Unit 2 Test

1/113

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

114 Terms

Demand

A schedule which shows the various amounts of a good/service consumers are willing and able to buy at each specific price in a series of possible prices that may arise in a specific period of time

Demand schedule

Represents the concept of demand and shows the series of prices of a product and its corresponding quantity demanded over a period of time

Demand Curve

Graphically represents a Demand schedule. In Economics, the independent variable, PRICE, goes on the vertical axis and the dependent variable, QUANTITY, goes on the horizontal axis

Slope of Demand Curve

Demand (D);

Relationship b/w the 2 variables on Demand Curve

Indirect (price increases as quantity decreases) shown by a downward-sloping line (curve) that is simply a series of points (combinations of prices and corresponding quantities at that desired price)

Demand Descends Downward

Law of Demand

Key economic principle that states as price increases, the corresponding quantity demanded decreases, ceteris paribus (and vice versa)

*DEMAND DOES NOT INCREASE OR DECREASE

Ceteris paribus

All else being equal, other things held constant

Accounts for all other factors that might come into play for how much of anything a consumer would be willing and able to buy. It holds these things constant, so that the only thing the Law of Demand looks at is the price of the good or service being analyzed

Behavior patterns that explain the Law of Demand

Diminishing Marginal Utility

Substitution Effect

Income Effect

Diminishing Marginal Utility

The extra satisfaction (usefulness) we get from using an additional unit of some good/service begins to diminish → we’re not as willing to pay as much for more of the same good as we did for the first

Marginal utility

Describes the extra usefulness/satisfaction obtained from one more unit of something

When will someone stop buying something?

When it’s not worth anything anymore! When marginal utility (extra usefulness/satisfaction) is less than the price

Substitution Effect

When a price of a product rises (now more expensive compared to other products), consumers become more likely to buy one of the alternatives as a substitute for the produce whose price increased

How do economists measure consumption?

By the amount of a good or service that’’s bought NOT the amount of money spent to buy it

Income Effect

Rising prices makes us feel poorer. When the price of any product increases, our limited budgets just wont buy as much as they used to, it feels as if we have less money → buy less of certain things (our real income is less)

Shift rightward on Demand Curve

Increase in demand

Movement along the demand curve

As price changes (raise or lower it) the quantity demanded changes

Determinants of Demand (Demand Shifters)

Consumer Preferences (Tastes)

Price of Related Goods

Consumer Income

Demographics/ # of Potential Buyers

Consumer Expectations

Consumer Preferences (Tastes)

Favorable change= increase in demand (unfavorable=decrease)

Ex. Winning sports team will see an increase in demand of their apparel

Factors that can influence a change in interest

Advertising/social media

Fad- temporary intense interest

News Event

New Product introduction

Seasonal or weather event

Price of Related Goods

Prices of Substitute and complementary goods of a product can change demand

Substitute goods

those that can be used in place of another

Price of one good and demand for its substitute are directly related

Ex. If price of Heinz ketchup increases, demand for Hunts Ketchup increases

Complementary Goods

Those that are used together

Inverse relationship b/w price of one good and demand for 2nd good

Ex. If price of tennis racket increases (b/c quantity demanded falls) demand for tennis balls decrease

Consumer income

When your income goes up, you can afford to buy more goods and services

Normal good

a good that consumers demand more of when their income increases (most goods like steak, veggies, and shopping at Macy’s)

Inferior Good

a good that consumers demand less of when their income increases (demand varies inversely with income) (ex.canned meat, powdered mac & cheese, shopping at a flea market)

Demographics/ Potential Buyers

More buyers = increase in demand (less=decrease)

Ex. Demand for prescription drug has increased as the population as grown older

Consumer Expectations

consumers have expectations about future prices, product availability, and income,and these expectations can shift demand

Ex. Expect price of gas to decrease next week, demand for gas this week decrease (wait for next week)

PRIDE or TRIBE

Preferences or Taste

Related Goods

Income

Demographics or Buyers

Expectations

3 ways to increase profits of a business

Selling more units

cut your costs

Raise price (not necessarily)

Why raising prices wont necessarily increase profits of business

The Law of Demand tells us that increased price causes a decrease in quantity demanded but it doesn’t tell us by how much (where the concept of elasticity comes in)

Elasticity

A measurement of how responsive one variable is to a change in another variable. It can be used with all sorts of variables

How does elasticity relate to increasing profits of a business

We look at the price elasticity of demand (how sensitive the quantity of a good that people demand is to a change in price of that good) when trying to increase profits

