CFA Volume 5 (Alternative Investments)

1/290

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

291 Terms

Alternative Investments

Investments other than ownership of public equity securities, fixed-income instruments, or cash that represent the more traditional asset classes.

Investors attracted to alternatives when seeking greater diversification and/or higher expected returns in exchange for what are often longer-term, illiquid investments in less efficient markets.

Distinguishing features of alternatives in comparison to traditional investments

1) Need for specialized knowledge to value cash flows and risks

2) Low correlation of returns with more traditional asset classes

3) Illiquidity, long investment time horizons, and large capital outlays

Key characteristics of alternative investments

1) Different investment structures

2) Incentive fees

3) Performance appraisal challenges

4) Longer time horizons

5) Larger financial commitments

Private Capital

Broad term for funding provided to companies that is sourced from neither the public equity nor the public debt markets. Broken down into private equity and private debt.

For a private capital fund, management fees are a percentage of committed capital rather than invested capital. For a hedge fund, management fees are a percentage of assets under management

Private Equity

Refers to investment in privately owned companies or in public companies with the intent to take them private. Generally used in the mature life cycle stages or for firms in decline, with LBOs being a key approach.

The best diversification approach is by vintage year (as timing of project relates to the economic environment and therefore performance).

Management fees are calculated as a percentage of committed capital (which reduces incentive for GPs to deploy the committed capital as quickly as possible to grow their fee base).

Average life is 10 years.

Venture Capital

Specialized form of PE whereby ownership capital is used for non-public companies in the early life cycle or startup phase (i.e., huge growth potential).

Usually make first investment suring the seed stage.

Venture Debt

Extended to early-stage firms with little or no cash flow.

Developed Land

Includes commercial and industrial real estate, residential real estate, and infrastructure.

Commercial Real Estate

Includes land and buildings where predicate business activity is the primary cash flow source, whereas residential real estate's cash flows stem from rents or mortgage payments by households.

Concession Agreement

Governs the private investor's obligations to construct and maintain infrastructure as well as the exclusive right to operate and earn fees for a pre-determined period.

Used mostly in public-private partnerships (PPPs).

Commodities

Plant, animal, energy, and mineral products used in goods and services production. Do not generate cash flows directly, but ultimately sold by commodity producers to commodity consumers for economic use. The supply of commodities is inelastic (difficult to replenish quickly).

With their lower correlation of returns with other asset classes, can also serve as a countercyclical holding and as an inflation hedge (as some commodities are components of inflation - food and energy and have a positive relationship to inflation rates).

Commodities perform well when inflation is higher. In stable inflation environments, commodity returns tend to be low but positive.

Examples of other real alternative assets

Tangible collectible assets such as fine art, wine, rare coins, watches.

Intangible assets such as patents, litigation, and digital assets.

Digital Assets

The umbrella term covering assets that can be created, stored, and transmitted electronically and have associated ownership or use rights. Digital assets include a variety of assets, such as cryptocurrencies, tokens (security and utility), and digital collectables.

Hedge Funds

Private investment vehicles that typically use leverage, derivatives, and long and short investment strategies. Invest in public equities or publicly traded fixed-income assets, private capital, and/or real assets.

Average life of 5 years.

Typically only available to institutional or accredited investors (which includes accredited retail investors such as high-net-worth individuals).

Fund of Funds

Mutual funds that primarily invest in other mutual funds (e.g., hedge fund).

Three categories of alternatives

1) Private Capital

2) Real Assets

3) Hedge Funds

Three ways investors can access alternatives

1) Fund investment (e.g., in a PE fund)

2) Co-investment into a portfolio company of a fund

3) Direct investment into a company or project (e.g., infrastructure or real estate)

Fund investing gives an investor access to a diversified pool of assets. Co-investing typically requires a larger investment amount. Direct investing provides the least diversification and requires the largest capital investment.

Fund Investing

Investor contributes capital to a fund and the fund identifies, selects, and makes investments on the investor's behalf. Requires a precommitment of funds by LPs before investment selection.

