Equilibrium in Macroeconomics: Supply and Demand Analysis

1/130

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

131 Terms

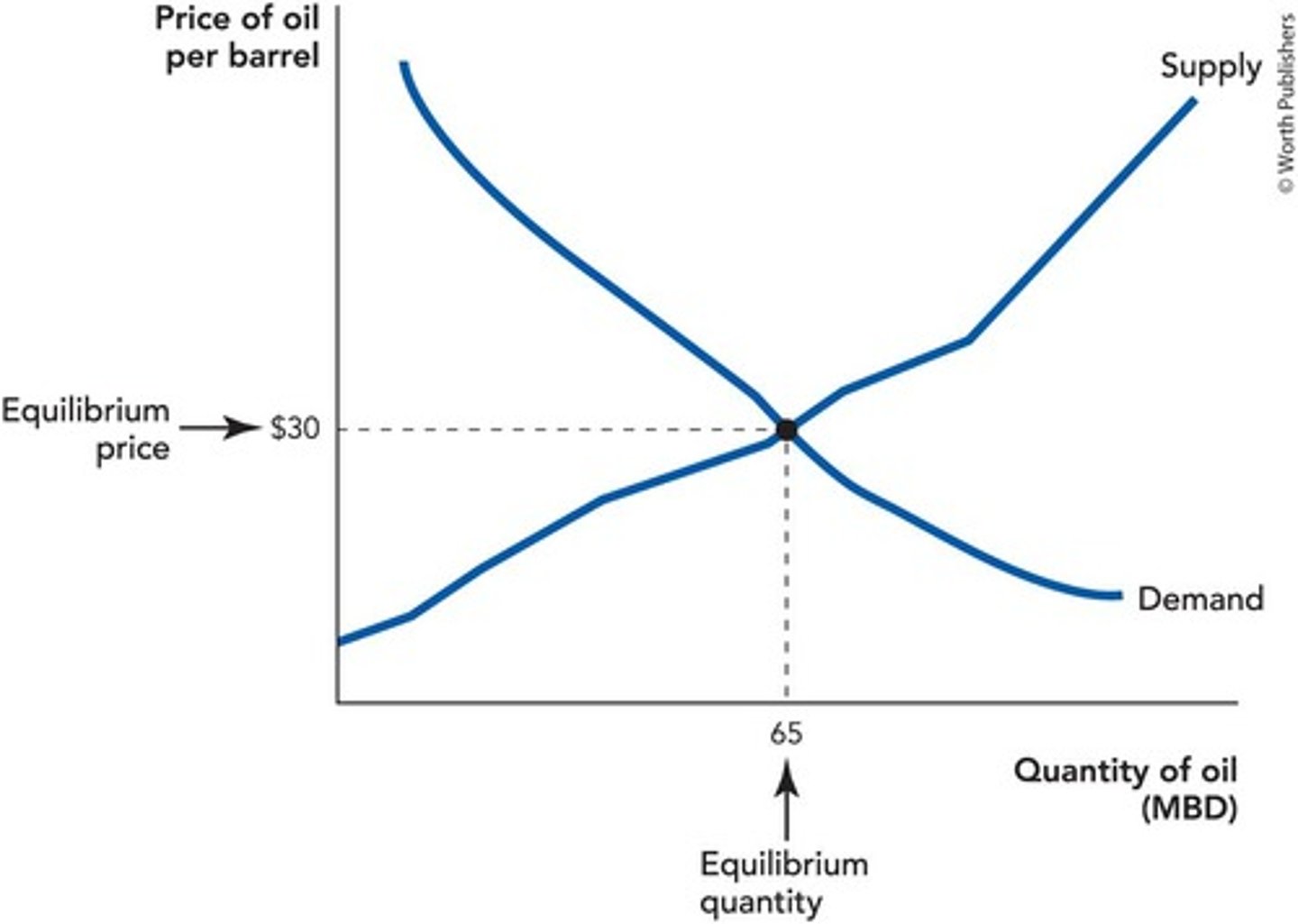

Equilibrium Price

Price where quantity demanded equals quantity supplied.

Equilibrium Quantity

Quantity exchanged at equilibrium price.

