Theme 1 Introduction to Markets and Market Failure

0.0(0)

Card Sorting

1/125

There's no tags or description

Looks like no tags are added yet.

Last updated 1:26 PM on 5/13/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

126 Terms

1

New cards

Ceteris Paribus

all other influencing factors are held constant

2

New cards

Neo-classical economists make a number of key assumptions in their analysis, including:

• people are rational;

• people (e.g. workers, business owners etc) aim to maximise their “utility” i.e. their ‘satisfaction’. For businesses, this means aiming to maximise their profit;

• people act independently of each other when making their decisions;

• the information needed to make decisions is always accurate and complete.

• people (e.g. workers, business owners etc) aim to maximise their “utility” i.e. their ‘satisfaction’. For businesses, this means aiming to maximise their profit;

• people act independently of each other when making their decisions;

• the information needed to make decisions is always accurate and complete.

3

New cards

Positive statements

objective statements that can be tested, amended or rejected by referring to the available evidence

Examples:

• If the government raises the tax on beer, this will then lead to a fall in profits of brewers.

• A fall in the cost of generating solar energy may cause a contraction of demand for coal

• A reduction in income tax will improve the incentives of the unemployed to find work.

• Higher mortgage interest rates will eventually reduce the average level of house prices

Examples:

• If the government raises the tax on beer, this will then lead to a fall in profits of brewers.

• A fall in the cost of generating solar energy may cause a contraction of demand for coal

• A reduction in income tax will improve the incentives of the unemployed to find work.

• Higher mortgage interest rates will eventually reduce the average level of house prices

4

New cards

Normative Statements

subjective statements – i.e. they carry value judgement

Examples:

• High unemployment is more harmful to a country such as the UK than high rates of inflation

• The retirement age in Britain should be raised to 70 to combat the effects of an ageing population.

• Scarce resources are best allocated by allowing the price mechanism to work without any intervention

• The government should enforce a minimum price for beers and lagers sold in supermarkets and off-licences to help control alcohol consumption and reduce the number of pubs that are closing

Examples:

• High unemployment is more harmful to a country such as the UK than high rates of inflation

• The retirement age in Britain should be raised to 70 to combat the effects of an ageing population.

• Scarce resources are best allocated by allowing the price mechanism to work without any intervention

• The government should enforce a minimum price for beers and lagers sold in supermarkets and off-licences to help control alcohol consumption and reduce the number of pubs that are closing

5

New cards

What is the basic economic problem?

The basic economic problem is about scarcity and choice i.e. economics is about coming up with ways to meet infinite wants when faced with finite resources.

Each society must decide:

• What goods and services to produce? Does the economy use its resources to build more hospitals, roads, schools or luxury hotels? Can the National Health Service afford free IVF treatment for childless couples or offer new but expensive cancer treatments? How should we source our energy in the years to come?

• How best to produce goods and services? What is the best use of our scarce resources? Should government land be sold off to provide more land for affordable housing? Should we subsidize the electric vehicles as a strategy to reduce carbon emissions from transport?

• Who is to receive goods and services? Who will get hospital treatment - and who not? Which areas get the go-ahead for major transport infrastructure projects such as CrossRail, HS2 and HS3 and which regions might miss out?

Each society must decide:

• What goods and services to produce? Does the economy use its resources to build more hospitals, roads, schools or luxury hotels? Can the National Health Service afford free IVF treatment for childless couples or offer new but expensive cancer treatments? How should we source our energy in the years to come?

• How best to produce goods and services? What is the best use of our scarce resources? Should government land be sold off to provide more land for affordable housing? Should we subsidize the electric vehicles as a strategy to reduce carbon emissions from transport?

• Who is to receive goods and services? Who will get hospital treatment - and who not? Which areas get the go-ahead for major transport infrastructure projects such as CrossRail, HS2 and HS3 and which regions might miss out?

6

New cards

What are the factors of production?

Capital: goods made by people that are used to supply other products e.g. machines, technology, factories, plant and software.

Enterprise: entrepreneurs organise factors of production and also take risks when seeking to exploit market opportunities.

Land: the stock of natural (environmental) factor resources available for production. Remember that this is any natural resource so this could, for example, include the sea or oil.

Labour: the quantity and quality of the human input into the production process

Enterprise: entrepreneurs organise factors of production and also take risks when seeking to exploit market opportunities.

Land: the stock of natural (environmental) factor resources available for production. Remember that this is any natural resource so this could, for example, include the sea or oil.

Labour: the quantity and quality of the human input into the production process

7

New cards

What is automation?

Automation is a production technique that uses capital machinery / technology to replace or enhance human labour. Replacing labour is known as capital-labour substitution. There have been many recent examples, for example robots in Amazon warehouses and grocery suppliers such as Ocado, that carry out “picking and packing”.

8

New cards

Non-renewable resources

Resources that are finite in supply, i.e crude oil, coal, natural gas, fossil fuels, etc.

9

New cards

Renewable resources

Resources that are replaceable if there ate of extraction is less than the natural rate at which a resource renews

10

New cards

Opportunity cost

the value of the next-best alternative when a decision is made; it's what is given up

11

New cards

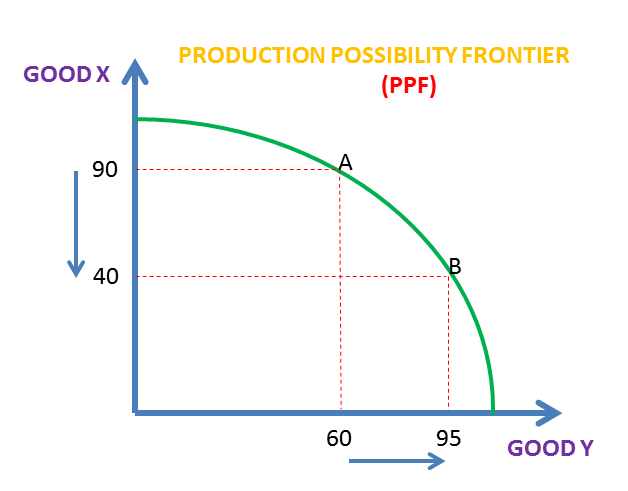

What is production possibility frontier (PPF)?

