Chapter 3 (Supply and Demand)

1/79

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

80 Terms

Demand

The various quantities

of a good or service

which a consumer

is both willing and able

to purchase

at various prices

per unit of time

ceteris paribus

Supply

The various quantities

of a good or service

which a seller

is both willing and able

to sell

at various prices

per unit of time

ceteris paribus

10 Fundamental Principles of Economics

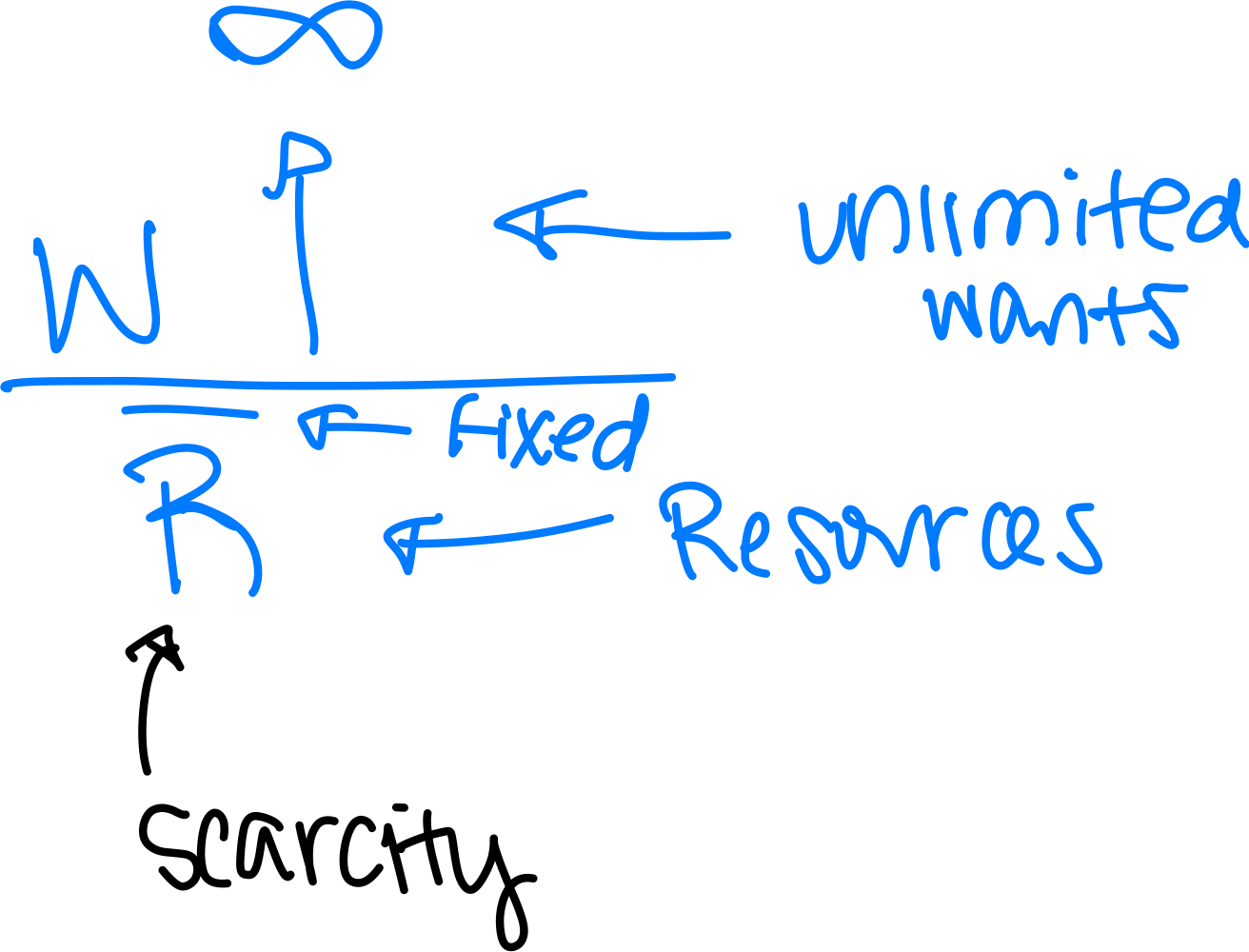

1)Scarcity is Inescapable

2)Risk is unavoidable

3)Therefore all persons must make choices

4)Incentives Matter

5)People generally act in their own self-interest

6)There is often more than one way to produce things

7)Voluntary exchange is mutually advantageous

8)It is wealth not poverty, which has causes

9)Public policies have primary and secondary effects

10)In the end, economic laws tend to prevail

Cobb-Douglas production Function

Y/Q=F(K,L)

Y/Q:Quantity, F:Function of, K:Capital, L:Labor

Economics

A social science that attempts to explain how individuals, firms, and nations allocate scarce resources among competing interests

Economics diagram

Social Science

Defined by the inability to replicate experiments

3 Basic Questions

1)What: What and how much will be produced? Allocation of Inputs

2)How: How will items be produced? Production

3)For Whom: For whom will items be produced? Allocation of Outputs

Centralized Command-Control System

A central authority decides the 3 basic questions.