Investor is charged a management fee, plus a performance fee if the fund manager delivers superior results versus a hurdle rate or benchmark.

Fund investors typically have neither the sophistication nor the experience to invest directly on their own. They're also typically unable to affect the fund's underlying investments.

Differences between fund investing for alternatives and traditional public equity and fixed-income funds

Alternatives usually involve:

1) the pre-commitment of funds prior to investment selection and an extended period during which the fund may not be sold

2) higher management fees with more complex fee structures (performance-based)

3) less frequent transparency on periodic returns and fund positions

Co-Investing

Investor invests in assets indirectly through the fund but also possesses rights (known as co-investment rights) to invest directly in the same assets.

Through co-investing, investor able to make an investment alongside a fund when the fund identifies deals.

Direct Investment

Largest, most sophisticated investors with sufficient skills and knowledge to manage individual alternatives without the use of an intermediary (e.g., purchase of a direct stake in a private company without the use of a fund managed by an external asset manager or GP).

Requires investor to have resources to provide the specialized knowledge, skills, and oversight capabilities.

Features of alternatives that complicate performance appraisal between investments and across asset classes

1) The timing of cash inflows and outflows for specific investments

2) The use of borrowed funds

3) The valuation of individual portfolio positions over specific phases of the investment life cycle

4) More complex fee structures and tax and accounting treatment

Three periods of the investment life cycle

1) Capital Commitment

2) Capital Deployment

3) Capital Distribution

Capital Commitment Period

Alternative managers identify and select appropriate investment with either an immediate or a delayed commitment of capital (known as a capital call).

Returns are usually negative over this phase because fees and expenses are immediately incurred prior to capital deployment and assets may generate little or no income during this first phase.

Capital Deployment

Alternative managers deploy funds to engage in construction or make property improvements in the case of RE, incur expenses in the turnaround phase of a mature company in the case of PE, or initiate operations for a start-up using VC.

Cash outflows typically exceed inflows, with management fees further reducing returns.

Capital Distribution

When the turnaround strategy, startup phase, or property improvements are completed and if the investment is successful, the underlying assets appreciate in price and/or generate income in excess of costs, causing fund returns to accelerate.

Fund may realize substantial capital gains from liquidating or exiting its investments (e.g., IPO for VC or the sale of properties in the case of RE).

Funds with vintage years during contractions are likely to earn higher rates of return if they specialize in __________ companies. Funds with vintage years during expansions are likely to earn higher rates of return if they specialize in __________ companies.

