ECON 3330 ~ Exam 2

1/81

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

82 Terms

coupon bonds

require coupon payments —> % of the bonds face value

( periodic coupon payments + principal repayment at maturity )

zero-coupon bond yield

promise a single payment on a future date , pays no additional coupon payments

- Ex: Treasury Bill

if coupon rate (%) < interest rate (%)?

bond price < face value

if coupon rate (%) i> interest rate (%)?

bond price > face value?

- you still get a total return that's greater than price!

consol (aka perpetuity)

security that makes annual interest payments forever, principal is never repaid

Consol Price = ?

Annual payment / interest ( i as a decimal )

who is yield to maturity relevant and irrelevant to?

relevant for long term investors and irrelevant for short term investors

current yield = ? —> a percent

(coupon payment / purchase price) x 100

how is yield to maturity different than current yield?

- ytm is used for long term investors bc it calculates total return if bond is held to maturity date (calculates capital gains/losses)

- current yield is used for short term investors and disregards capital gains/losses (return on coupon payments)

holding period return

buying and selling early

- plans change so CY doesn't make sense

Holding Period Return = ?

(Coupon Payment / Purchase Price) + [(Selling Price - Purchase Price) / Purchase Price]

bond ratings

assessing risk of the potential investments (bonds)

Bond Ratings:

Investment Grade

least risky; highest quality borrowers - guaranteed return

- (AAA, AA, A, BBB)

Bond Ratings:

non-investment grade

below BBB

Bond Ratings:

non-investment grade:

speculative

some default risk (missing/late payment) but not immediate concern

- (BB, B)

Bond Ratings:

non-investment grade:

highly speculative

borrowers with clear default risk (missing/late payments)

- (CCC, CC, C, D)

fallen angels

issuers that were once investment grade, but they've been downgraded

rising stars

new issuers w/o a track record of creditworthiness

how does an upgrade affect a bond's price and its yield?

Price rises, Yield falls

how does a downgrade affect a bond's price and its yield?

Price falls, Yield rise

commercial paper

very short term bond, 0% coupon, unsecured —> only most creditworthy issuers can use

- 5 < n < 45 days (average is 30 days)

secured debt

collateral (pay these 1st bc if you don't, they'll take your stuff away)

- house (mortgage), car (car note)

unsecured debt

no collateral (pay these last bc your stuff won't be taken)

- loans, debt

Commercial Paper Ratings:

p-1

90% (of the time commercial paper is P-1)

Commercial Paper Ratings:

p-2

9% (of the time commercial paper is p-2)

Commercial Paper Ratings:

p-3

exist, but cannot be issued (you were p-1 or p-2, but you became a "fallen angel")

municipals

gov't bonds that are tax exempt

after tax yield = ?

taxable yield x (1 - tax rate)

Term Structure of Interest Rates:

How Are Short-Term and Long-Term Yields/Interest Rates Related?:

Short-Term Yields are more volatile (unpredictable/risky)

Long-Term & Short-Term Yields move together

Long term Yields > Short term Yields

expectations hypothesis

says that Bonds with different maturities are perfect substitutes for each other, which can explain the trend of the yields moving together and the trend that short-term yields are more volatile

liquidity premium theory

says that As “n” increases, risk increases, explaining why Long-Term Yields are greater than Short-Term yields. As more time passes, lenders are more uncertain that they will be repaid, so they charge a higher risk premium.

yield curve

relates ytm to time to maturity (N)

what does a normal yield curve show?

- positive (normal) slope

- rates are expected to rise

- lt rates > st term rates

what does a no slope yield curve show?

that for any period of investments they equal

- lt rates = st rates

what does an inverted yield curve show?

- rates expected to fall

- if you're a borrower you might want to wait

- predicts recession within a yr

- st rates > lt rates

- negative slope

what is significant about the inverted yield curve?

the inverted yield curve shows recession

- may be a recession w/o inverted yc, but every time there's an inverted yc there is recession

explain how yield curves might be used as a tool for forecasting recessions?

the different yield curves show how the economy is doing

- normal is good

- 0 slope is questionable

- inverted indicates a recession

stock

share of ownership in a firm

residual claimants

in a liquidation, stockholders are paid last after all other creditors

limited liability

stockholders can lose no more than their initial investment

dow jones industrial average (DJIA)

tracks the performance of the top 30 U.S. firms, Price-weighted index (greater weight to firms with larger share prices), measures the return to owning a typical share of stock

s&p 500 index

value-weighted index ~> firms get more weight if they have larger market capitalization

mirrors changes to economy’s overall wealth and is a good benchmark for investments and investment strategies

Market Capitalization

The value of a firm

total market value of a firm:

market cap equation

share prices x total shares outstanding

what is the difference between the DJIA and the S&P 500?

the S&P 500 relates to the economy

- if S&P 500 is up, the economy is up

DJIA just takes into consideration the share prices

Mutual Funds

Index Mutual Funds: portfolio built to mimic overall market performance

Managed Mutual Funds: portfolio built by an investment manager

Why are Mutual Funds attractive Investments?

Affordability

Liquidity

Diversification

Management (professionals vs. indexes)

Cost (lower index fund fees)

Theory of efficient markets

Price reflects all available information

Implies stock price movements are unpredictable

Impossible to beat the market

What is a “Random Walk”

We don’t know which stocks will increase or decrease in value → no one can beat the market average

% Recovery = ? (increase necessary to recover from a given stock market decline)

[Decline / (100 - Decline)] x 100

what are the 4 categories of mutual funds?

- large cap

- mid cap

- small cap

- international

what is the key difference for ROTH IRA's?

they grow tax free

are stocks risky investments in the short run? In the Long run?

