Unit 1: Basic Economic Principles

1/52

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

53 Terms

scarcity

the condition in which unlimited wants exceed the limited (or finite) resources available to fulfill those wants

this is the fundamental principle that underlies the study of economics

rationing device

a means for deciding who gets what portion of the available resources and goods/services (and thereby satisfaction/utility)

in our society, money is the default/primary rationing device, but other rationing devices include: power, popularity/status, "first come, first served," charity, etc.

goods and services

the objects (goods) and the actions (services) that people value and produce to satisfy human wants (i.e. things we consume to give us satisfaction/utility)

Examples:

Goods - sneakers, iPhone, Pop-Tarts, etc.

Services - watching movie at theater, Uber/Lyft ride, doctor visit, etc.

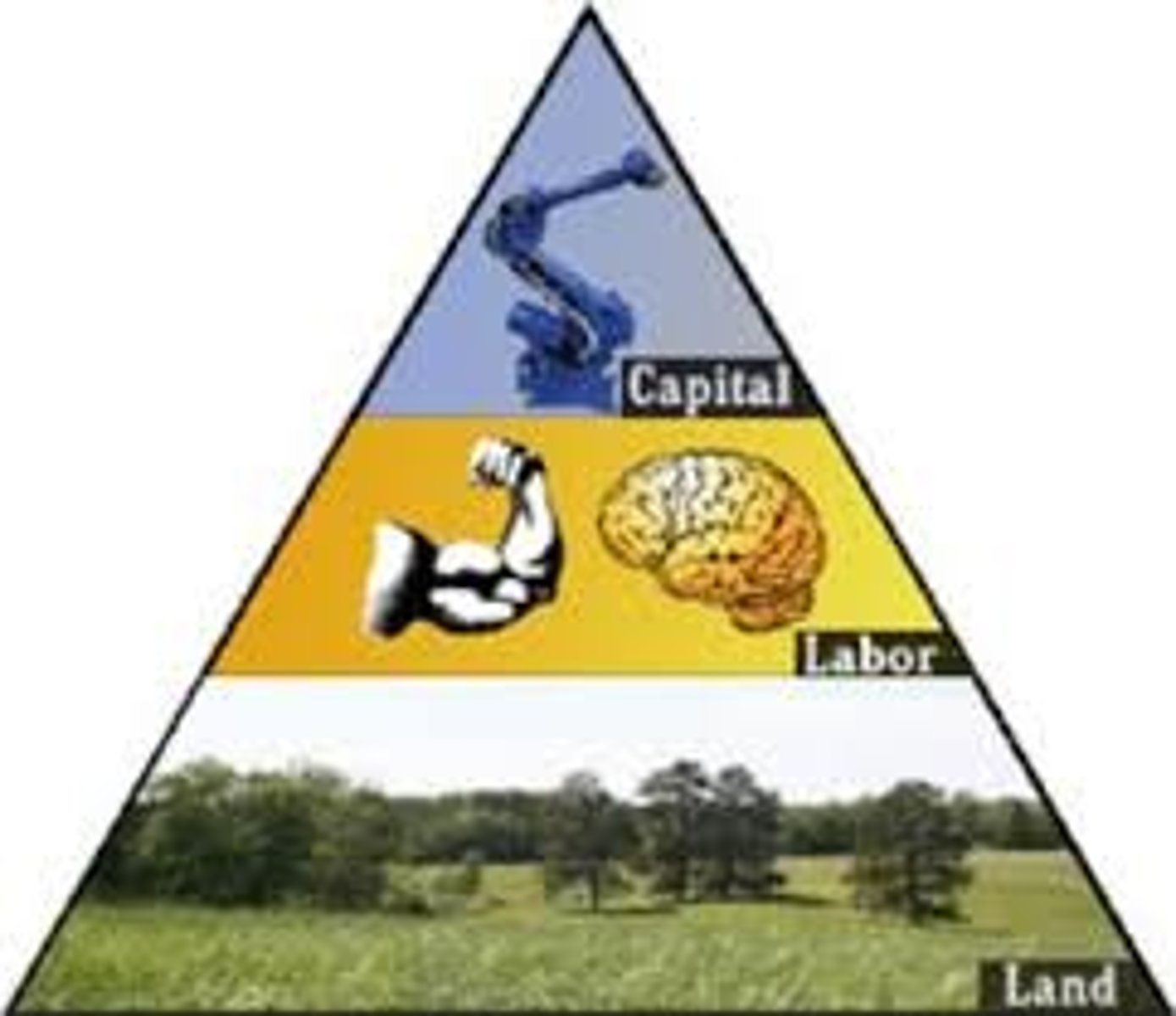

factors of production

resources that are used to make all goods and services, including: land, labor, capital, and entrepreneurship

human capital

the knowledge and skills that workers acquire through education, training, and experience

Example:

an executive chef at a restaurant attained a degree from Le Cordon Bleu Culinary School (education), spent three years as a sous-chef under Bobby Flay (training), and has worked in various roles in restaurant kitchens since they turned 14 years old (experience)

physical capital

any produced resource that is used in the production of other goods and services, including equipment, tools, machinery, factories and buildings

Examples of physical capital in picture include: assembly line/conveyor belt, wrench, factory building, lug nuts, etc.

liquid capital

money that can be used to purchase the other needed factors of production

Example: To start a furniture making business, an entrepreneur takes out a $300,000 loan (liquid capital) from the bank to purchase building and woodworking equipment such as saws, sanders, chisels, etc. (physical capital), pay workers (labor), purchase raw materials such as timber (land), etc.

labor

human effort directed toward producing goods and services

Examples: driving a taxi, doctor performing a check-up, bank teller depositing check into account, etc.

land

natural resources, minerals, and other raw materials that are used to make goods and services; "gifts of nature"

Examples: water, arable land (i.e. suitable for cultivating crops), marine animals, forests and vegetation (not cultivated by man; such as wild mushrooms), precious metals (e.g. gold), minerals (e.g. salt)

entrepreneurship

the organization and management of the factors of production (land, labor, capital) to produce goods and services

Note: Entrepreneurship is the role of a business owner, who assumes the risk of operating the business in the hopes of generating a profit; typically, the success or failure of a business depends upon the abilities of a business (e.g. Bill Gates was a successful entrepreneur that founded and managed Microsoft to become a $1 trillion company)

opportunity cost

the most desirable (or next best) alternative that is given up as the result of a decision and its foregone benefits; NOT the sum of the alternatives

Example: If your family chooses to go to Disneyland for a week vacation, the opportunity cost is whatever the next best/second option that had to be given up because there wasn't enough time/money to do both (e.g. camping in the Great Smoky Mountains); NOT all of the other vacation options that your family considered going on

trade-off

an alternative that we sacrifice when we make a decision

Example: If I have $5 in my wallet, the trade-off of getting a Whip-D-Dip from Hunter's is what I sacrifice/give-up to make that choice, such as hitting a bucket of golf balls at Tee-To-Green's driving range

dollar cost

the dollar value attached to a good or service (e.g. a student ticket to the football game is $3)