Distressed, Early-Stage

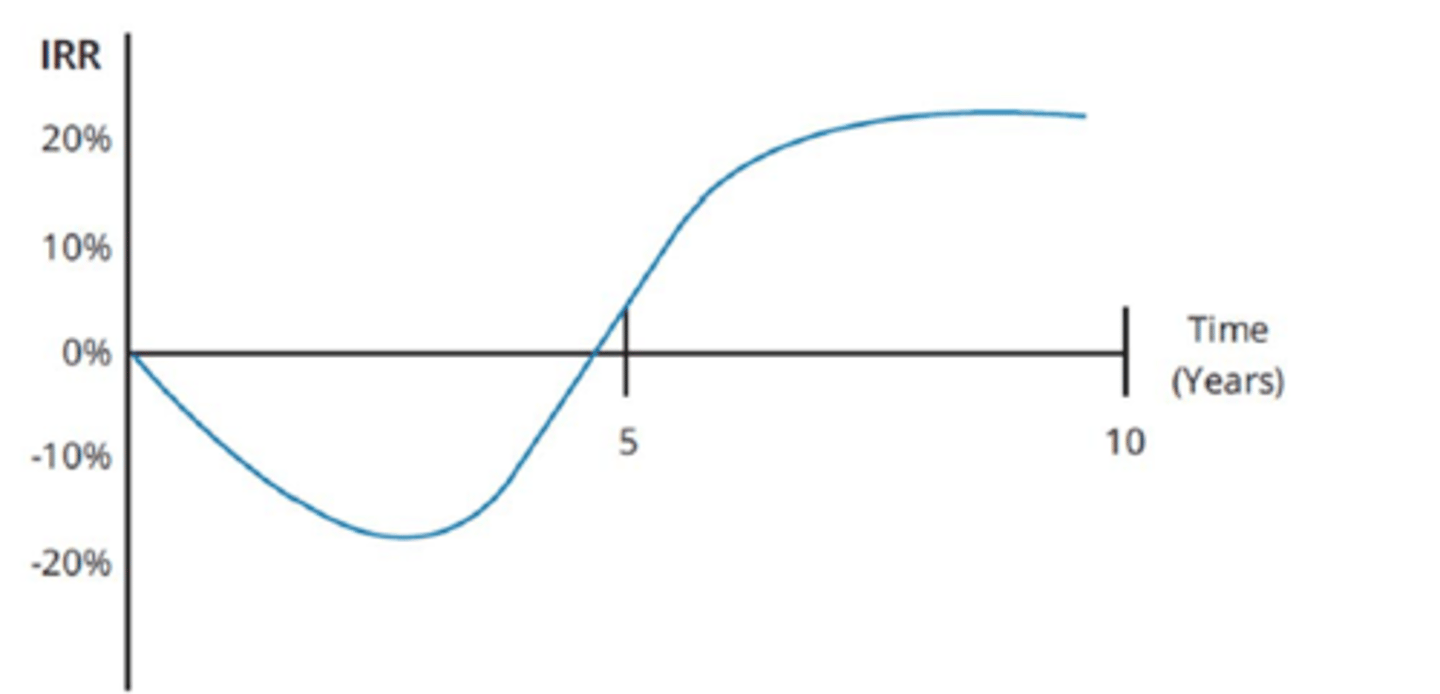

J-Curve Effect

Represents the initial negative return in the capital commitment phase followed by an acceleration of returns through the capital deployment phase.

IRR is the metric used to measure performance here (PE and RE).

Multiple of Invested Capital (MOIC)

(Realized value of investment + Unrealized value of investment) / Total amount of invested capital

Margin Financing

Prime broker essentially lends the hedge fund the shares, bonds, and derivatives, and the hedge fund deposits cash or other collateral into a margin account with the prime broker based on certain fractions of the investment positions.

Fair Value

The fair value of an investment is a market-based measure based on observable or derived assumptions that market participants use to exchange an asset or liability.

Level 1 of Fair Value Hierarchy

Quoted prices in active markets for identical asset/liability that may be accessed as of measurement date.

Most reliable measures for valuation (true observations).

Example: exchange-traded public equities

Level 2 of Fair Value Hierarchy

Inputs other than quoted market prices in Level 1 that are directly or indirectly observable for an asset/liability.

Approaches to fair value calculations include some sort of modeling or interpolation.

Example: OTC derivatives

Level 3 of Fair Value Hierarchy

Unobservable inputs are used to measure fair value for asset/liability in which there is little, if any, market activity as of the measurement date.

Use appraisal process to estimate value, which has data quality issues related to smoothing (i.e., shows less volatility).

Example: private equity and real estate

Different leverage approaches

1) Borrowing capital to invest directly in securities

2) Using derivatives requires a small initial margin to gain greater exposure (e.g., futures)

3) Margin financing: a prime broker lends any securities needed, in return for collateral deposited into a margin account

Key benefit of using leverage

More exposure with a small amount of cash

Key difference between traditional and alternative investment returns

In the traditional world, performance is mainly driven by asset allocation, where for alternatives performance is mainly driven by the manager (and therefore comes with higher fees).

Redemption

Redemptions frequently occur when a hedge fund is performing poorly. Redemptions may require the hedge fund manager to liquidate some positions and potentially receive particularly disadvantageous prices when forced to do so by redemption pressures, while also incurring transaction costs.

Redemption Fee

Fee to discourage redemption and offset the transaction costs for remaining investors in the fund.