Capitalism (Price) System

Price answers the 3 basic questions.

Compromise System

Government and Price answer the 3 basic questions

Customary (traditional) System

Tradition answers the 3 basic questions

Post hoc ergo propter hoc

“After this therefore because of this” First economic warning that states that just because one event proceeds another, it doesn’t mean it caused the second event. Time-series data.

Fallacy of Composition

Second economic warning that states that what holds true for an individual does not always hold true for the whole.

Correlation does not necessarily equal causation

Third economic warning. Cross-sectional data.

Violation of Ceteris Paribus

Fourth economic warning that says “other things being held constant” should not be violated.

Inclusion of an irrelevant variable

Fifth economic warning that states unrelated factors should not be taken into consideration

Exclusion of relevant variables

Sixth economic warning

Cause of bowed outward shape

Law of increasing opportunity cost

Consumer sovereignty

Actions in the marketplace dictate what is being made

Allocative efficiency

Right mix of goods, dictated by consumer sovereignty

Economic good

More of the good is preferred to less

Economic Bad

Less of the good is prefered to more

Consumer durable goods

Goods that are around for a long time

Consumer non-durable goods

Goods that dont last

Capital goods

Goods that create other goods. They allow for faster further development

Non-Price parameters of demand

Income, price of other goods, tastes/preferences, advertising, number of buyers, expectations

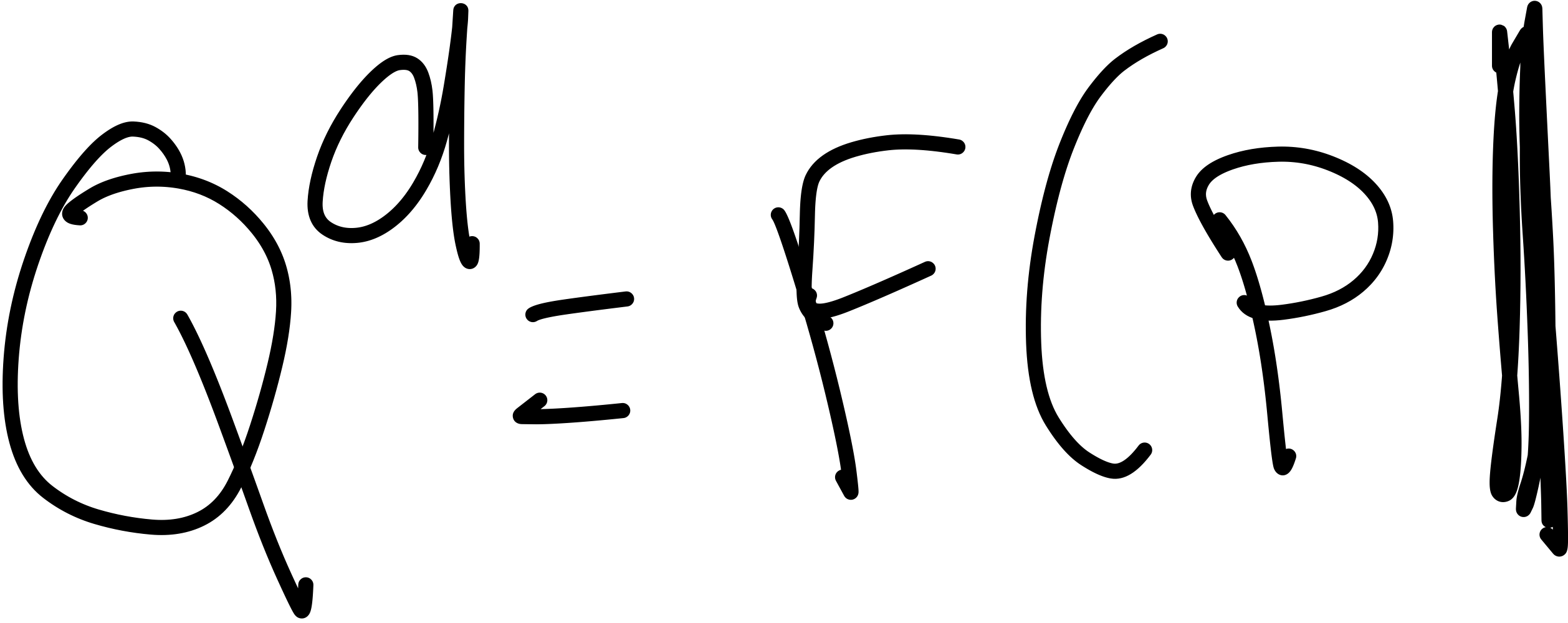

Formula for demand

Q^d=F(P|

Q^d:Quantity demanded, F:function of, P:price, |:Ceteris Paribus “all other things constant”

*Q and P are inverse (-)

Positive Statement

Statement of fact. EX “If the price of gas goes up, people will buy less”.

