Reporting depreciation

The lifecycle of an asset

The lifecycle of an asset involves various stages, starting from its acquisition to its eventual disposition.

Stages of the asset lifecycle:

Acquisition

A business purchases or acquires an asset

Depreciation

The process by which the cost of the asset is allocated over its useful life

Ongoing use and maintenance

Throughout the useful life of an asset, bookkeepers monitor and record any ongoing costs associated with its use and maintenance

Disposition

At the end of an asset’s useful life, the business may decide to remove, sell, or dispose of the asset

Acquisition

Asset account and accumulated depreciation

When an asset is acquired, a bookkeeper creates an asset account to represent its initial value.

This account keeps track of the cost of the asset.

An accumulated depreciation sub-account is established.

Accumulated depreciation represents the total amount of depreciation expense that has been allocated for the asset since it was put into use.

Calculating accumulated depreciation

Accumulated depreciation increases each year offsetting the value of the asset.

Contra asset account

Accumulated depreciation is a specific type of contra asset account.

A contra account is set up to offset the balance of another account on the balance sheet.

In the case of accumulated depreciation, it reduces the overall value of the asset.

Unlike regular asset accounts, the natural balance of accumulated depreciation is either zero or a credit (negative) balance.

Note: Negative values are often noted by being shown in parenthesis, for example: ($6,000).

Sub-account in the chart of accounts

The chart of accounts is a list of all the accounts used in a business’s financial records.

Within the chart of accounts, the accumulated depreciation account is set up as a sub-account.

This helps organize and track the accumulated depreciation specifically for each asset.

Journal entry

When depreciating an asset, you need to credit the accumulated depreciation account in the journal entry.

This account is special because it is a contra asset account with a credit balance.

Depreciation expense = (original cost - salvage value) / useful life

Depreciation: financial statements

Depreciation impacts both the balance sheet and the income statement

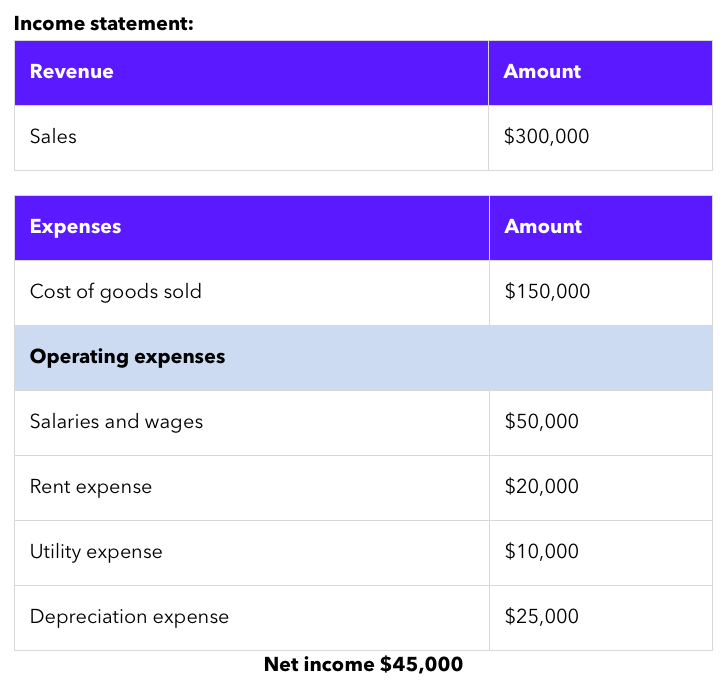

Income statement

Depreciation expense is listed as one of the expenses

It represents the portion of an asset’s cost that is recognized as an expense over the accounting period.

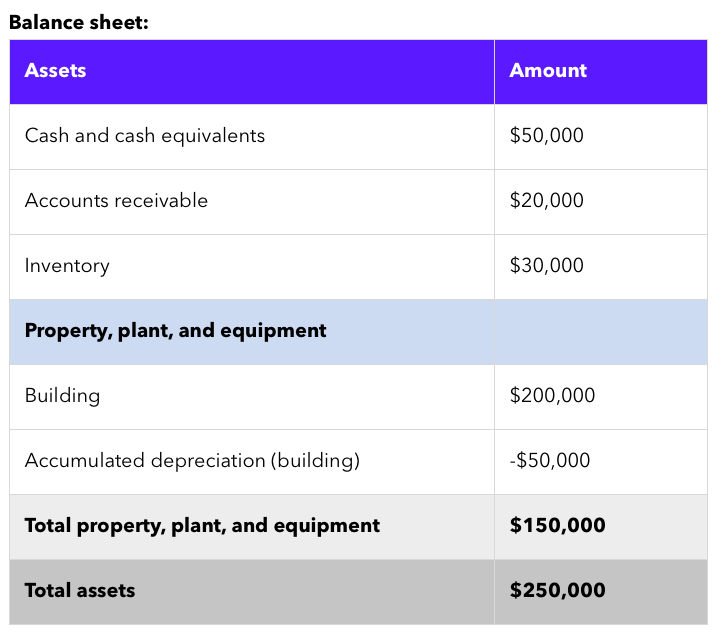

Balance sheet

Accumulated depreciation is a contra asset account, as it works in the opposite direction of other asset accounts and carries a credit balance.

