Reporting depreciation

1/12

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

13 Terms

acquisition

When a business acquires an asset

What is accumulated depreciation?

The initial cost of acquiring an asset.

The amount of money saved to purchase new assets.

The total amount of depreciation expense that has been allocated for an asset since it was put into use.

The total value of all assets in a business.

The total amount of depreciation expense that has been allocated for an asset since it was put into use.

Accumulated depreciation is the total amount of depreciation expense that has been allocated for an asset since it was put into use. It represents the gradual decrease in the value of the asset over time due to depreciation.

How is accumulated depreciation account classified?

It is classified as a liability account.

It is classified as an expense account.

It is classified as an asset account.

It is classified as a contra asset account.

It is classified as a contra asset account.

Accumulated depreciation is classified as a contra asset account. Contra accounts are used to offset the balance sheet. In the case of accumulated depreciation, it offsets the value of the corresponding asset account.

How is accumulated depreciation recorded in the chart of accounts?

It is classified as a sub-account under the asset account.

It is classified as a liability account.

It is classified as an income account.

It is classified as an expense account.

It is classified as a sub-account under the asset account.

Accumulated depreciation is recorded in the chart of accounts as a sub-account under the asset account. This helps in organizing and tracking the accumulated depreciation specifically for each asset.

What is the purpose of an asset account?

To track the depreciation expense of an asset.

To record the accumulated depreciation of an asset.

To represent the initial value of an asset.

To calculate the profit generated by an asset.

To represent the initial value of an asset.

The purpose of an asset account is to represent the initial value of an asset. It helps in tracking the cost and value of the asset over time.