Notice Period

A period (typically 30-90 days) in advance that investors may be required to notify a fund of their intent to redeem some or all their investment. This notice period allows the fund manager an opportunity to liquidate a position in an orderly fashion without magnifying the losses.

Lockup Period

The minimum holding period before investors are allowed to make withdrawals or redeem shares from a fund.

Gate

A provision that when implemented limits or restricts redemptions for a period of time, usually at the discretion of the fund manager.

Different from a lockup period

Founders Class Shares

A way to entice early participation in startup funds whereby managers offer incentives that entitle investors to a lower fee structure and/or other favorable terms.

Either/Or Fees

Choosing between fixed management and variable performance fees. Managers agree either to charge a lower, 1% management fee (to cover expenses during down years) or to accept a higher, 30% incentive fee above a mutually agreed-upon annual hurdle (to incentivize and reward managers during up years), whichever is greater.

Survivorship Bias

A form of selection bias that is characterized by the exclusion of failed funds from a given benchmark that can lead to overly optimistic return expectations.

Backfill Bias

A form of bias that is characterized by a fund manager including only the most successful funds in an index, or "backfilling" of prior performance data on a selective basis serving to increase average reported returns.

Only including funds after they have successful performance to report.

Selection Bias

Likely to result in a misallocation of funds to an index for a particular strategy but is less likely to result in an overestimation of performance compared to survivorship and backfill bias.

Three types of private equity strategies

1) Leveraged Buyout (LBO)

2) Venture Capital (VC)

3) Growth Capital

Leveraged Buyouts

Highly leveraged transactions that arise when PE firms establish buyout funds (or LBO funds) to acquire public companies or established private companies, with a significant percentage of the purchase price financed through debt.

Target company's assets typically serve as collateral for the debt, and target company's cash flows expected to be sufficient to service the debt.

LBO transactions sometimes called "going private" transactions.

Management Buy-In (MBI)

Types of LBO where the current management team is replaced with the acquiring team involved in managing the company.

Pre-Seed Capital (or Angel Investing)

Capital provided at the idea stage. Funds may be used to develop a business plan and to assess market potential. Amount of financing is usually small coming from individuals (usually friends and family).

Seed-Stage Financing (or Seed Capital)

Generally supports product development and marketing efforts, including market research. This is the first stage at which VC funds usually invest.

In the seed stage of venture capital investing, capital is furnished for product development, marketing, and market research. The angel investing stage is when investment funds are used for business plans and assessing market potential. The early stage refers to investments made to fund initial commercial production and sales.

Early-Stage Financing (or Start-Up Stage Financing)

Goes to companies moving toward operation but prior to commercial production or sales, in both of which early-stage financing may be injected to initiated.

Later-Stage Financing

Comes after commercial production and sales have begun but before an IPO. Funds may be used to support initial growth a major expansion, product improvements, or a major marketing campaign.

Mezzanine-Stage Financing

Prepares a company to go public as it continues to expand capacity and enhances its growth trajectory. Represents the bridge financing needed to fund a private firm until it can execute an IPO or be sold.

Typically either equity-like (to capture potential gains from the planned IPO) or short-term debt.

Private Investment in Public Equity (PIPE)

A private offering to select investors with fewer disclosures and lower transaction costs that allow the issuer to raise capital more quickly and cost effectively than with other means that may be more regulated, expensive, and lengthy.

Investors are typically investment firms, mutual funds, or other institutional investors.

Common in work-out or rescue situations where there is a material difference in the market price and valuations.

Trade Sale

A portion or division of a private company sold via either direct sale or auction to a strategic buyer interested in increasing the scale and scope of an existing business.

Key advantage is that a strategic investor will be willing to pay a premium as they price in potential synergies with their existing business.

Direct Listing

Exit strategy in which the equity of the entity is floated on the public markets directly, without underwriters, reducing the complexity and cost of the transaction.

Special Purpose Acquisition Company (SPAC)

Exit strategy in which a "blank check" company exists solely for the purpose of acquiring an unspecific private company with a predetermined period.