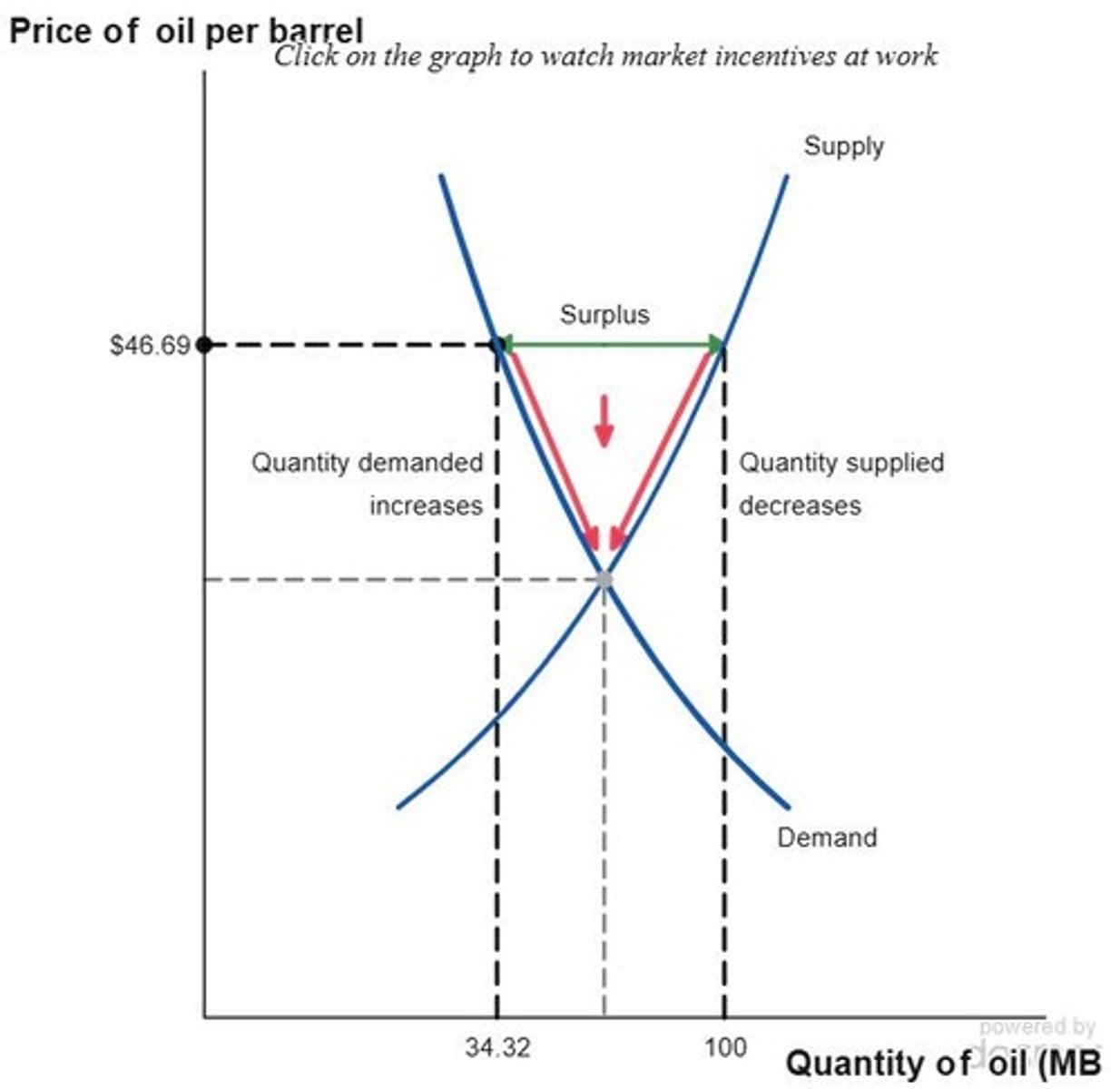

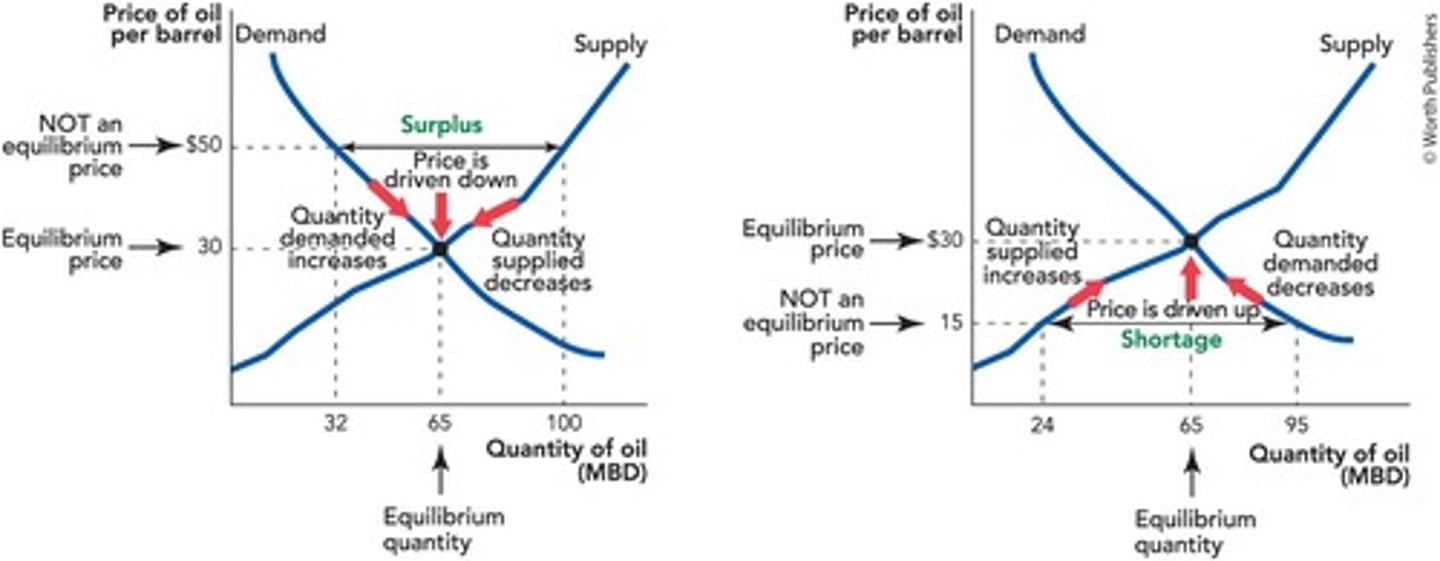

Surplus

Quantity supplied exceeds quantity demanded.

