CFI - Corporate Finance Fundamentals | Quizlet

1/72

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

73 Terms

Corporate Finance objective:

...A...of a business while...B...

A) Maximizing the value

B) balancing risk and profitability

Capital Investment:

Deciding what...A...while the...B...

A) projects/businesses to invest in

B) highest possible risk-adjusted return

Capital financing:

Determining how to...A...while optimizing the firm's...B...

A) fund capital investments

B) capital structure

Dividends & Return of Capital:

Deciding how and when to...

return capital to investors

Corporate finance is mainly about: (3)

1.Capital Investments

2.Capital financing

3.Dividends & Return of Capital

Players in corporate finance – primary market (4)

1. Corporations ( need capital )

2. Institutions ( investors )

3. Investment Banks (broker)

4. Public accounting firms (over all financial info)

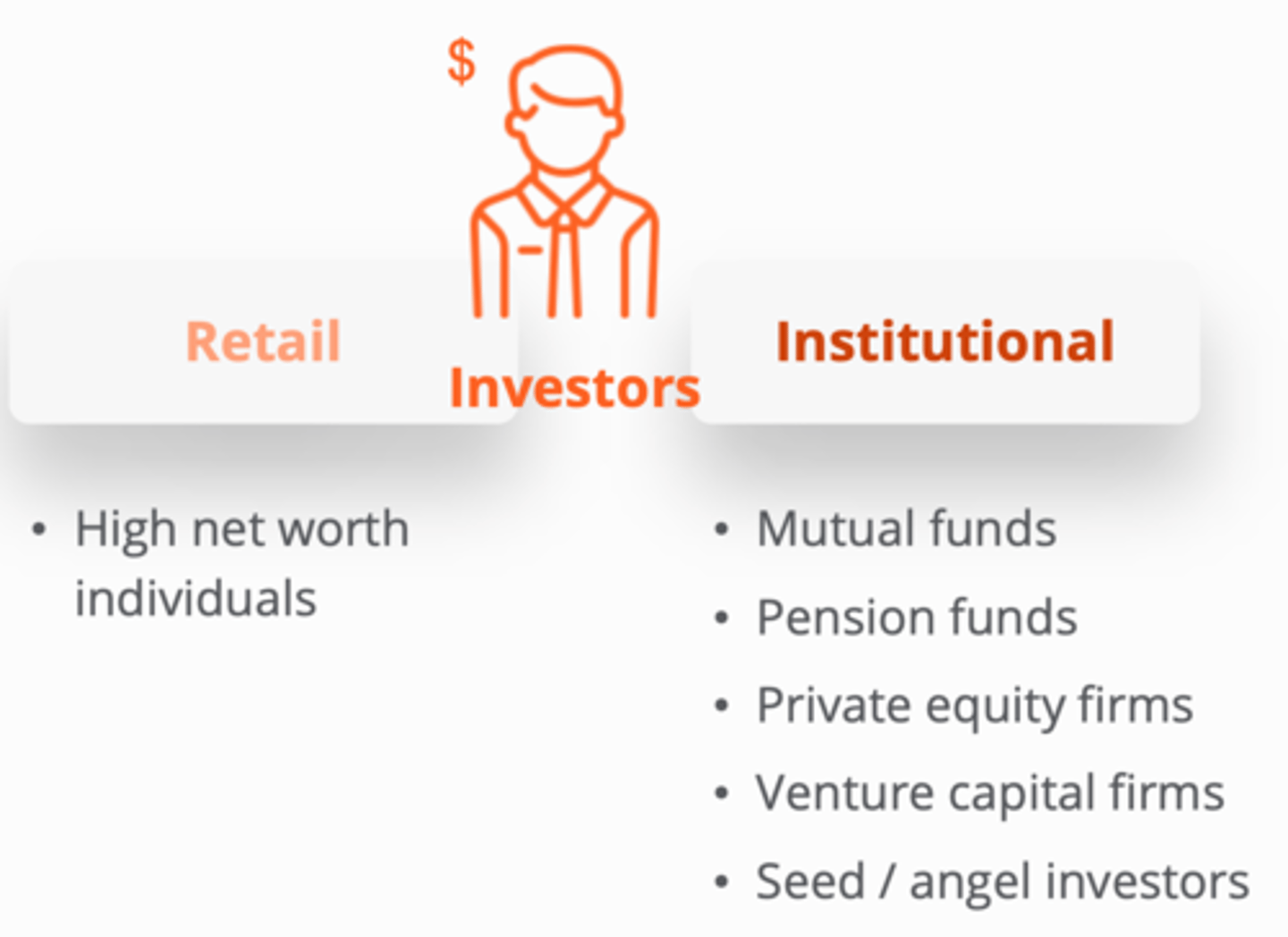

Investors

1. Retail:(1)

2. Institutional:(5)

1. a) HNWI

2.

a) mutual funds

b) pension funds

c) private equity firms

d) VC firms

e) seed / angel investors

Corporations:

1. ...

2. ... - ...

1. public

2. private - traded and owned by a few investors

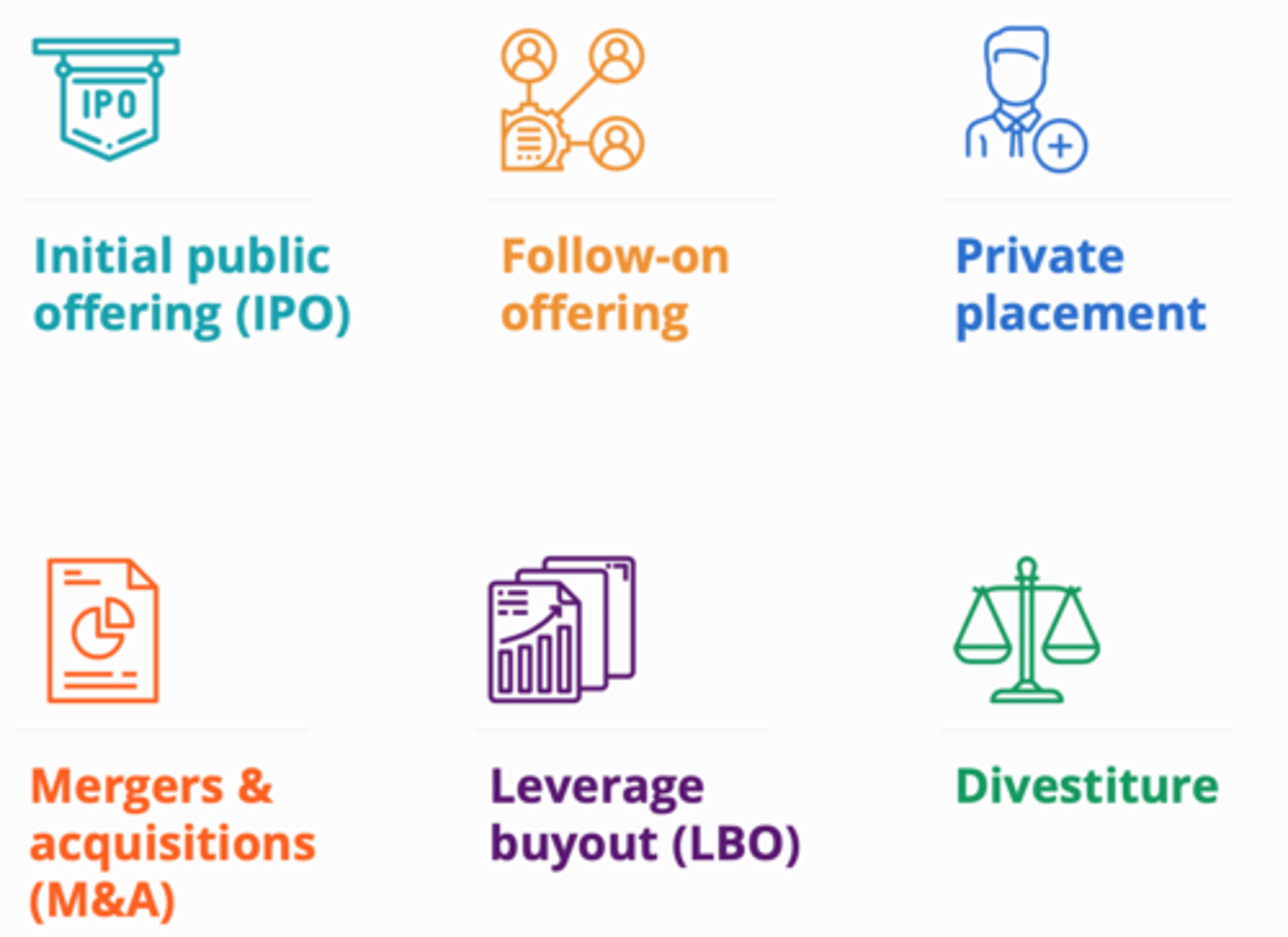

Types of transactions: (6)

1. IPO

2. Follow-on offering

3. Private placement

4. M&A

5. LBO

6. Divestiture

IPO (initial public offering):

The first time a company...

sells shares of its stock to the public.