.essentially a graph that shows the maximum potential output combinations of two goods that an economy can achieve when all its resources are fully and efficiently employed. they also show the maximum potential output of combinations of two goods that a firm can achieve when it uses all its resources

12

New cards

Explain and describe the shaped of a PPF curve

.a PPF curve is drawn as concave to the origin (bowed outwards)

.this is because as you move along the PPF, as more resources are allocated towards Good X, then the extra output as we lose production of Capital Goods, gets smaller (diminishing marginal productivity sort of)

.this occurs because not all factor inputs are equally suited to producing different goods and services

.this is because as you move along the PPF, as more resources are allocated towards Good X, then the extra output as we lose production of Capital Goods, gets smaller (diminishing marginal productivity sort of)

.this occurs because not all factor inputs are equally suited to producing different goods and services

13

New cards

The PPF and economic efficiency

\-any point on the PPF represents a productively efficient allocation of scarce resources- all factors of production are being used in their most efficient way

\-Points inside the PPF represent an inefficient allocation of resources (its possible to produce more of one good without sacrificing any of the other

\-Points beyond the PPF are unattainable without an increase in factor resource, productivity or improvement in technology

★Specialisation, trade and exchange between countries and nations allows them to consume beyond their own PPF (theme 3)

\-Points inside the PPF represent an inefficient allocation of resources (its possible to produce more of one good without sacrificing any of the other

\-Points beyond the PPF are unattainable without an increase in factor resource, productivity or improvement in technology

★Specialisation, trade and exchange between countries and nations allows them to consume beyond their own PPF (theme 3)

14

New cards

Shifts in the PPF: (outwards)

Causes of an outward shift:

\-higher productivity/efficiency of factor inputs

.increases the output per unit of an input used in production

\-better management of factor inputs

.improved management reduces waste and also improves quality

\-increase in the stock of capital and labour supply

.e.g. from inward labour migration/increased capital investment

\-innovation and invention of new products and resources

.improved production processes help to lift efficiency

\-discovery/extraction of new natural resources (land)

.discovery of commercially viable land drives extraction

\-higher productivity/efficiency of factor inputs

.increases the output per unit of an input used in production

\-better management of factor inputs

.improved management reduces waste and also improves quality

\-increase in the stock of capital and labour supply

.e.g. from inward labour migration/increased capital investment

\-innovation and invention of new products and resources

.improved production processes help to lift efficiency

\-discovery/extraction of new natural resources (land)

.discovery of commercially viable land drives extraction

15

New cards

Shifts in the PPF: (inwards)

★overall, all causes are essentially falls in the productive potential of a country

\-natural disasters

\-war

\-emigration/ human capital flight

\-fall in the productivity of labour

\-natural disasters

\-war

\-emigration/ human capital flight

\-fall in the productivity of labour

16

New cards

Resource depreciation

when the productivity/efficiency of resources diminishes with age and also with repeated use when producing goods and services

17

New cards

Specialisation

when an individual, firm or country produces a narrow range of goods or services and over time develops a comparative cost advantage in producing these goods and services

18

New cards

Division of labour

.the breaking down of a production process of a good/service into smaller tasks, each of which is carried out by a different person/factor input.

.associated with Adam Smith

.associated with Adam Smith

19

New cards

Possible advantages of specialisation:

• Higher output: Total production of goods and services is raised, and quality can be improved

• Variety: Consumers have access to a greater variety of higher-quality products

• A bigger market: Specialisation and global trade increase the size of the market offering opportunities for economies of scale to be exploited, leading to lower unit costs and prices

• Variety: Consumers have access to a greater variety of higher-quality products

• A bigger market: Specialisation and global trade increase the size of the market offering opportunities for economies of scale to be exploited, leading to lower unit costs and prices

20

New cards

Possible disadvantages of specialisation:

1\. Unrewarding, repetitive work that requires little skill can lower motivation and eventually causes lower productivity.

2\. Workers may take less pride in work and quality suffers.

3\. Dissatisfied workers cause absenteeism to increase

4\. People move to less boring jobs creating a problem of high worker turnover and increased hiring/training costs

5\. Increased risk of repetitive strain injuries at work

6\. Some workers receive little training and may not be able to find alternative jobs when out of work – they suffer structural unemployment / occupational immobility

7\. Mass-produced standardized goods may lack variety

2\. Workers may take less pride in work and quality suffers.

3\. Dissatisfied workers cause absenteeism to increase

4\. People move to less boring jobs creating a problem of high worker turnover and increased hiring/training costs

5\. Increased risk of repetitive strain injuries at work

6\. Some workers receive little training and may not be able to find alternative jobs when out of work – they suffer structural unemployment / occupational immobility

7\. Mass-produced standardized goods may lack variety

21

New cards

Functions of money

1\. A medium of exchange - money is any asset widely acceptable as a medium of exchange. It facilitates transactions between buyer & seller. Specialisation and the division of labour require a means of exchanging goods and services.

2. A store of value - an asset that holds its value over time.

3\. A unit of account – money is a unit of measure used to value/cost products, assets (e.g. houses), debts, incomes and spending.

4\. A standard of deferred payment - the accepted way, in a given market, to settle a debt

2. A store of value - an asset that holds its value over time.

3\. A unit of account – money is a unit of measure used to value/cost products, assets (e.g. houses), debts, incomes and spending.

4\. A standard of deferred payment - the accepted way, in a given market, to settle a debt

22

New cards

Characteristics of money

1\. Durability i.e. it needs to last

2\. Portable i.e. easy to carry around, convenient, easy to use

3\. Divisible i.e. money can be broken down into smaller denominations to facilitate purchases

4\. Hard to counterfeit - i.e. it cannot easily be faked or copied by currency fraudsters

5\. Accepted i.e. money must be accepted as legal tender – there must be sufficient trust in money

6\. Valuable – i.e. it generally holds value over time and is not destroyed by the effects of rapid / hyper-inflation

2\. Portable i.e. easy to carry around, convenient, easy to use

3\. Divisible i.e. money can be broken down into smaller denominations to facilitate purchases

4\. Hard to counterfeit - i.e. it cannot easily be faked or copied by currency fraudsters

5\. Accepted i.e. money must be accepted as legal tender – there must be sufficient trust in money

6\. Valuable – i.e. it generally holds value over time and is not destroyed by the effects of rapid / hyper-inflation

23

New cards

Free market economy:

\-Market allocates resources through the price mechanism

\-there is a limited role for the government: they are restricted to protecting property right of people and businesses using the legal system and protecting the value of money or the value of a currency

★essentially there is no government intervention

\-there is a limited role for the government: they are restricted to protecting property right of people and businesses using the legal system and protecting the value of money or the value of a currency

★essentially there is no government intervention

24

New cards

Planned/command economy:

\-associated with a socialist or communist system

\-the government owns scarce resource

\-the state allocates resources and sets production targets and growth rates according to its own view of peoples’ wants

★Market prices play little or no part in informing resource allocation decisions and queuing rations scarce goods

\-the government owns scarce resource

\-the state allocates resources and sets production targets and growth rates according to its own view of peoples’ wants

★Market prices play little or no part in informing resource allocation decisions and queuing rations scarce goods

25

New cards

Mixed economy:

\-some resources are owned by the public sector (government) and some are owned by the private sector

\-the public sector typically provides public, quasi-public and merit goods, and intervenes to correct market failure

★Nearly all economies in the world are mixed, but this changes as some industries are privatised or nationalised

\-the public sector typically provides public, quasi-public and merit goods, and intervenes to correct market failure

★Nearly all economies in the world are mixed, but this changes as some industries are privatised or nationalised

26

New cards

Advantages of free market economies:

1\. An efficient allocation of scarce resources – factor inputs tend to go where the expected profit is highest, and in turn this represents the goods/services most desired by consumers (economists often link this to idea of consumer sovereignty).