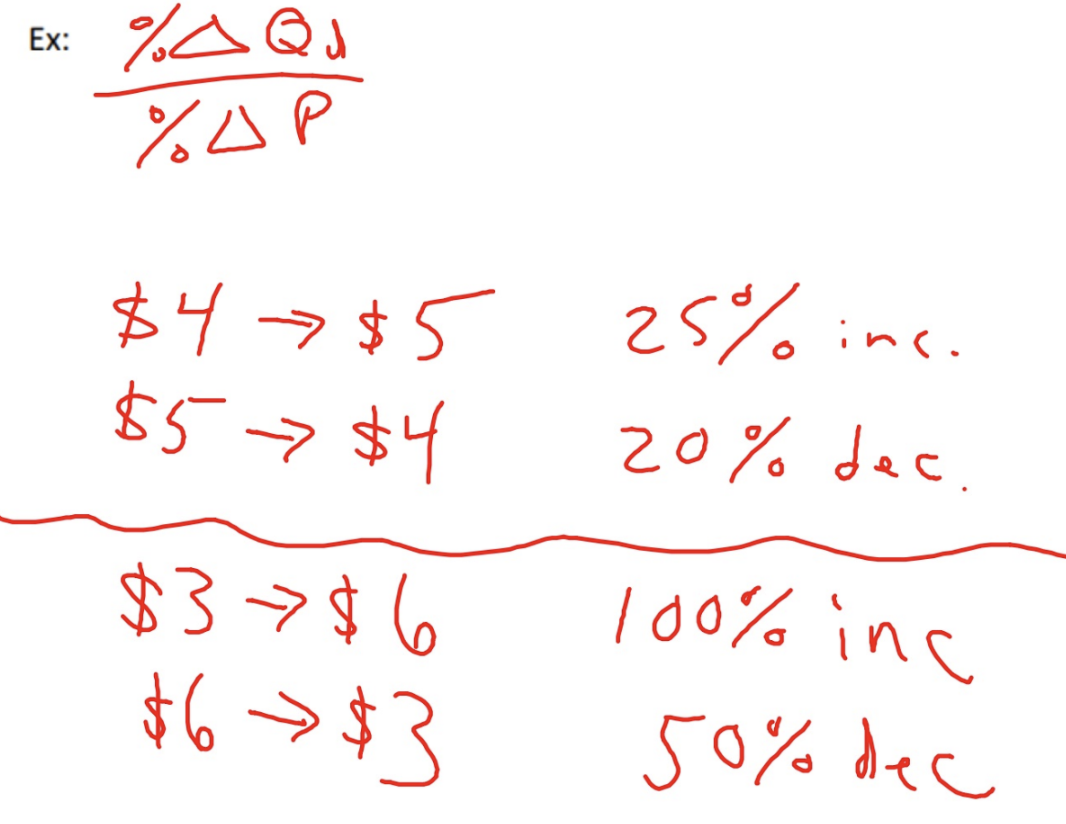

Price elasticity of demand (demand elasticity)

A measure of how much the quantity demanded changes when the price changes

Simple Price Elasticity of Demand Formula

Demand Elasticity Continuum

Perfectly inelastic demand

change in price results in NO change in quantity demanded of a product

elasticity coefficient=0

Inelastic Demand

when the % change in quantity demanded is less than the % change in price

Elasticity coefficient < 1

Unit Elastic Demand

when the % change in quantity demanded is equal to the % change in price

Elasticity coefficient = 1

Elastic Demand

when the % change in quantity demanded is more than the % change in price

Elasticity coefficient >1

Perfectly Elastic Demand

buyers will only buy at one price → small change in price → infinite change in quantity demanded

Elasticity Coefficient approaches infinity

Demand is inelastic when..

a given change in price causes a relatively smaller change in quantity demanded

Demand is unit elastic when..

a given change in price causes a proportional change in quantity demanded

Demand is elastic when..

a given change in price causes a relatively larger change in the quantity demanded

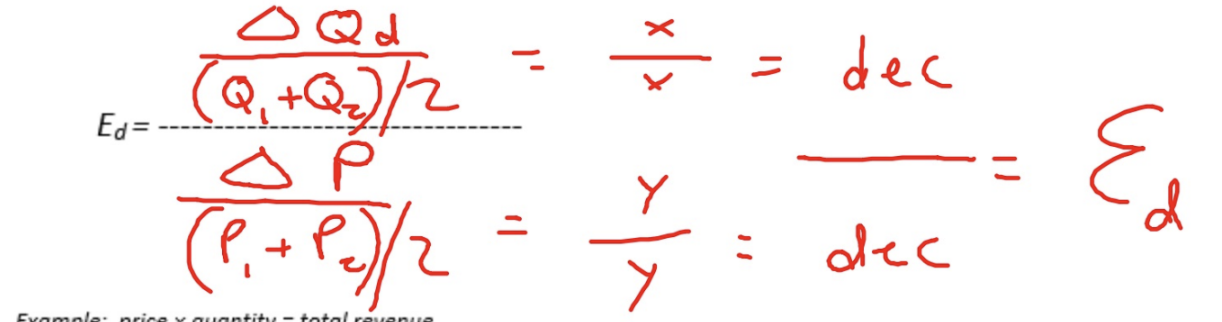

Problem of the simple Demand elasticity formula

The senstivity of the change in quantity shouldn’t depend on whether the price goes up or down