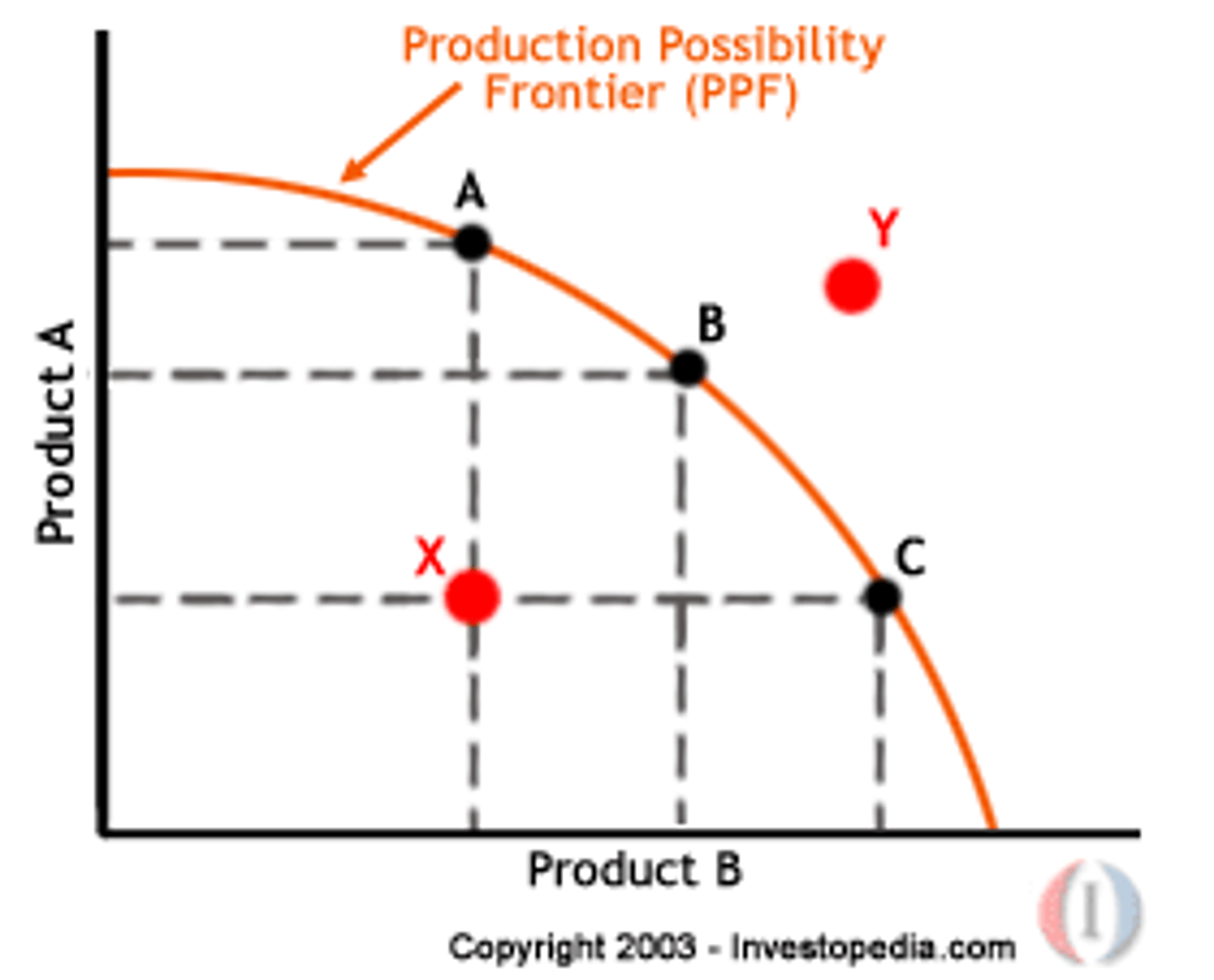

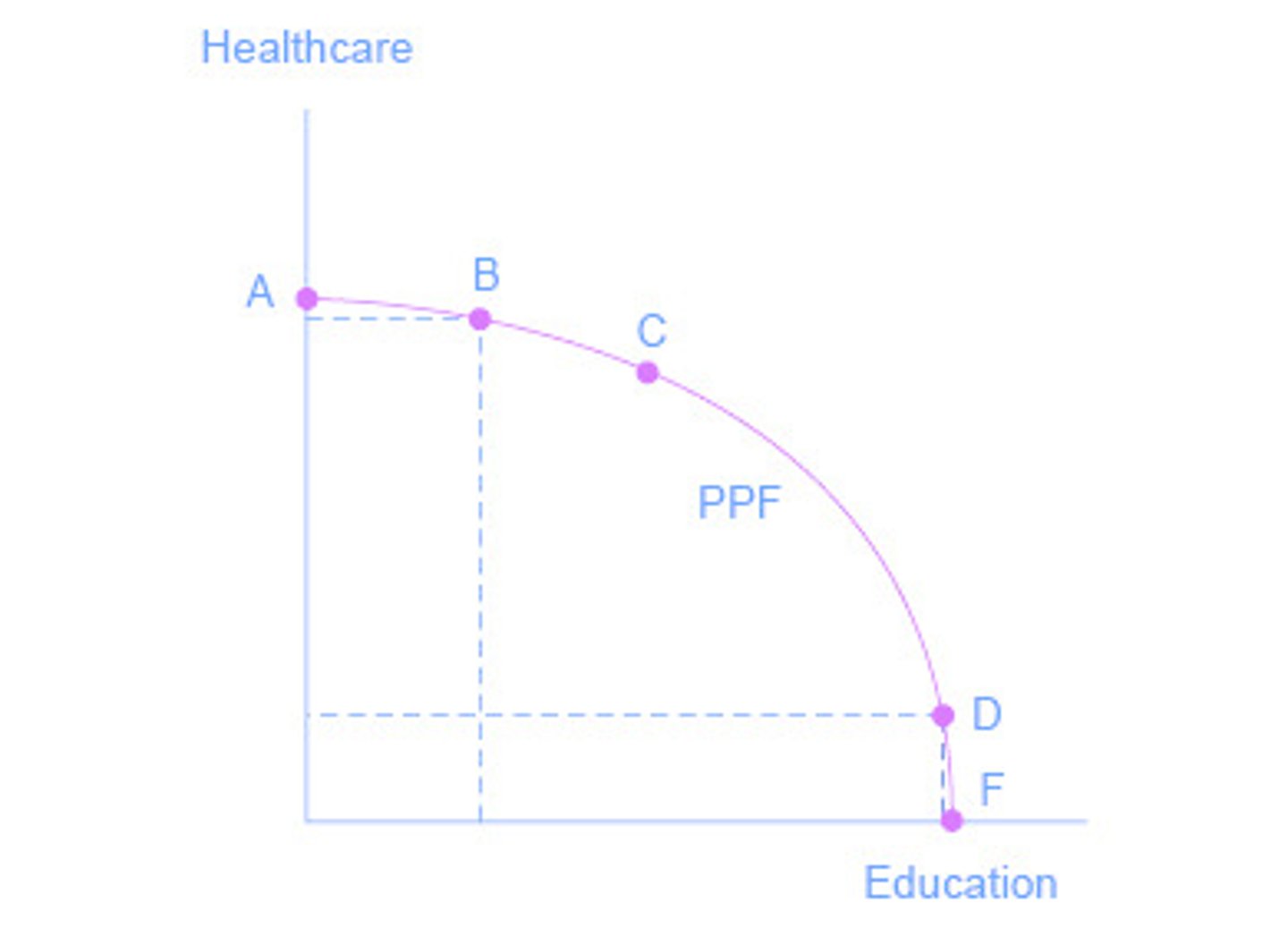

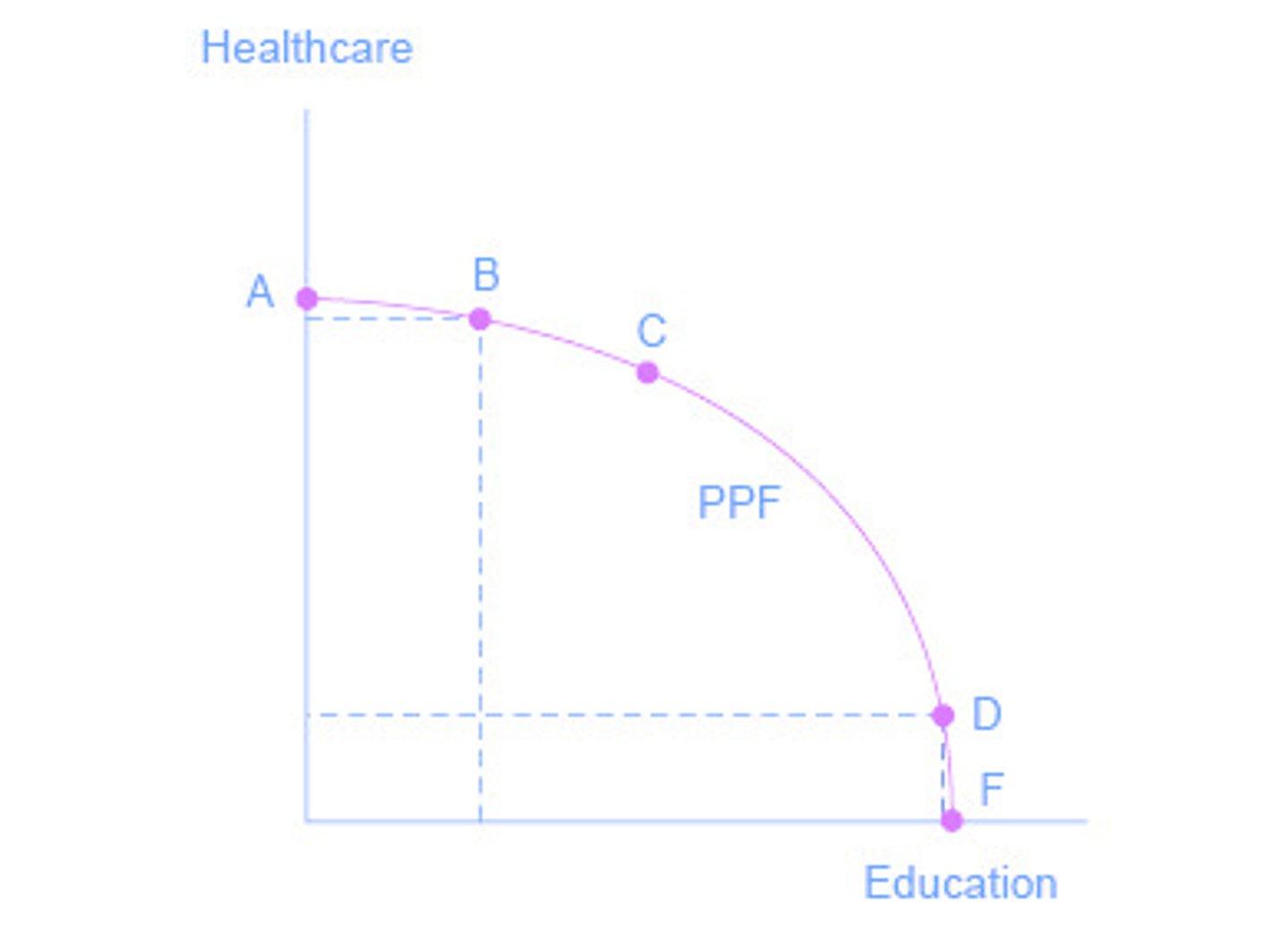

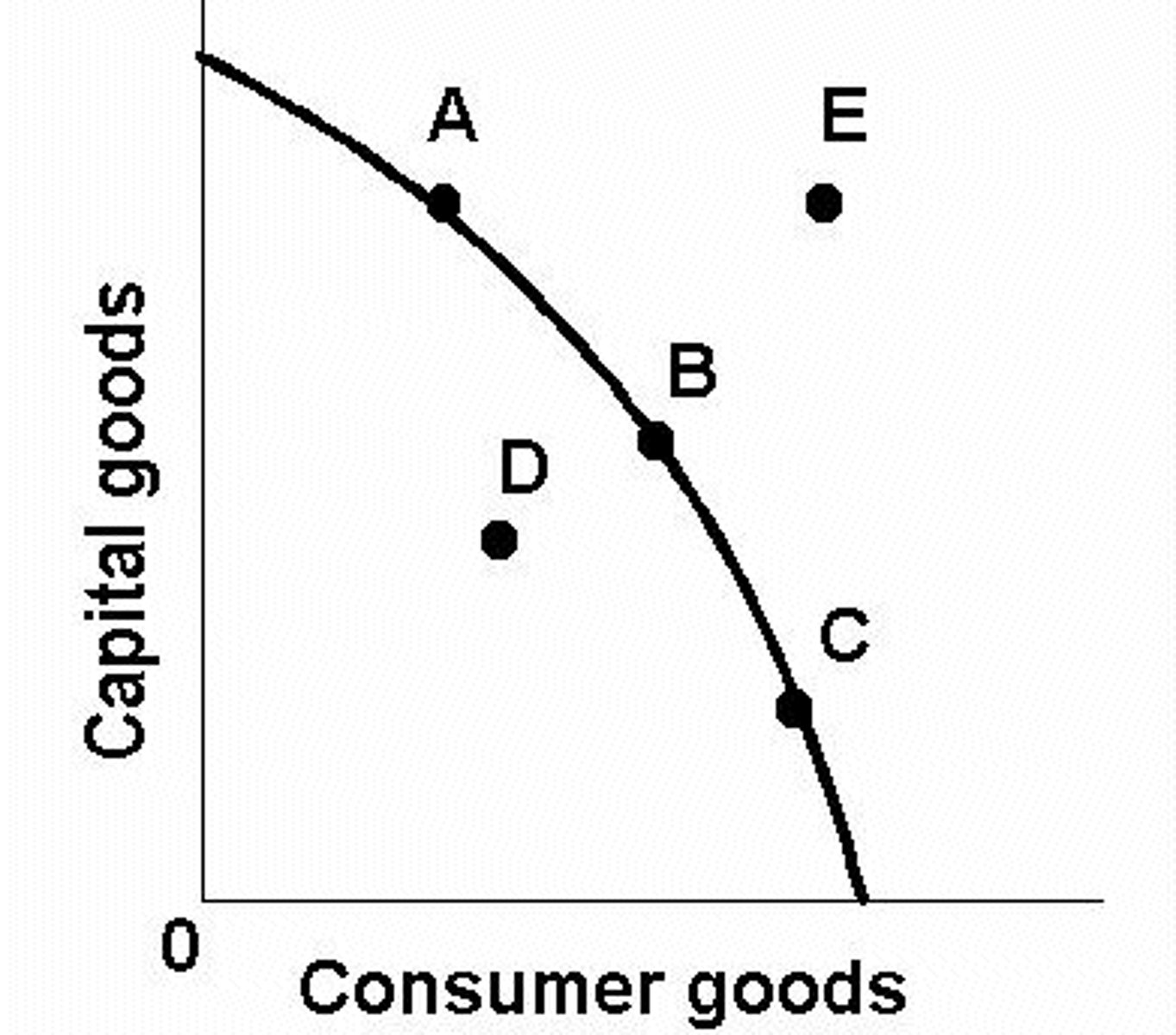

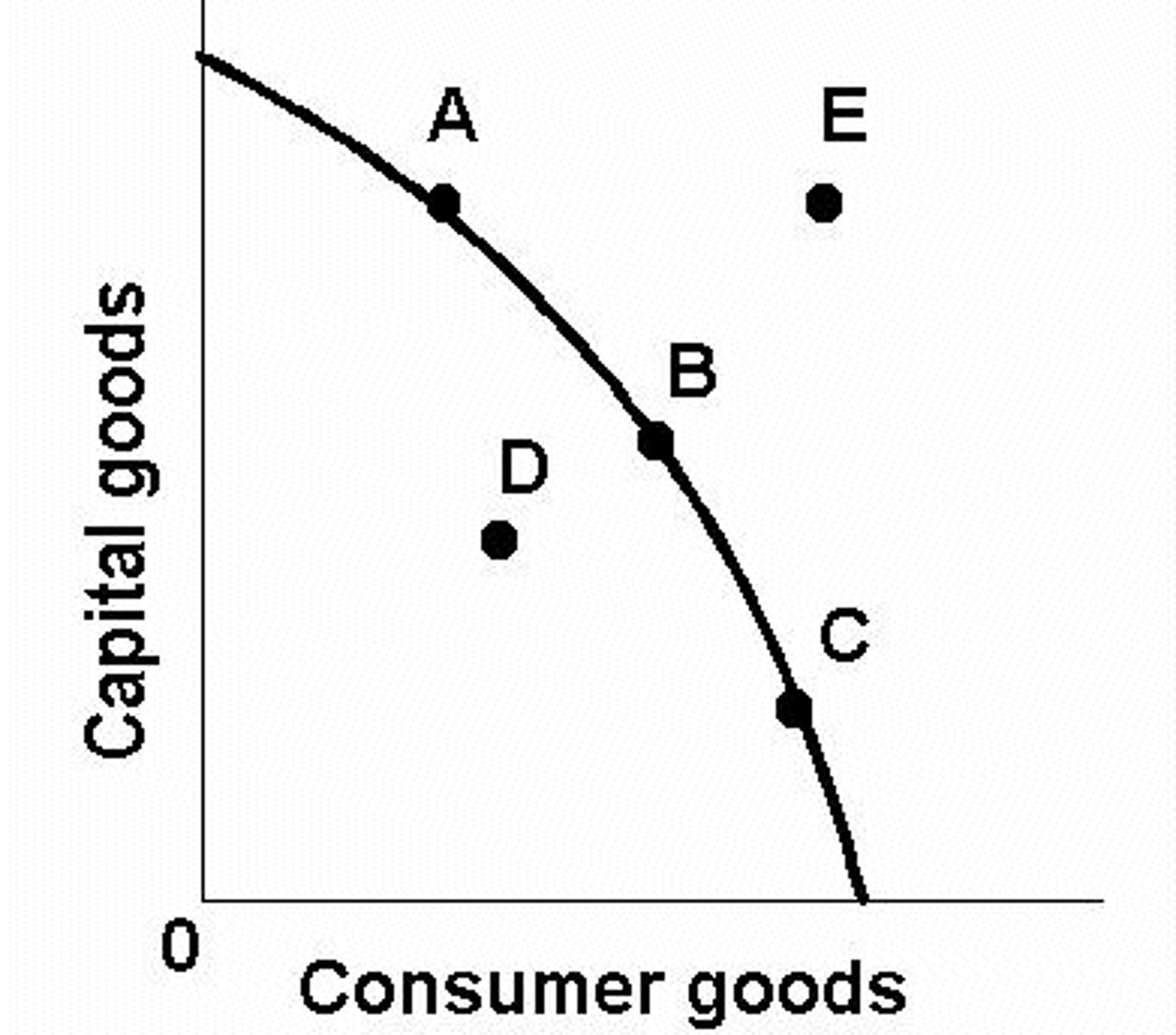

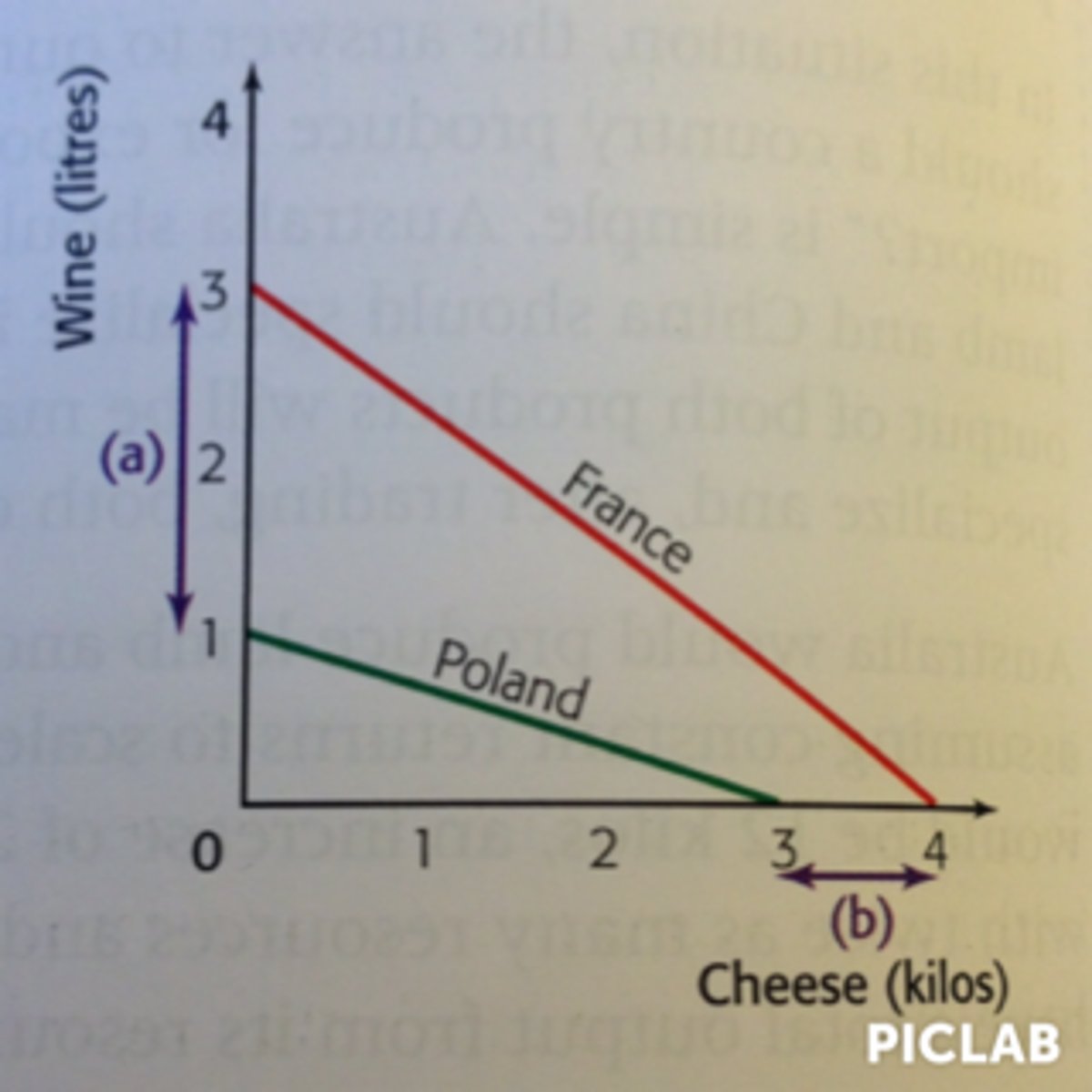

production possibilities frontier