Follow-on offering:

Issuance of stock shares following a company's...

Initial public offering (IPO)

private placement:

...A...in which shares are sold directly to a...B...

A) primary offerings

B) small group of institutional or wealthy investors

Mergers and acquisitions:

A merger is the combination of two firms, which subsequently form a new legal entity under the banner of one corporate name. An acquisitions when, one company purchases another outright

Leveraged Buyout (LBO):

...A...is completed almost entirely with...B...

A) the acquisition of another company

B) borrowed funds

Divestiture:

Disposing all or some of its...A... by...B...,...C...,...D...them down, or through...E...

A) assets

B) selling, exchanging, closing them down, or through bankruptcy.

What is a capital investment ?

Any investment for which...A.. is ...B...

A) the economic benefit

B) greater than one year

capital investment examples

1.

2.

3.

4. ...A... and ...B... of ...C...

Opening a new factory

Entering a new market

Acquiring another business

4. A) Research B) development C) new products

Before any capital investment the company assesses

Investment payoff

Techniques for valuing an investment

1.Net Present Value (NPV)

2.Internal Rate of Return (IRR)

terminal value (Vt)

company's value into perpetuity beyond a set forecast period

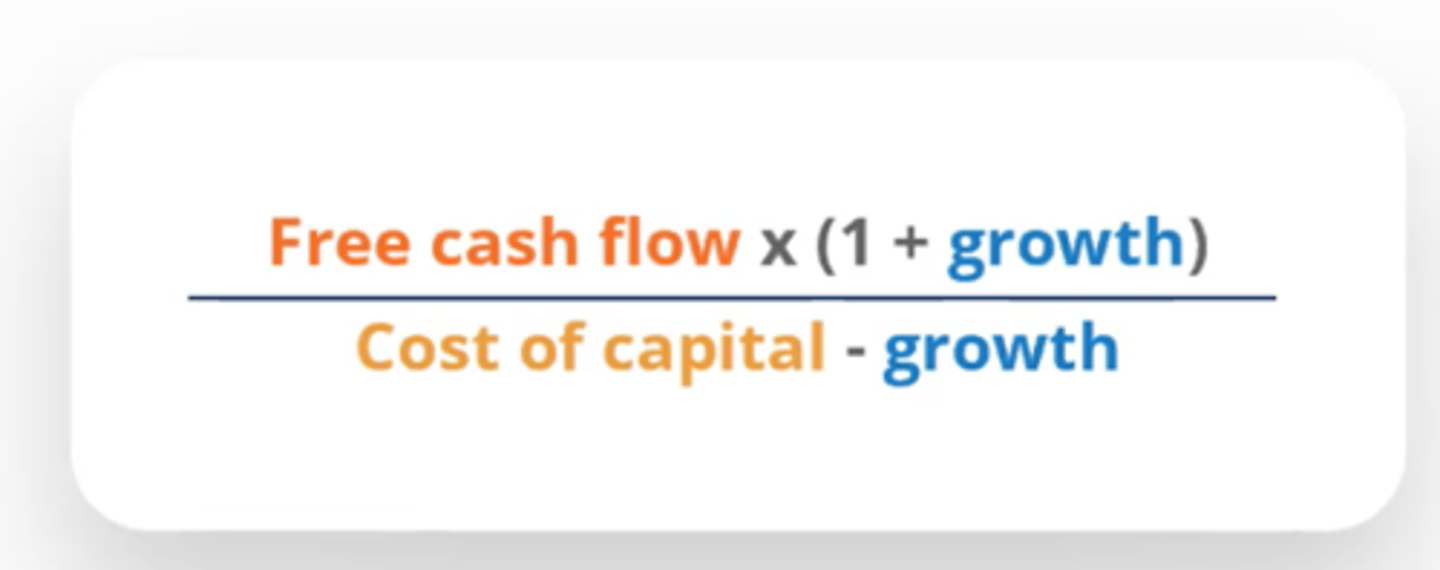

Terminale value calculation methods

1.Growing perpetuity formula

2.Exit multiple formula

Growing Perpetuity Formula

Free cash flow*( 1+growth ) / ( Cost of capital - growth )

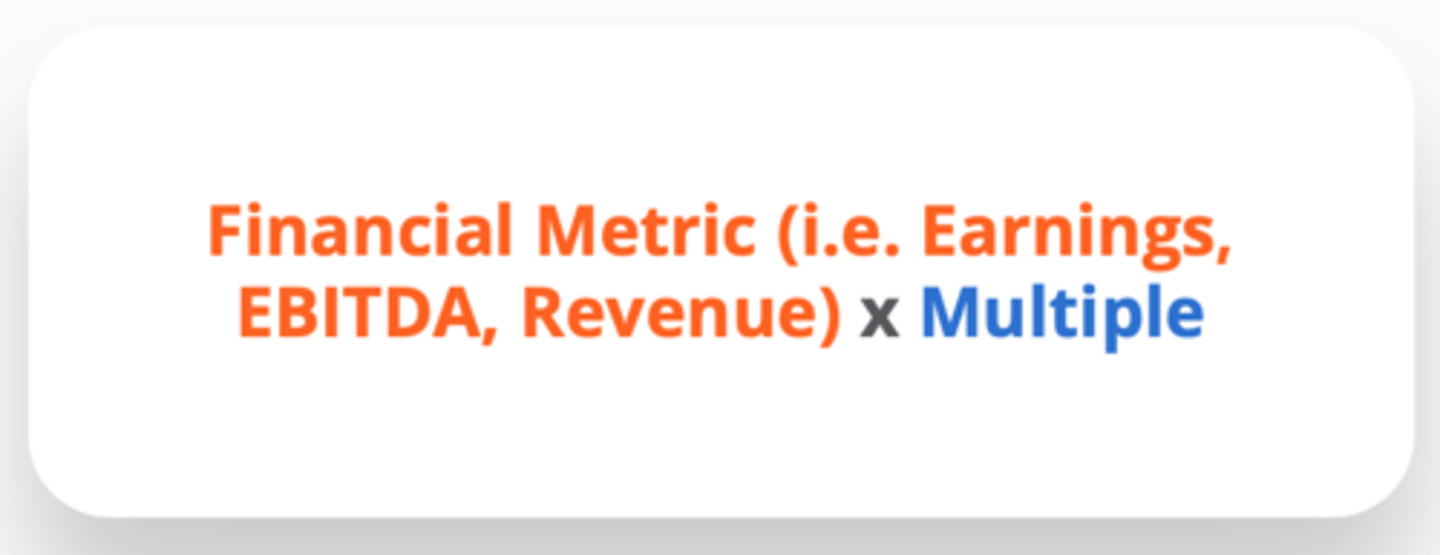

Exit Multiple Formula

assume that the business is sold at the end of the forecast period

Free Cash Flow refers to

Business strategy

Revenue

Cost structure

Asset utilization

Growth refers to

Organic growth

What's sustainable

Cost of capital refers to

Risk

Current capital structure

Macrofactors

Organic growth

growth achieved through the expansion of current business activities

Enterprise Value (EV)

the value of the entire business

Equity Value/Market Capitalization

the value shareholders would receive if the company is sold

Equity Value Formula

=Share Price x Outstanding Shares

=NPV of the business - Debt + Cash

Enterprise Value Formula

=Equity Value + Debt - Cash

=NPV of the business

Internal Rate of Return (IRR)

the annual rate of growth that an investment is expected to generate

the higher the IRR

the more valuable is the project is

IRR goal is to

identify the rate of discount, which makes the present value of the sum of annual nominal cash inflows equal to the initial net cash outlay for the investment.

