price falls from P1 to P2,

quantity demanded increases from Q1 to Q2

Law of Demand: As price increases from P2 to P1,

quantity demanded decreases from Q2 to Q1

Price and Quantity (demanded) are our ___

variables

Draw Law of Demand graph

What happens if the price of a good changes?

The existing demand curve can show the new quantity demanded.

What happens if something other than price changes?

A new demand curve is needed.

Can the current demand curve handle changes in price?

Yes, it can show the new quantity demanded when price changes.

If demand changes, this is a shift in the ___

demand curve

If quantity demanded changes, this is a ____

movement along the demand curve.

Why does a demand curve slope downward?

Diminishing Marginal Utility, Income Effect, & Substitution Effect

Diminishing Marginal Utility

As more units of a good are consumed, the utility from each additional unit decreases, leading people to pay less for each subsequent unit.

Income Effect

When the price of a good falls, consumers experience an increase in purchasing power

Substitution Effect

When the price of a good increases, consumers switch to (substitute) less expensive alternatives.

Market demand

adding together the quantities that all consumers in the marketplace are willing to buy at each price

What causes a shift in demand?

1. Tastes and Preferences

2. Number of Consumers

3. Price of Related Goods

4. Income

5. Future Expectations

Substitutes

used in the place of the other

If the price of one increases, the demand for the other will increase (or vice versa).

Complements

two goods that are bought for the other will increase (or vice versa)

If the price of one increase, the demand for the other will fall (or vice versa).

Normal Goods

As income increases, demand increases

As income falls, demand falls

Inferior Goods

As income increases, demand falls

As income falls, demand increases

Future Expectations

If you expect the price to increase soon, you are more likely to go out and buy something now.

If you expect the price to decrease, you will wait for the price drop and decrease current consumption.

Demand is on whose side?

Consumers

Supply is on whose side?

Producers

Supply

the relationship between a good’s price and the quantity supplied by producers/sellers

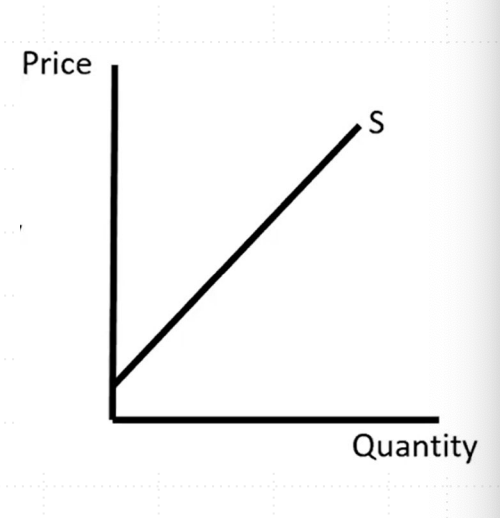

Law of Supply

an increase in the price of a good causes an increase in the quantity supplied

Draw Law of Supply Curve

Law of Supply: As price falls from P1 to P2,

quantity supplied decreases from Q1 to Q2

Law of Supply: As price increases from P2 to P1,

quantity supplied increases from Q2 to Q1

Long run

period of time long enough that anything can be changed.

Short run

the period before the long run, when some things may be fixed.

5 Shifters (Determinants) of Supply

Prices/Availability of inputs (resources)

Number of Sellers

Technology

Government Action: Taxes & Subsidies

Expectations of Future Profit

Taxes

raise the market price of a good, across all prices; but the

government gets the extra money, not the firm.

The firm will sell fewer units; they don’t like taxes.

Subsidies

government payments to firms to encourage particular industries or goods.

The firm gets extra money for selling that good, so they will produce more units.

