AP Micro Economics Unit 1

1/63

Earn XP

Description and Tags

fuhyuh

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

64 Terms

Scarcity

The problem of economics (unlimited wants but limited resources)

Incentives

How we make decisions

Opportunity Cost

What is given up when a decision is made (the 2nd choice)

Market Economies

Individuals and Private entities make decisions. (Property rights = incentives)

Command Economies

Governments or Central bodies make decisions

Land

Natural Resources (timber, oil, coal)

Labor

Workers

Capital

Machines, tools, buildings

Entrepreneurship

the owning of a business? idrk

Microeconomics

Small economics (zoomed in)

One single industry, store, person

Macroeconomics

Whole economy

U.S. Unemployment

Normative

based on norms, beliefs

positive

based on positions, facts/reality

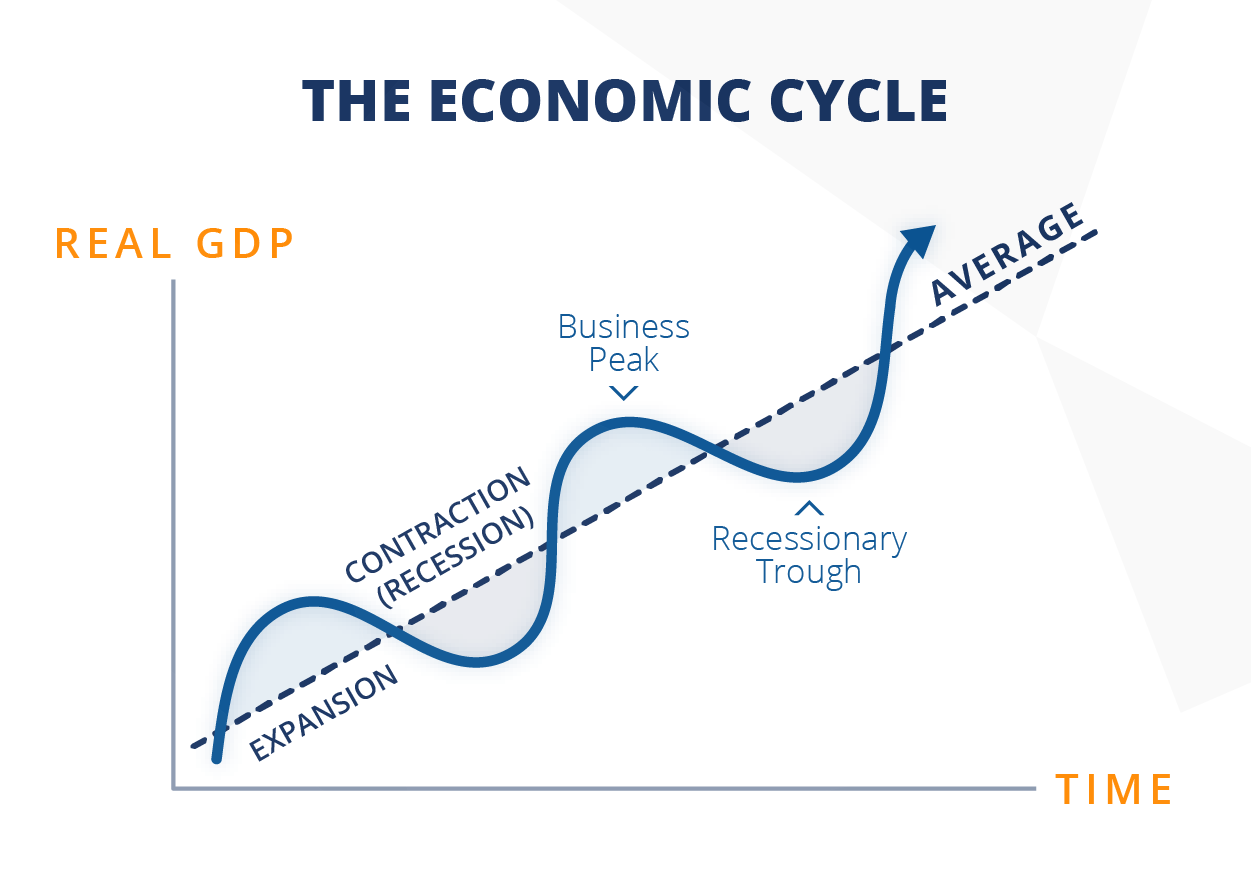

What does the Business Cycle Model shows?