American-Style Waterfall Structure

An American-style waterfall structure has a deal-by-deal calculation of incentive fees to the GP. In this case, a successful deal where incentive fees are paid, followed by the sale of a holding that has losses in the same year, can result in incentive fees greater than those calculated using a European-style (whole-of-fund) waterfall

A clawback provision, coupled with an American-style waterfall, will result in the same overall performance fees as a European-style waterfall if the transactions occur in subsequent years

Stockholder Overhang

The downward pressure on the share price of stock as large blocks of shares are being sold on the open market.

Advantages of Trade Sales

1) Immediate cash exit

2) Higher price from synergy-seeking strategic buyers

3) Fast and simple execution

4) Streamlined process on transaction cost, disclosure, and confidentiality from dealing with only one party

Disadvantages of Trade Sales

1) Potential existing management opposition

2) Limited set of buyers

3) Reduces financial appeal to employees due to forgone monetization of ownership stakes/options

Advantages of IPOs

1) Highest potential share price

2) Likeliest management approval

3) Notoriety to private equity sponsor

4) Sharing in potential share price appreciation from ongoing ownership stake

Disadvantages of IPOs

1) High transaction costs

2) Long lead time

3) Stock market volatility creating value uncertainty

4) Onerous disclosure

5) Potential lockup period freezing capital committed to deal

6) Suitable mainly for large and fast-growing companies

Advantages of SPACs

1) Extend disclosure time and ability to provide forward guidance to develop investor interest

2) Fixed valuation with lower share price volatility

3) Transaction structure flexibility

4) Involvement of high-profile, seasoned sponsors and their investor networks

Disadvantages of SPACs

1) Potential higher capital costs of dilution, warrants, and fees

2) Divergence between announced and true equity value due to dilution

3) Deal and capital risk of potential redemptions

4) Prolonged post-merger stockholder overhand and churn

Recapitalization

Exit strategy in which the steps a firm takes to increase or introduce leverage to its portfolio company and pay itself a dividend out of the new capital structure.

Not a true exit strategy because the PE firm typically maintains control, but allows the PE investor to extract money from the company to pay its investors and improve its IRR.

Secondary Sale

Exit strategy in which there is a sale of the company to another PE firm or group of financial buyers.

Write-Off/Liquidation

Exit strategy for when a transaction has not gone well, and the investment is likely to lose value. The PE firm then revises the value of its investment downward or liquidates the portfolio company before moving on to other projects.

Direct Private Debt Investment

Investor makes a loan directly to a specific operating company.

Indirect Private Debt Investment

Investor purchases an interest in a fund that pools contributions typically on behalf of multiple participants to buy into the debt from a set of operating companies.

Leveraged Loan

A loan that is itself levered. Private debt firms that invest in leveraged loans first borrow money to finance the debt and then extend it to another borrower. By using leverage, a private debt firm can enhance the return on its loan portfolio.

Mezzanine Debt

Private credit subordinated to senior secured debt but senior to equity in the borrower's capital structure.

A pool of additional capital available to borrowers beyond senior secured debt, often used to finance LBOs, recapitalizations, corporate acquisitions, and similar transactions.

Because of its typically junior ranking and its usually unsecured status, it is riskier than senior secured debt.

May have feature such as warrants to compensate investors for additional risk.

Distressed Debt

Entailed buying the debt of mature companies in financial difficulty (bankrupt, defaulted on debt, or seem likely to default on debt).

Investors buy the company's debt expecting both the company and its debt to increase in value.

Unitranche Debt

Consists of a hybrid or blended loan structure that combines different tranches of secured and unsecured debt into a single loan with a single, blended interest rate.

Since it's a blend of secured and unsecured debt its interest rate will generally fall in between the interest rates often demanded on secured and unsecured debt.

Typically ranks between senior and subordinated debt.

Vintage Year

The year in which the fund makes its first investment. Typically, a PE fund operates over a 10- to 12-year period, which is often segmented into an initial investment period and a subsequent harvesting period.