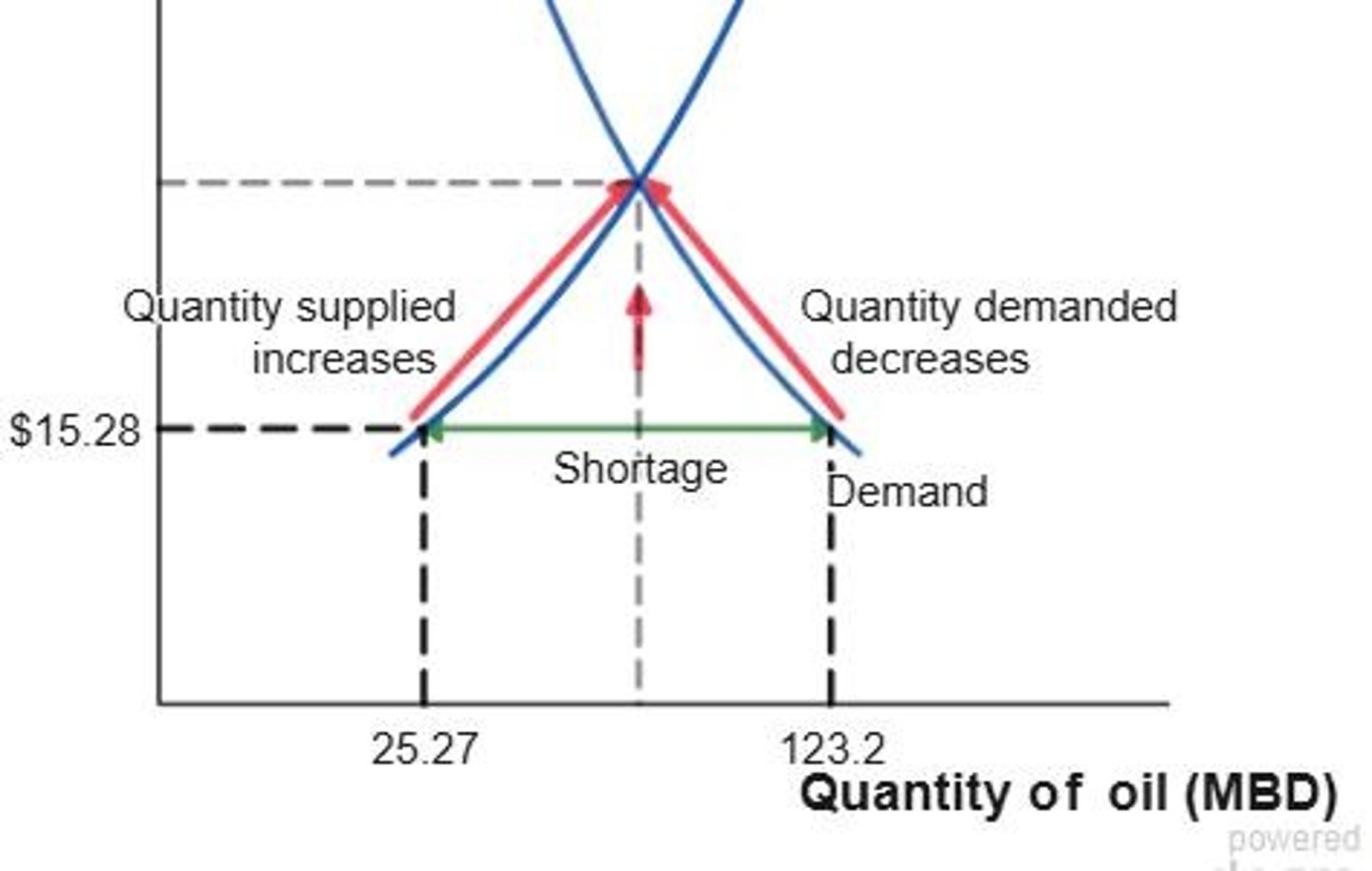

Shortage

Quantity demanded exceeds quantity supplied.

Adjustment Process

Market response to changes in supply and demand.