Fluctuations in output over time

Economic growth

Increase in capacity to produce

What is economic growth caused by?

More resources

Improving the Quality of Resources

Technology (combination of resources)

What happens to Unemployment and Price during a recession?

unemployment increases and price decreases

What happens to Unemployment and Price during an expansion?

price increase and unemployment decreases

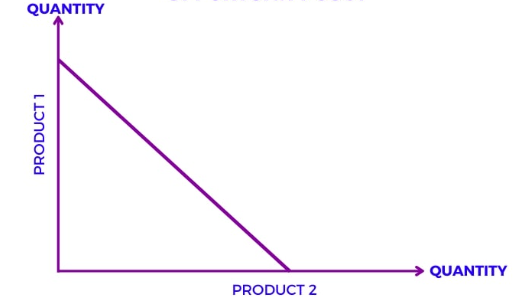

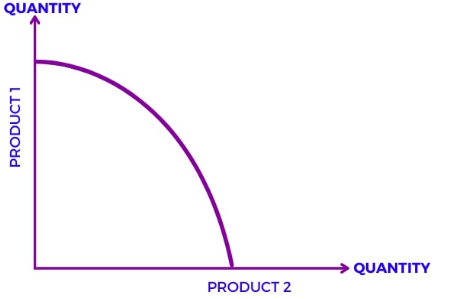

What is a Production Possibilities model

A model showing the opportunity cost and productive efficiency

Define Productive Effecient

full employment of resources

What graph is this

Constant Opportunity Cost Graph

What graph is this

Increasing Opportunity Cost

Where would an inefficient point be on an increasing opportunity cost graph?

Underneath the curve

Where would an infeasible point be on an PPC graph

Above the curve

Trade

Mutually beneficial Exchanges

Absolute Advantage

More output given the same inputC

Comparative Advantage

Lower opportunity cost given the same inputs (impossible to have a comparative advantage in both goods)

What is a seller’s opportunity cost?

The minimum price the seller will accept

What is the buyer's opportunity cost

the maximum price the buyer is paying

What is the benefit of trade?

allows consumption beyond individuals PPC curve

Acceptable terms of trade

Mutually benenficial

Unacceptable terms of trade

below seller’s minimum price OR above buyer’s maximum price

What are the assumptions of a perfect competition market model?

Large # of buyers and sellers

identical products

Quantity Demand

the amount people are willing and able to buy at a specific price

Demand

Relationship between all prices and their respective quantity demanded

Relationship between Market Size and Demand

proportional

Relationship between the expectation of future prices?

proportional

What is the relationship between the price of a complementary good and demand?

Inverse relationship

What is the relationship between the price of a substitute good and demand?

proportional

What is the relationship between income and demand for a normal good?

proportional

What is the relationship between income and demand for an inferior good?

inverse

What is the relationship between preferences for a good and the demand for the good

proportional

Quantity Supplied

The quantity that producers are willing and able to sell at a specific price

Supply

relationship between all prices and respective quantities supplies

Relationship between Quantity supplied and Demand

Proportional

What is the relationship between the number of producers and the supply curve?

proportional

What is the relationship between input costs and the supply?

inverse

What is the relationship between a per unit tax and supply?

inverse

What is the relationship between subsidies and supply?

proportionalwhat

What is the relationship between technology (productivity of each resource) and supply?

proportional

What is the relationship between expectations of future prices and supply?

proportional

Increase in demand causes…

Increase in both quantity and price

Decrease in demand causes…

Decrease in both quantity and price

Increase in supply causes…

increase in quantity but a decrease in demand

Decrease in supply causes…

decrease in quantity but an increase in price

What happens when supply increases and demand decreases

Price decreases

Quantity is indeterminate

What happens when supply decreases and demand increases?

Price increases

Quantity is indeterminate

What happens when supply and demand both increase

quantity increases

price is indeterminate

What happens when both supply and demand decrease?

Quantity decreases

price is indeterminate

What do price ceilings cause?

a shortage

What do price floors cause?

a surplus

What does a tariff do

Decreases the amount of imports necessary. More domestic producers.

What does a quota do?

increases price

What does a per unit tax do?

increases the price for buyers