B2 - Financial Management

1/76

Earn XP

Description and Tags

How a company funds itself (capital structure & WACC). How it keeps the lights on daily (working capital). How we value the business/assets (absolute/relative, fair value). How we decide on big investments (NPV, IRR, payback). How we weigh smaller decisions (marginal analysis). All of it boils down to one question: “Are we creating value above the cost of money?”

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

77 Terms

What is capital structure?

Mix of:

Debt (short & long term)

Equity (common & preferred)

Used to finance operations and growth

What is WACC (weighted average cost of capital)?

Used as “hurdle rate” in capital investment decisions

It is the weighted average after-tax cost of:

Debt

Preferred stock

Common equity

What is “Cost of retained earnings”?

The opportunity cost of not paying dividends to shareholders for higher retained earnings.

Opportunity cost: Don’t pay dividends = higher retained earnings but risks losing shareholders.

Example: If Luna Bikes reinvests $1M of profit into expansion instead of paying dividends, shareholders still “expect” a 10% return on that $1M — that 10% is the cost of retained earnings.

How can cost of retained earnings be calculated?

CAPM (Capital Asset Pricing Model)

DCF (Discounted Cash Flow)

BYRP (Bond Yield + Risk Premium)

What is CAPM (Capital Asset Pricing Model)?

A model that estimates the return investors expect based on how risky a stock is compared to the overall market.

CAPM tells us: the expected return = risk-free rate (if you got something with no risk like a T-Bill) + beta (volatility of stock) × extra reward for taking on market risk.

Ex:

Risk-free rate = 3%

Market return = 9%

Beta = 1.2

Using CAPM:

Expected return = 3% + 1.2 × (9% – 3%) = 10.2%

Meaning:

Investors expect about a 10.2% return to be compensated for the extra risk of this stock.

If a project or investment can’t earn at least 10.2%, it’s not worth the risk.

What is beta?

Volatility. Measures how much a stock’s price moves compared to the overall market.

Beta > 1 → Stock is more volatile (riskier)

Beta < 1 → Stock is steadier

Beta = 1 → Stock moves in line with the market.

What is DCF (Discounted Cash Flow)?

Estimates the return investors expect from dividends and growth.

Cost of Equity = (Dividend ÷ Price) + Growth

Example:

Price = $40, Dividend = $2, Growth = 5%

→ (2 ÷ 40) + 5% = 10%

Meaning: Investors expect ~10% total return (5% dividend + 5% growth).

What’s the difference between DCF and CAPM?

They’re two lenses on the same question: “What return do investors expect from us?”

Both might land near the same number, but:

CAPM = risk-based estimate

DCF = cash-flow-based estimate

CAPM looks outward, at the market:

“How risky is my stock compared to the whole market, and what return should investors demand for that risk?”

It’s about systematic risk — volatility and market behavior.DCF looks inward, at the company’s own dividends:

“Given what we pay out and how fast those payouts grow, what return do shareholders effectively get?”

It’s about cash flows and growth expectations.

Example:

If CAPM gives a 10.2% cost of equity (from market risk), and DCF gives 9.8% (from dividends), a company might average or compare them to sanity-check whether their cost of equity feels right.

What is BYRP (Bond Yield + Risk Premium)?

Estimates the cost of equity when market data (like beta) isn’t available.

Company’s bond yield (the rate the company pays to borrow money — this is like beta because it tells us how risky banks think the company is).

Add a few percent as a risk premium to reflect the extra risk equity investors take by buying the stock.

Example: if bond yield = 6% and risk premium = 4%, cost of equity = 10%. Used by private companies or analysts needing a quick, practical estimate.

What is the optimal capital structure?