2\. Competitive prices for consumers as suppliers look to increase and then protect their market share.

3\. Competition drives innovation & invention bringing higher profits for businesses and better products for consumers – economists often call this dynamic efficiency (you will meet this concept again in Theme 3).

4\. The profit motive stimulates investment which encourages economies of scale (i.e. lower unit costs in production) and, in turn, lower prices for consumers.

5\. Competition through trade helps to reduce domestic monopoly power and increases choice.

6\. Historically, economies with a large free-market aspect to resource allocation have grown more quickly than those with a command economy.

2\. Competitive prices for consumers as suppliers look to increase and then protect their market share.

3\. Competition drives innovation & invention bringing higher profits for businesses and better products for consumers – economists often call this dynamic efficiency (you will meet this concept again in Theme 3).

4\. The profit motive stimulates investment which encourages economies of scale (i.e. lower unit costs in production) and, in turn, lower prices for consumers.

5\. Competition through trade helps to reduce domestic monopoly power and increases choice.

6\. Historically, economies with a large free-market aspect to resource allocation have grown more quickly than those with a command economy.

27

New cards

Disadvantages of free market economies:

1\. Some members of society may be unable to work e.g. the elderly, those with disabilities or additional needs, parents with young children etc. Without government intervention, these people will likely live in poverty. This can create significant inequality in an economy.

2\. Goods that are bad for us (often called demerit goods) may be over-produced; these could include products such as cigarettes and alcohol. Similarly, products that are very good for us (often called merit goods) may not be consumed in large enough quantities; these could include healthcare and education (which will not be provided by the government in a completely free-market system).

3\. Because of the profit motive, firms may be tempted to cut costs, and so exploit labour (e.g. paying low wages or using child labour), use environmentally unsound production methods etc.

4\. Some firms may grow so large that they gain significant monopoly power, which allows them to charge very high prices to consumers, which could be unfair. Without government intervention, there may be no easy way to prevent this from happening.

5\. Public goods (which you will meet later in Theme 1) will not be provided. Examples include streetlights, free-to-use roads, lighthouses, flood defences etc.

2\. Goods that are bad for us (often called demerit goods) may be over-produced; these could include products such as cigarettes and alcohol. Similarly, products that are very good for us (often called merit goods) may not be consumed in large enough quantities; these could include healthcare and education (which will not be provided by the government in a completely free-market system).

3\. Because of the profit motive, firms may be tempted to cut costs, and so exploit labour (e.g. paying low wages or using child labour), use environmentally unsound production methods etc.

4\. Some firms may grow so large that they gain significant monopoly power, which allows them to charge very high prices to consumers, which could be unfair. Without government intervention, there may be no easy way to prevent this from happening.

5\. Public goods (which you will meet later in Theme 1) will not be provided. Examples include streetlights, free-to-use roads, lighthouses, flood defences etc.

28

New cards

Advantages of planned/command economies

1\. There is generally a low level of inequality and a low level of unemployment. Many command economies have had strong gender equality.

2\. Resources are allocated according to the ‘common good’ rather than according to the ‘profit motive’. This is likely to result in universal provision of healthcare and education, amongst other things.

3. It may be more straightforward / fast to get large-scale infrastructure projects built.

2\. Resources are allocated according to the ‘common good’ rather than according to the ‘profit motive’. This is likely to result in universal provision of healthcare and education, amongst other things.

3. It may be more straightforward / fast to get large-scale infrastructure projects built.

29

New cards

Disadvantages of planned/command economies

1\. Bureaucratic costs of central planning of resources – petty officialdom can lead to wasteful inefficiencies and therefore higher costs.

2\. Problems in fixing prices of goods and services – planners are unlikely to be as accurate as the market in determining suitable prices.

3\. Absence of incentives for both workers (i.e. no wage ‘differentials’) and businesses (i.e. no ‘profit motive’) can damage productivity and also lead to large levels of over-employment.

4\. Low productivity and weak incentives lead to rising losses for many state-owned businesses. The incentive to innovate is also limited.

5. Changing consumer needs and wants are not expressed as preferences in markets – the state is often slow to react to these

6\. The state can suffer from information failures and corruption 7. State-run economies are at higher risk of mal-investment driven by political motivations rather than market-assessed cost-benefit analysis

2\. Problems in fixing prices of goods and services – planners are unlikely to be as accurate as the market in determining suitable prices.

3\. Absence of incentives for both workers (i.e. no wage ‘differentials’) and businesses (i.e. no ‘profit motive’) can damage productivity and also lead to large levels of over-employment.

4\. Low productivity and weak incentives lead to rising losses for many state-owned businesses. The incentive to innovate is also limited.

5. Changing consumer needs and wants are not expressed as preferences in markets – the state is often slow to react to these

6\. The state can suffer from information failures and corruption 7. State-run economies are at higher risk of mal-investment driven by political motivations rather than market-assessed cost-benefit analysis

30

New cards

What are the assumptions of the rational choice model?

\-Rational consumers make choices with the aim of maximising utility

\-Consumers choose independently

\-A consumers has fixed and constant tastes and preferences, or transitive preferences

\-Consumers gather complete information on the alternative

\-Consumers always make an optimal choice given their preferences

\-Consumers choose independently

\-A consumers has fixed and constant tastes and preferences, or transitive preferences

\-Consumers gather complete information on the alternative

\-Consumers always make an optimal choice given their preferences

31

New cards

Total utility

the total satisfaction from a given level of consumption

32

New cards

Marginal utility

The additional satisfaction from consuming an extra unit

33

New cards

Diminishing marginal utility

states that if the consumption of a good or service increases, the satisfaction derived gradually increases but at a decreasing rate, to the point where it reaches zero. Total satisfaction is maximised when marginal utility is zero.