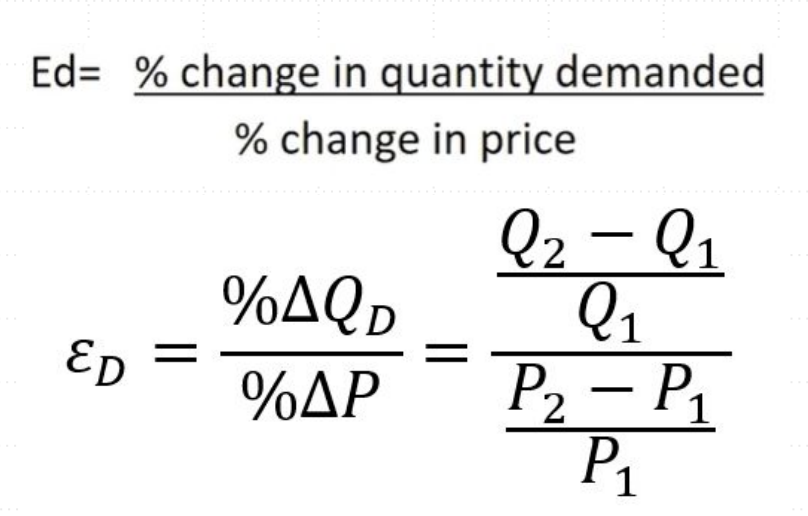

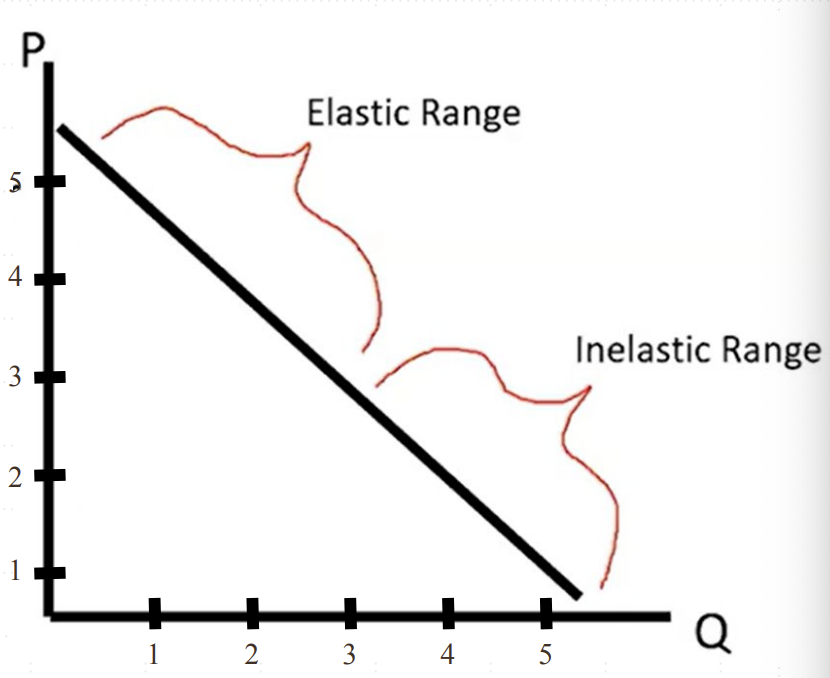

Price Elasticity of Demand/Supply

Measure of how responsive quantity demanded/supplied is to changes in price

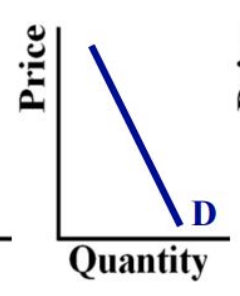

Elastic Demand

A price increase causes a large decrease in quantity demanded

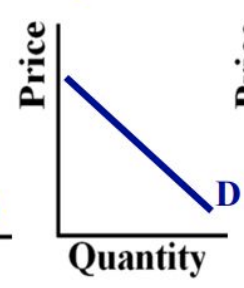

Inelastic Demand

A price increase causes a small decrease in quantity demanded

Price Elasticity of Demand FORMULAS (2)

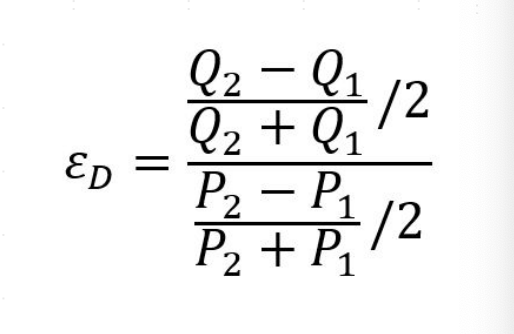

Midpoint Formula for Elasticity

Where is the elastic range and inelastic range on graph?

