PAS 41 AGRICULTURE C22

1/15

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

16 Terms

Biological assets

are living animals and living plants.

Agricultural produce

is the harvested product of an entity's

biological assets.

Harvest

is the detachment of produce from a biological asset or the cessation of a biological asset's life processes.

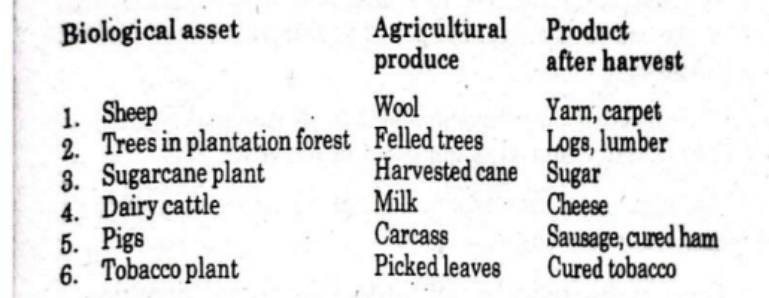

Examples of biological assets

The following table provides examples of biological assets,

agricultural produce and products that are the result of

processing after harvest.

Biological asset

1. Sheep .

9. Treesinplantation forest

3. Sugarcaneplant

4. Dairycattle

5. Pigs

6. Tobaccoplant

Agricultural Product

Wool

Felled trees

Harvested cane

Milk

Carcass

Picked leaves

Product after harvest

Yarn, carpet'

Logs, lumber

Sugar'

Cheese

Sausage, cured ham

Cured tobacco

Agricultural activity

___

is the management by an enlity of the

biological transformation and harvest of biological assets for sale

or for conversion into agricultural produce or'into additional

biological assets.

Examples of agricultural activity

Agricultural activity covers a diverse range of activities such

as the. following:

1. Raising livestock, such as poultry and piggery

2. Annual or perennial cropping

3. Cultivating orchards and plantations

4. Floriculture

5. Aquaculture, including fish farming

Recognition

An entity shall recognize a biological asset or agricultury

produce when:

a. The entity controls the asset as a result of past event.

b. It is probable that future economic benefits associated with

the asset will flow to the entity.

¢. The fair value or cost of the asset can be measured reliably

In agricultural activity, control may be evidenced by, fo,

example, legal ownership of cattle and the branding o,

otherwise marking of the cattle on acquisition or birth.

fair value less cost of

disposal.

biological asset shall be measured on initial recognition and

at the end of each reporting period at __

at fair value

less cost of disposal at the point of harvest.

Agricultuiral produce harvested shall be measured ___

measured at

fair value less cost of disposal.

Agricultural produce growing on bearer plant is ___

Gain on biological asset and agricultural produce

gain or loss arising on initial recognition of a biological asset at

fair value less cost of disposal and any subsequent in fair

value less cost of disposal shall be included in profit or loss,

A loss may arise-on initial recognition of a biological asset because

cost of disposal ¢ deducted in determining fair value less cost of disposal of a biological asset.

A gain may arise on initial recognition of a biological asset, for

example, when a calf is born. ¢

A gain may arise on initial recognition of agricultural produce

as a result of harvesting

Agricultural land

___ is not deemed a biological asset.

The _ may be classified either as property,

plant and equipment or investment property for purposes of

measurement.

bearer plant

___is a living plant used in the production of

agflcultural produce, expected to bear produce for more than one period and has a remote likelihood of being sold as

agricultural produce, except as scrap.

_ are used solely to grow agricultural produce

over several periods.

At the end of their productive life, the __ are

usually scrapped.

A __ that no longer bears produce is commonly cut

down and sold as scrap at the end of the productive life.

Agricultural produce growing on bearer plants

The agricultural produce as 'it ‘grows is measured at the epy

of each reporting period prior to harvest at fair value leg,

cost of disposal.

The agricultural produce growing on bearer plant is classifieq

as biological asset.

Once harvested, the agricultural produce is measured at faj,

value less cost of disposal at the point of harvest.

The fair value less cost of disposal at the point of harvest ig

the deemed cost of inventory.

The harvested product is recorded as inventory and recognized

as gain from agricultural produce.

Bearer animals

___, like bearer plants, may be held solely for

the produce that they bear.

However, bearer animals continue to be reported as

biological assets and not property, plant and equipment.

Animal-related recreational activities

Managing recreational activities, for example, game parks

and zoo, is not agricultural activity.

The reason is that there is no management of the biological

asset but simply control of the number of animals.

" The natural breeding that takes place is not a managed activity and is incidental only to the main activity of providing

a recreational facility. i

Accordingly, animals related to recreational activities shall

be accounted for as property, plant and equipment.