34

New cards

What is demand?

the quantity of a good or service that consumers are willing and able to buy at a given price in a given time period; effective demand is when a desire to buy id backed up by the ability to pay (demand usually refers to this)

35

New cards

What is derived demand?

the demand for a factor of production used to produce another good service, i.e. demand for land (steel) is affected by the demand for goods (cars or construction)

36

New cards

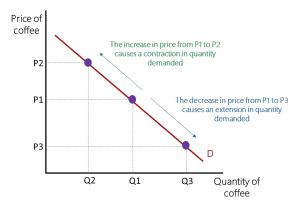

Law of Demand

There is an inverse relationship between the price of a good and demand

\-as price falls there is an extension of demand, as price rises there is a contraction of demand

\-as price falls there is an extension of demand, as price rises there is a contraction of demand

37

New cards

Why is the demand curve downward sloping?

1) The Income Effect: when the price of a good fall, the consumer can maintain the same consumption for less expenditure, effectively increasing their ‘real income’. Provided the good is normal, some of the ‘increase’ in real income is used to buy more

2) The Substitution Effect: when the price of a good falls, ceteris paribus, the product is now relatively cheaper than alternatives (substitutes) and some consumers will switch their spending to this now cheaper good/service; the more substitutes there are in the market and the lower the cost/inconvenience of switching, the bigger substitution effect is likely to be

3)The Law of Diminishing Marginal Utility: As more of a good consumed, the additional utility from each extra unit consumed falls; as consumers are assumed to be rational, they will not pay more for a good than the additional utility it provides

2) The Substitution Effect: when the price of a good falls, ceteris paribus, the product is now relatively cheaper than alternatives (substitutes) and some consumers will switch their spending to this now cheaper good/service; the more substitutes there are in the market and the lower the cost/inconvenience of switching, the bigger substitution effect is likely to be

3)The Law of Diminishing Marginal Utility: As more of a good consumed, the additional utility from each extra unit consumed falls; as consumers are assumed to be rational, they will not pay more for a good than the additional utility it provides

38

New cards

Draw a demand curve

39

New cards

What cause movements in along the demand curve?

\-A change in price

40

New cards

What causes shifts of the demand curve? (mnemonic)

Population: the larger the population, the higher the demand, changing the structure of the population also affects demand, such as the distribution of different age groups

Income: if consumers have more/less disposable income, they are able to afford more/less goods/services, so demand increase/decreases

Related goods: i.e. substitutes and complements. A substitute can replace another good, so if the price of a substitute falls, the demand for the original good will fall because consumers will switch to the cheaper option. A complement goes with another good, if the price of a complement increases, fewer people will buy the other good (demand falls) as they will be less of the good that increased in price

Advertising: this will increase consumer loyalty to the good and increase demand

Tastes and fashions: the demand curve will also shift if consumer tastes change: the demand for physical books might fall as consumers start to prefer reading e-books

Expectations: this of future price changes: if speculators and consumers expect the price of shares in a company to increase int he future demand will likely increase in the present

Seasons: demand changes according to season due to changing preferences, i.e. demand for ice cream in summer and demand for hot chocolate in winter

Income: if consumers have more/less disposable income, they are able to afford more/less goods/services, so demand increase/decreases

Related goods: i.e. substitutes and complements. A substitute can replace another good, so if the price of a substitute falls, the demand for the original good will fall because consumers will switch to the cheaper option. A complement goes with another good, if the price of a complement increases, fewer people will buy the other good (demand falls) as they will be less of the good that increased in price

Advertising: this will increase consumer loyalty to the good and increase demand

Tastes and fashions: the demand curve will also shift if consumer tastes change: the demand for physical books might fall as consumers start to prefer reading e-books

Expectations: this of future price changes: if speculators and consumers expect the price of shares in a company to increase int he future demand will likely increase in the present

Seasons: demand changes according to season due to changing preferences, i.e. demand for ice cream in summer and demand for hot chocolate in winter

41

New cards

What is joint demand?

when demand for one product is positively related to another: they are complements, i.e. fish and chips, pencils and rubbers, etc.

42

New cards

What is composite demand?

when goods have more than one use, and so an increase in the demand for one product leads to a fall in supply of the other, i.e. milk and cheese, yoghurt, butter or oil and fuel, plastics

43

New cards

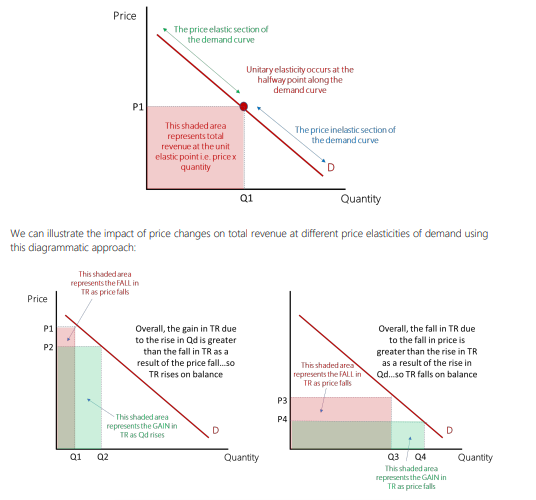

Price elasticity of demand (PED)

\-measures the responsiveness of quantity demanded in response to a change in the goods price

\-calculated as: percentage change in quantity demanded/percentage change in price

\-the coefficient of PED lies between 0 and -1, usually the minus is ignored

\-calculated as: percentage change in quantity demanded/percentage change in price

\-the coefficient of PED lies between 0 and -1, usually the minus is ignored

44

New cards

Interpreting the coefficient of PED

\-if PED is between 0 and -1 demand is price inelastic: demand is not particularly responsive to price changes (more vertically tilted)

\-if PED is 0, demand is perfectly inelastic: demand doesn’t change at all in response to price (perfectly vertical demand curve)

\-if PED is -1, demand is unit price elastic (perfect demand curve, diagonal line)

\-if PED is between -1 and -∞, demand is price elastic: demand responds more than proportionately to a change in price (more horizontally tilted)

\-if PED is -∞, demand is perfectly elastic: quantity demanded will fall to zero if the price rises (the demand is perfectly horizontal)

\-if PED is 0, demand is perfectly inelastic: demand doesn’t change at all in response to price (perfectly vertical demand curve)

\-if PED is -1, demand is unit price elastic (perfect demand curve, diagonal line)

\-if PED is between -1 and -∞, demand is price elastic: demand responds more than proportionately to a change in price (more horizontally tilted)

\-if PED is -∞, demand is perfectly elastic: quantity demanded will fall to zero if the price rises (the demand is perfectly horizontal)

45

New cards

Factors affecting PED

1\. Number of close substitutes – the more substitutes there are in the market, the more elastic is demand because consumers find it easy to switch. For example, air travel and train travel are weak substitutes for inter-continental flights but closer substitutes for journeys of 200-400km between major cities.

2\. Cost of switching between products – there may be costs involved in switching. In this case, demand tends to be inelastic. For example, mobile phone service providers may require a contract which has the effect of locking-in some consumers once a choice has been made.