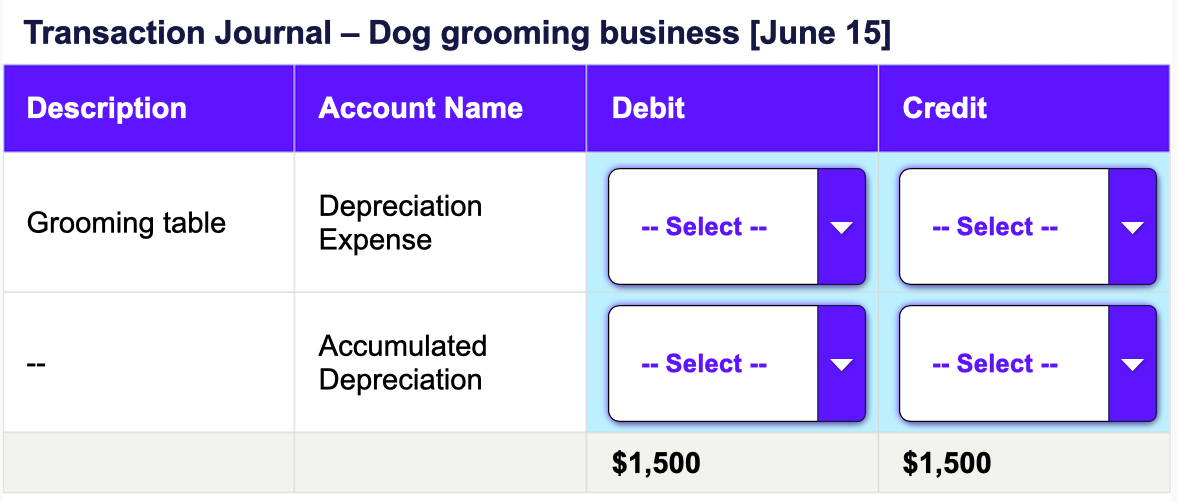

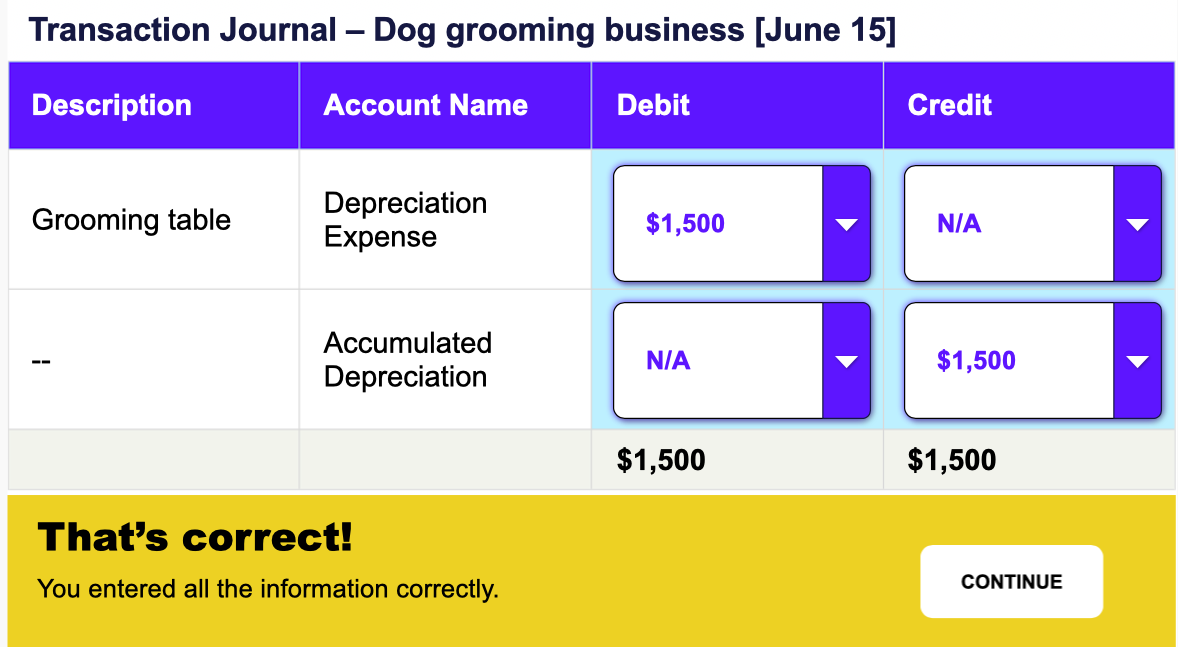

Ben owns a small dog grooming business. He recently purchased a grooming table for his new business workspace. The table has an original cost of $15,000 and an estimated useful life of 10 years with no salvage value. The business's CPA has advised you, as the bookkeeper, to use the straight-line depreciation method for this asset. At the end of the first year, the business needs to record the depreciation expense.

Which of the following statements accurately describes the nature of the depreciation expense account’s balance?

Depreciation expense has a credit balance.

Depreciation expense has a debit balance.

Depreciation expense has a zero balance.

Depreciation expense can have either a credit or debit balance.

Depreciation expense has a debit balance.

Depreciation expense is recorded as a debit entry in the accounting records, representing the portion of an asset’s cost that is recognized as an expense over its useful life.

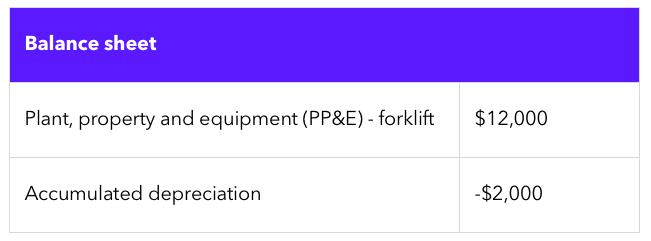

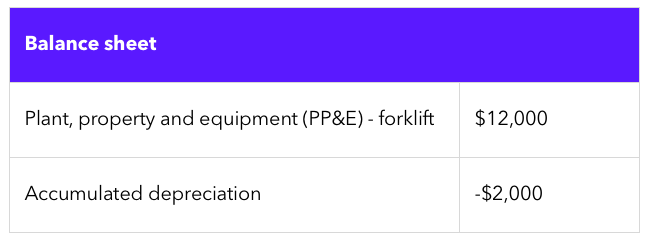

Assume a 6-year useful life.

The following shows the balance sheet for a business with a forklift that has been in service one year. What will the accumulated depreciation value be after 3 years?

$8,000

-$8,000

$6,000

-$6,000

-$6,000

On the balance sheet, where accumulated depreciation is shown, it will have a negative value. This negative value helps reduce the overall value of the asset.

Annual depreciation expense = (Initial value - Salvage value) / Useful life Annual depreciation expense = $12,000 - $0 / 6 annual depreciation expense = -$2,000

Accumulated depreciation after 3 years = -$2,000 × 3 = -$6,000

What will the book value of the forklift be in 3 years?

$8,000

-$8,000

$6,000

-$6,000

$6,000

To calculate the book value of the asset after 3 years, we subtract the accumulated depreciation from the initial value of the asset.

Book value = Initial value - Accumulated depreciation

Book value = $12,000 - $6,000 = $6,000

After 3 years of straight-line depreciation, the book value of the asset would be $6,000. This represents the remaining value of the asset that has not been depreciated over the period.

When an asset is fully depreciated and sold for an amount higher than its book value, what is the financial impact?

The business records a loss on asset disposal.

The business records a gain on asset disposal.

The business does not record any financial impact.

The bookkeeper removes the asset from the books.

The business records a gain on asset disposal.

When an asset is sold for an amount higher than its book value, the business records a gain on asset disposal to reflect the positive financial impact of the sale.

How is depreciation expense typically recorded in the books? Select all that apply.

Debit the depreciation expense account

Credit the depreciation expense account

Debit the accumulated depreciation account

Credit the accumulated depreciation account

Debit the depreciation expense account

Credit the accumulated depreciation account

To record depreciation expense you will need to debit depreciation expense and credit accumulated depreciation.

What does it indicate if the depreciation expense account has a credit balance?

Depreciation expense is overstated

Depreciation expense is understated

Additional review is needed as it is unusual

The depreciation method used is incorrect

Additional review is needed as it is unusual

Depreciation expense normally carries a debit balance, so a credit balance is unusual and may indicate an error or unusual circumstance that requires further review.

On which financial statement is depreciation expense typically reported?

Balance sheet

Income statement

Statement of cash flows

Statement of retained earnings

Income statement

Depreciation expense is typically reported on the income statement as an expense item.