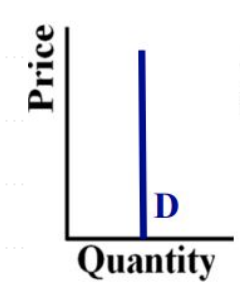

Perfectly inelastic value

0

Relatively Inelastic value

<1

Unit Elastic value

1

Relatively Elastic

>1

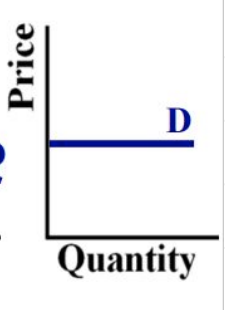

Perfectly Elastic

Infinite

Total Revenue =

Price * Quantity

Inelastic means arrows for price and TR are

facing same direction

Elastic means the arrows for price and TR are

opposite direction

Determinants of Elasticity

Availability of Close Substitutes

Necessity vs, Luxury

Percentage of Budget

Time

Availability of Close Substitutes

Demand is more elastic if there are many substitutes.

Necessity vs. Luxury

Demand is more inelastic if you need the good.

Percentage of Budget

Demand is more elastic for larger purchases.

Time

Demand is more inelastic when you have to make a decision quickly (and because you have less time to wait for a price change).

Elastic supply

A price increase causes a large increase in quantity supplied

Inelastic supply

A price increase causes a small increase in quantity supplied

Price of Alternative Input

supply is more elastic if it is easy to find alternative inputs.

Time

supply is more elastic when producers have more time to adjust to price changes

The absolute value of the price elasticity of supply increases when…

the price of alternative inputs decreases

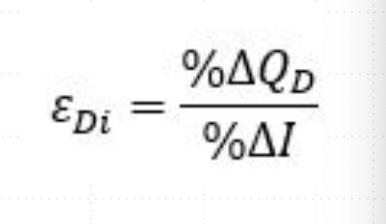

Income Elasticity of Demand

Measure of how responsive quantity demanded is to changes in income(don’t take absolute value anymore!)

Income Elasticity of Demand: If the result is positive…

the good is normal - (quantity increases as income increases).

Income Elasticity of Demand: If the result is negative…

the good is inferior - (quantity decreases as income increases).

Queens (Quantity) over

Peasants (Price)

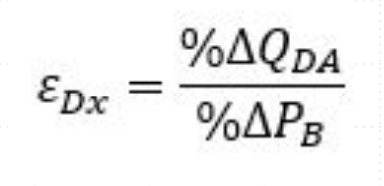

Cross-Price Elasticity of Demand

Measure of how responsive quantity demanded of one good is to changes in price of another good.

Cross-Price Elasticity of Demand: If the result is positive…

the goods are substitutes.

Cross-Price Elasticity of Demand: If the result is negative…

the goods are complements.

Market Equilibrium - where is it found?