Mergers and acquisitions

the process of companies buying, selling, or combining businesses.

Mergers and acquisitions benefits

• Cost savings

• Revenue enhancements

• Increase market share

• Enhance financial resources

Mergers and acquisitions potential drawbacks

• Overpaying

• Large expenses associated with the investment

• Negative reaction to the merger or acquisition

10 steps acquisition process

M&A process step 1

Acquisition Strategy tying with company overall strategic plan

M&A process step 2

Defining acquisition criteria (size, location, type of business)

M&A process step 5

Business Evaluation & Detailed Evaluation based on public information

M&A process step 10

Integration of the business when the transaction is closed

Two types of buyers in M&A

1.Strategic Buyers

2.Financial Buyers

Strategic Buyers are

Operating businesses looking for expansion (vertical or horizontal) and achieve operating synergies ( cost savings or revenue enhancement)

Financial Buyers are

Private equity or Professional investor looking for maximizing their ROE

rival bidder

another party offering to buy the asset from the seller at a specific price

Companies pay more than rival bidders because

Acquisition valuation process

1. Value the target as stand-alone (Enterprise value)

2. Value synergies (Hard (cost savings) and soft (revenue enhancements))

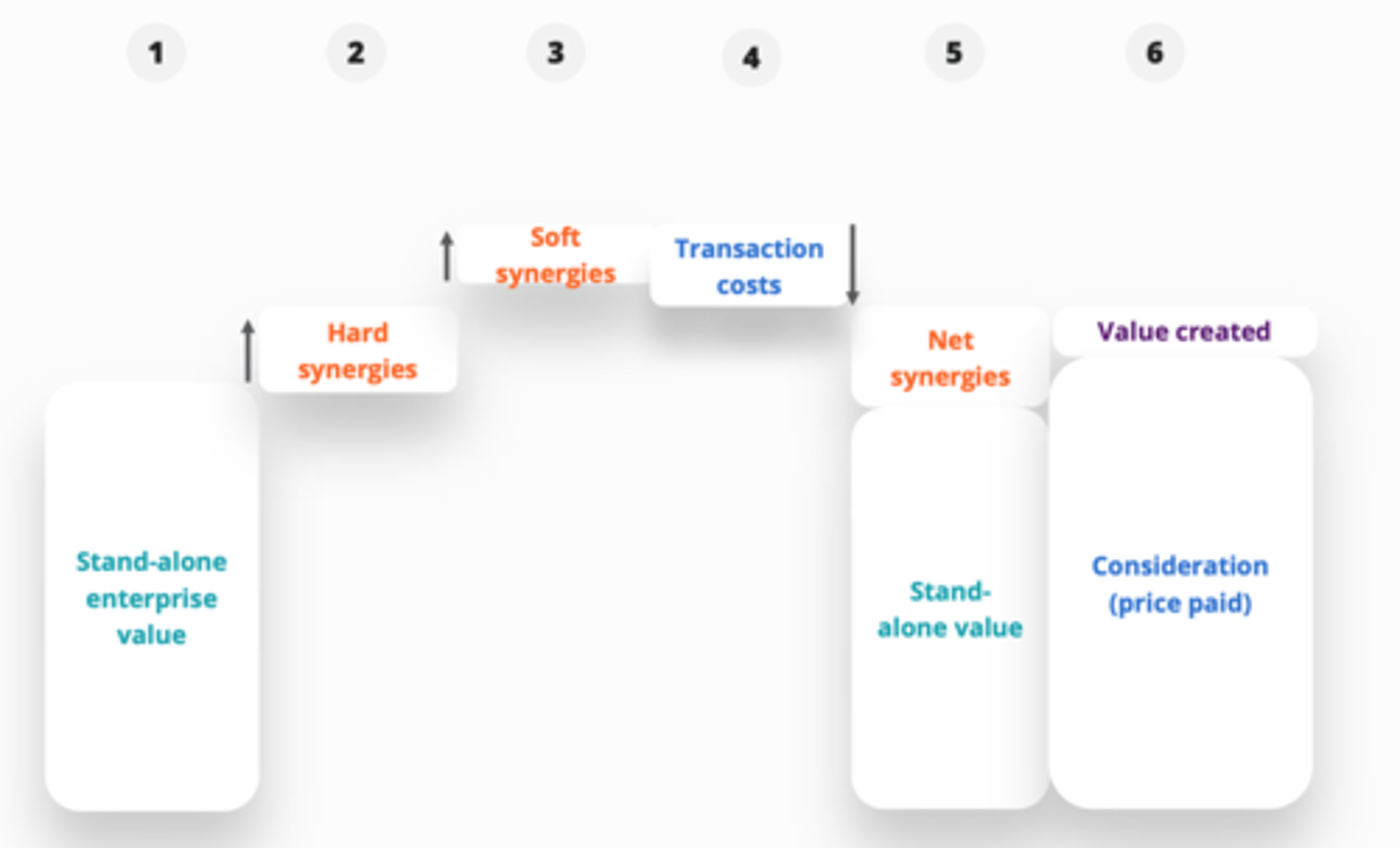

Best practice acquisition analysis

1. stand-alone...

2. hard...

3. soft...

4. transaction...

5. net...A... and...B...

6. ...A...created and...B...

1. enterprise value

2. synergies

3. synergies

4. costs

5. A) synergies B) stand-alone value

6. A) value B) consideration (price paid)

Value the target as stand-alone (Enterprise value)

• Sales growth

• EBIT margin

• Operating tax

• Working capital requirements

• Capital expenditures

Value synergies (Hard (cost savings) and soft (revenue enhancements))