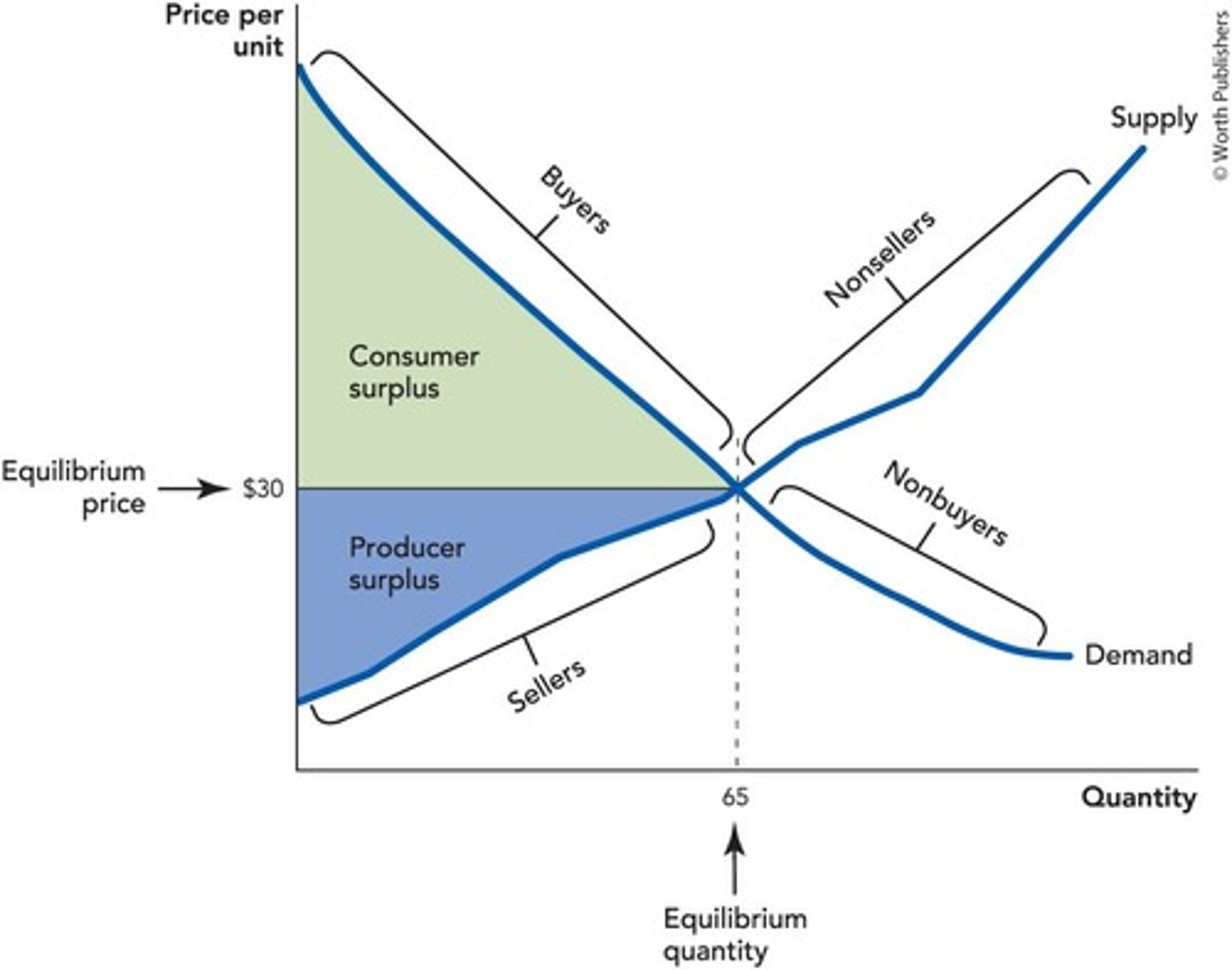

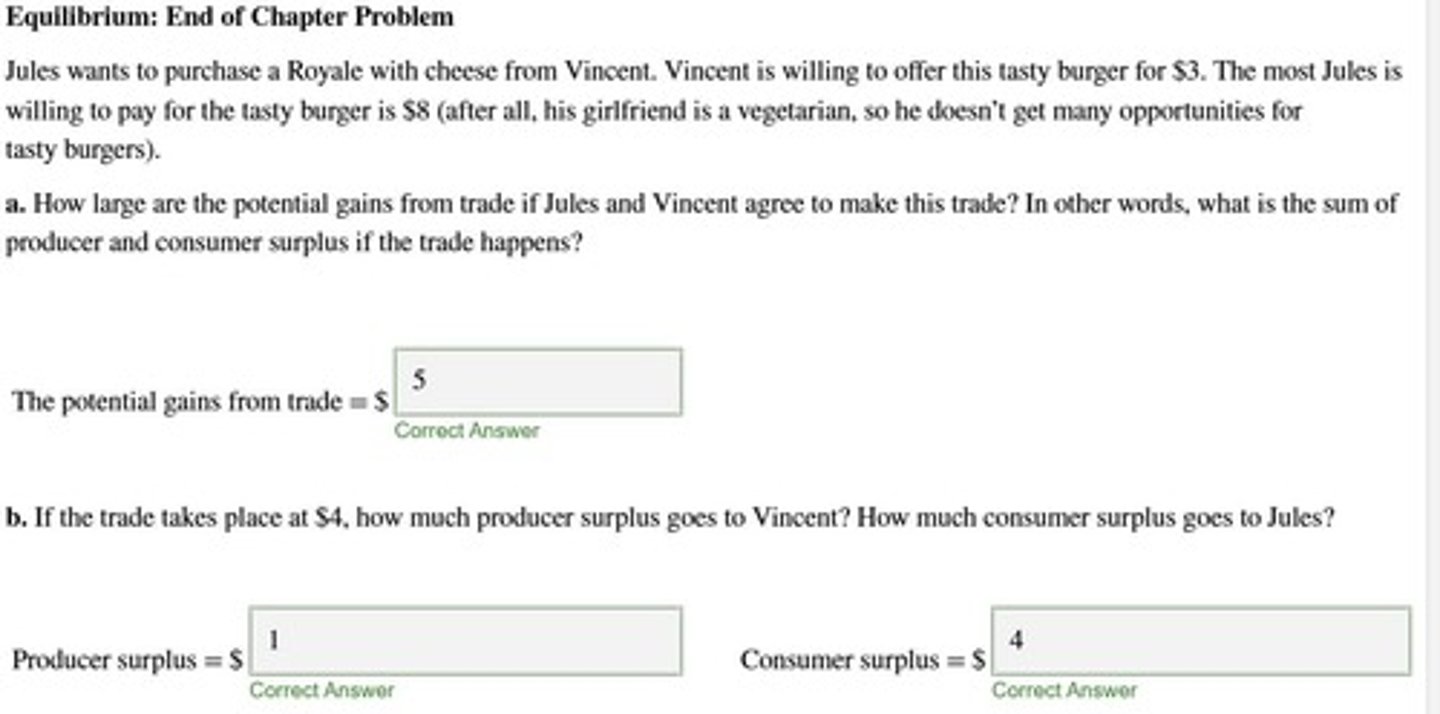

Producer Surplus

Difference between selling price and cost of production.

Consumer Surplus

Difference between willingness to pay and market price.

Market Forces

Economic factors that influence price and quantity.

Price Decrease

Occurs when there is a surplus.

Price Increase

Occurs when there is a shortage.

Demand

Desire for a good or service at various prices.

Quantity Demanded

Amount of a good buyers are willing to purchase.

Supply

Amount of a good producers are willing to sell.

Quantity Supplied

Amount of a good available for sale at a price.

Excess Supply

Another term for surplus in the market.

Excess Demand

Another term for shortage in the market.

Incentive

Motivation for buyers or sellers to change behavior.

Price Stability

Condition where prices remain relatively constant.

Free Market

Economic system with minimal government intervention.

Laboratory Evidence

Experimental data supporting economic theories.

Gains from Trade

Benefits obtained from voluntary exchange.

Oil Price Understanding

Analysis of factors affecting oil pricing.

Equilibrium Quantity

Quantity at equilibrium price, no surplus or shortage.

Price Incentive

Motivation for price changes based on supply and demand.

Competition Effect

Sellers lower prices above equilibrium; buyers raise below.

Stable Equilibrium

Equilibrium price remains unchanged due to balanced demand and supply.

Buyer Behavior

Buyers buy freely at equilibrium, no price increase incentive.

Seller Behavior

Sellers sell freely at equilibrium, no price decrease incentive.

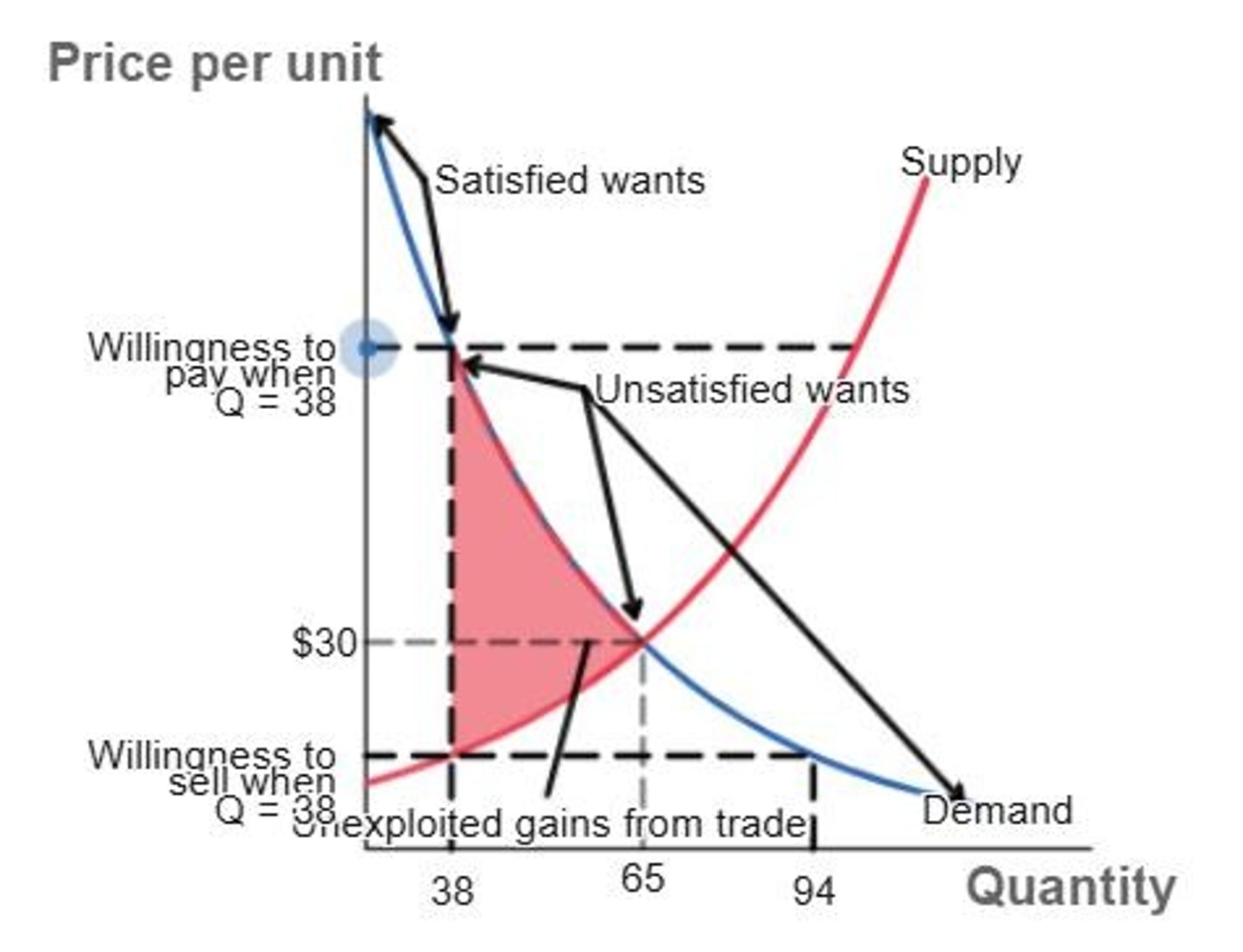

Unexploited Gains from Trade

Potential benefits when quantity is below equilibrium quantity.