3\. Degree of necessity or whether the good is a luxury – necessities tend to have an inelastic demand whereas luxuries tend to have a more elastic demand. An example of a necessity is rare-earth metals that are an essential raw material in the manufacture of solar cells, batteries. Another example might be essential medicines such as insulin for people with diabetes.

4\. Proportion of a consumer’s income allocated to spending on the good – products that take up a high % of income will have a more elastic demand.

5\. Time period allowed following a price change – demand is more price elastic, the longer that consumers have to respond to a price change. They have more time to search for cheaper substitutes.

6\. Whether the product is subject to habitual consumption – consumers become less sensitive to the price of the good when they buy something out of habit (it has become the “default choice”).

7\. Peak and off-peak demand - demand is price inelastic at peak times and more elastic at off-peak times – this is the case for transport services.

8\. Breadth of definition of a good or service – if a good is broadly defined, i.e. the demand for petrol or meat, demand is often inelastic. Individual brands of petrol or beef are likely to be price elastic.

9\. Method of payment – people tend to notice price changes more when they pay in cash rather than card, or direct debit.

2\. Cost of switching between products – there may be costs involved in switching. In this case, demand tends to be inelastic. For example, mobile phone service providers may require a contract which has the effect of locking-in some consumers once a choice has been made.

3\. Degree of necessity or whether the good is a luxury – necessities tend to have an inelastic demand whereas luxuries tend to have a more elastic demand. An example of a necessity is rare-earth metals that are an essential raw material in the manufacture of solar cells, batteries. Another example might be essential medicines such as insulin for people with diabetes.

4\. Proportion of a consumer’s income allocated to spending on the good – products that take up a high % of income will have a more elastic demand.

5\. Time period allowed following a price change – demand is more price elastic, the longer that consumers have to respond to a price change. They have more time to search for cheaper substitutes.

6\. Whether the product is subject to habitual consumption – consumers become less sensitive to the price of the good when they buy something out of habit (it has become the “default choice”).

7\. Peak and off-peak demand - demand is price inelastic at peak times and more elastic at off-peak times – this is the case for transport services.

8\. Breadth of definition of a good or service – if a good is broadly defined, i.e. the demand for petrol or meat, demand is often inelastic. Individual brands of petrol or beef are likely to be price elastic.

9\. Method of payment – people tend to notice price changes more when they pay in cash rather than card, or direct debit.

46

New cards

Revenue changes and PED

\-When demand is price inelastic, a price rise leads to a rise in revenue and vice versa

\-When demand is price elastic, a price rise leads to a fall in revenue and vice versa

\-When demand is perfectly inelastic, a price change, results in the same amount of revenue change

\-When demand is unit elastic, a change in the price leads to no change in the revenue

\-When demand is price elastic, a price rise leads to a fall in revenue and vice versa

\-When demand is perfectly inelastic, a price change, results in the same amount of revenue change

\-When demand is unit elastic, a change in the price leads to no change in the revenue

47

New cards

PED and the demand curve

\-As you go from left to right along the demand curve PED becomes more price inelastic, with the middle being unitary elasticity: this is because we are looking at proportional changes and not absolute changes

48

New cards

How can producers use PED?

They can predict:

\-changes in price on revenue

\-price volatility in a market following changes in supply

\-effect of a change in an indirect tax and price and demand and whether they can pass on most of the tax onto the consumer

\-they can also used PED for price discrimination

\-however it is difficult to calculate PED in reality

\-changes in price on revenue

\-price volatility in a market following changes in supply

\-effect of a change in an indirect tax and price and demand and whether they can pass on most of the tax onto the consumer

\-they can also used PED for price discrimination

\-however it is difficult to calculate PED in reality

49

New cards

Income elasticity of demand (YED)

\-measures the responsiveness of demand following a change in real income

\-calculated as percentage change in demand/percentage change in income

\-calculated as percentage change in demand/percentage change in income

50

New cards

Interpreting the coefficient of YED

\-Positive YED indicates a normal good: a good where demand rises at each price as consumers’ incomes rises

\-Normal necessities have a YED between 0 and 1, demand rises less than proportionately to income (income inelastic)

\-Luxury goods have a YED greater than 1, demand rises more than proportionately to a change in income (income inelastic)

\-Inferior goods have a negative YED, meaning demand falls as income rises, inferior goods/services exist where superior good are available, i.e. economy own label foods in supermarkets versus branded products (malted wheaties vs. shreddies)

\-Normal necessities have a YED between 0 and 1, demand rises less than proportionately to income (income inelastic)

\-Luxury goods have a YED greater than 1, demand rises more than proportionately to a change in income (income inelastic)

\-Inferior goods have a negative YED, meaning demand falls as income rises, inferior goods/services exist where superior good are available, i.e. economy own label foods in supermarkets versus branded products (malted wheaties vs. shreddies)

51

New cards

Examples of inferior goods

\-own label discounters

\-public transport

\-cigarettes

\-economy class travel

\-own-label cereal

\-economy foodstuffs

\-public transport

\-cigarettes

\-economy class travel

\-own-label cereal

\-economy foodstuffs

52

New cards

How do businesses make use of YED?

It helps them predict the effect of an economic cycle on sales, i.e. luxury products have higher sales volatility over a business cycle than necessities

53

New cards

Cross price elasticity of demand (XED)

\-measures the responsive of demand for good X in response to a change in price of good Y (a related good)

\-substitutes have a positive XED

\-complements have a negative XED

\-substitutes have a positive XED

\-complements have a negative XED

54

New cards

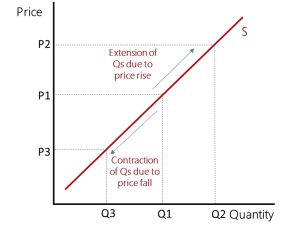

What is supply?

the quantity of a good or service producers are willing to supply at a given price in a given time period

55

New cards

Draw a supply curve

56

New cards

Explain the law of supply (why is the curve sloped upwards)

1\. Profit motive: When market price rises following an increase in demand, it becomes more profitable for businesses to increase their output

2\. Production and costs: When output expands, a firm’s production costs tend to rise; therefore, a higher price is needed to cover these extra costs of production. This may be due to diminishing returns as more factor inputs are added to production.

3\. New entrants into the market: Higher prices may create an incentive for other businesses to enter the market leading to an increase in total supply. (note – if businesses enter the market for any reason other than an increase in the price of the product, then the supply curve will shift to the right, rather than there being a movement along it

2\. Production and costs: When output expands, a firm’s production costs tend to rise; therefore, a higher price is needed to cover these extra costs of production. This may be due to diminishing returns as more factor inputs are added to production.