Mix of debt/equity that produces the lowest WACC

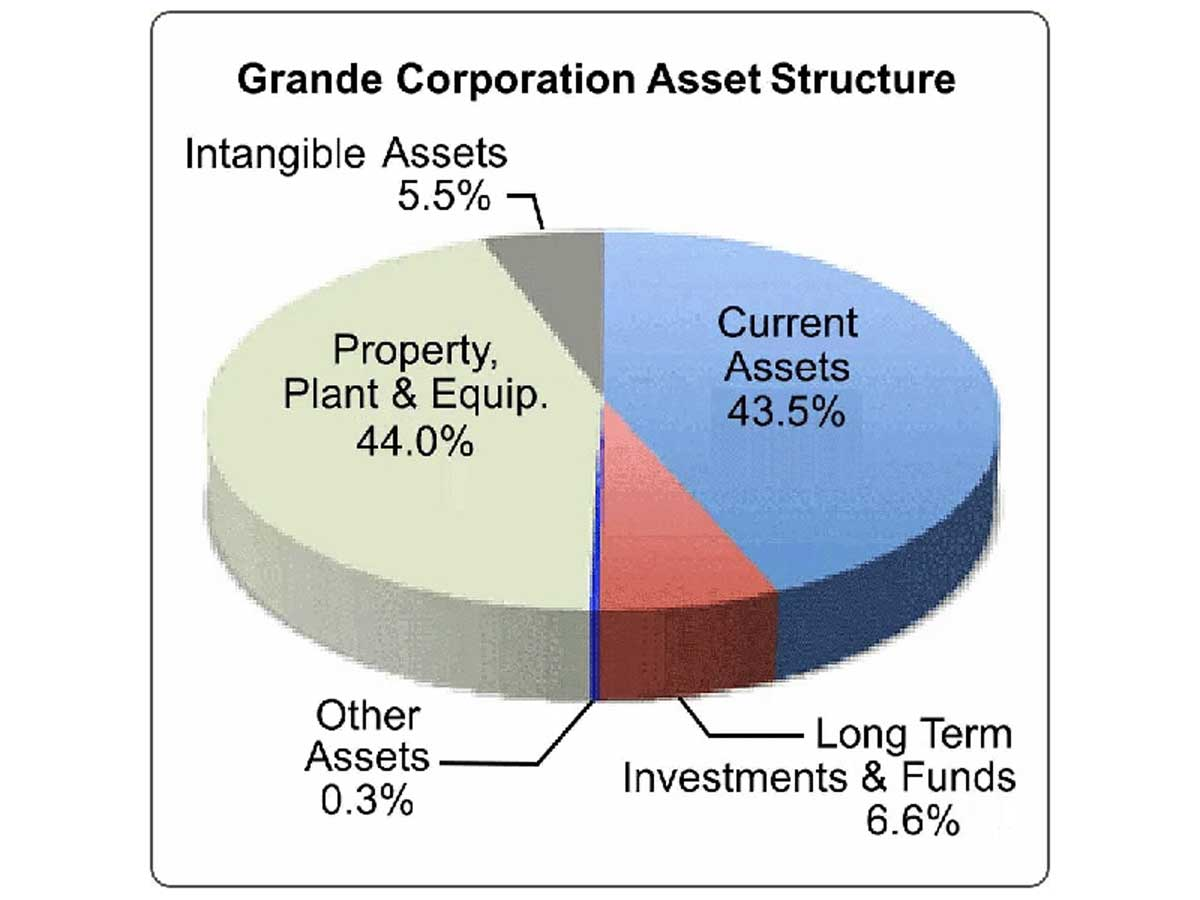

What is asset structure?

Composition of assets on balance sheet (not financing mix)

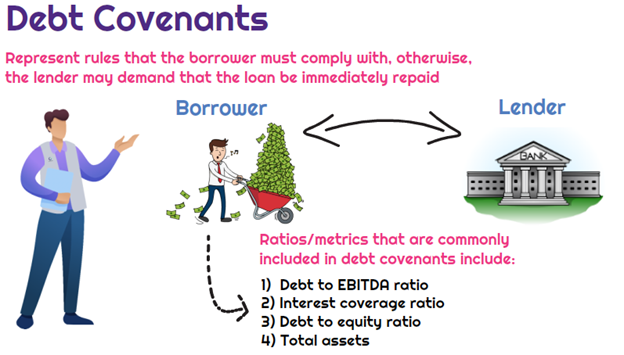

Why do lenders use debt covenants?

Protect lender’s position; limit borrower actions that may harm lenders

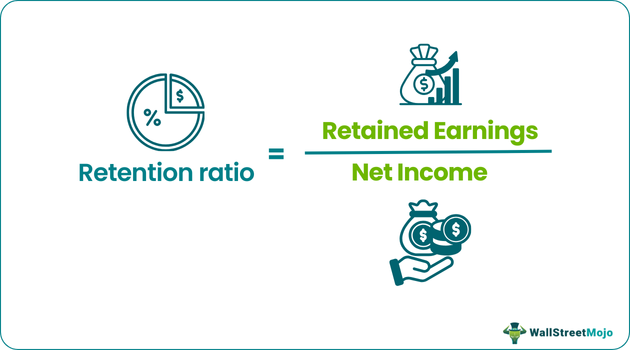

What is retention ratio?

The portion of net income a company keeps/retains instead of paying out as dividends.

If a company earns $100 and pays $40 in dividends, it keeps $60 — so the retention ratio is 60% (or 0.6).

How do you calculate growth rate (g)?

g = (Retention ratio × ROA) ÷ [1 – (Retention ratio × ROA)]

In plain English:

ROA tells you how efficiently the company turns assets into profit.

Retention ratio tells you how much of those profits are reinvested.