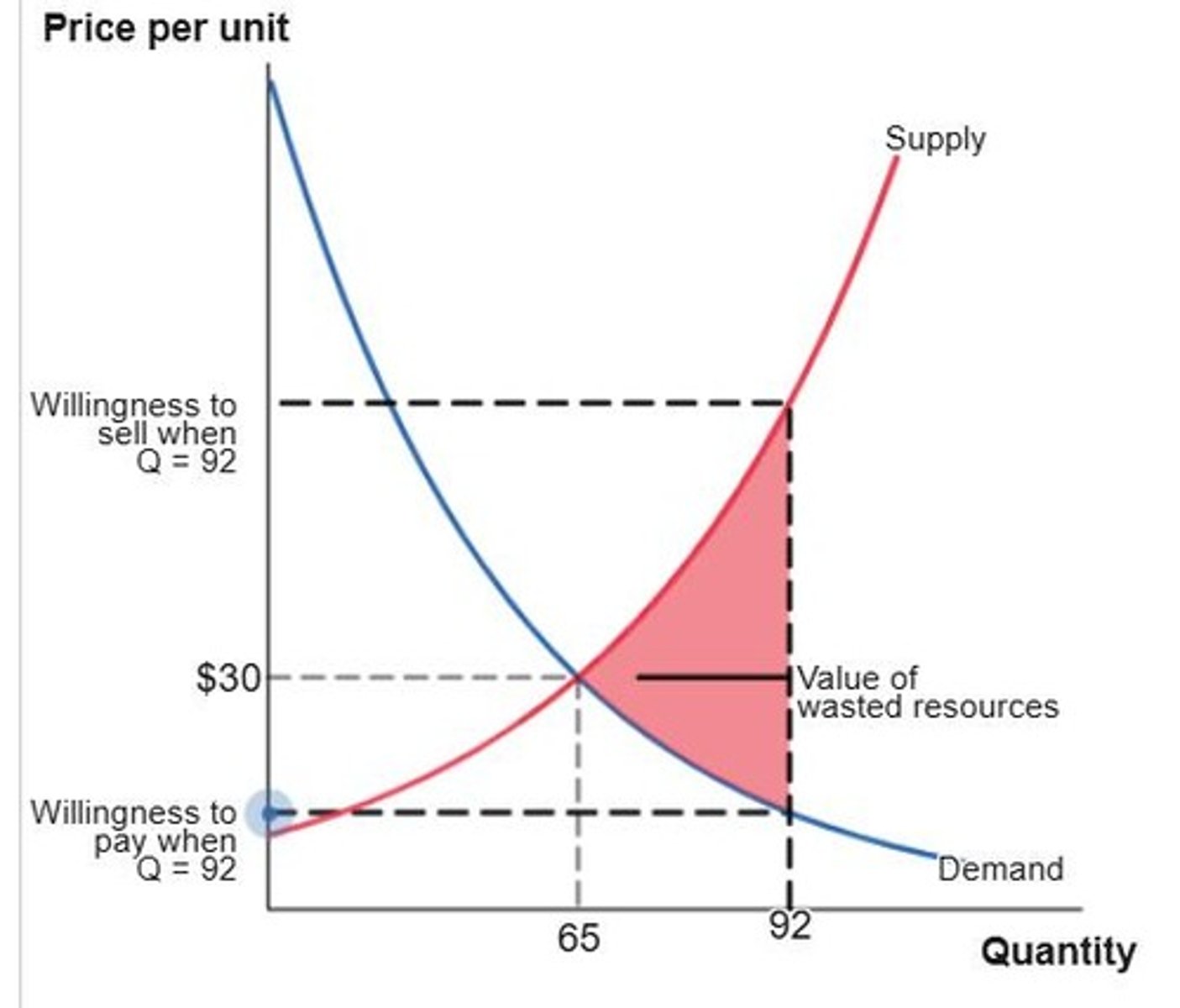

Wasted Resources

Loss incurred when quantity exceeds equilibrium quantity.

Demand Curve Value

Maximum price buyers pay at specific quantity demanded.

Satisfaction of Wants

Buyers allocate resources to highest-valued wants.

Producer Surplus

Difference between what sellers receive and minimum acceptable price.

Consumer Surplus

Difference between what buyers pay and maximum willing price.

Market Dynamics

Interaction of buyers and sellers influencing prices.

Quantity Supplied

Amount sellers are willing to sell at a given price.

Quantity Demanded

Amount buyers are willing to purchase at a given price.

Price Floor

Minimum price set by government, above equilibrium.

Price Ceiling

Maximum price set by government, below equilibrium.

Market Equilibrium

State where supply equals demand in a market.

Trade Gains

Benefits from exchanging goods or services between parties.

Resource Allocation

Distribution of resources to meet consumer demands.

Market Efficiency

Optimal distribution of resources without waste.

Gains from Trade

Benefits achieved through voluntary exchange in markets.

Producer Surplus

Difference between selling price and production cost.

Equilibrium Price

Price where quantity supplied equals quantity demanded.

Equilibrium Quantity

Quantity sold at the equilibrium price.

Free Market

Market with minimal government intervention and regulation.

Willingness to Pay

Maximum price a buyer is ready to pay.

Lowest Cost Seller

Seller with the minimum production cost for goods.

Unexploited Gains

Potential benefits from trade not realized in the market.

Wasteful Trades

Exchanges that do not maximize total surplus.

Market Supply Curve

Graph showing quantities supplied at various prices.

Market Demand Curve

Graph showing quantities demanded at various prices.