3\. New entrants into the market: Higher prices may create an incentive for other businesses to enter the market leading to an increase in total supply. (note – if businesses enter the market for any reason other than an increase in the price of the product, then the supply curve will shift to the right, rather than there being a movement along it

57

New cards

Factors that shift the supply curve (mnemonic)

Productivity: higher productivity causes and outward shift in supply as average costs for the firm fall so they can produce more at any given price

Indirect taxes and regulation: increases the cost of production, average costs increases causing a fall in supply at any given price

Number of firms: new entrants into a market increases supply putting downward pressure on price, business objectives can also affect this

Technology: more advanced technology causes an outward shift

Subsidies : decreases the cost of productions, causes an outward shift of supply

Weather: relevant for agriculture, favourable weather conditions increases supply

Costs of production: if costs of production fall, the firm can afford to supply more, if costs rise, such as wages increasing, there will be an inward shift of supply, similar effect with a depreciation of the exchange rate. lower costs of production can also be passed along the supply chain

Indirect taxes and regulation: increases the cost of production, average costs increases causing a fall in supply at any given price

Number of firms: new entrants into a market increases supply putting downward pressure on price, business objectives can also affect this

Technology: more advanced technology causes an outward shift

Subsidies : decreases the cost of productions, causes an outward shift of supply

Weather: relevant for agriculture, favourable weather conditions increases supply

Costs of production: if costs of production fall, the firm can afford to supply more, if costs rise, such as wages increasing, there will be an inward shift of supply, similar effect with a depreciation of the exchange rate. lower costs of production can also be passed along the supply chain

58

New cards

Competitive supply

goods and services in competitive supply are alternative products that a business could make with its factor resources

59

New cards

Joint supply

an increase/decrease in the supply of one good leads to an increase/decrease in supply of another, i.e beef and hide, sheep and wool, wheat and straw

60

New cards

Price elasticity of supply (PES)

\-measures the responsiveness of quantity supplied in response to a change in market price

\-calculated as % change in quantity supplied/ %change in price

\-calculated as % change in quantity supplied/ %change in price

61

New cards

Interpreting the coefficient of PES

\-When PES is greater than 1, supply is price elastic (more horizontally tilted)

\-When PES is less than 1, supply is price inelastic (more vertically tilted)

\-When PES is 0, supply is perfectly price inelastic (vertical curve)

\-When PES is ∞, supply is perfectly elastic (horizontal curve)

\-When PES is less than 1, supply is price inelastic (more vertically tilted)

\-When PES is 0, supply is perfectly price inelastic (vertical curve)

\-When PES is ∞, supply is perfectly elastic (horizontal curve)

62

New cards

Factors affecting PES

\-Spare production capacity: if there is plenty of spare capacity, a business can increase output without a rise in costs and supply will be elastic in response to a change in demand

\-Stock of finished products and components: if stocks of raw materials and finished products are at a high level, a firm is able to respond to a change in demand- supply will be elastic. Perishable goods are often harder/more expensive to store

\-Ease and cost of factor substitution/factor mobility: if capital and labour are occupationally mobile, the elasticity of supply will be higher as resources can be mobilised to supply extra output, this is more likely if the product is supplied by low-skilled labour

\-Time period and production speed: supply is more elastic the longer the time a firm has to adjust its production levels

a. The short-run for an economist refers to the period of time in which at least one factor of production is fixed; in the short-run, PES will be relatively inelastic

b. The long-run for an economist refers to the period of time in which all factors of production are variable; in the long-run, PES will be relatively elastic

\-Complexity of the production process: if a production process is particularly complex (building an airplane), then supply will be relatively price inelastic

\-Stock of finished products and components: if stocks of raw materials and finished products are at a high level, a firm is able to respond to a change in demand- supply will be elastic. Perishable goods are often harder/more expensive to store

\-Ease and cost of factor substitution/factor mobility: if capital and labour are occupationally mobile, the elasticity of supply will be higher as resources can be mobilised to supply extra output, this is more likely if the product is supplied by low-skilled labour

\-Time period and production speed: supply is more elastic the longer the time a firm has to adjust its production levels

a. The short-run for an economist refers to the period of time in which at least one factor of production is fixed; in the short-run, PES will be relatively inelastic

b. The long-run for an economist refers to the period of time in which all factors of production are variable; in the long-run, PES will be relatively elastic

\-Complexity of the production process: if a production process is particularly complex (building an airplane), then supply will be relatively price inelastic

63

New cards

What is meant by market equilibrium?

a state of equality or balance between market demand and supply

64

New cards

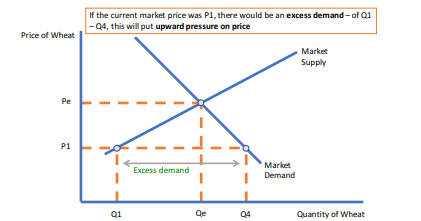

Disequilibrium- excess demand

\-when demand exceeds available supply

\-occurs when the current market price is below the equilibrium price

\-this results in queuing and upward pressure on price

\-occurs when the current market price is below the equilibrium price

\-this results in queuing and upward pressure on price

65

New cards

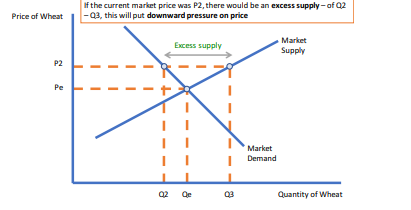

Disequilibrium- excess supply

\-when supply is greater than demand and there are unsold goods in the market (sometimes known as ‘glut’)

\-puts downwards pressure on price

\-as prices fall, there is an extension of demand which cuts the surplus and takes a market towards an equilibrium

\-puts downwards pressure on price

\-as prices fall, there is an extension of demand which cuts the surplus and takes a market towards an equilibrium

66

New cards

The Price Mechanism and its functions

\-the price mechanism describes how decisions taken by consumers and businesses interact to determine the scarce resources between competing uses

\-Adam Smith descried it as an invisible hand that, through the pursuit of self interest, allocates resources in society’s best interests

\-performs three main functions: signalling, incentivizing, rationing

\-signalling: if prices rises, this signals producers to expand supply, if there is excess supply, this signals to producers to contract supply

\-incentives: higher prices incentivize producers to increase supply (profit motive), lower demand incentivizes producers to contract supply

\-rationing: excess demand signals to producers to ration their good to those with effective demand

\-Adam Smith descried it as an invisible hand that, through the pursuit of self interest, allocates resources in society’s best interests

\-performs three main functions: signalling, incentivizing, rationing

\-signalling: if prices rises, this signals producers to expand supply, if there is excess supply, this signals to producers to contract supply

\-incentives: higher prices incentivize producers to increase supply (profit motive), lower demand incentivizes producers to contract supply

\-rationing: excess demand signals to producers to ration their good to those with effective demand