the Demand curve and the Supply curve intersect: Qd = Qs at this price

Market Equilibrium

Consumers want to purchase the same amount producers want to sell

No shortages or surpluses

Qe is equilibrium quantity, Pe is equilibrium price

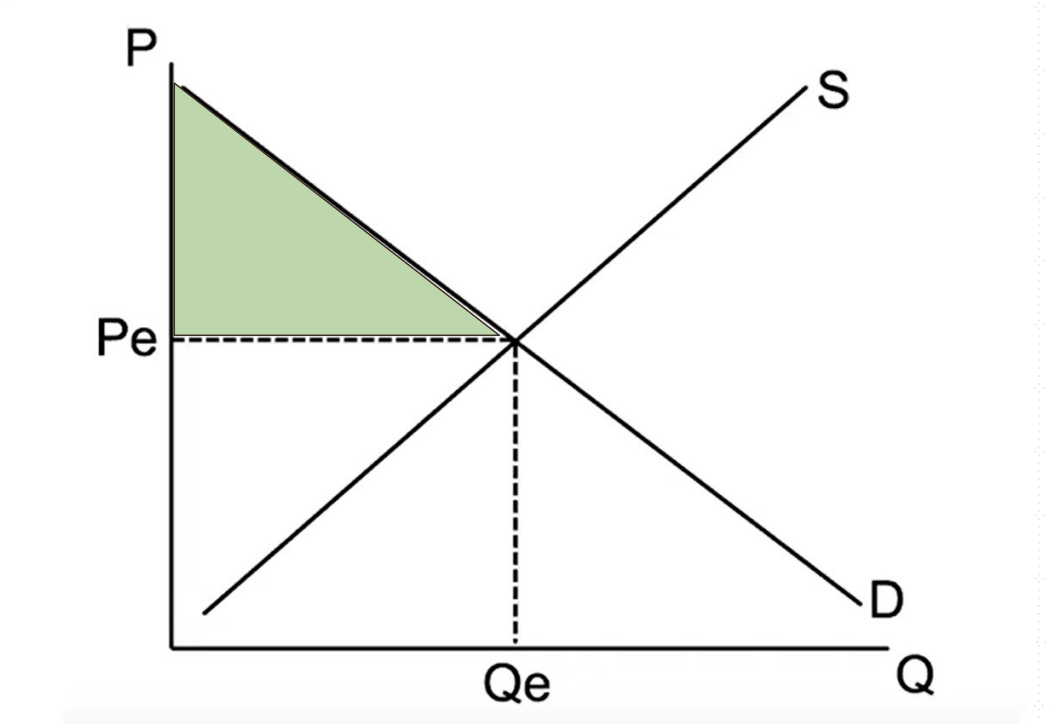

(2.6) Consumer Surplus

the benefit to consumers from paying less than the price they are willing to pay; consumers benefit from lower prices.

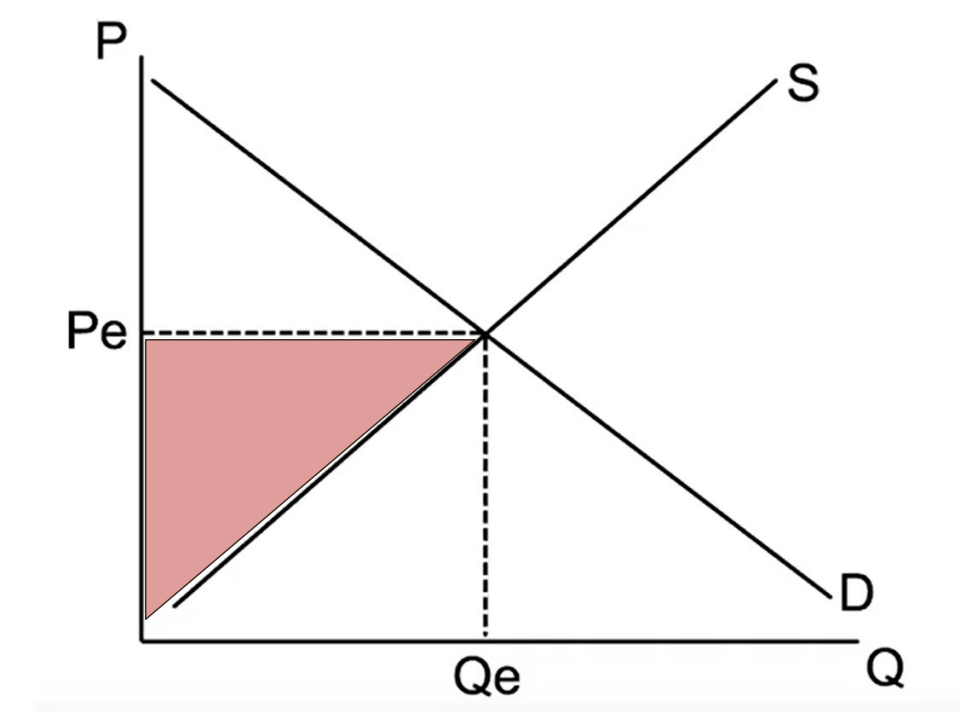

(2.6) Producer Surplus

the benefit to sellers from selling at a price higher than the price for which they’d be willing to sell; producers benefit from higher prices.