• Sales : volume & price

• EBIT margin : Product mix & Overhead reductions

• Operating tax :Tax efficiency & Tax losses

• Working capital : Vendor relationships

• Capital expenditures : Efficiencies

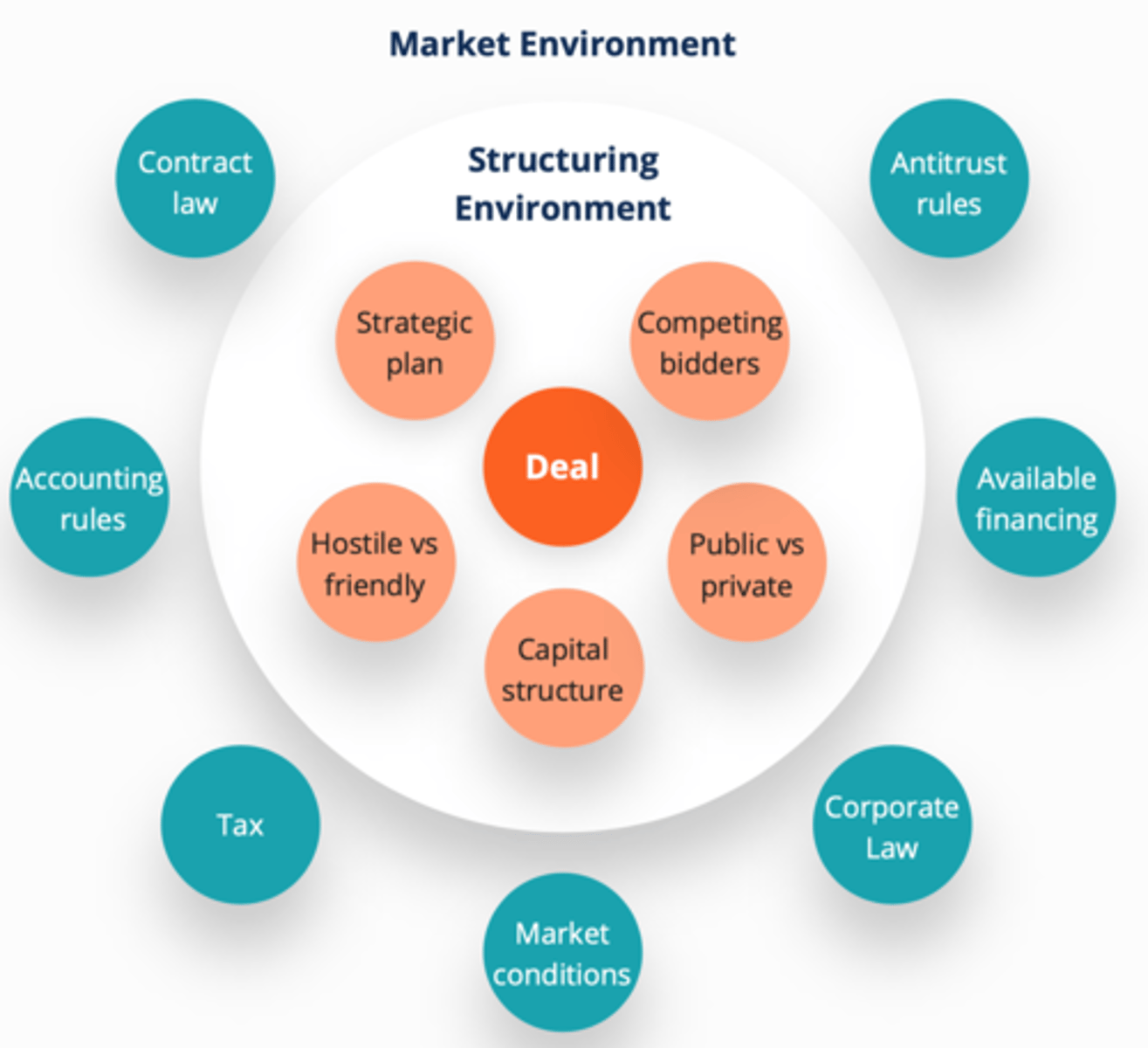

Issues to consider when structuring a deal

Structuring Environment

Market Environment

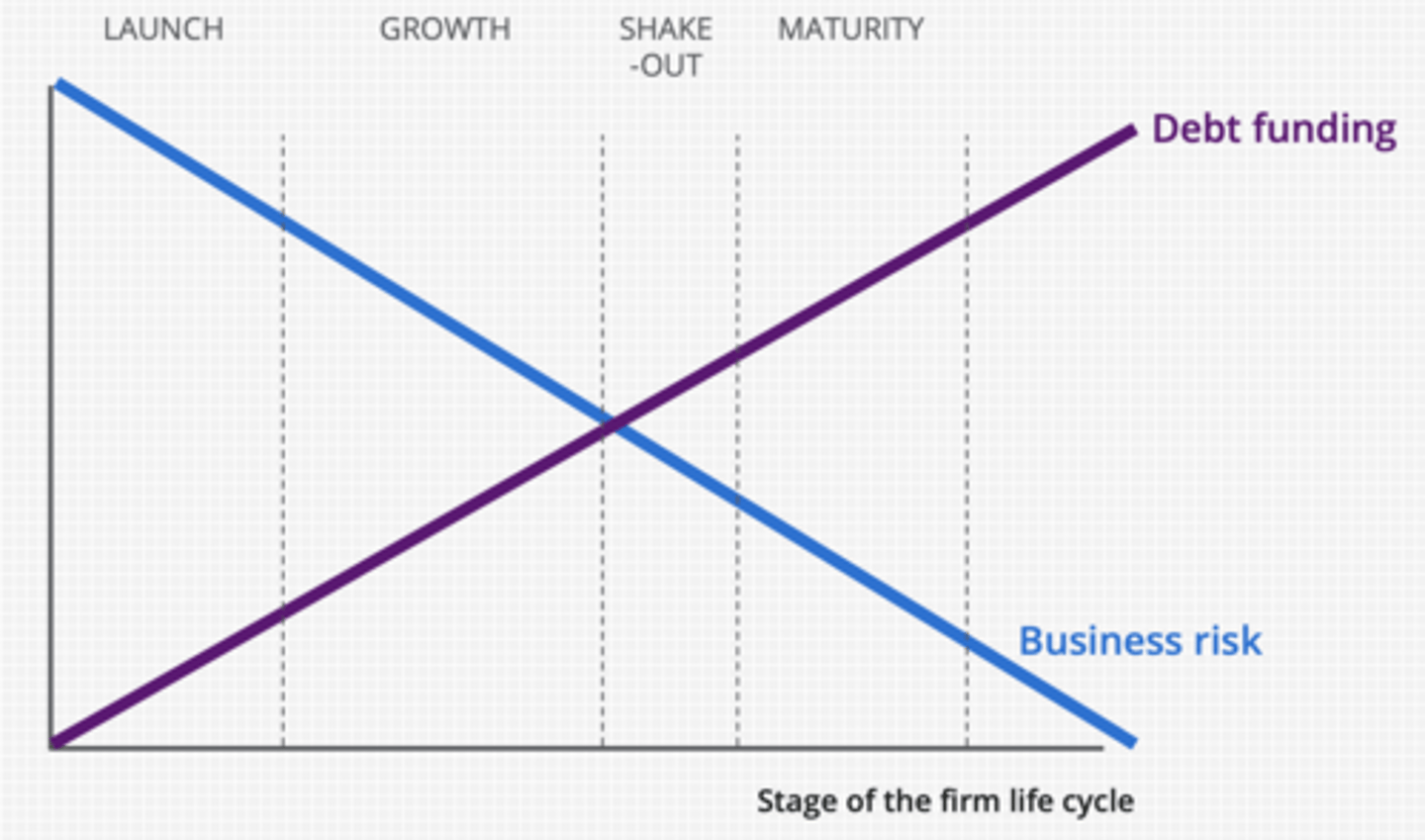

The corporate funding life-cycle - with time:

1. ...decreases

2. ...increases

1. business risk

2. debt financing

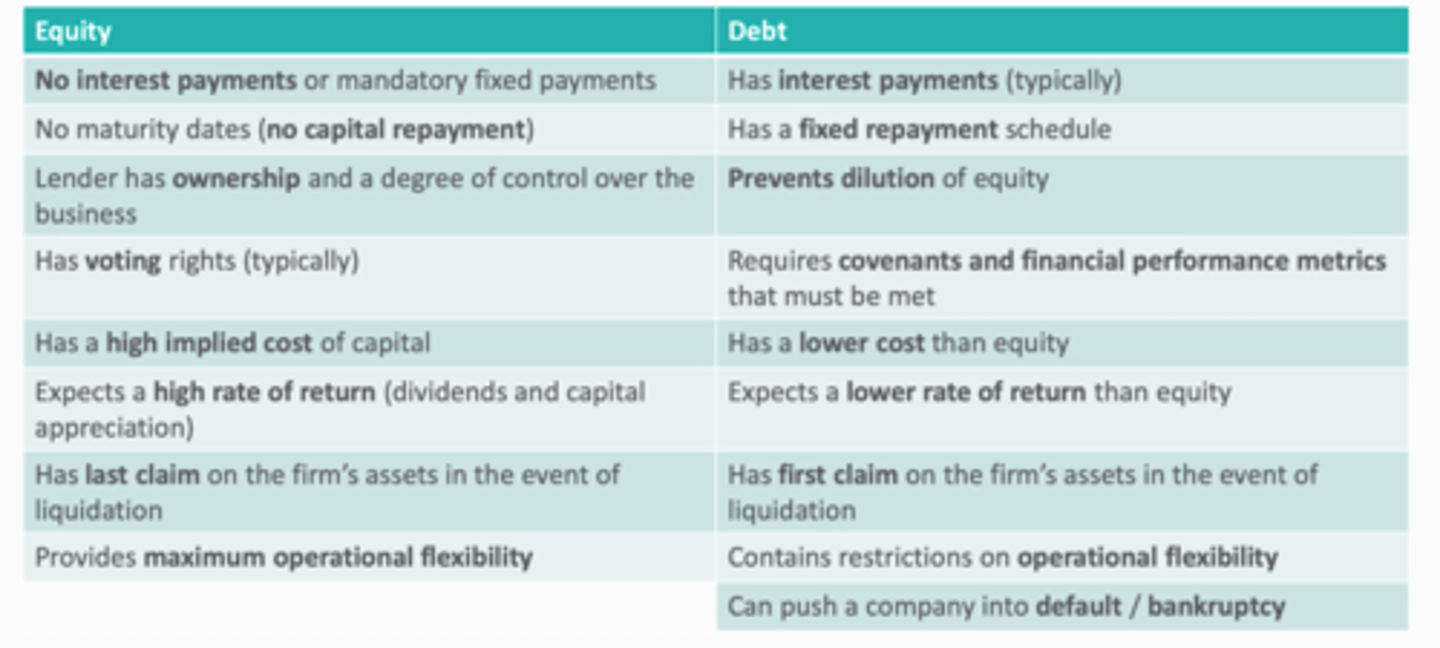

capital structure refers to:

the amount of debt and/or equity employed by a firm to fund its operations and finance its assets.

Optimal capital structure relies on a large number of factors

The current economic climate

The business' existing capital structure

The business' life cycle stage

capital structure is important because

1.Having too much debt may increase the risk of default in repayment.

2.Depending too heavily on equity may dilute earnings and value for original investors.

Weighted Average Cost of Capital (WACC) is

the proportion of debt and equity a firm has, multiplied by their respective costs.

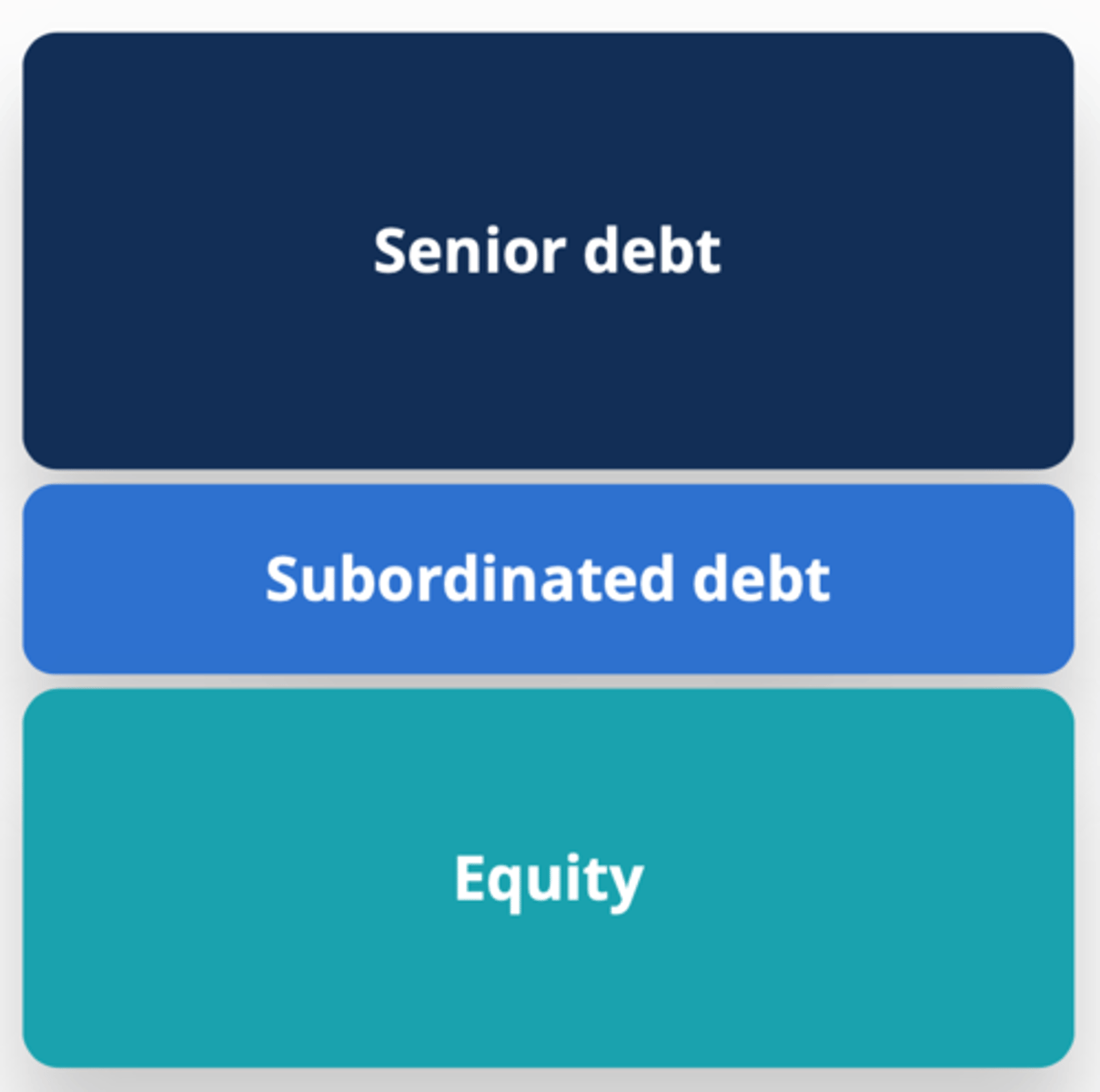

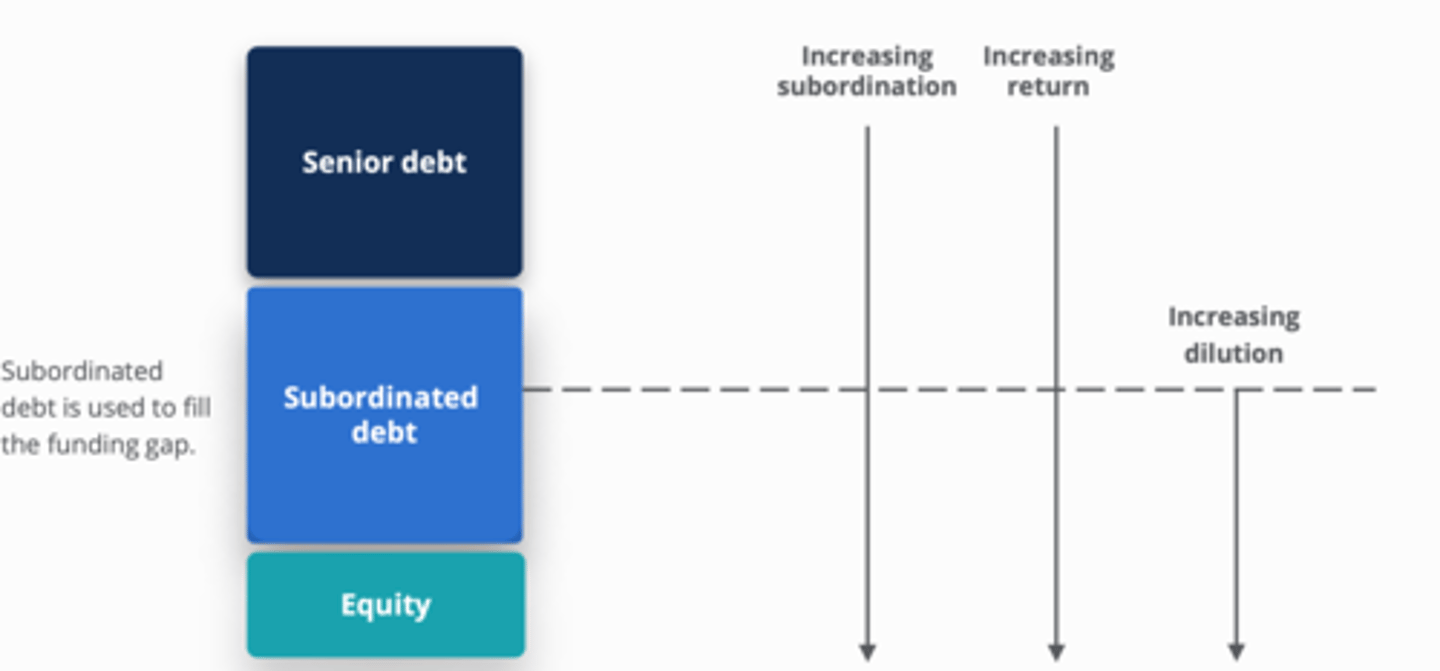

Capital Stack (Structure)