Midpoint Formula (Arc Method)

Calculates price elasticity across a price quantity range to overcome the problem of selecting the reference points for price and quantity. In this formula, the average of the 2 quantities and the average of the 2 prices are used as reference points. USE THE ABSOLUTE VALUE

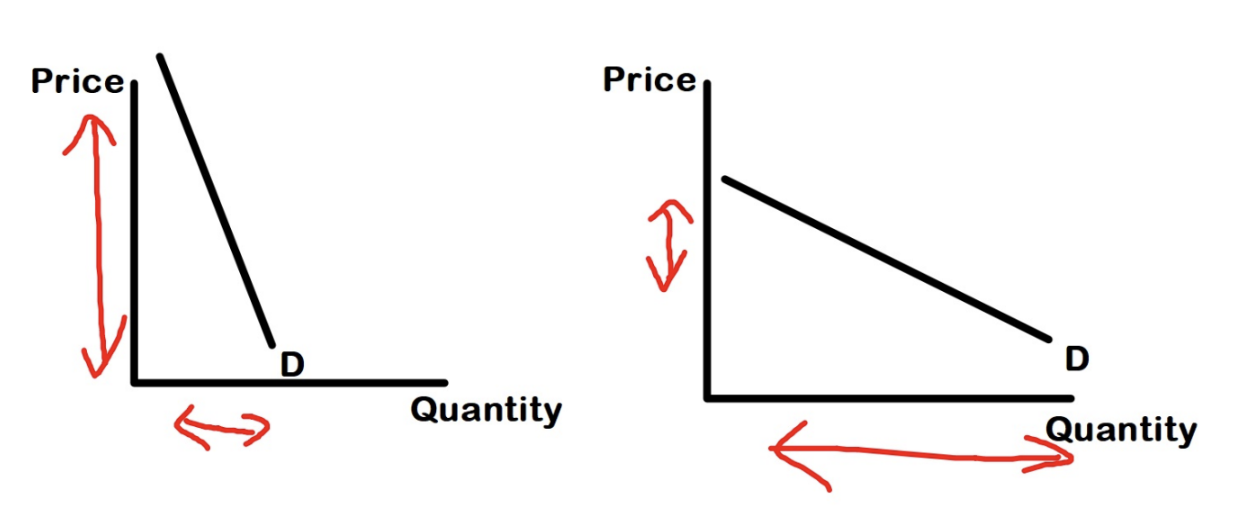

Slope of Demand Curve and Elasticity

If we generalize: steeper slopes show inelastic demand while flatter slopes show elastic demand

Slope of Demand Curve…

DOES NOT MEASURE ELASTICITY (elastic at higher prices, changes in sensitivity to how much money lost differs from $1 to $100)

4 Determinants of Demand Elasticity (LIST)

Luxuries vs Necessities

Proportion of one’s Income used

Number of Substitutes

Time frame available to adjust the price change

Luxuries vs Necessities

Necessities tend to have inelastic demand whereas luxuries tend to have more elastic demand (ex. Diapers are a necessity for anyone with a baby and going out to dinner is NOT)

Is the good habit-forming?

Consumers become less sensitive to the price of the good if they buy something out of habit (it has become the default choice) (ex. Going to a pizza place everyday even when they raise their prices)

Addictive products

Tend to be more severe in their behavior results → these will be very inelastic

Proportion of One’s Income used

products that take up a high percentage of one’s income will have a more elastic demand

Number of Substitutes

The more close substitutes there are in the market, the more elastic is demand because consumers find it easy to switch

Breadth of the definition of the product

If the good is broadly defined (i.e., the demand for autos in general), demand is often inelastic, as opposed to a good that’s more narrowly defined (i.e., the demand for Honda Civic). Then the demand tends to be more elastic

Time frame to adjust to the price change

Demand is more price elastic the longer that consumers have to respond to a price change. They have more time to search for cheaper substitutes and switch their spending

Off-peak vs peak demand

Demand is more price inelastic at peak times and more elastic at off-peak times

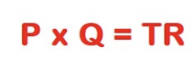

Total Revenue Formula

Price x Quantity = Total Revenue

Total Revenue (TR) changes when..

Price changes

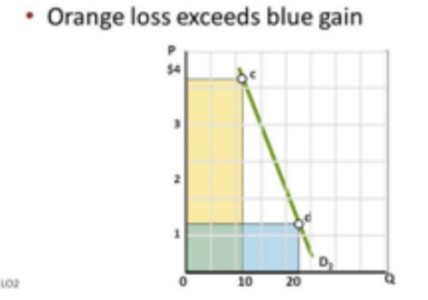

The total revenue test shows when demand is..

inelastic, unit elastic, and inelastic

The price effect dominates with..