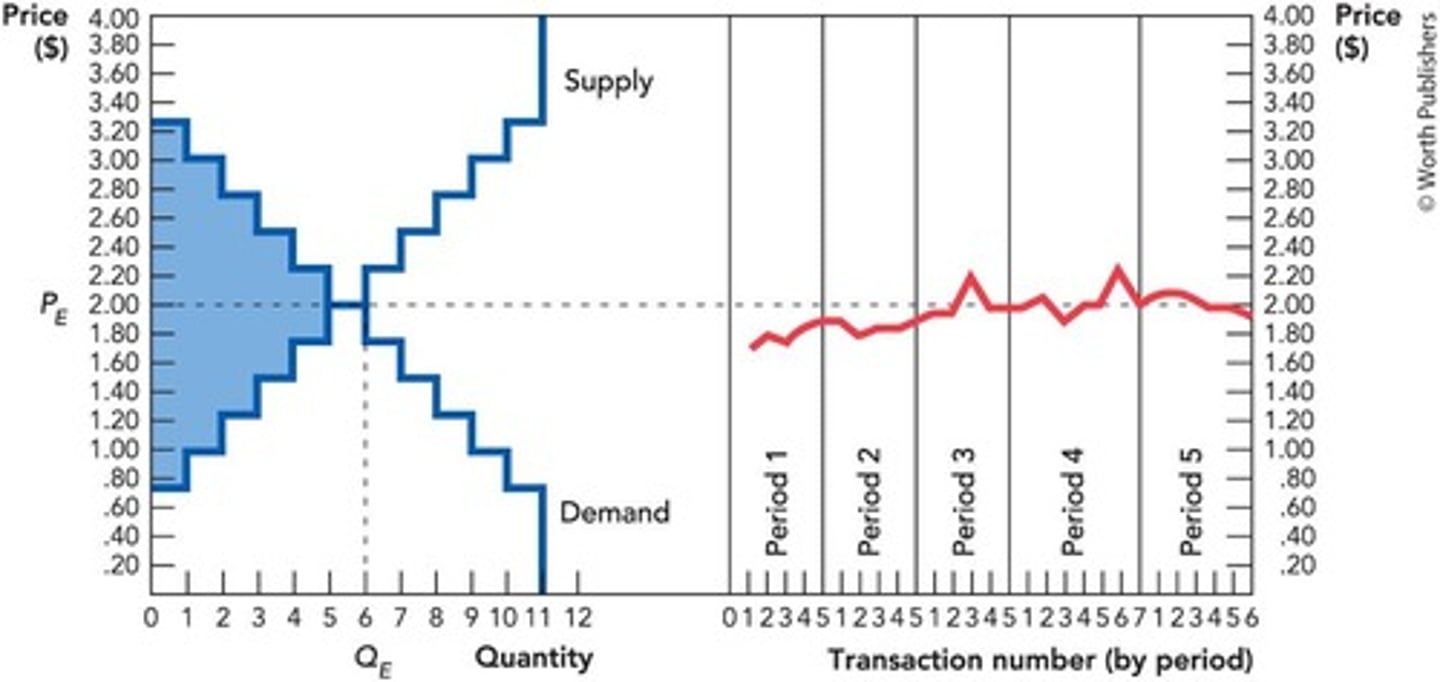

Vernon Smith

Economist known for experimental economics and market testing.

Experimental Economics

Field studying economic behavior through controlled experiments.

Supply and Demand Model

Framework explaining price formation through supply and demand.

Bids and Offers

Proposals made by buyers and sellers in a market.

Maximum Willingness to Pay

Highest price a buyer is willing to pay.

Minimum Selling Price

Lowest price a seller is willing to accept.

Convergence to Equilibrium

Process where market prices and quantities stabilize at equilibrium.

Laboratory Experiment

Controlled study to test economic theories in practice.

Market Efficiency

Optimal allocation of resources in a free market.

Trade Periods

Segments of time during which trades are conducted.

Willingness to Pay

Maximum price buyers are willing to pay.

Lowest Costs

Minimum price suppliers are willing to accept.

Quantity Traded

Total units bought and sold in the market.

Total Surplus

Sum of producer and consumer surplus.

Equilibrium Quantity

Quantity at which supply equals demand.