1. Senior debt

2. Subordinated debt

3. Equity

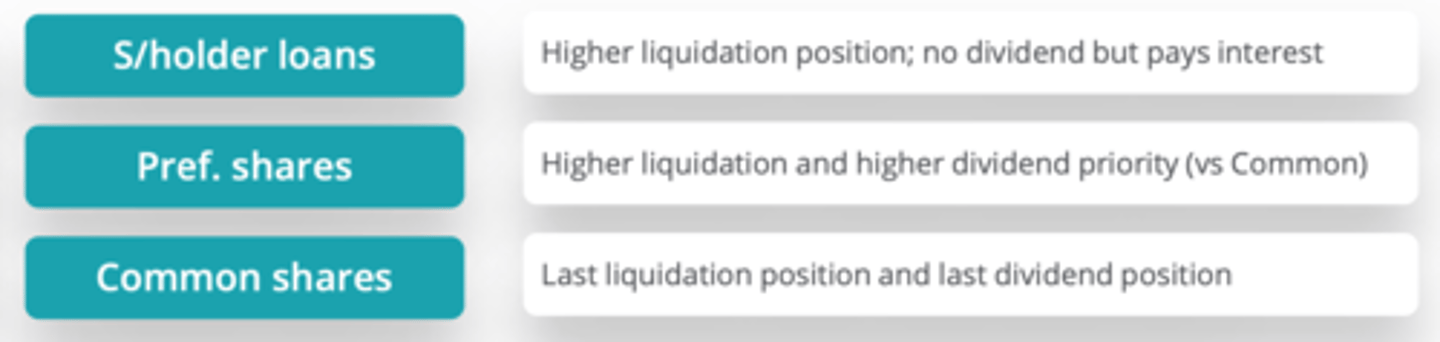

Types of Equity

1. ... - higher...A...;...B... but...C...

2. ...shares - higher...A...and higher...B...

3. ...shares - last...A... and last...B...

1. S/holder loans - A) liquidation position B) no dividend C) pays interest

2. pref. shares - A) liquidation B) dividend priority (vs common)

3. common shares - A) liquidation position B) dividend position

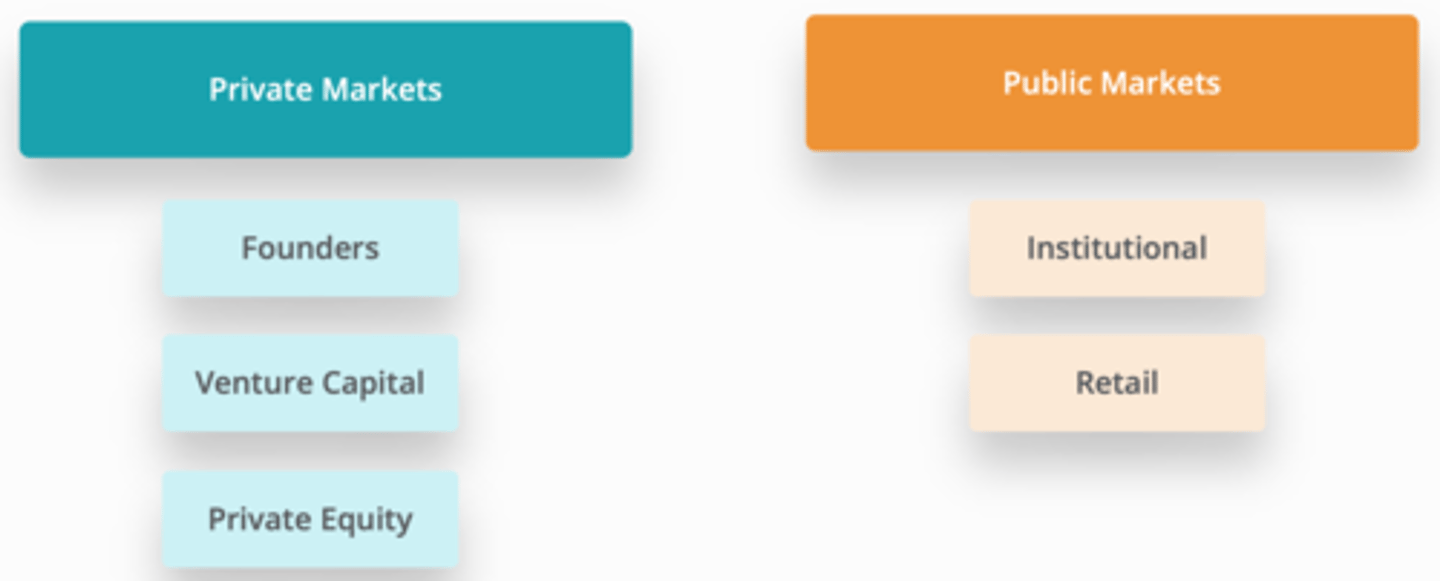

Sources of equity

1. private markets: (3)

2. public marets: (2)

1.

a) founders

b) venture capital

c) private equity

2.

a) institutional

b) retail

Private equity firms manage...A...that invest in companies that represent an opportunity for a...B...for...C...

funds or pools of capital that invest in companies that represent an opportunity for a high rate of return for limited time periods

Why use debt financing?

Corporation: (1) to lower the cost of capital, and (2) avoid equity dilution

Investor : to increase their equity return

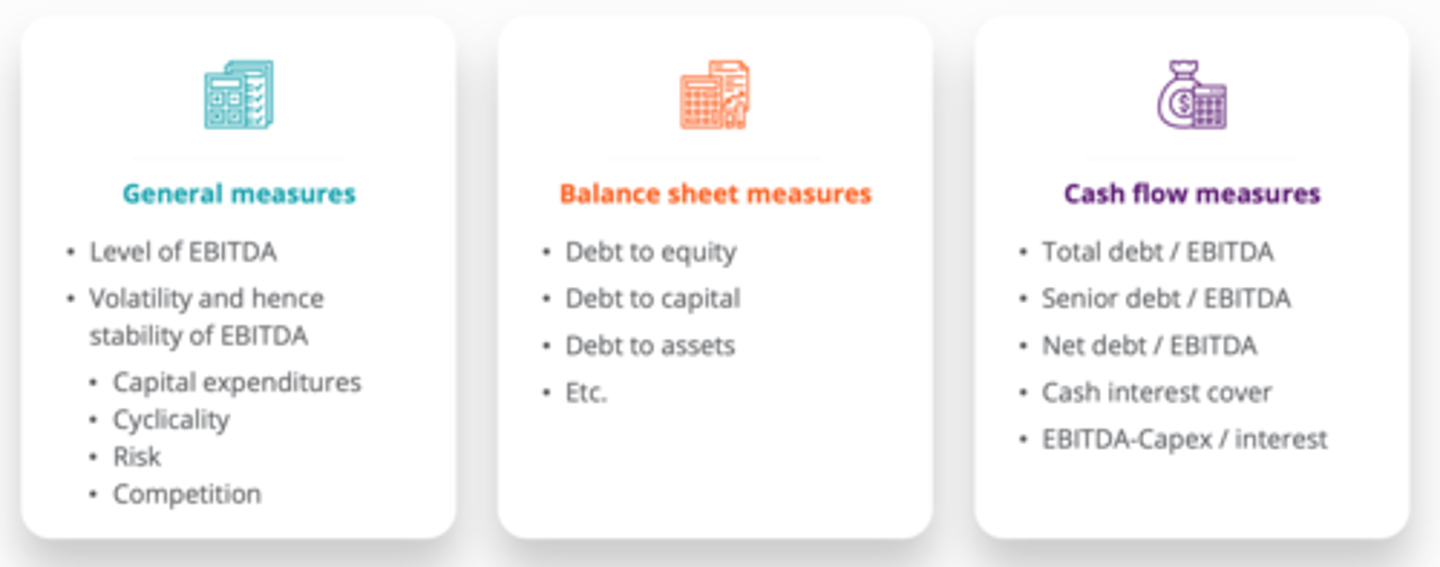

Assessing debt capacity: (3)