Lower price and inelastic demand

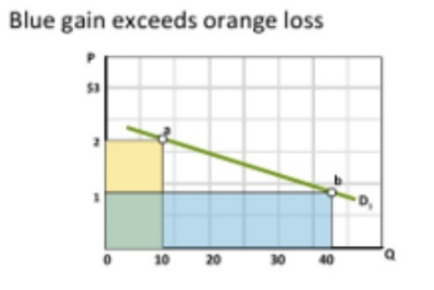

The quantity effect dominates with..

Lower price and elastic demand

Increase in price for Inelastic demand

Increase in total revenue for Inelastic Demand

Decrease in Price for Inelastic Demand

Decrease in Total Revenue for Inelastic Demand

Increase/Decrease in Price of Unit Elastic Demand

No change in Total Revenue

Increase in Price of Elastic Demand

Decrease in Total Revenue of Elastic Demand

Decrease in Price of Elastic Demand

Increase in Total Revenue of Elastic Demand

Supply

a schedule which shows the various amounts of a good/service producers are willing and able to produce and sell at each specific price in a series of possible prices that may arise in a market in a specific period of time

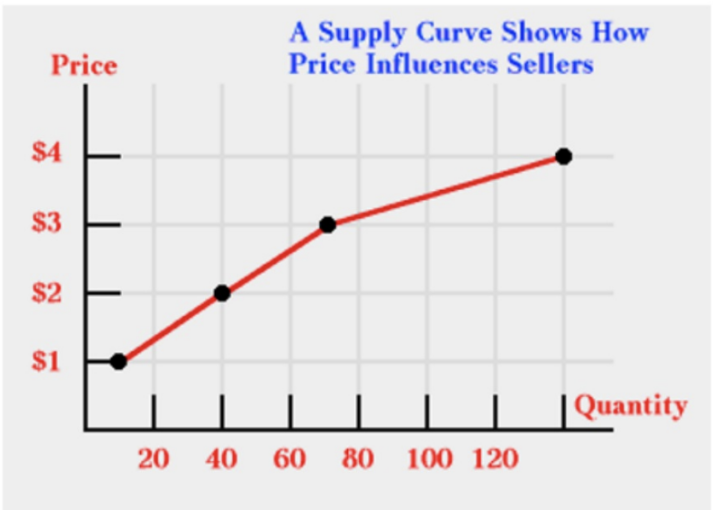

Supply Curve

Graphically represents a supply schedule. In Economics, the independent variable, PRICE, goes on the vertical axis, and the dependent variable, QUANTITY, goes on the horizontal axis

Relationship b/w Quantity supplied and Price

There’s a DIRECT relationship b/w quantity supplied and price (as price goes up, quantity supplied goes up)

Law of Supply

States that producers/suppliers/sellers will produce/supply/sell more of their good/service at a high price than a low price. There’s a direct relationship between price and quantity supplied

Explanation of Law of Supply

Give production/supply costs as they are, a higher price means greater potential earnings and ultimately, profits, and thus, an incentive to increase the quantity supplied

Is the Law of Supply always true?

No, beyond some production quantity, producers will encounter increasing costs per added unit of output (ex. more costly to find oil)

When all factors held constant, what is one thing that will change the quantity being supplied?

The PRICE of the product

Change in Quantity Supplied

No shift in supply curve; change in amount offered for sale in response to a change in price; Producers have the freedom, if the price fall too low, to slow or halt production or leave the market completely, if the price rises the producer can step up production levels

Shifting Supply Curve

Generally, if you decrease the costs of production, you’ll increase supply (shift curve right) and if you increase the costs of production, you'll decrease supply (shift curve left)

Decrease= LEFT is LESS; Increase= RIGHT is MORE

Changes in Supply

A situation where suppliers supply different amounts of products for sale at all possible prices in the market

Supply Shifters/ 7 Basic Determinants of Supply (PIGTOES)

Productivity

Input Prices

Government Actions

Technology/Methods

Other Production Goods’ Prices

Expectations of Suppliers

# of Suppliers

Productivity

Has mostly to do with the workers’ motivation to produce (less motivated= decrease supply (curve shifts left); more motivated= increase supply (curve shifts right))

Input prices

Cost to produce (labor, materials, packaging, etc.); price of inputs drops= increase supply (curve shifts right); price of inputs increase= decrease supply (curve shifts left)

Government Actions (RST)

Regulations (Tighter=less supply/increased production costs; Relaxed=more supply/decrease production costs)

Subsidies (more= more supply/lower production costs; less= less supply/higher production costs)

Taxes (more= less supply/increased production costs; less= more supply/ lower production costs)

Technology/Methods

tends to shift supply curve right because of lowering productions costs and/or increase productivity (allowing for greater supply at each and every price in the market)

War, natural disasters, and the like often set technology back → increase production costs, decrease supply (curve shifts left)

Other Production Goods’ Prices

Price of substitute good decreases, Supply of good increases (indirect relationship) like with milk and cheese

Price of Complement Good increases, Supply of good increases (direct relationship) like with beef and leather

Substitutes-in-Production

Two or more goods that can be produced using the same resources. Can only produce one good at a time

Complements-in-production

Two or more goods that are jointly produced using a given resource. Producing one leads to producing both goods.