Total Surplus =

Consumer Surplus + Producer Surplus

Total surplus is _____ at market equilibrium.

maximized

Market Disequilibrium

Qd no longer equals Qs at the current price; total surplus is no longer maximized.

Shortage

When the quantity demanded is greater than the quantity supplied at the prevailing price

QD > QS

Consumers want to buy more units than producers want to sell

Surplus

When the quantity supplied is greater than the quantity demanded at the prevailing price

QS > QD

Producers want to sell more units than consumers want to buy

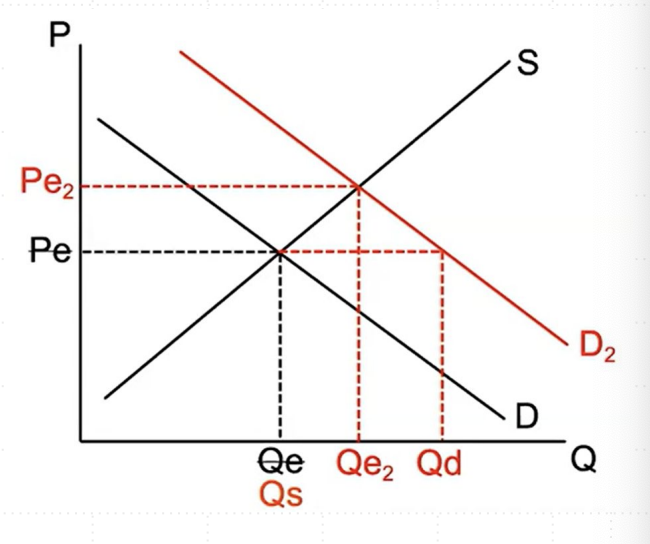

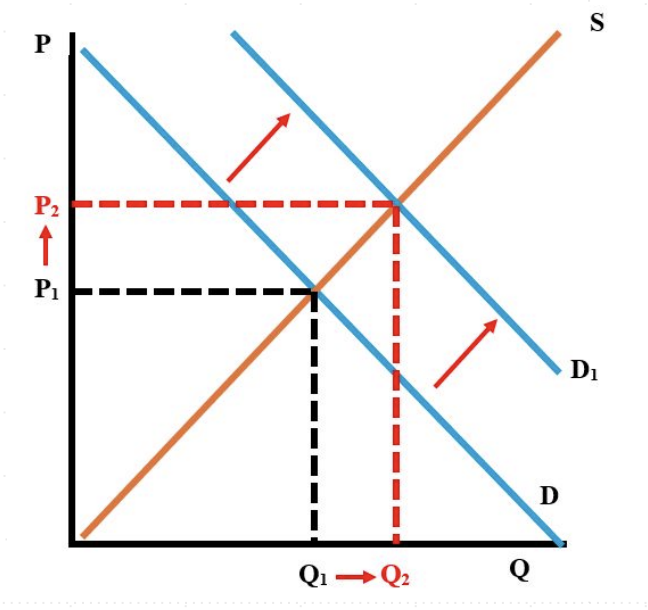

Increase in Demand

Initially creates shortage

(QD > QS at P1 )

Quantity increases Price increases

Decrease in Demand

Initially creates surplus

(QS > QD at P1 )