Normative Statement

Value judgement, what “ought’ to be. EX “If the price of gas goes up, people will buy less. So we should not allow the price to go up”.

Household Macroeconomic Sector

Supplies the inputs, demands the output

Business Macroeconomic Sector

Demanding the inputs, supplying the outputs

4 Factors of Production

1)Land (Rent, smallest)

2)Labor (Wages, biggest)

3)Capital (Interest)

4)Entrepreneurship (Profit)

National Income

Sum of the 4 factors of production

Complementary goods

As the price of one good goes down, demand for the other goes up. (-).

Substitute good

As the price of one good goes up, the demand for the other also goes up. (+).

Normal Good

Increase in income=Increase in demand (+)

Inferior good

Increase in income=decrease in demand

Non-price parameters of Supply

Number of sellers, expectations of sellers, price of inputs, taxes and subsidies, technology, weather

Law of supply Equation

Q^s=f(P|

Consumer surplus

You have money left over from what you were willing to pay

Producer Surplus

More product left over from what you were willing to sell

Shift of the curve (Change in demand/supply)

Change in non price parameters

Shift along the curve (change in quantity demanded/supplied)

Change in price

Equalibrium

no shortage or surplus

Comparative statistics

1) Identify the original equilibrium price and quantity

2)Identify the shift (demand or supply)(left or right)

3)identify the new equilibrium price and quantity

Price floor

A case in which the government says, “you must charge at least ____”

The seller

Side the Government takes with a Price Floor

Effective price floor

Must be set above the equilibrium price and must result in a surplus and unemployment

Price ceiling

A case in which the government says “you can charge no more than___”

The buyer

Side the Government takes with a Price Ceiling

Effective price ceiling

Must be put below the equilibrium price and must result in a shortage

Case #1

D→ S→

P*=? Q*=up

Case #2

D← S←

P*=? Q*=down

Case #3

D→ S←

P*=up Q*=?

Case #4

D← S→

P*=down Q*=?

Output

Deals with GNP and GDP

Price Level

Deals with CPI(most controversial), PPI, and GDP deflator

Fair’s model

Output+Price

Predicts popular vote using output and price

Phillips curve

Price+Unemployment

When inflation is high, unemployment is low

Oken’s Law

Output+Unemployment

%changeGDP=3%-2 X A changeUnemployment

As unemployment goes down, GDP goes up

Full Employment Act of 1946

Pursued all 3 goals, Output, Price Level, Unemployment

Output increase, Price steady, Employment increase

Gross Domestic Product

1) The total dollar value

2)of all FINAL goods and services

3)Produced by ANYONE

4)within US BOARDERS

5)in a given calendar year

Gross National Product

1)The total dollar value

2)of all FINAL goods and services

3)produced by US CITIZENS/FIRMS

4)ANYWHERE in the world

5)in a given calendar year

Shift from GNP to GDP

Caused by texaco in Saudi Arabia in 1991

Nominal GDP

(CPa X CQa)+(CPo X CQo)

Real GDP

(BPa X CQa)+(BPo X CQo)

CPI

Fixed market basket of goods. Consumer goods, can include foreign products

CPI formula

((CPa X BQa) + (CPo X BQo))/((BPa X BQa) + (BPo X BQo))

Everything is base except Price in numerator

Laspeyres Price Index

Another name for CPI

GDP Deflator

Changing market basket. All goods and services produced within US borders.

GDP Deflator formula

((CPa X CQa) + (CPo X CQo))/((BPa X CQa) +(BPo X CQo))

Everything is current except for price in the denominator

Inflation

Increase in the overall price level

Deflation

Decrease in the overall price level

Hyperinflation

Extremely rapid increase in the overall price level

Disinflation

Slowing of the inflation rate

Arthur Oakum misery index

Inflation rate + unemployment rate

One-to-one trade off

The opportunity cost of receiving one grade higher in economics, is one grade lower for math

Comparative advantage

Ability to perform an activity at a lower opportunity cost

Only thing that matters when allocating time

Absolute advantage

If you were to spend a given amount of time on any duty, you could produce more than anyone else