Expectations of Suppliers

If producers think that price of good will increase in the future → present supply decreases (suppliers withhold for the future and curve shifts left). If they fear that price of good may drop in the future → present supply increases (suppliers sell as much as they can now and curve shifts right)

Number of Suppliers

Only affects the market supply curve (not individual supply curve); more firms enter an industry = supply increases (curve shifts right); less firms= supply decreases (curve shifts left)

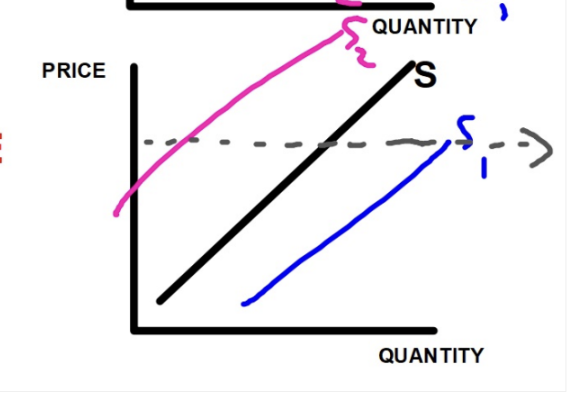

Supply Elasticity

A measure of the way in which quantity supplied responds to a change in price

Elastic supply

Small change in price leads to a relatively larger change in output; Coefficients greater than 1

Inelastic supply

Quantity changes very little relative to change in price; Coefficients less than 1

Difference b/w demand elasticity and supply elasticity

If quantities are being PURCHASED= DEMAND elasticity

If quantities are being BROUGHT TO THE MARKET = SUPPLY elasticity

Determinants of Supply

Its production (nature of the business, more easily a firm can adjust to a change in price = more likely the supply is elastic)

Supply Elasticity does not depend on..

number of substitutes, necessity of the product, or percentage of budget used to purchase the product (demand elasticity does), ONLY affected by PRODUCTION CONSIDERATIONS!

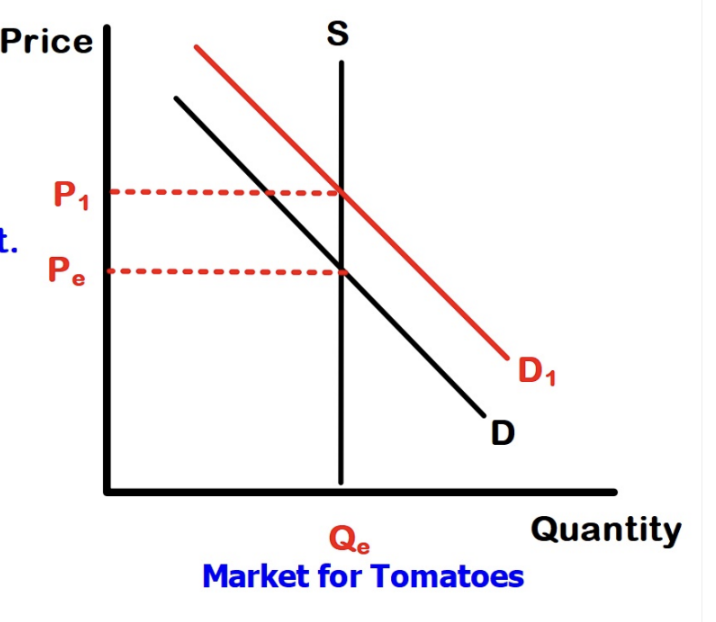

Market Period

A time period so short that the producer CANNOT respond to the change in price. Insufficient time to change output. Supply is perfectly inelastic (ex. Tomato farmer cannot produce more tomatoes at the end of growing season)