Quantity decreases Price decreases

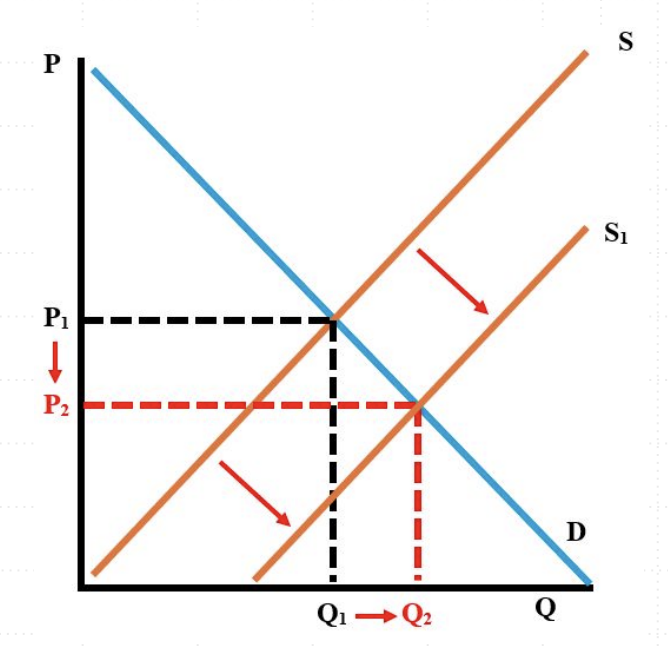

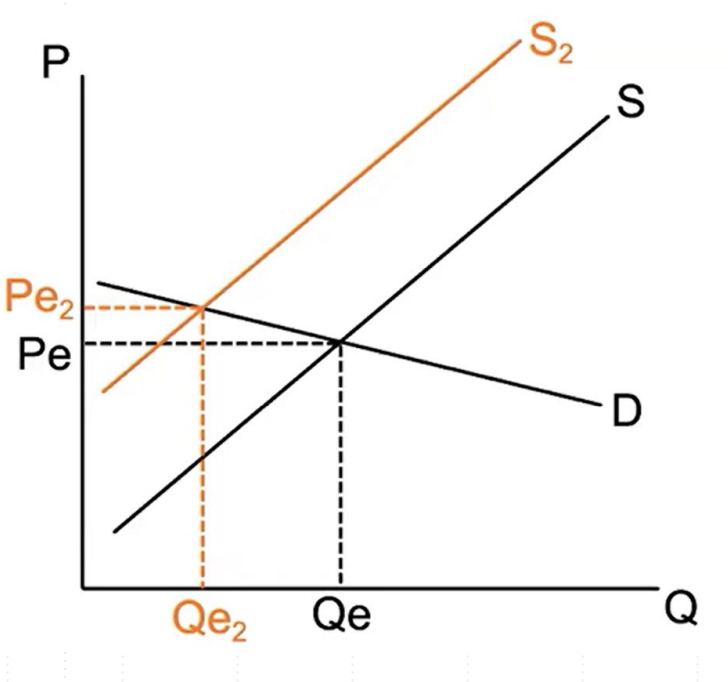

Increase in Supply

Initially creates surplus

(QS > QD )