1. General measures

2. Balance sheet measures

3. Cash flow measures

Capital stack order of increasing subordination & return + partially dilution)

1. senior debt

2. subordinated debt

3. equity

Mezzanine debt characteristics

Non-traded

Subordinated to senior debt

Repaid as a bullet (not amortized)

Combination of cash and accrued interest built into return

Can have equity warrants attached

Debt with warrants, convertible loan stock,

convertible preferred shares

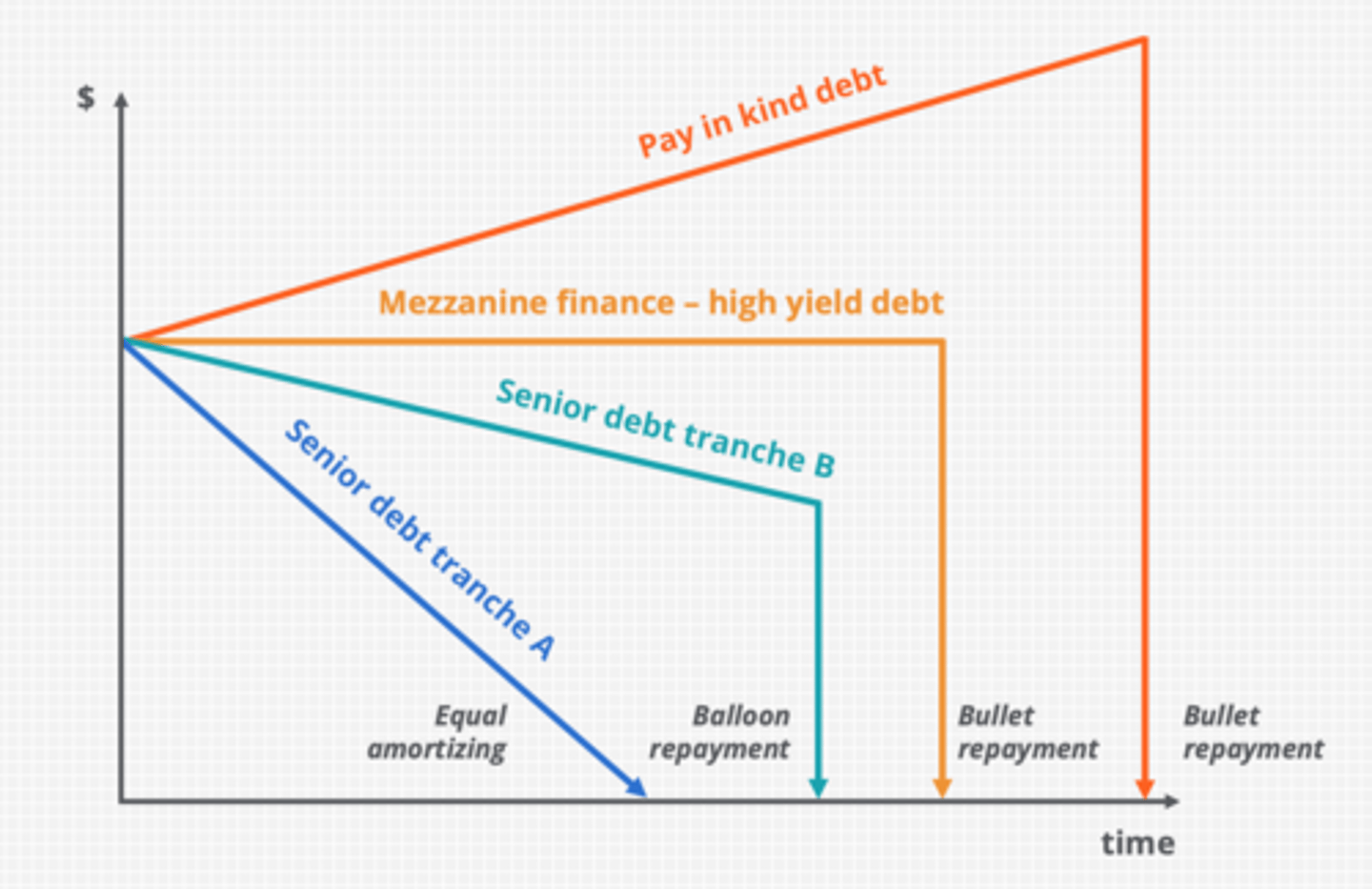

Debt repayment profiles

1. senior debt tranche A

2. senior debt tranche B

3. mezzanine finance - high yield debt

4. pay in kind debt

1. equal amortizing

2. balloon repayment

3. bullet repayment

4. bullet repayment

Tradeoffs between debt and equity (8)

Underwriting - the process where a bank...A...for a...B..., or...C...from investors in the form of...D... or...E...

A) raises capital

B) corporation

C) institution

D) equity

E) debt securities.

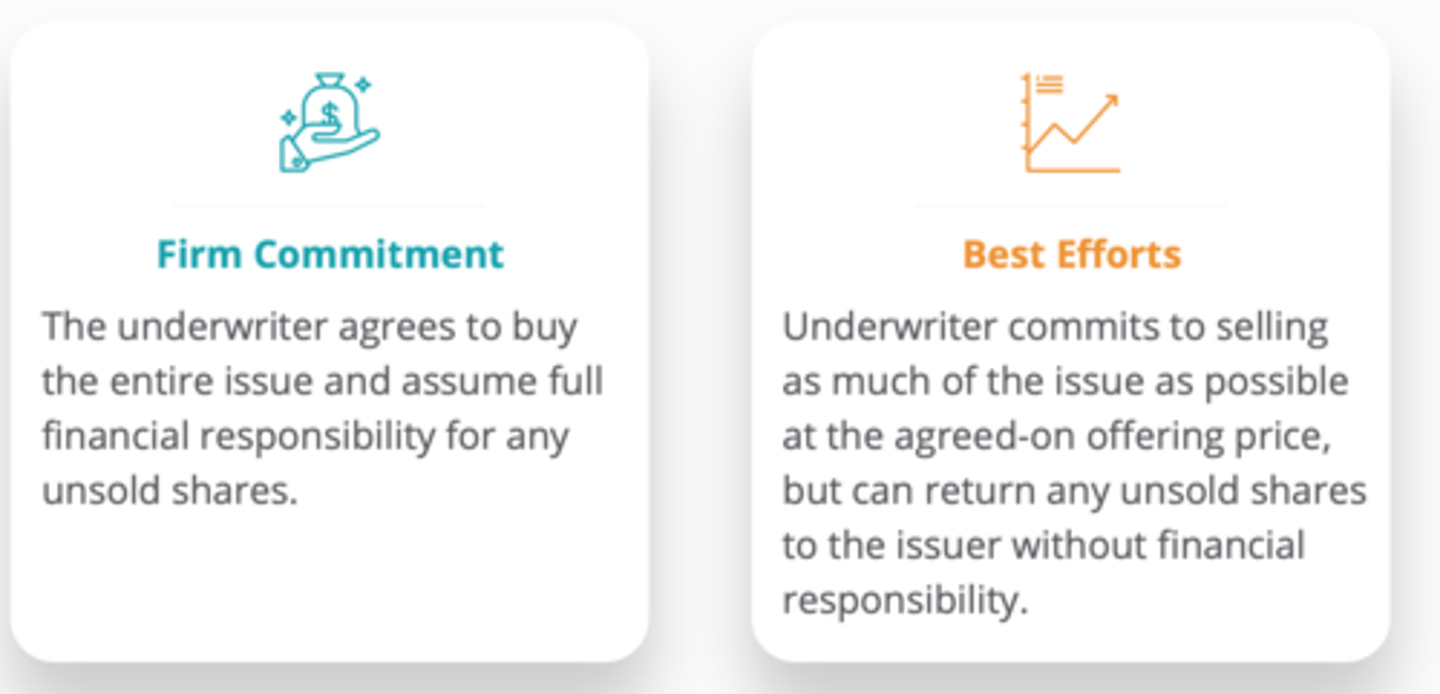

Types of Underwriting Commitments

1) ... - the underwriter agrees to buy the...A...and assume full...B...for any...C...