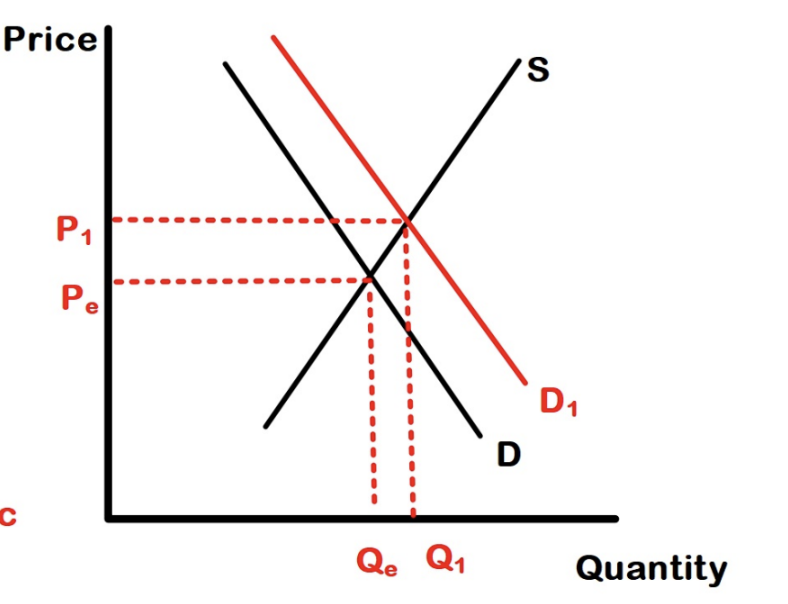

Short Run

A period of time that will not allow for a change in the physical plant capacity (capital goods) but will allow for some temporary change in output from that physical plant (Ex. Tomato farmer can construct a temporary greenhouse)

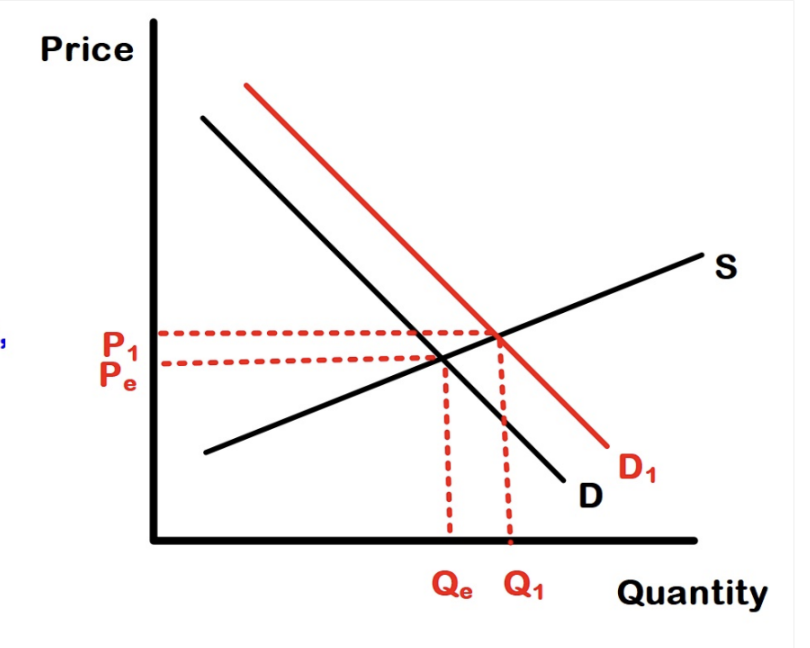

Long Run

There’s an ample of time to make major adjustments to production-change methods, expand the physical plant, increase capital, hire more workers, etc. (ex. Tomato farmer buys more land)