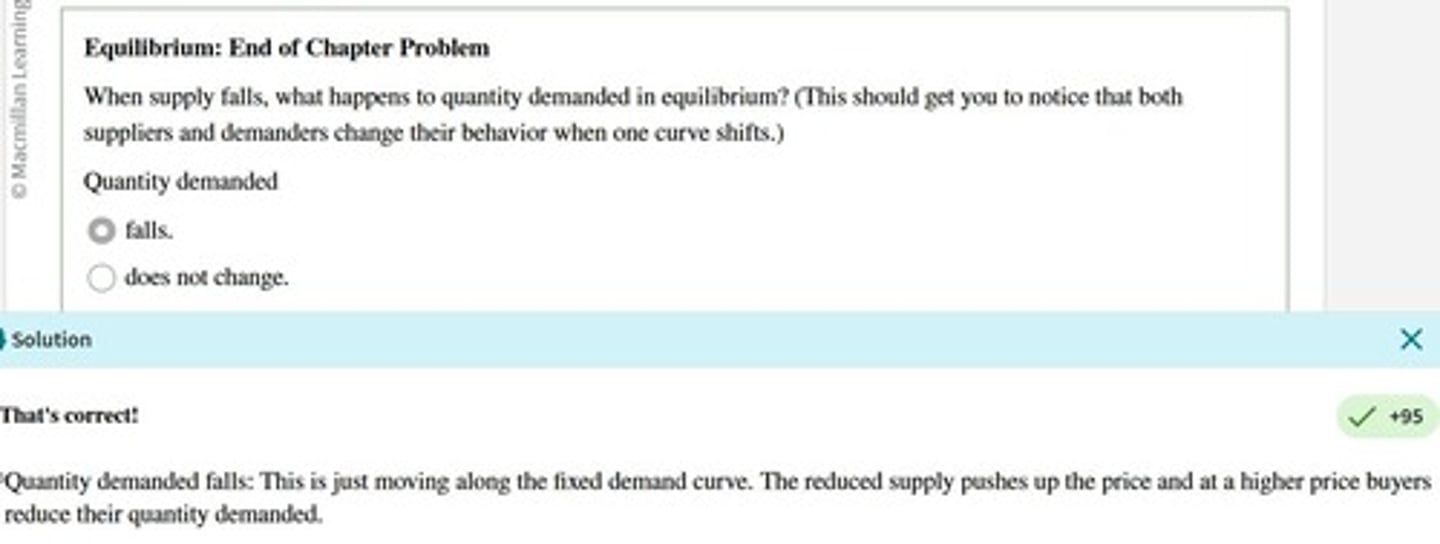

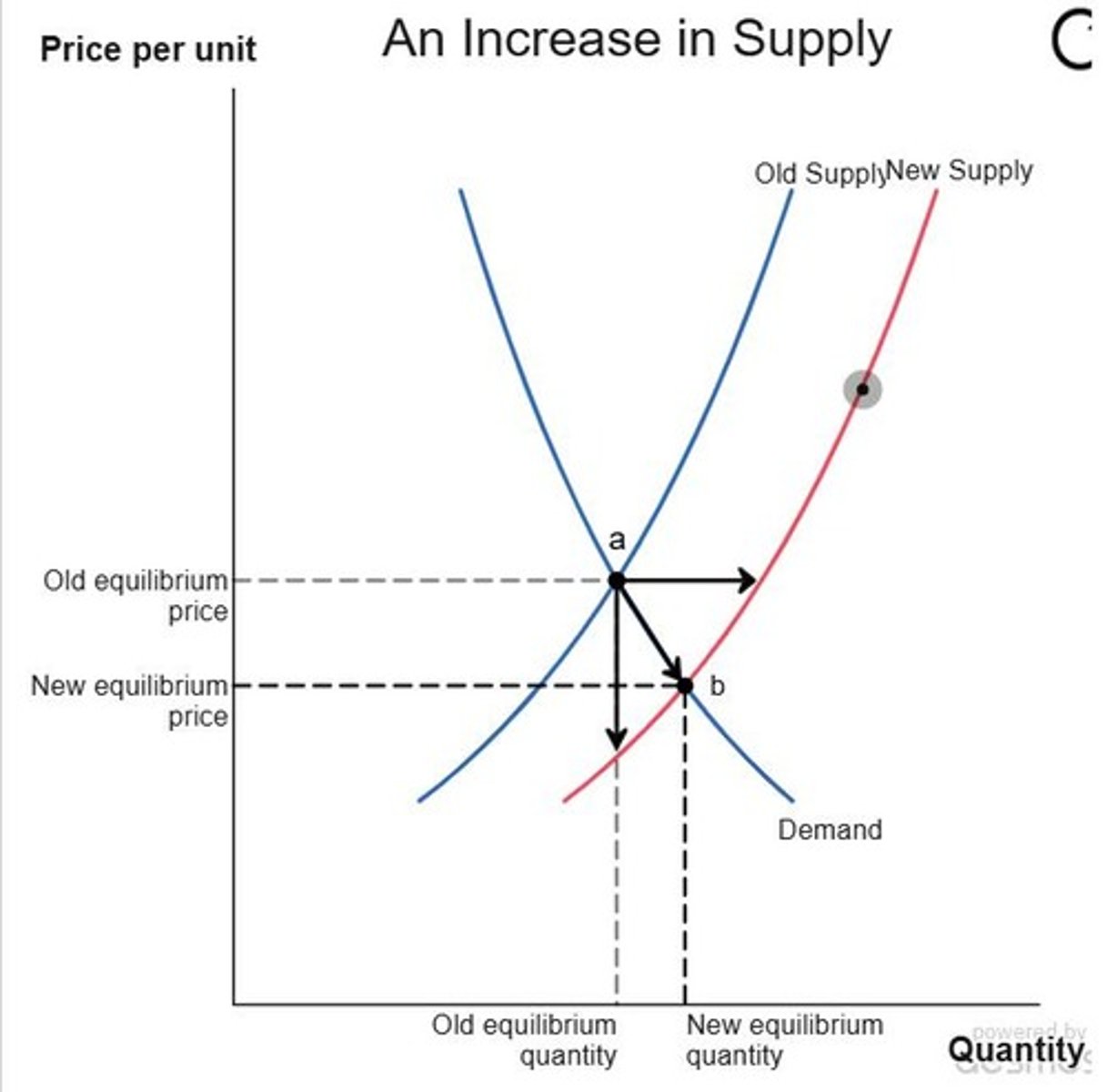

Supply Curve Shift

Change in supply due to cost variations.

Demand Curve Shift

Change in demand due to external factors.

Surplus

Excess supply at a given price.

Temporary Surplus

Short-term excess supply before market adjustment.

Competition Effect

Market forces that drive prices toward equilibrium.

Technological Innovations

Advancements that lower production costs.