a graph that shows the combinations of output of two goods/services that an economy can possibly produce given the available factors of production and the available production technology

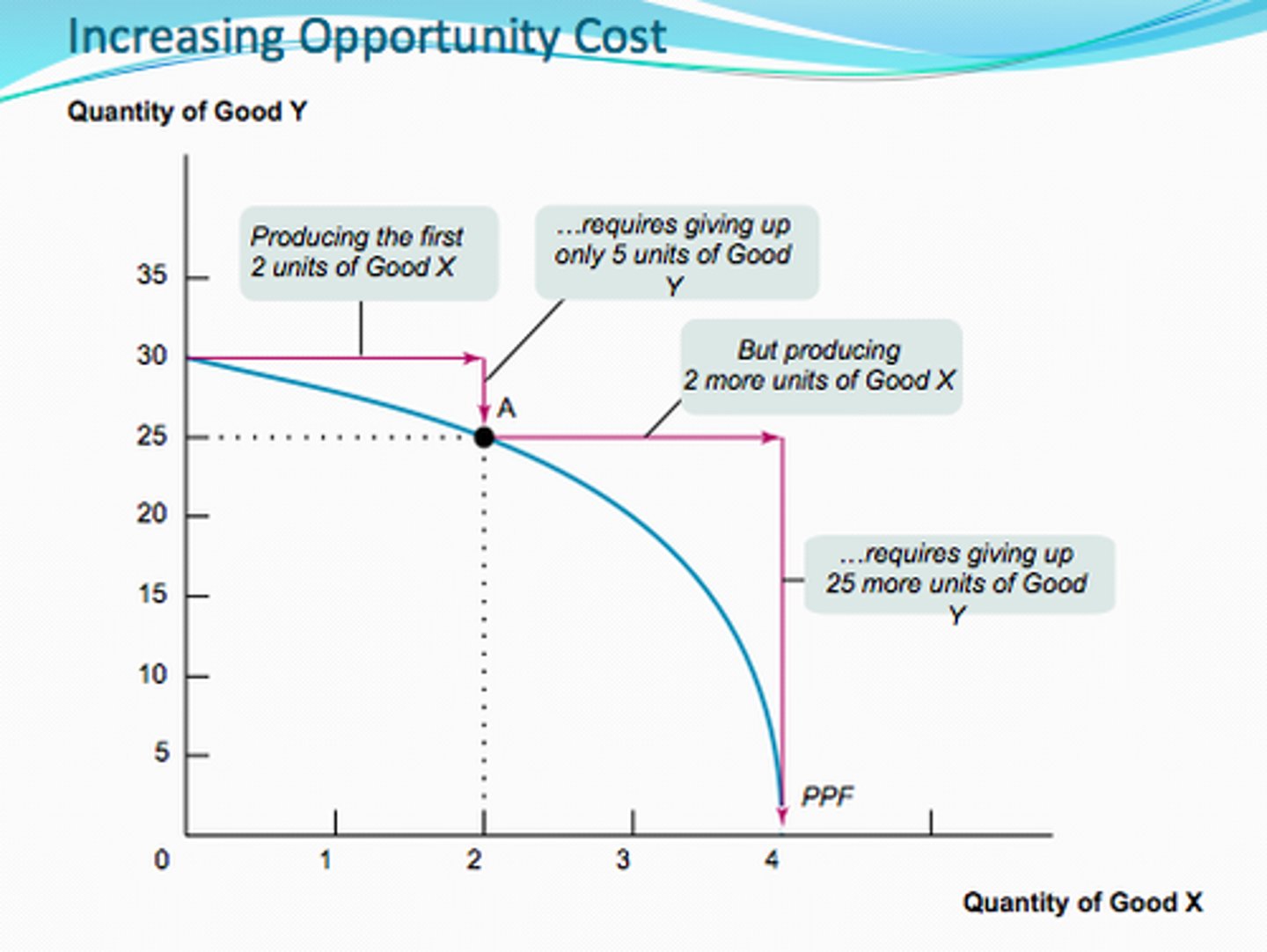

increasing opportunity cost

a situation in which producing more of one good requires giving up an increasing amount of production of another good (see image for visualization); this is why a PPF curve is bowed outward

imperfect transfer of resources

when reallocating resources for the production of a good/service, you would begin with resources that are most suitable/best adapted for producing the new good/service (e.g. a computer used for charting in a hospital could easily be used for instructional purposes in a classroom), but in order to continue producing more of the new good/service, you would eventually have to use resources that are less suitable/adaptable for its production (e.g. a stethoscope is extremely useful to a doctor, but not so much when trying to teach in a classroom)