When you multiply them, you’re finding how much new profit the company can generate from reinvested earnings.

The fraction part adjusts that for compounding — it shows how growth feeds on itself over time.

So the idea is simple:

The more profit you keep and the better you use it, the faster you grow.

Example:

Retention = 60%, ROA = 10%

→ g = (0.6 × 0.10) ÷ [1 – (0.6 × 0.10)] = 0.06 ÷ 0.94 ≈ 6.4% growth

Meaning the company can grow earnings and dividends roughly 6.4% per year if it keeps reinvesting at that rate.

What are key profitability ratios?

ROI (Return on Investment); ROA (Return on Assets); ROE (Return on Equity); all use net income in numerator

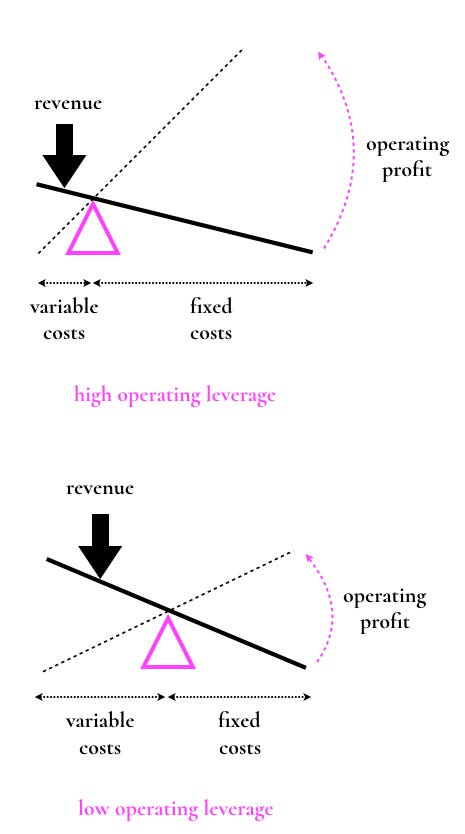

What is operating leverage?

more fixed cost & less variable cost = more chance for profit when sell more.

less fixed cost & high variable cost = lower profit even when sell more

What is financial leverage?

get more loans vs equity = more money fast but riskier.

PRO of this = don’t have to share as much profits with stockholders = more money and financial leverage for you.

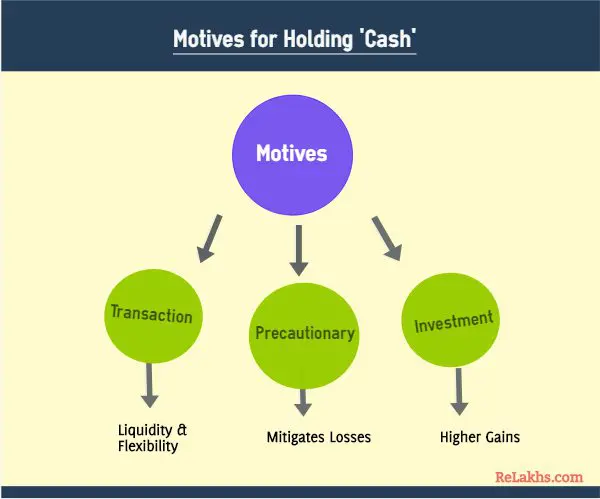

What are the motives for holding cash?

Transaction; speculation; precaution

What are common cash management tools?

Synchronize inflows/outflows; float; overdraft protection; compensating balances

What is accounts receivable management?

Balance credit and collection policies; optimize collection period and days sales outstanding; factoring receivables = faster cash but costly

How is inventory valued?

Lower of cost or market (LCM) or net realizable value (NRV)

What are inventory systems?

Periodic: based on physical counts; perpetual: continuously updated

What are common inventory cost flow methods?

Specific identification; FIFO; LIFO; weighted average; moving average

What is safety stock?

Extra inventory held to reduce risk of stockouts

What is reorder point?

Inventory level at which a new order should be placed

What is EOQ (economic order quantity)?

Optimal order size minimizing total carrying plus ordering costs

What are contemporary inventory management techniques?

MRP (Materials Requirements Planning); JIT (Just-in-Time); Kanban (visual scheduling system)

What is supply chain management (SCM)?

Integration of business processes from customer back to original supplier

What is trade credit?

Short-term financing from vendors (payment 30–45 days later); usually largest source for small firms

What are methods to delay disbursements?

Request deferment from vendor; use bank line of credit

What is a letter of credit?

Bank guarantee of financial obligation

What is a line of credit?

Revolving loan with a bank; renewable at maturity

What are pros and cons of short-term financing?

Pros: lower rates, more liquidity, higher profitability; cons: higher interest rate risk, lower capital availability

What are pros and cons of long-term financing?