Yes, stocks are volatile in the short run, but stable in the long run

How do stocks compare to bonds in the long run?

stocks are safer and outperform bonds for every 30 yr Time Period

asset bubbles

persistent or expanding gaps between actual asset values and those warranted by fundamentals

what happens to firms inside bubble as asset bubble inflates?

firms inside bubble are linked to the new asset

- find finance easy to obtain

-tend to overinvest in these companies

what happens to firms outside the bubble as asset bubble inflates?

firms outside bubble are not linked to new asset

- firms outside bubble find finance difficult to obtain

-tend to under invest in these companies

what happens when the bubble eventually (and it will eventually) burst?

markets CRASH —> decreased sales, decreased revenue, decreased employment for everyone as households reassess their wealth

asymmetric (imperfect) information

2 parties to a transaction have unequal information

adverse selection

if quality cannot be assessed, then only "bad choices" remain in the market

what's the 1st solution for buyers to find out if it's a peach or lemon?

warranty

- allows buyers to know that they are getting a reliable car

signaling

an action taken by the informed party that reveals important information to an uninformed party

effective signals are _____ , talk is _____

expensive, cheap

whats the 2nd solution to find out if peach or lemon?

screening beforehand (screening afterwards is too late)

Price Discrimination

Charging different rates for different people —> risk must be accounted for in price

moral hazard

occurs when effort cannot be observed so managers can't tell whether bad outcome is intentional or bad luck

sometimes borrower may not act in best interest of lender. What is the solution?

restrictive covenant

- you have to use $ on what you told bank you would use it on

principal agent problem in equity finance

owners (shareholders) (aka principles) hire managers (aka agents) to run firm day to day

- owners are separated from control

- owners goal is to max share price (increase wealth) but managers goal is to not get fired. this creates a problem bc managers take too little risk bc they dont want to get fired

- no risk = no growth

solution to principal agent problem in equity finance

have mgmt invest in company stock

- takes care of moral hazard (now effort can be assessed - if stock value increases, effort has increased) but this doesn’t fix all problems

- Beware of fraud

how are adverse selection and moral hazard problems in financial markets?

when you cannot assess quality (adverse selection) and you cannot assess effort (moral hazard) you create failing situations.

- we need price discrimination (adverse selection) and restrictive covenants (moral hazard)

limited liability/moral hazard problem in debt finance

owners keep all profits in excess of debt payments —> might cause mgmt to take too much risk

solution to limited liability/moral hazard in debt finance

force borrowers into a restrictive covenant

what must you do after implementing your "solutions" to principal agent problem in equity finance and limited liability/moral hazard problem in debt finance?

you must monitor afterwards - you only abide by the rules (restrictive covenant) if you're being monitored

what are some ways you can monitor after implementing your solution?

- check inventories

- membership on board of directors

- stake in ownership

- threat of takeover

financial arbitrage

We try to buy low and sell high

Bond Price = ?

[Coupon Payment / (1 + i)^n] + [Face Value / (1 + i)^n]

Yield to Maturity (i) = ?

[(Coupon Payment + Face Value) / Purchase Price] - 1

Three types of bond risk

Default Risk

Interest Rate Risk

Inflation Risk

Bond Risks —> Default Risk

risk of a missed payment

Bond Risks —> Interest Rate Risk

prices & interest rates are inversely related → interest goes up, bond prices fall = capital loss | interest goes down, bond prices rise = capital gain

Bonds Risks —> Inflation Risk

r = i - π → π goes up, r goes down → Lenders 🙁, Borrowers 🙂

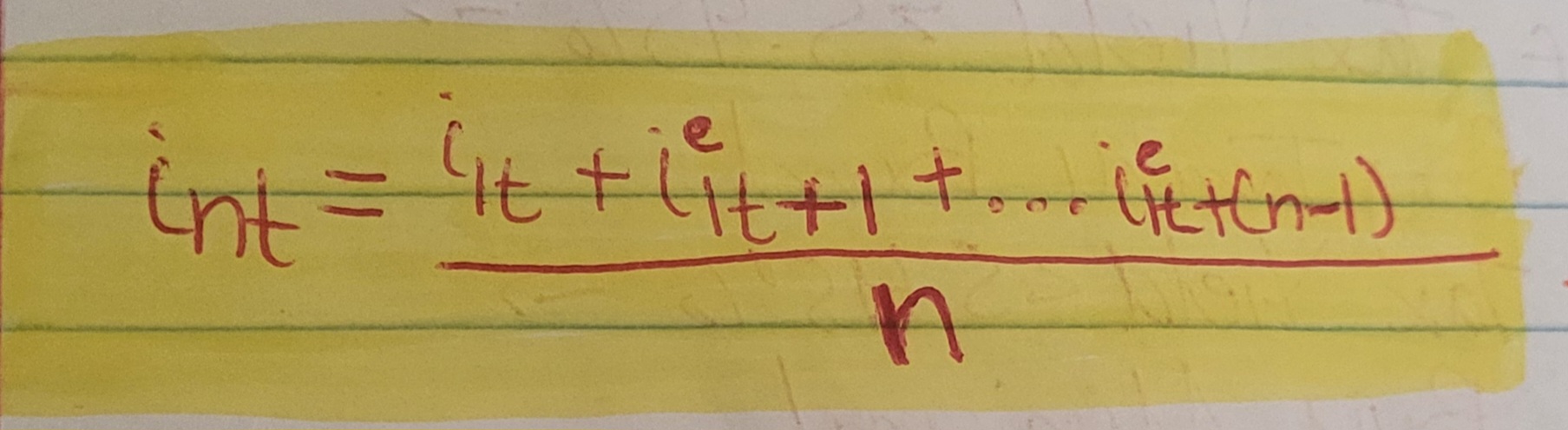

Expectations Hypothesis w/ Interest Rates