Quantity increases Price decreases

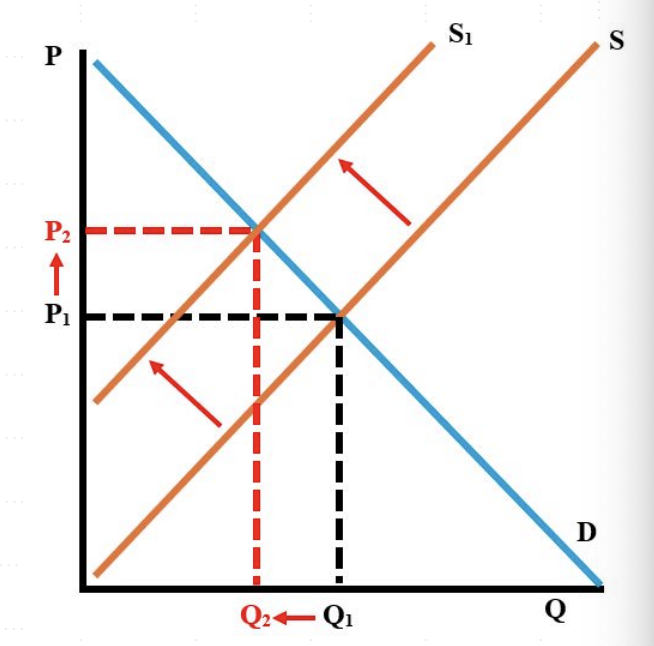

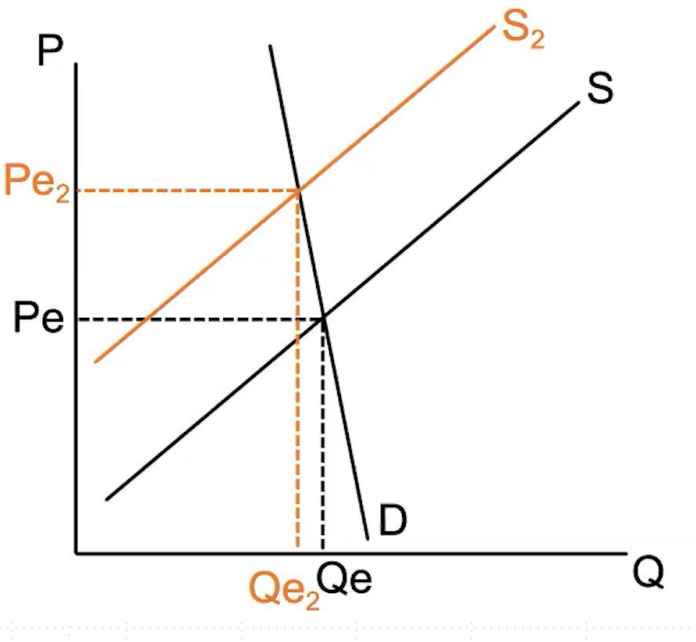

Decrease in Supply

Initially creates shortage

(QD > QS )

Quantity decreases Price increases

If both curves shift, either price or quantity will have a definite change and the other will be ______.

indeterminate

Elasticity and New Equilibria

The price elasticity of supply and demand will affect how large the change in the equilibrium will be after a curve shift.

Relatively elastic demand

small change in equil. price

large change in equil. quantity

Relatively elastic demand

large change in equil. price

small change in equil. quantity

For supply shifts…

the price elasticity of demadn affects the magnitude of the changes in price and quantity

For demand shifts…

the price elasticity of supply affects the magnitude of the changes in price and quantity

Changes in Surplus

Surplus changes when equilibrium changes; one of Consumer or Producer Surplus will increase or decrease depending on curve shifts.

Indeterminate Change

The change in the other surplus (Consumer or Producer) is indeterminate and cannot be determined with given information.