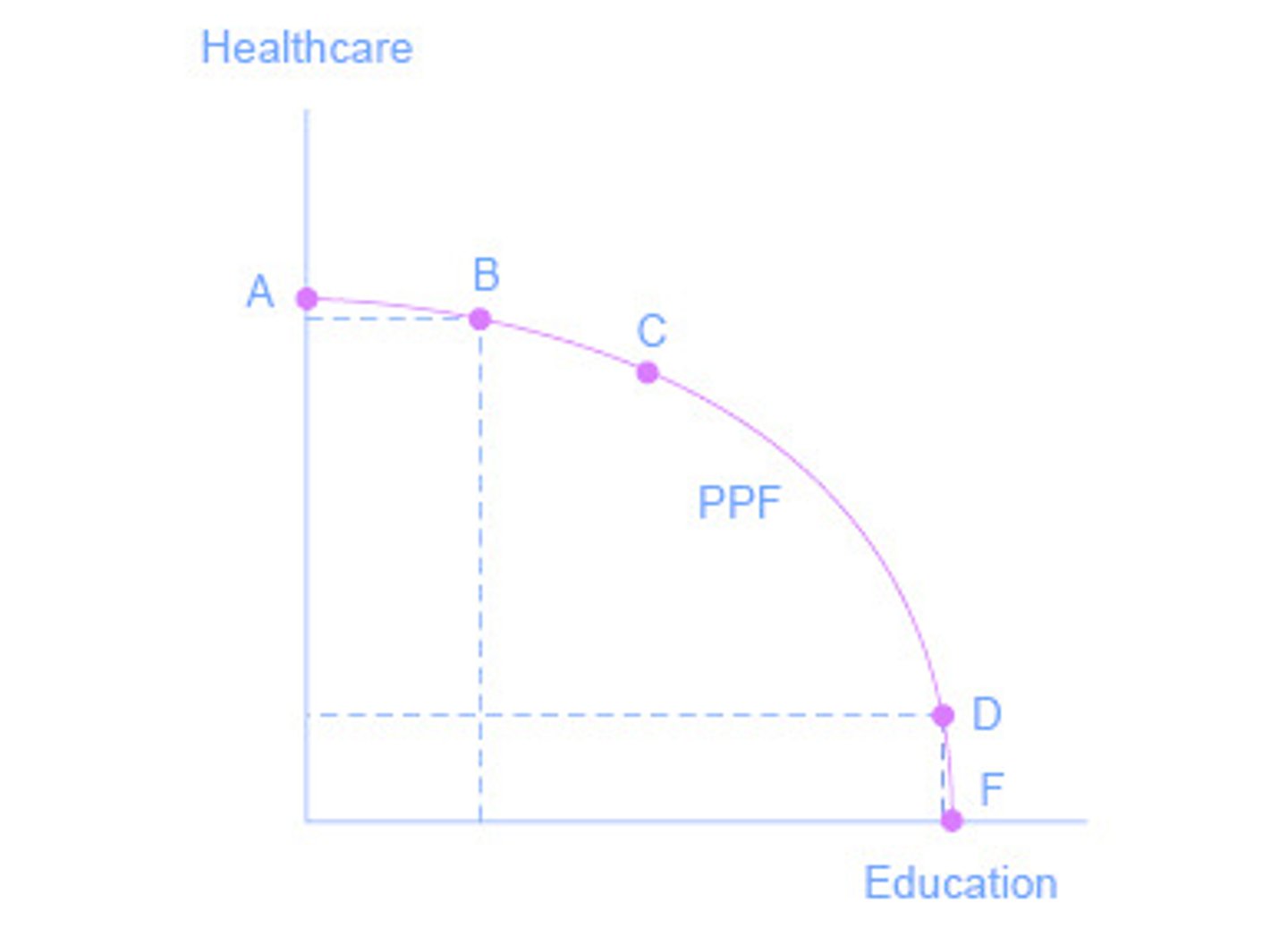

productive efficiency

producing the maximum amount of goods/services possible by using all available resources to their fullest (i.e. no wasted resources); this is represented by any point ON the actual PPF curve

Points A, B, C, D, and F on the PPF depicted are all "productively efficient" because they use all of the resources available with no waste, but they are not all necessarily "allocatively efficient" (see next term)

allocative efficiency

producing at a level considering the wants/demands of the society; typically seen as a combination of BOTH goods/services ON the actual PPF curve

Points B, C, and D on the PPF depicted are "allocatively efficient." As a society, we want both healthcare and education; not one extreme or the other (points A and F)

inefficient point

any point below the production possibilities curve (Point D), at which not all available resources are being used fully (i.e. under-utilization); in this scenario, more goods could be produced using the given existing resources

unattainable point

any point outside/beyond the production possibilities curve (Point E), which represents production beyond what can currently be produced with available resources; this point could be produced in the future through economic growth

economic growth

the ability of the economy to increase the production of goods and services from acquisition of additional resources, greater investment of capital, new technology, increased productivity, etc.; economic growth is shown by an outward shift of the PPF

Note: Economic growth can be symmetric (as depicted), meaning maximum possible production of BOTH goods increases through something such as improved education; economic growth can be asymmetric (not depicted), meaning there is increased productivity in only one of the two sectors of the economy (e.g. a new pesticide might increase corn production, but would not improve beef production)

marginal cost

the cost of producing one additional unit of a good/service; NOT the total cost

marginal utility (benefit)

the utility/benefit of consuming one additional unit of a good/service; NOT the total utility/benefit

