1.2 ~ Opportunity Costs

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

15 Terms

What is Opportunity Cost?

the value of the next best alternative that is forgone when making a decision

Choice

eg. time

What do you consider when Making CHOICES?

Benefits must outweigh the costs

Rational Decision making

What is Self-Interest in Decicion Making?

choices you make that you think are best for you

What is Social Interest in Decision Making?

choices that are best for society as a whole

What are Incentives?

rewards and penalties for choices and you are more likely to choose actions with rewards and avoid actions with penalties

What is a Free Good?

Any good that isn’t scarce

Anything that can be obtained without sacrificing something else

Free goods have zero opportunity cost

There goods are rare

Consumers can obtain all they want of these goods at no charge

Ex. air, sunlight

Types of Free Goods?

Public Goods (provided by the government

Produced by scarce resources and paid by our taxes (opportunity cost)

Common Pool Resources

Certain natural resources not owns by anyone by becomes scarce due to overuse and depletion

eg. clean air, forests, fish

What is an Economic Good?

any good that is scarce

Can be naturally occurring

Can be produced by scarce goods

All economic goods have an opportunity cost greater than zero

Most goods are economic goods

What is a “trade-off”?

For every good a nation produces, it faces a “trade-off” in terms of some other good it can no longer produce

This is because production of goods is limited by the amount of resources that exist (labour, capital and materials)

Three Basic Economic Questions

WHAT?

All must decide what particular good or service to produce and in what quantities

HOW?

All must decide how to use their resources in order to produce goods and services

FOR WHOM?

All must make choices about how the goods and services produced are to be distributed among the population

For whom to produce? (3)

Distribution of Output

How much of what is produced do different individuals or groups of individuals in the population receive

Distribution of Income

The amount of output people get depends on how much of it they can buy

This, in turn, depends on how much income they have

Redistribution of Income:

When the distribution of income our output changes so that different social groups now receive more, or less, income and output

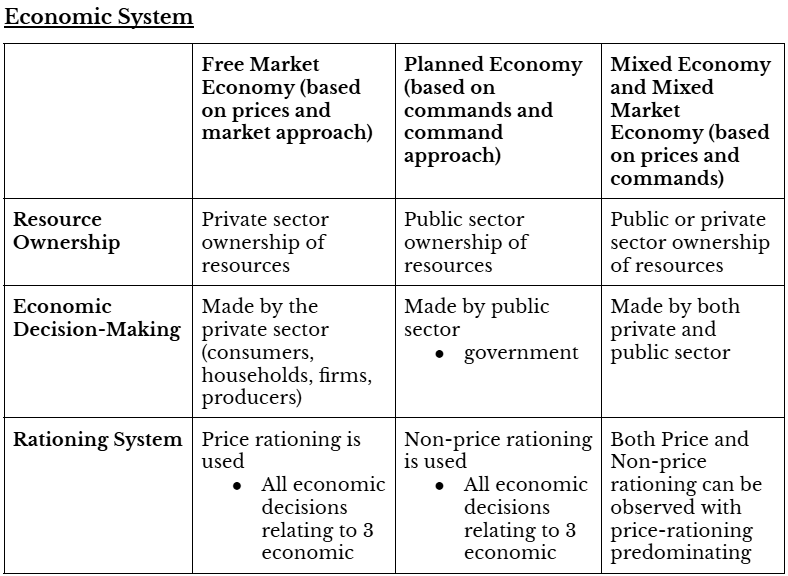

Market Method

Involves a private sector where resources are owned by private individuals or groups. Decisions are made by consumers and firms responding to prices determined in markets, about what, how, and for whom to produce.

Command Method

Involves a public sector where resources, particularly land and capital, are owned by the government. Decisions are made by commands from the government about what, how, and for whom to produce.

Mixed Economies

Real-world economies that combine elements of both market and command methods. The global trend is towards less government intervention, resulting in more reliance on market forces.

Economic System