Pros: stable capital, less interest rate risk; cons: higher costs, lower liquidity, reduced profitability

What are absolute valuation models?

Intrinsic value = PV of future cash flows

What is an annuity?

Equal cash flows over time

What is a perpetuity?

An annuity that lasts forever

What is the Dividend Discount Model (DDM)?

Intrinsic stock value = PV of expected future dividends

What are relative valuation models?

Compare stock to similar companies using price multiples

What are common price multiples?

P/E ratio (earnings focus); PEG ratio (P/E adjusted for growth); price-to-sales (less manipulable); price-to-cash-flow (cash focus); price-to-book (balance sheet focus)

What is an option?

Contract giving right to buy (call) or sell (put) asset at a set price in set time

What is the Black-Scholes model?

Complex option pricing model; values security at one point in time

What is the binomial model?

Option pricing model considering security over multiple periods

How is a bond valued?

PV of future cash flows discounted for risk

How can tangible assets be valued?

Cost method; market value method; appraisal method; liquidation value

How can intangible assets be valued?

Market approach; income approach; cost approach

What are fair value measurement approaches?

Market, cost, income, or combination

What is the fair value hierarchy?

Level 1: quoted prices; Level 2: observable inputs; Level 3: unobservable inputs

What are stages of capital budgeting cash flows?

Inception (time 0); ongoing periodic inflows/outflows; terminal/disposal value

What are direct vs. indirect cash flow effects?

Direct: immediate inflows/outflows; indirect: related, e.g. tax shield from depreciation

How do you compute after-tax cash flows for a project?

Estimate inflows; subtract noncash deductible expenses; compute tax; subtract tax = after-tax CF

What are DCF (discounted cash flow) methods?

PV of all expected future cash flows using discount rate (e.g., WACC)

What is Net Present Value (NPV)?

PV of inflows – initial investment; positive = accept, negative = reject

What are strengths & limits of NPV?

Strengths: flexible, handles varying returns; limits: doesn’t show rate of return

What is capital rationing?

Allocating limited funds to maximize total NPV

What is the profitability index (PI)?

PI = PV of inflows ÷ initial investment; PI < 1.0 is undesirable

How is NPV used in lease vs. buy?

Compare cash flows of leasing vs. purchasing asset

What is Internal Rate of Return (IRR)?

Discount rate that makes NPV = 0; accept if IRR > hurdle rate

What are IRR limitations?

Unrealistic reinvestment assumption; inflexible with alternating cash flows; only relative measure

What is the payback period method?

Time to recover initial investment (ignores time value of money); pros: simple, liquidity focus; cons: ignores time value, later profitability

What is the discounted payback method?

Uses discounted cash flows; still ignores total profitability

What is EVA (economic value added)?

Excess income after taxes over cost of capital (WACC)

What is expected value in decision-making?

Weighted average of outcomes based on probabilities

What is marginal analysis?

Compares relevant revenues and costs of alternatives; relevant: incremental and opportunity costs; irrelevant: sunk costs

When should a special order be accepted?

If excess capacity: accept if price > variable cost per unit; if full capacity: include opportunity cost of lost sales

What is make vs. buy decision?

Compare insourcing vs. outsourcing; consider only relevant costs; choose lowest cost

What is a sell or process further decision?

Compare incremental revenue vs. incremental cost past split-off; process if revenue > cost, else sell

What is keep or drop a segment decision?

Keep if lost contribution margin > avoided fixed costs; drop if avoided fixed costs > lost contribution margin

What is the most advantageous market (fair value)?

The market that gives the best price for the entity after considering transaction costs: [B2 | PDF]

For an asset → maximizes the selling price

For a liability → minimizes the amount paid to transfer it

How is the “most advantageous market” different from just “best quoted price”?

It’s the best market after considering transaction costs, not just the highest/lowest raw price.

What does Becker mean by “valuation using accounting estimates”?

Some financial statement amounts are measured using estimates/judgment, not direct market prices (because the exact amount isn’t known).

Why do accounting estimates matter in valuation?

Because the reported value depends on assumptions (management judgment), so the number can change if assumptions change. [B2 | PDF]

Give examples of financial statement line items commonly valued using accounting estimates.

Examples include items like allowances, impairments, and other estimated balances (anything requiring judgment to measure).

What determines the covenants/interest terms in short-term institutional borrowing?

The borrower’s creditworthiness (stronger credit = better terms)

What’s a key difference between a line of credit and institutional short-term credit arrangements?

Institutional arrangements usually come with more covenants and detailed rate provisions, and disclosure is emphasized.

How does Becker describe discounting bond cash flows?

When might multiple discount rates be used for a bond’s cash flows?

When different cash flows have different risk levels, you can use different rates to reflect that risk.