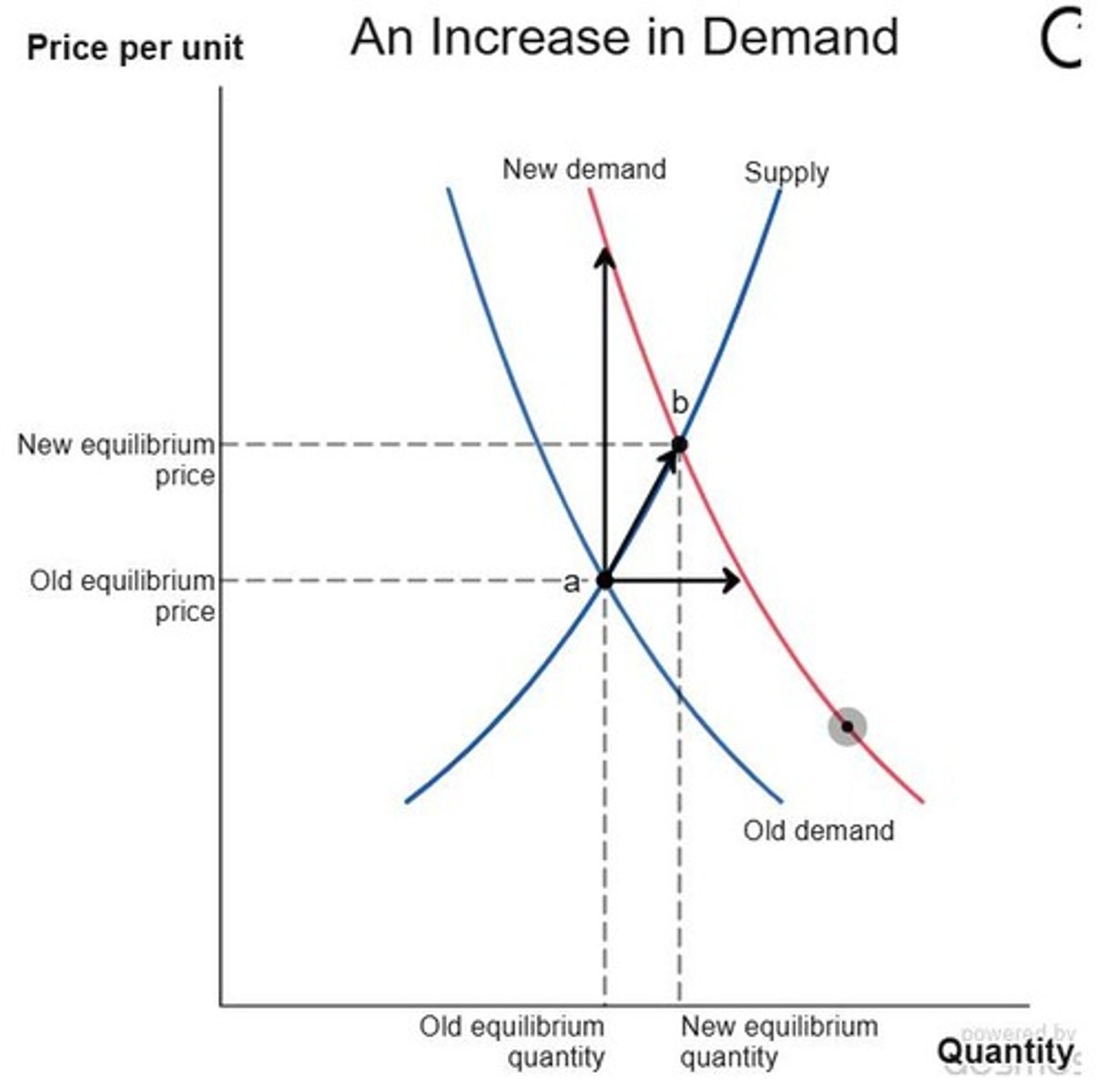

Old Equilibrium

Initial price and quantity before shifts occur.

New Equilibrium

Adjusted price and quantity after shifts occur.

Decrease in Supply

Reduction in quantity supplied at all prices.

Increase in Supply

Higher quantity supplied at all prices.

Decrease in Demand

Lower quantity demanded at all prices.

Increase in Demand

Higher quantity demanded at all prices.

Market Model Test

Experiment validating supply and demand principles.

Producer Surplus

Difference between selling price and cost.

Consumer Surplus

Difference between willingness to pay and price.

Supply and Demand Model

Framework explaining market behavior.

Price Adjustment

Change in price due to supply and demand shifts.

Quantity Demanded

Amount consumers are willing to buy at a price.

Supply

Amount of a good or service available for sale.

Quantity Supplied

Amount producers are willing to sell at a price.

Increase in Demand

Shift of the demand curve up and right.

Increase in Quantity Demanded

Movement along the demand curve due to price change.

Increase in Supply

Shift of the supply curve down and right.

Increase in Quantity Supplied

Movement along the supply curve due to price change.

Market Price

Price determined by supply and demand interactions.

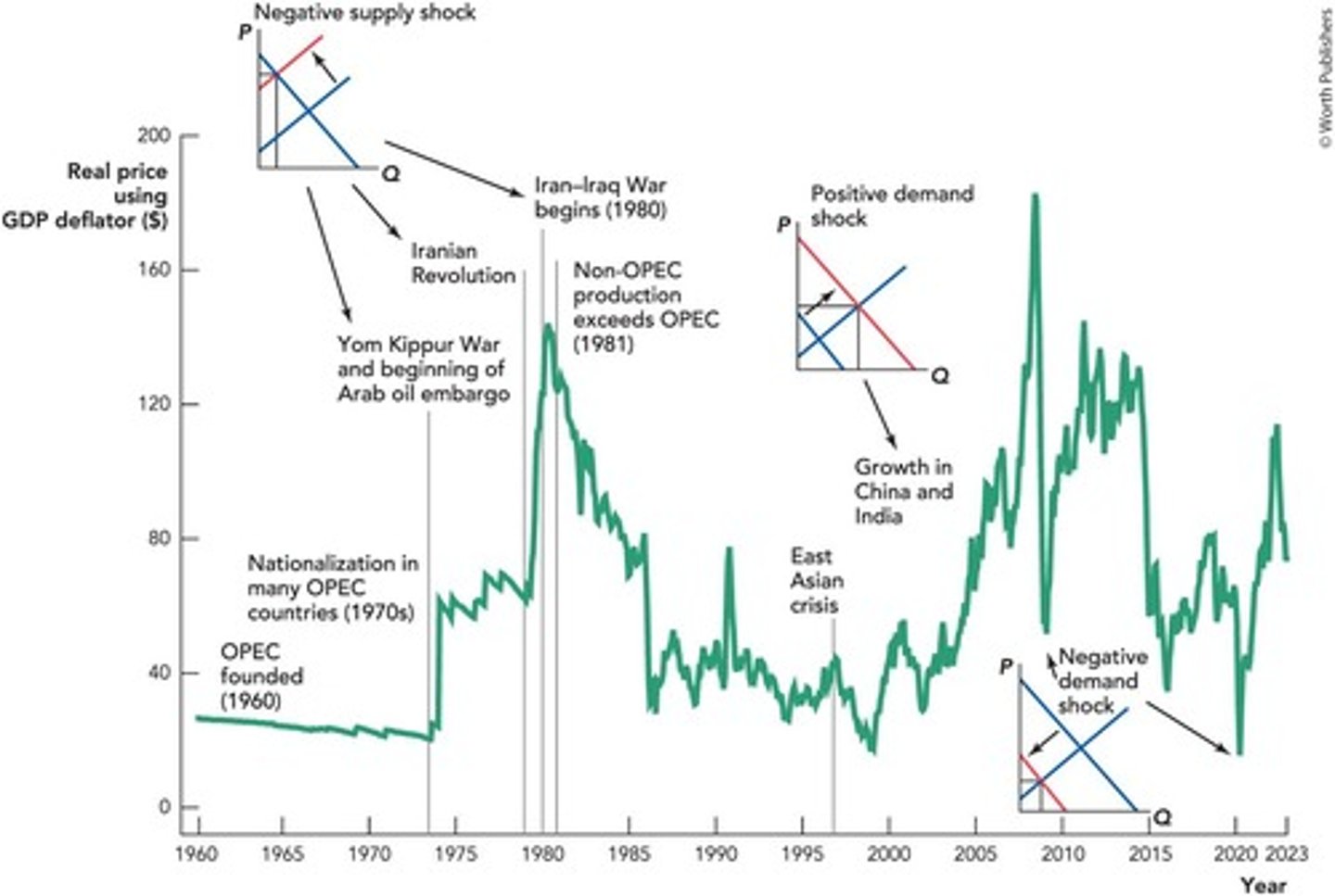

Real Price of Oil

Oil price adjusted for inflation over time.

Oil Supply Increase

Improved production techniques and discoveries boost supply.

Oil Demand Increase

Growing need for oil from early 20th century.

Competitive Conditions

Market structure where many firms compete freely.

Shifts in Demand

Changes in consumer preferences affecting demand curve.

Shifts in Supply

Changes in production costs affecting supply curve.