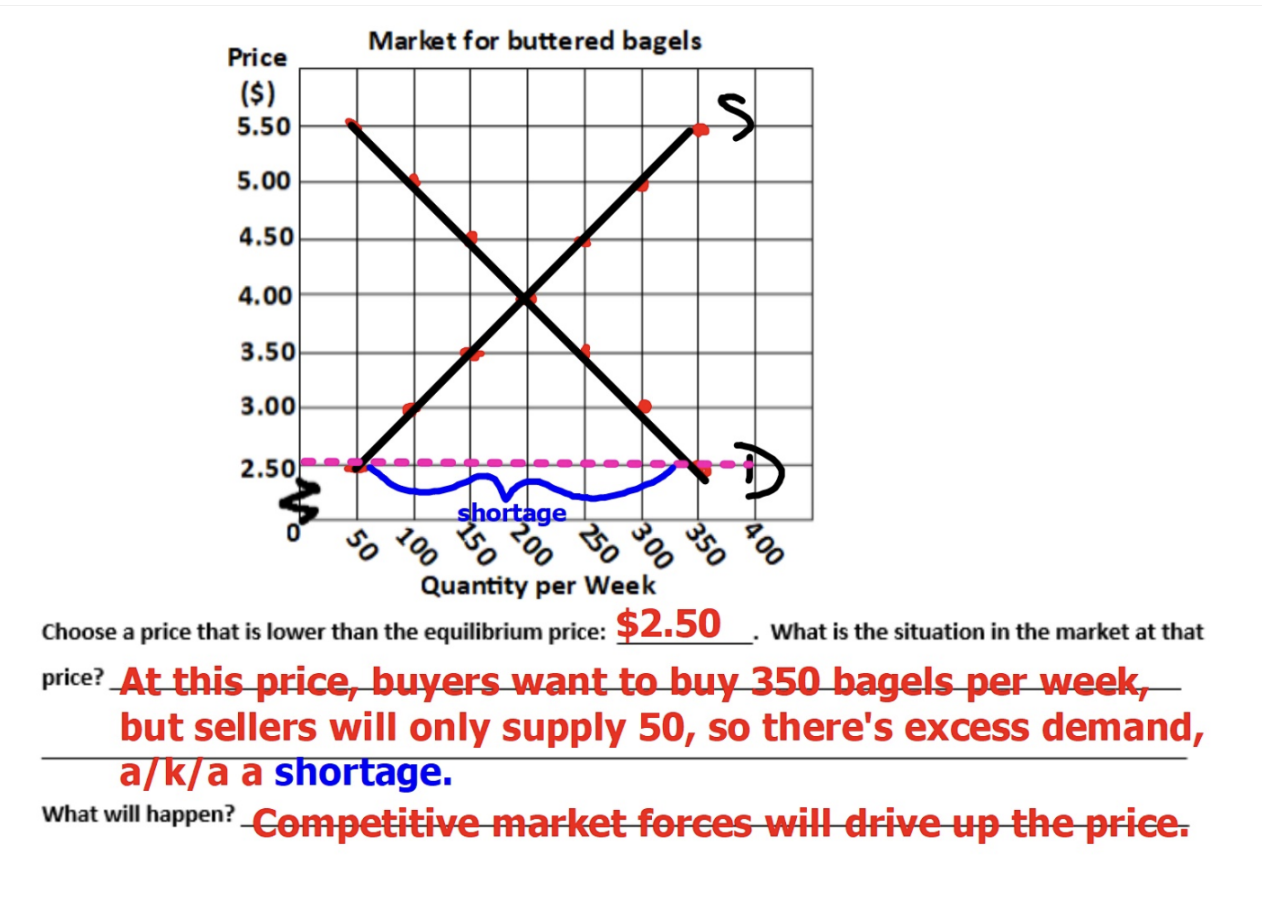

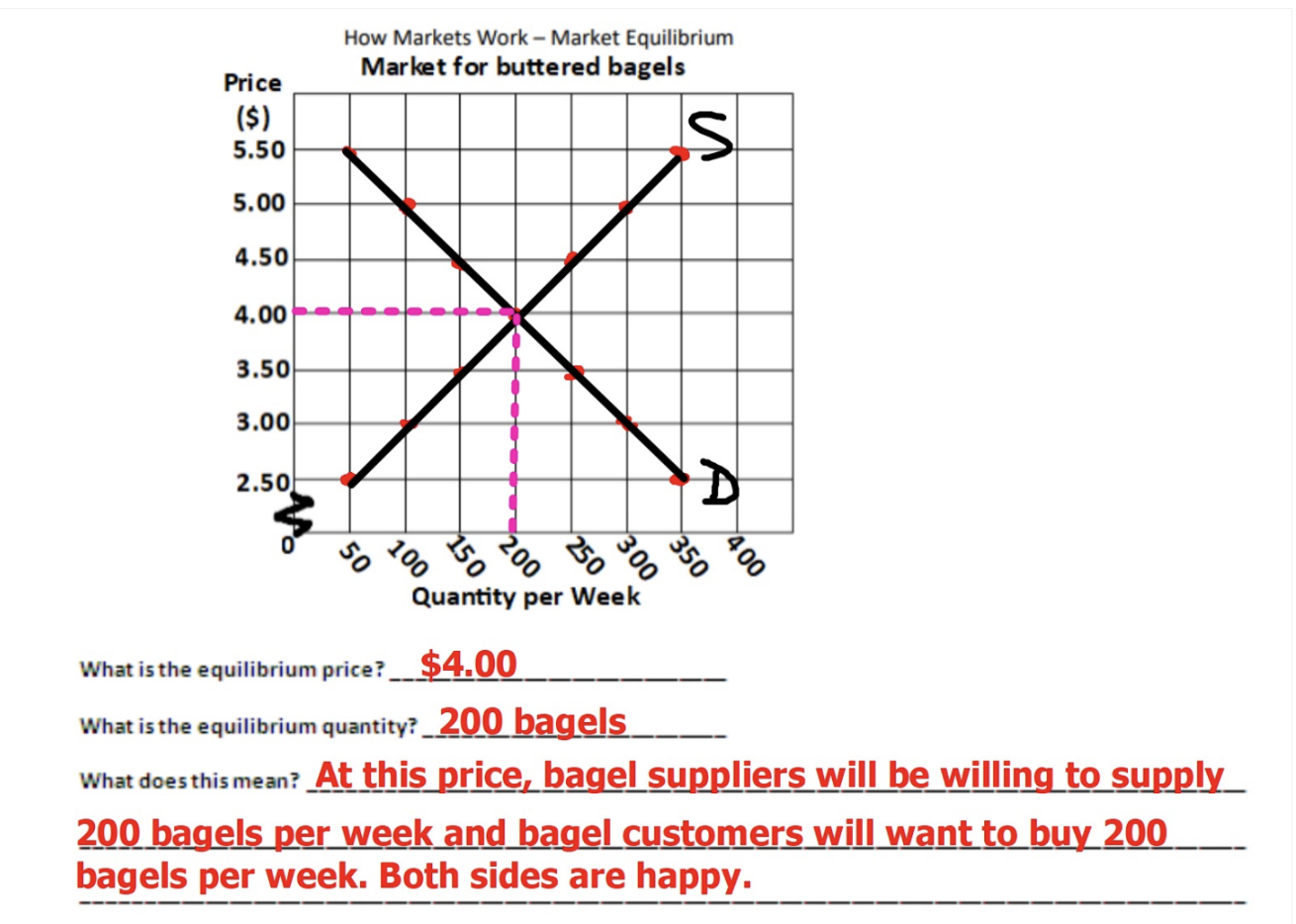

Market Equilibrium

When the quantity demanded equals the quantity supplied (both suppliers and consumers are happy)