Investors are encouraged to pursue vintage diversification by investing in multiple vintage years.

Typical property types for residential real estate

Owner-occupied, single residences, single-family

Typical property types for commercial real estate

Residential properties owned for lease or rental, office, retail, industrial, warehouse, hospitality, and mixed-use properties

Source of equity for residential real estate

Owners

Source of equity for commercial real estate

Privately held by owners, publicly held through investors

Source of debt for residential real estate

Directly: lenders (banks) through residential mortgages

Indirectly: investors in MBS that package residential mortgages

Source of debt for commercial real estate

Directly: lenders (banks) through commercial mortgages

Indirectly: investors in MBS that package commercial mortgages

Source of investor return from residential real estate

Enjoyment of the property, price or capital appreciation

Source of investor return from commercial real estate

Income, or cash flow, generated by the property, price or capital appreciation

Private forms of real estate debt

1) Mortgage Debt

2) Construction Loans

3) Mezzanine Debt

Private forms of real estate equity

1) Sole Ownership (Direct)

2) Joint Ventures (Direct)

3) Limited Partnerships (Direct)

4) Real Estate Funds (Indirect)

5) Private REITs (Indirect)

Public forms of real estate debt

1) MBS / CMBS / CMOs

2) Covered Bonds

3) Mortgage REITs

4) Mortgage ETFs

Public forms of real estate equity

1) Construction (Publicly Traded Shares)

2) Operating (Publicly Traded Shares)

3) Development (Publicly Traded Shares)

4) Public REITs

5) UCITS / Mutual Funds / ETFs

Key advantages to owning real estate directly

1) Control

2) Tax Benefits

3) Diversification

Real estate also offers predictable cash flows (via leases) and inflation protection because lease payments are regularly adjusted

Key disadvantages to owning real estate directly

1) Complexity

2) Need for specialized knowledge

3) Significant capital needs

4) Concentration risk

5) Lack of liquidity

Senior Debt Real Estate Strategies

First mortgages (first lien), investment-grade CMBS, low risk, low returns

Core Real Estate Strategies

REITs and other private real estate funds are structured as infinite-life, open-end funds and allow investors to contribute or redeem capital throughout the life of the fund (similar to mutual fund structure). These open-end funds generally offer exposure to well-leased, high-quality commercial and residential real estate in the best markets.

Investors expect core real estate to deliver stable returns, primarily from income from the property.

Bond-like returns.

Core-Plus Real Estate Strategies

Value-add investments that require modest redevelopment or upgrades to lease any vacant space together with possible alternative use of the underlying properties.

Compared to core real estate strategies, these may be appealing for investors seeking higher returns and willing to accept additional risks from development, redevelopment, repositioning, and leasing.

Bond-like returns.

Value-Add Real Estate Strategies

Larger-scale redevelopment and repositioning of existing assets.

Larger speculative sources of price appreciation. Equity-like returns.

Opportunistic Real Estate Strategies

Include major redevelopment, repurposing of assets, taking on large vacancies, or speculating on significant improvement in market conditions. These may be appealing for investors seeking higher returns and willing to accept additional risks from development, redevelopment, repositioning, and leasing.

Very illiquid (time to construct/development).

Infrastructure Investments

Real, capital-intensive, and long-lived assets intended for public use and provide essential services, such as airports, health care facilities, and sewage treatment plants.

Most infrastructure assets are financed, owned, and operated by governments, and a substantive proportion of these investments comes from public sources in the developing world.

Four categories of infrastructure investments

1) Transportation Assets

2) Information and Communication Technology (ICT) Assets

3) Utility and Energy Assets

4) Social Infrastructure Investments

Economic Infrastructure Investments

Support economic activity through:

1) transportation assets

2) information and communication technology (ICT) assets, and 3) utility and energy assets.

Transportation Assets

Include roads, bridges, tunnels, airports, seaports, and heavy and light/urban railway systems. Income will usually be linked to demand based on traffic, airport and seaport charges, tools, and rail fares and hence is deemed to carry market risk.