67

New cards

Secondary markets

Occurs when buyers and sellers are prepared to sue a second market to re-sell items that have already been purchased

68

New cards

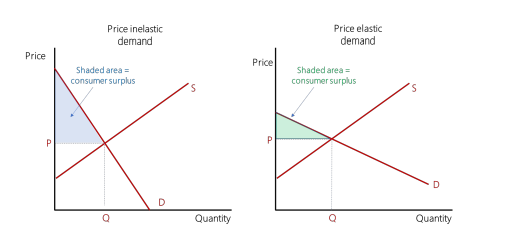

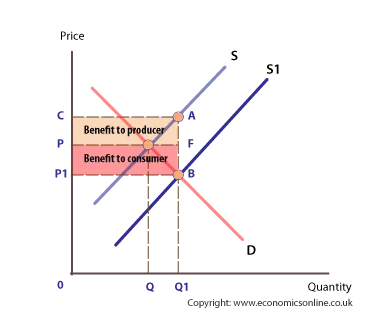

Consumer surplus

\-a measure of the welfare that people gain from consuming goods and service: the difference between the maximum that consumers are willing and able to pay for a good/service and what they actually pay

\-on a supply and demand diagram it is represented by the area underneath the demand curve an above the market price

\-on a supply and demand diagram it is represented by the area underneath the demand curve an above the market price

69

New cards

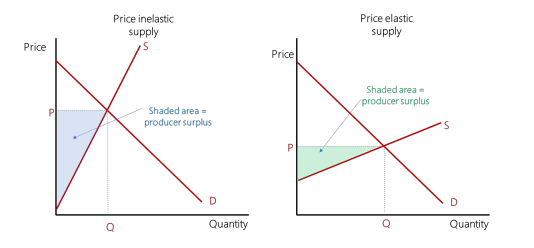

Producer surplus

\-the difference between the price producers are willing and able to supply a product for and the price they get in the market

\-shown by the are above the supply and below the market price

\-shown by the are above the supply and below the market price

70

New cards

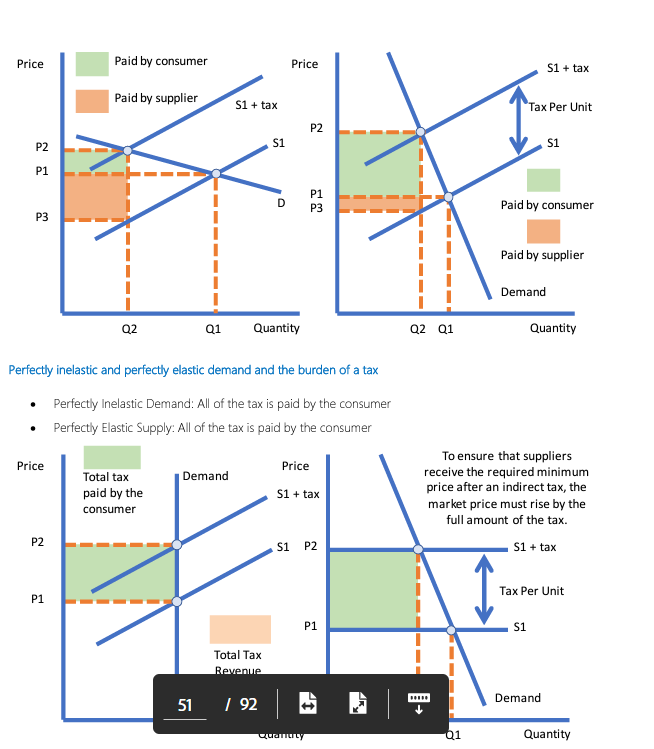

Indirect tax

a tax imposed by the government that increases supply costs faced by producers, i.e. excise duties and VAT

71

New cards

Types of indirect tax

Specific tax: a set tax per unit, e.g a £5 tax per unit, causes a parallel shift of the supply curve

Ad valorem tax: a percentage tax on the unit price, causes a pivot shift of the supply curve

Ad valorem tax: a percentage tax on the unit price, causes a pivot shift of the supply curve

72

New cards

Subsidy

any form of government support-financial or otherwise- offered to producers and sometimes consumers, causes an outward shift of the supply curve

73

New cards

Reasons for subsidies

\-helping poorer families with food and childcare costs

\-encourage output and investment in fledgling sectors

\-protect jobs in loss-making industries hit by recession

\-make some key health care treatments more affordable

\-reduce the cost of training and employing workers

\-achieve a more equitable distribution of income

\-reduce some of the external costs of mass transport

\-encourage output and investment in fledgling sectors

\-protect jobs in loss-making industries hit by recession

\-make some key health care treatments more affordable

\-reduce the cost of training and employing workers

\-achieve a more equitable distribution of income

\-reduce some of the external costs of mass transport

74

New cards

What does rational behaviour assume?

1- agents choose independently of one another

2- an agent has fixed and stable tastes and preferences

3- an agent gathers complete information on all alternatives

4- always make an optimal choice with given preferences

2- an agent has fixed and stable tastes and preferences

3- an agent gathers complete information on all alternatives

4- always make an optimal choice with given preferences

75

New cards

Habitual consumption

\-occurs when people have strong default choices

\-repeat choices become automatic because they don’t require much mental effort, compelling incentives may be given to then steer people away from these choices

\-repeat choices become automatic because they don’t require much mental effort, compelling incentives may be given to then steer people away from these choices

76

New cards

Computational weakness

when consumers find it difficult to calculate the probability of something happening when they make purchasing decisions, i.e. underestimating the long-term health consequences of relying heavily on prescription painkillers

77

New cards

Herd Behaviour

when individuals in a group act collectively without centralised direction

78

New cards

Anchoring effect

value is often set by anchors in peoples’ minds that are used as mental reference points

79

New cards

Framing

\-framing questions or offering in different ways generates different responses, i.e. presumed consent for human organ donations

Asymmetric framing: involves including an obviously inferior choice or hyper-expensive choice to guide consumers to more expensively-priced items

Asymmetric framing: involves including an obviously inferior choice or hyper-expensive choice to guide consumers to more expensively-priced items

80

New cards

What is market failure

market failure occurs when the competitive outcome of markets is not efficient form the point of the economy as a whole; resources are not allocated as efficiently as they could be due to to the benefits the market confers on individuals or firms carrying out a particular activity diverges from the benefits to society as a whole

81

New cards

Complete market failure

occurs when the market does not supply products at all- there is a missing market, i.e. public goods

82

New cards

Partial market failure

when the market exists but supplies the wrong quantity of a product or a wrong price

83

New cards

The importance of properrty rights

\-Property rights confer legal control or ownership, for market to operate efficiently property rights must be protected, i.e. regulation