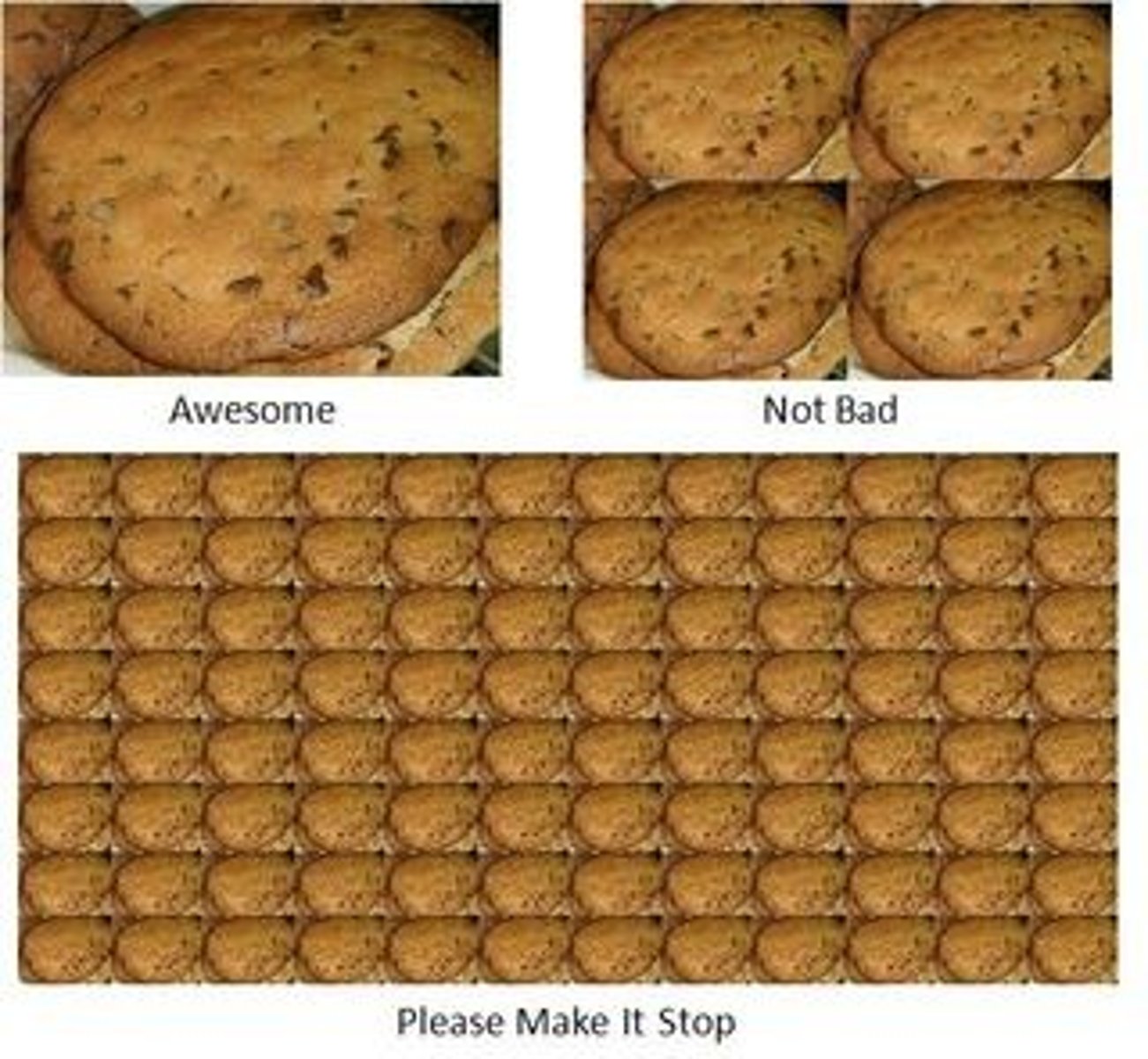

diminishing marginal utility

The Law of Diminishing Marginal Utility states that "as consumption increases the marginal utility derived from each additional unit declines, ceteris paribus (all else equal)." In other words, the more you consume something, the less satisfaction you get each time.

Think about how much you would enjoy eating a slice of chocolate chip cookie right now. Now, compare that to how much you would enjoy the 4th cookie in one sitting. How about the 96th cookie? It would be diminish over time, right (because you're full/getting nauseated)?

division of labor

assigning different parts of a production process or task to different workers in order to improve efficiency (which lowers cost per unit); in the context of trade, different steps of the production process are carried out by different countries but all ultimately contribute to the final product

specialization

by remaining focused on the production of narrow set of goods rather than all areas of production, an individual (or country, in the context of trade) can become more efficient in producing that good such that it generates enough to satisfy domestic demand/consumption and a surplus to trade with others

comparative advantage

the ability to produce a good at a lower opportunity cost than another producer or country (i.e. must give up less of other goods to produce the good)

Example: Compared to most other countries that we trade with, the U.S. has a comparative advantage in wheat production. The U.S. has to give up very few goods to produce more wheat, mainly because we have an abundance of resources (e.g. soil/climate) suitable for producing wheat. We do NOT have a comparative advantage in banana production when comparing the U.S. to a country like Costa Rica. Since our soil/climate is not well adapted for growing bananas, we would have to give up a great deal of other goods in an effort to reallocate resources to banana production. This is why the U.S. should specialize in producing wheat and Costa Rica should specialize in producing bananas, and then trade our surpluses with one another.

protectionism

the theory or practice of shielding a country's domestic industries from foreign competition by taxing imports (known as tariffs) or establishing quotas

Example: Since taking office, President Trump has imposed tariffs on imported items to the U.S. such as aluminum and steel as a way of helping protect American manufacturers, including the jobs of workers in those industries. This has led to a "trade war" with countries like China, who have implemented reciprocal tariffs on goods that they important from the U.S., such as soy and pork, and has hurt U.S. producers that rely on exporting their products (i.e. farmers).

Tragedy of the Commons

situation in which people, acting in their own self-interest, use up commonly available but limited (rivalrous) resources, typically leading to the overuse/extinction of the resource

Example: Wild fish stocks are a rivalrous good, as the amount of fish caught by one boat reduces the number of fish available to be caught by others. Since a fisherman's income is directly correlated with the amount of fish they catch, they are incentived to catch as many fish as possible. When each fisherman does this, it leads to the depletion of the fish stock and left unchecked, could lead to the extinction of the resource.

incentives

an action or reward that influences a decision and motivates/encourages one to act a certain way

Example #1: If your parents give you an allowance as long as you complete your list of chores each week, they are providing a monetary incentive for you to complete your chores.

Example #2: You have an incentive to pass up shooting a 6-point buck this year because you know that it could be an 8-point buck next year.

property rights

private ownership (i.e. not accessible to the general public) and the ability to exercise control over scarce resources through enforceable rules; this creates an incentive to sustainably use and conserve the resource to guarantee long-term access

disincentives

a negative or withdrawn reward, like a fine or a punishment, that motivates one to avoid an improper behavior

Example #1: If your parents ground you for breaking your 10:00 p.m. curfew, they are creating a disincentive for you to arrive home after 10 p.m., thus motivating you to avoid being late.

Example #2: You have a disincentive from shooting a spike buck in Pennsylvania because if the game warden catches you, you could receive a fine of up to $1,500, forfeiture of your hunting license, and face possible jail time (for repeat offenses).

regulations

rules, typically put in place by government or another authority, backed by the use of penalties that are intended to modify behavior; must be enforced for effect to take place

Three Basic Economic Questions

As a result of scarcity, all societies must answer three specific questions:

1. What to produce?

2. How to produce?

3. For whom to produce?

economic freedom

an economic value focused on the avoidance of government involvement/intervention in the production and distribution of goods and services

economic innovation & growth

an economic value focused on attaining greater levels of production and therefore income; growth relies upon innovation (in technology & capital) and improvements to productivity to take place (NOT a result of increased efficiency)

economic efficiency

an economic value focused on producing the most goods and services possible with the resources available; conservation & use without wast

economic security

an economic value focused on making certain that all can safely work/operate within the economy with little risk and ensuring that all members of society have access to necessities

economic equity

an economic value focused on enacting policies that benefit all members of society and strives toward equal outcomes

economic sustainability

an economic value focused on the ability of an economy to support a defined level of production indefinitely (into the future);

capitalism (market economy)

an economic system, championed by Adam Smith, in which individuals own the factors of production and make economic decisions based on the forces of supply and demand (i.e. the "invisible hand") in attempt to promote their own rational self-interest (profit maximization) through competition; buyers and sellers make decisions relatively free from government involvement

communism (command economy)

an economic system, championed by Karl Marx, in which the government (or the public) own the factors of production and makes economic decisions to guarantee a more equitable distribution of wealth among members of society; Marx argued that although capitalism is the most productive system, it leads to inequity where the capitalist class (bourgeoisie) dominates and takes advantage of the working class (proletariat), necessitating a working class revolt to achieve communal ownership of resources

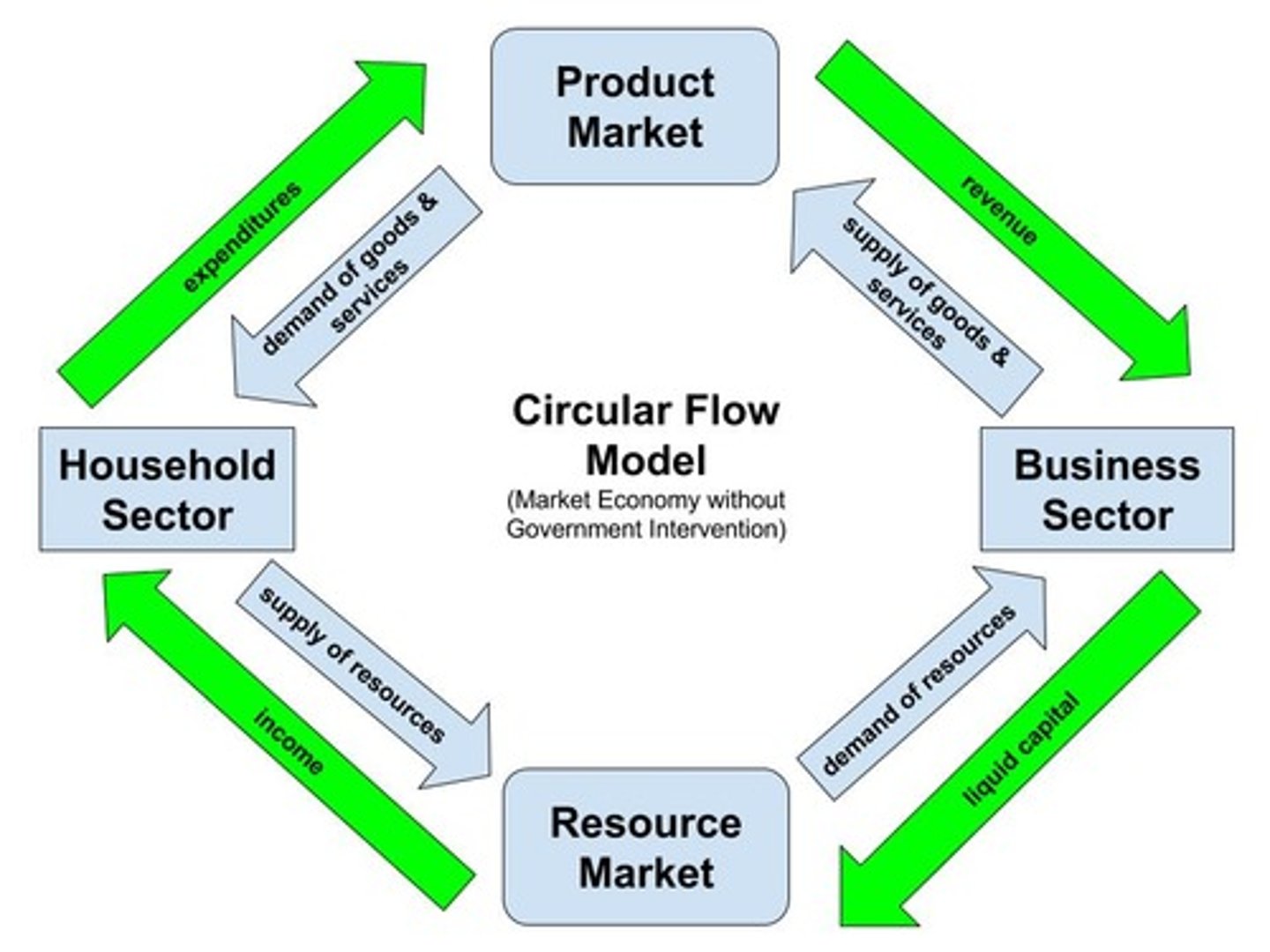

Circular Flow Model

a diagram that traces the flow of resources (e.g. land, labor, human capital), goods/services, liquid capital, income, and revenue among economic decision makers (i.e. Businesses & Households/Consumers); demonstrates how the market economy operations without governmental intervention

revenue

the income from the sale of goods and services; this = # of units sold x price/unit

profit

this = total revenue - total cost (expenses)

double coincidence of wants

one of the primary functions of money is ensure each party in an exchange/transaction happens to have what the other party desires, which leads to more efficient transactions

Note: a double coincidence of wants is less likely to occur in a system of bartering because one party may not possess a good/service that the other desires; thus, the reason most modern economies have evolved to revolve around some form of money

characteristics of money

The characteristics for "good money," according to former Fed Chair Paul Voelker, include:

divisible - can be made into smaller denominations ($10, $5, $1, $0.25, etc.)

easily held (portable) - can be carried on one's person for transactional purposes

trusted - all members of society will accept it for payment because they know that other members will accept it in return

durable - not easily destroyed; long lasting

uniform - all units look alike and are easily recognizable

limited supply - can not be too easily produced (by government or otherwise) that would make it too common and worthless

commodity money

objects that have value in themselves and that are also used as money for exchanges

Examples: grain, gold, cattle, nails, etc.

representative money

objects that have value because the holder can exchange them for something else of value

Examples: gold receipt, clay tablet linked to grain, silver certificate, etc.

fiat money

money without intrinsic value nor linked to anything of value but is used as money because of government decree and accepted because others are also willing to accept

Example: legal tender (this is currently the type of money that we use in the U.S. and most societies around the world)

medium of exchange

one of the functions of money that allows it to used to determine value and facilitate the exchange of goods and services (replaces barter system with potentially high transaction costs - how many chickens is equivalent to a cow?)

unit of account

one of the functions of money is to create a way to compare values; a car worth $25,000 and grapes worth $3.00 (able to make judgment of values)

store of value

one of the functions of money is to preserve purchasing power over time to be used for future spending (e.g. if I'm a tomato farmer in a barter system, I can only use my tomato to purchase something as long as it's fresh, because once it goes bad/starts to rot, it loses it's value; on the other hand, if I can sell my tomato now for money, I can hold on to that money and use it later when I need to purchase a good or service)