Equilibrium Price

The price at which quantity demanded equals quantity supplied

Equilibrium Quantity

The quantity bought and sold at the equilibrium price

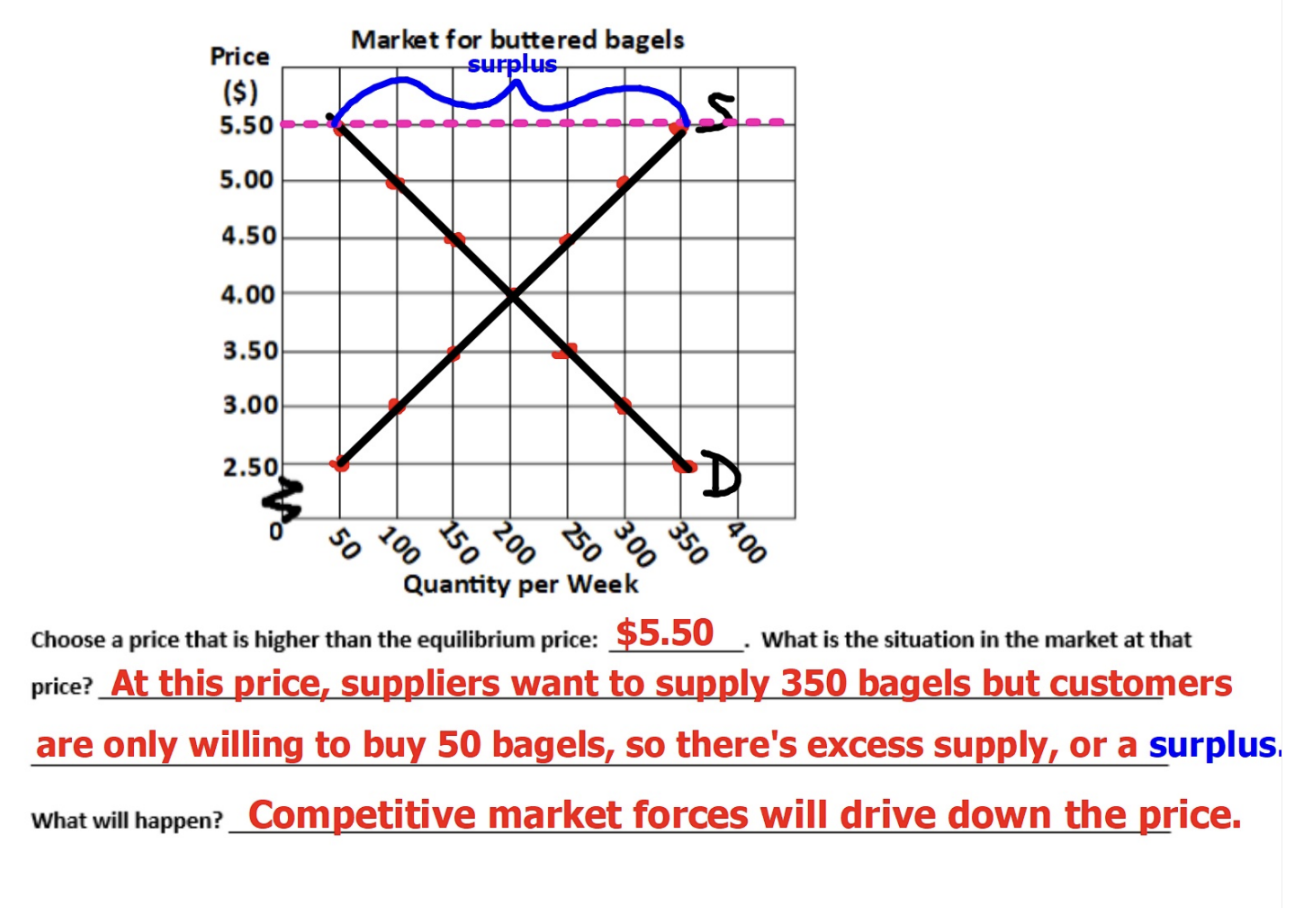

Surplus

A situation in which the quantity supplied exceeds the quantity demanded (competitive market forces will drive down the price)

Shortage

A situation in which the quantity demanded exceeds the quantity supplied (competitive market forces will drive up the price)