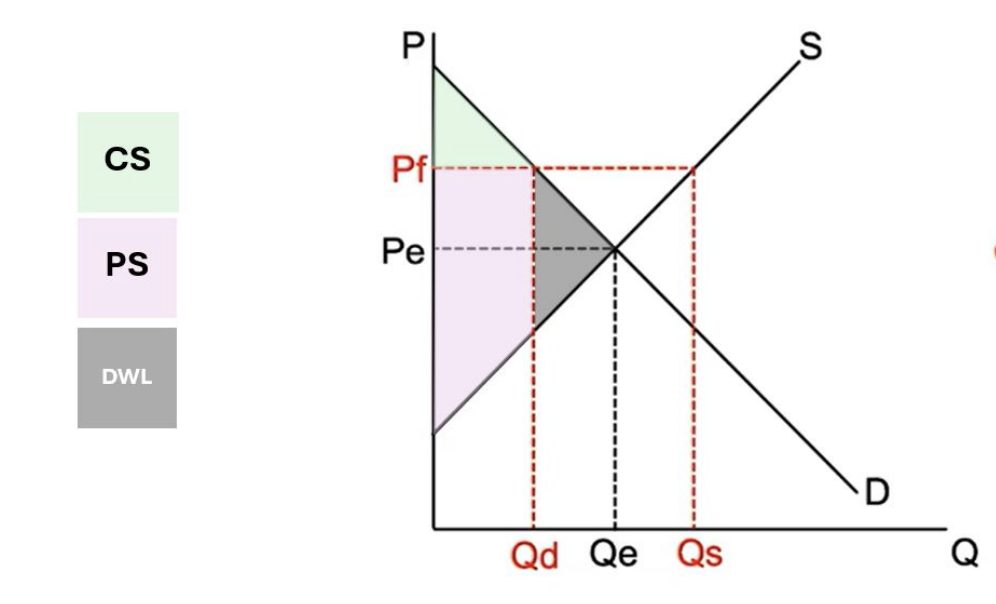

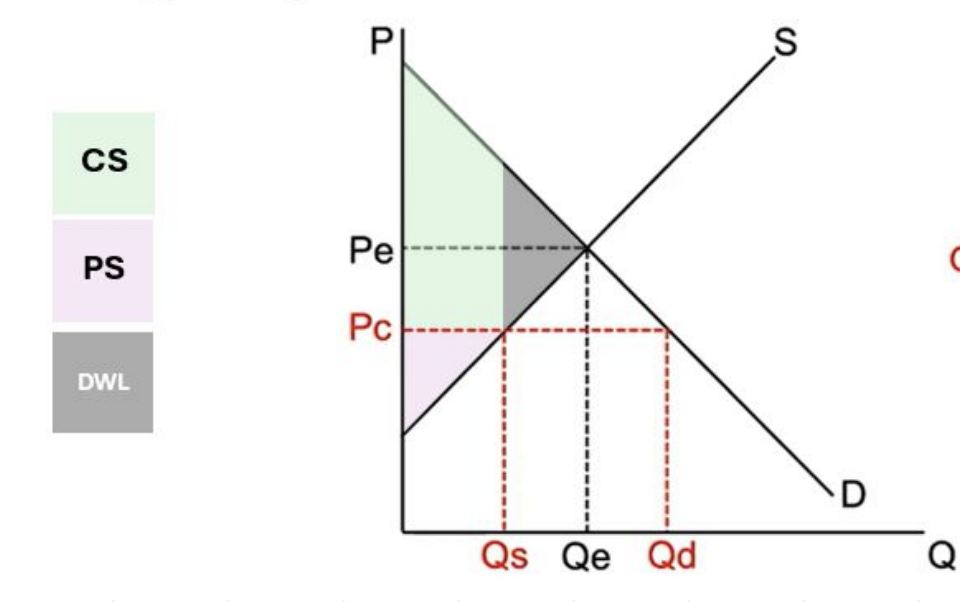

Price Ceiling

a legal upper limit (maximum) on the price that can be charged; must be below equilibrium price to be effective (binding)

Price Floor

a legal lower limit (minimum) on the price that can be charged; must be above equilibrium price to be effective (binding)

Quota

a limit on the quantity that can be sold in a market

Deadweight Loss

Loss in surplus due to non-equilibrium pricing, indicating allocative inefficiencyy

Allocative efficiency

not achieving optimal allocation of resources based on consumer preferences

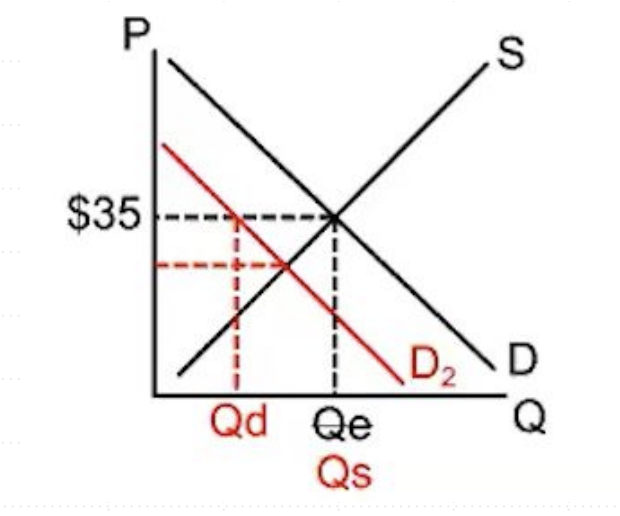

How does price floor graph look like? What is the calculation?

Qs - Qd = surplus

How does price ceiling graph look like? What is the calculation?

Qd - Qs = shortage

A ceiling must be ___ the equilibrium price.

below

A floor must be ___ the equilibrium price.

above

Excise tax

per-unit tax on the purchase of a good; this discourages production of that good

Subsidy

a per-unit cash transfer from the government for producing a good; this encourages production of that good.

We treat the tax as an ____ in the cost of production

increase