2) ... - underwriter commits to...A...at the agreed-on offering price, but can...B...to the...C...without...D...

1) firm commitment - A) entire issue B) financial responsibility C) unsold shares

2) best efforts

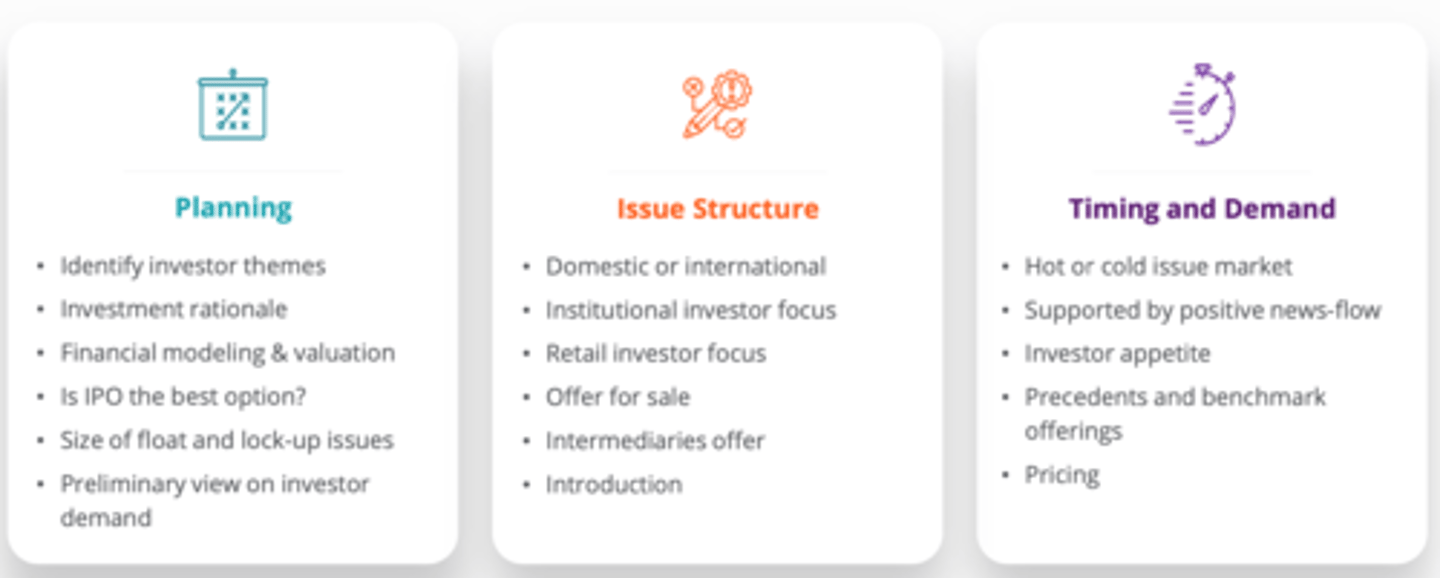

Underwriting advisory services: (3)

1. planning

2. issue structure

3. timing and demand

Underwriting - the book building process

1. ...range

2. ...A...investor commitment at...B...

3. ...built

4. ...A...is set to ensure...B...

5.

1. indicative price

2. A) institutional B) fair price

3. book of demand

4. A) price B) clearing

5. allocation

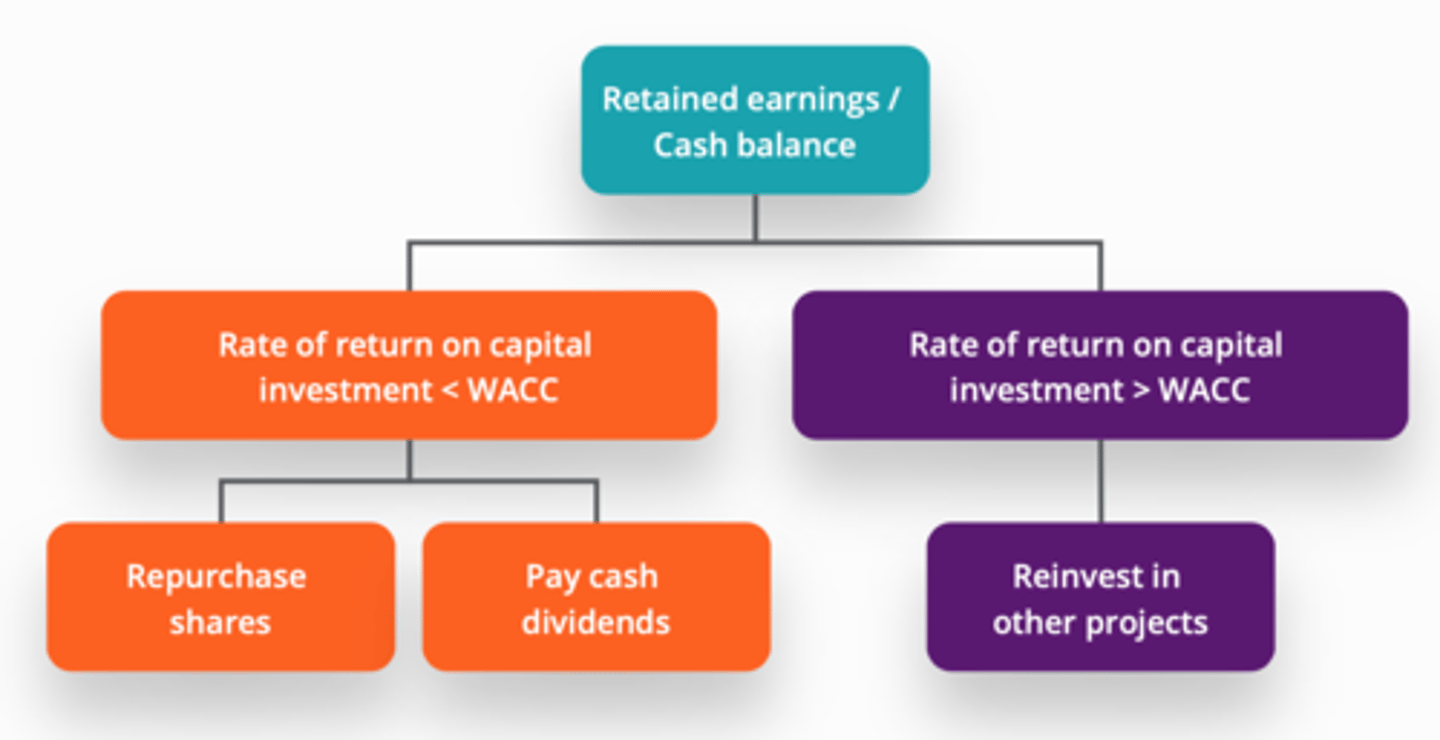

decision to return capital to investor is based on

IRR vs WACC

Retained earnings / excess cash decision flowchart:

1) ROIC < WACC : (2)

2) ROIC > WACC: : (1)

1)

a. repurchase shares

b. pay dividends

2) reinvest in other projects