\-if an asset is unowned no one has an incentive to protect it from abuse

\-this leads to the Tragedy of the Commons, i.e. over use of common land or over-fishing of local waters

\-if an asset is unowned no one has an incentive to protect it from abuse

\-this leads to the Tragedy of the Commons, i.e. over use of common land or over-fishing of local waters

84

New cards

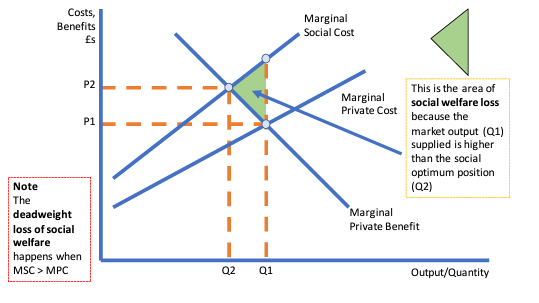

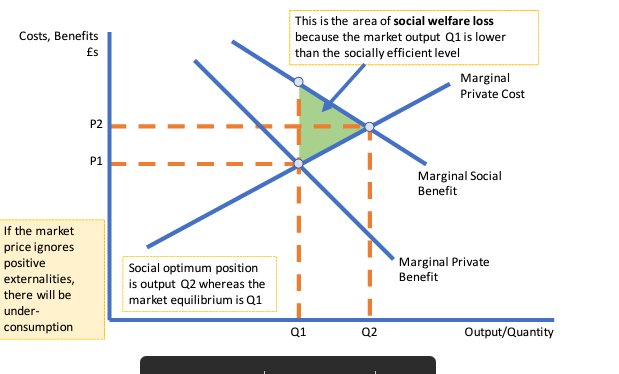

What are externalities?

spill-over effects from production and/or consumption, for which no appropriate compensation is paid to one or more third parties affected or third parties benefit from the spill over effects, e.g. social returns from investment, or university education

85

New cards

Ways to value externalities

1)Shadow pricing: the assignment of a monetary value to an abstract commodity that is not ordinarily quantifiable as having a market price, e.g. the external cost of road congestion can be calculated by multiplying the numbers of hours lost by the average wage

2)Compensation: estimates the cost of ‘putting right’ an externality, internalises the externality

3)Revealed preference: how much people are willing to pay to avoid an externality, if 200 homeowners are willing to pay £2000 to avoid noise, the externality caused by road noise is valued at £40m

2)Compensation: estimates the cost of ‘putting right’ an externality, internalises the externality

3)Revealed preference: how much people are willing to pay to avoid an externality, if 200 homeowners are willing to pay £2000 to avoid noise, the externality caused by road noise is valued at £40m

86

New cards

Negative production externality diagram

87

New cards

Positive consumption externality diagram

88

New cards

What are public goods?

\-goods that are non-rival (consumption of the good does not reduce the amount available for others/ the marginal cost of supplying a public good to an extra person is 0)

\-and non-excludable (it is not possible to provide the good/service to one without other being able to enjoy)

\-non-rejectable (the collective supply of a public good for all means none can reject it)

\-and non-excludable (it is not possible to provide the good/service to one without other being able to enjoy)

\-non-rejectable (the collective supply of a public good for all means none can reject it)

89

New cards

Quasi-public goods

\-semi non-rival: up to a point, more consumers using the good does restrict the consumption of others, i.e. a beach, but a certain point it gets too crowded for anyone else to consume

\-semi non-excludable: its is possible but difficult or costly to exclude non-paying consumers, e.g. fencing a park or beach and charging entrance fees

\-semi non-excludable: its is possible but difficult or costly to exclude non-paying consumers, e.g. fencing a park or beach and charging entrance fees

90

New cards

The Free Rider Problem

Because public goods are non-excludable it is difficult to charge people for benefitting once a product is available. The free rider problem leads to under provision of a good and thus causes market failure. Free riders have no incentive to reveal how much they are willing and able to pay for a public good because they can enjoy benefit without paying

91

New cards

Cases fore government intervention for public goods

• The non-rival nature of consumption provides a strong case for the government to replace the market to provide and pay for public goods

• Many public goods are provided free at the point of use and funded by taxation or a charge such as the BBC’s licence fee

• State provision may help to prevent under-provision and under-consumption of public goods so that social welfare is improved

• If the government provides public goods, they may do so more efficiently because of economies of scale

• Providing essential public goods helps affordability and access to important services for lower income households and therefore help to address inequalities of income

• Many public goods are provided free at the point of use and funded by taxation or a charge such as the BBC’s licence fee

• State provision may help to prevent under-provision and under-consumption of public goods so that social welfare is improved

• If the government provides public goods, they may do so more efficiently because of economies of scale

• Providing essential public goods helps affordability and access to important services for lower income households and therefore help to address inequalities of income

92

New cards

Arguments against government intervention for public goods

• If the government becomes a monopoly provider, there is a danger of a lack of efficiency arising from a lack of competition

• There are many other demands on government finances, and so there could be a significant opportunity cost of public goods being provided. In some cases, the state funds and the private sector provides public goods e.g. via Public Private Partnerships / Private Finance Initiative – although the track record on many of these projects suggests that the long-term cost is quite high.

• There are many other demands on government finances, and so there could be a significant opportunity cost of public goods being provided. In some cases, the state funds and the private sector provides public goods e.g. via Public Private Partnerships / Private Finance Initiative – although the track record on many of these projects suggests that the long-term cost is quite high.

93

New cards

What are club goods?

goods that are excludable but non-rival, e.g. Wi-Fi in a coffee a shop

94

New cards

Information failure

occurs when people have inaccurate, incomplete, uncertain or misunderstood data and so make potentially sub-optimal choices

95

New cards

Causes of information gaps

\-misunderstanding the true costs/benefits

\-uncertainty about costs and benefits

\-complex information for specialist products

\-addiction

\-lack of awareness

\-habitual purchase

\-uncertainty about costs and benefits

\-complex information for specialist products

\-addiction

\-lack of awareness

\-habitual purchase

96

New cards

Symmetric information

when consumers and producers have the same knowledge about products, they know everything there is to know about the effects of consuming them

97

New cards

Asymmetric information

when there is an imbalance in information between buyer and seller which can distort choices

98

New cards

Moral hazard

occurs when there is a lack of incentive to guard against risk where one is protected from its consequences, i.e. insured consumers more likely to take risks

99

New cards

Adverse selection

\-a case where asymmetric information is exploited, i.e. health insurance is most likely to be used by those with chronic health conditions or smokers/drinkers so health insurance companies raise the average price of insurance cover to prevent large claims, thus pricing healthy low-risk consumers out the market (market failure)

100

New cards

Merit Goods

Goods for which the MPB is higher than realised (suffers from under-consumption)