This account helps reduce the balance of the corresponding asset account on the balance sheet.

The accumulated depreciation for an asset will increase over time as depreciation is recorded over the useful life of the asset.

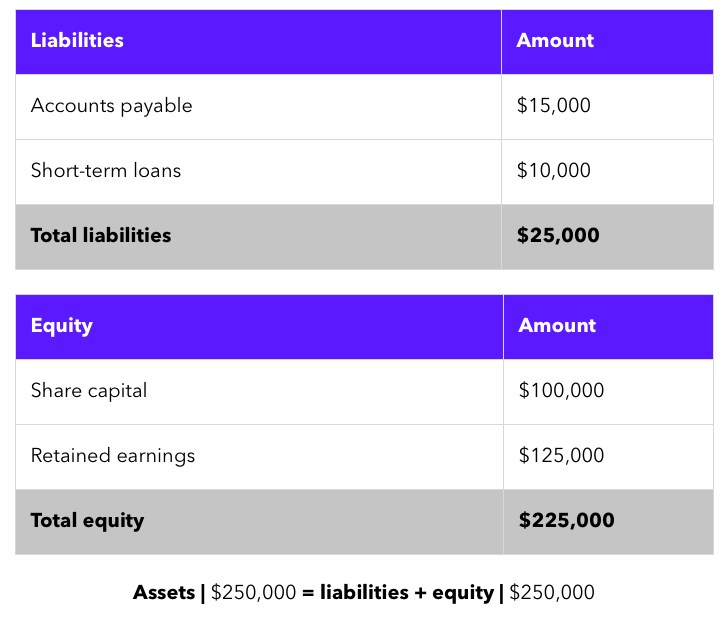

When you compare the balance sheet and the income statement side-by-side, you’ll notice a specific pattern.

When you compare the balance sheet and the income statement side-by-side, you’ll notice a specific pattern.

On the balance sheet, where accumulated depreciation is shown, it will show a negative value.

This negative value helps reduce the overall value of the asset.

On the income statement, where we find depreciation expense, it will have a positive value.

It is an expense because it represents the amount of asset cost that has been used up during the accounting period.

Disposition

When an asset reaches the end of its service life, it’s either sold, removed, or disposed of by the business.

Zeroing out the accounts

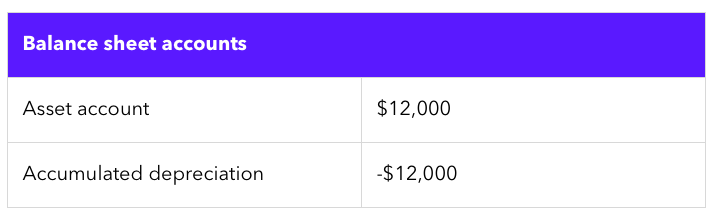

At the end of the asset’s service life, the net effect of the balance sheet accounts related to the asset should be zero.

This means that the asset account and its corresponding accumulated depreciation sub-account should zero each other out.

Disposal of asset with no book value

There may be a gain or loss on an asset disposal.

When an asset with no salvage value is sold at the end of its service life, the bookkeeper first records a journal entry to zero out the asset accounts.

After the entry to zero out the asset account is made, a second entry will need to be made to Other income to record any gain, or to the appropriate expense account if there is any loss, upon the disposal of the asset.

Journal entry with gain:

Debit: Cash account

Credit: Other income

Journal entry with loss:

Debit: Expense account

Credit: Cash account

Disposal of asset with remaining book value

This may be due to disposal before being fully depreciated or it may have a salvage value.

Salvage value is the remaining book value of an asset that has already been fully depreciated or is at the end of its service life.

An asset at times is disposed of for less than its book value. In these cases, the business realizes a loss that must be expensed.

For example:

We have a vehicle with a remaining book value of $2,000. If the business sells it for $5,000, Cash would be debited for $5,000, Accumulated depreciation would be credited for $2,000, and the remaining $3,000 would be credited to Other income

Journal entry with gain:

Debit: Cash account

Credit: Accumulated depreciation

Credit: Other income

If the business sold it for $1,500, Cash would be debited for $1,500, the $500 loss debited to Other expense, and Accumulated depreciation would be credited for $2,000.

Journal entry with loss:

Debit: Cash account

Debit: Other expense

Credit: Accumulated depreciation

When an asset is disposed of, bookkeepers ensure that the asset account and accumulated depreciation account zero out. They may record any gain as other income and any loss as other expense.

The salvage value of an asset represents the amount the business expects to receive when selling or disposing of the asset at the end of its useful life.