from 3.5 to 3.8. Learn pros/cons the importance of each.

Cash Flow

Payments received by a business (inflows) and payments made by a business (outflows).

Cash Inflows

the amount of cash flowing into or earned by the business from sales, debtors and other activities, such as the sale of unused fixed assets or the rent from extra office space.

Cash Outflows

the amount of cash paid out by the business for core operations such as raw materials, creditors and electricity and other activities such as legal fees.

Net Cash Flow

the difference between the total cash inflows and cash outflows. It could be positive or negative. Typically, businesses aim for a positive net cash flow

Opening Balance

Opening balance refers to the amount of cash the business has in the bank at the beginning of the month. I

Closing Balance

the amount of cash that the business has at the end of the month. It is the sum of the opening balance and the net cash flow.

Cash Flow Forecasts

A prediction of future cash inflows, cash outflows and net cash flow for a specific time period. To manage their operations effectively and avoid cash flow problems.

Cash Flow Forecasts Elements

Opening Balance, Cash inflows, Cash outflows, Net cash flows, and Closing balance.

Strategies to Increase Cash Inflows

Tighter credit control

Accepting cash payments only

Changing pricing policy

Improving the firm’s product portafolio

Strategies to decrease Cash outflows

Seeking alternative suppliers and preferential credit terms

Better stock control

Reduce expenses

Leasing rather than buying

Formulas of Cash Flow Forecast

Net Cash Flow: Cash inflows - cash outflows

Opening Balance: Closing balance - net cash flow

Closing Balance: Opening balance - net cash flow

Investment Appraisal

A process of quantative and qualitative evaluation of an investment decision.

Cumulative Net Flow (used on the investment appraisal)

cumulative net flow in previous year + net flow of current year

Payback Period (PBP)

the number of years and months it will take for the investment of a business to pay for itself.

amount left to pay/net cash flow in that year × 12

Average rate of return (ARR)

the average annual amount expected from an investment

Formula is given in the booklet. Where total returns = Total net cash flows

Net present value (NPV)

A method of using a discount rate to adjust the value of future returns. Used to work out the present value of the return on an investment.

Formula is given in the booklet.

Steps:

Discount the net cash flows in each year using the present value formula

Find the net present value

If net present value is positive, then the investment would have a positive return.

Present Value

Present value (single year)= net cash flow × discount factor

Found with the discount table

Discount Rate

the rate a business could earn on another comparable investment.

The discount table is given in the booklet

Budget

A financial plan for a defined period of time.

Short-term budgets: Budgets are usually set over a period of a year/monthly

Coordinated budgets: Departmental budgets typically feed into a centralised budget for the whole business.

Profit centres

A department in a business that generates both revenues and expenditures

Cost centres

for areas of the business that generate costs but no revenue.

The role of profit and cost centres

Managers can use this information to make budgets for the business as a whole with greater accuracy.

can provide teams of employees with a greater sense of autonomy over budgets.

can make better decisions about future strategy and where to invest.

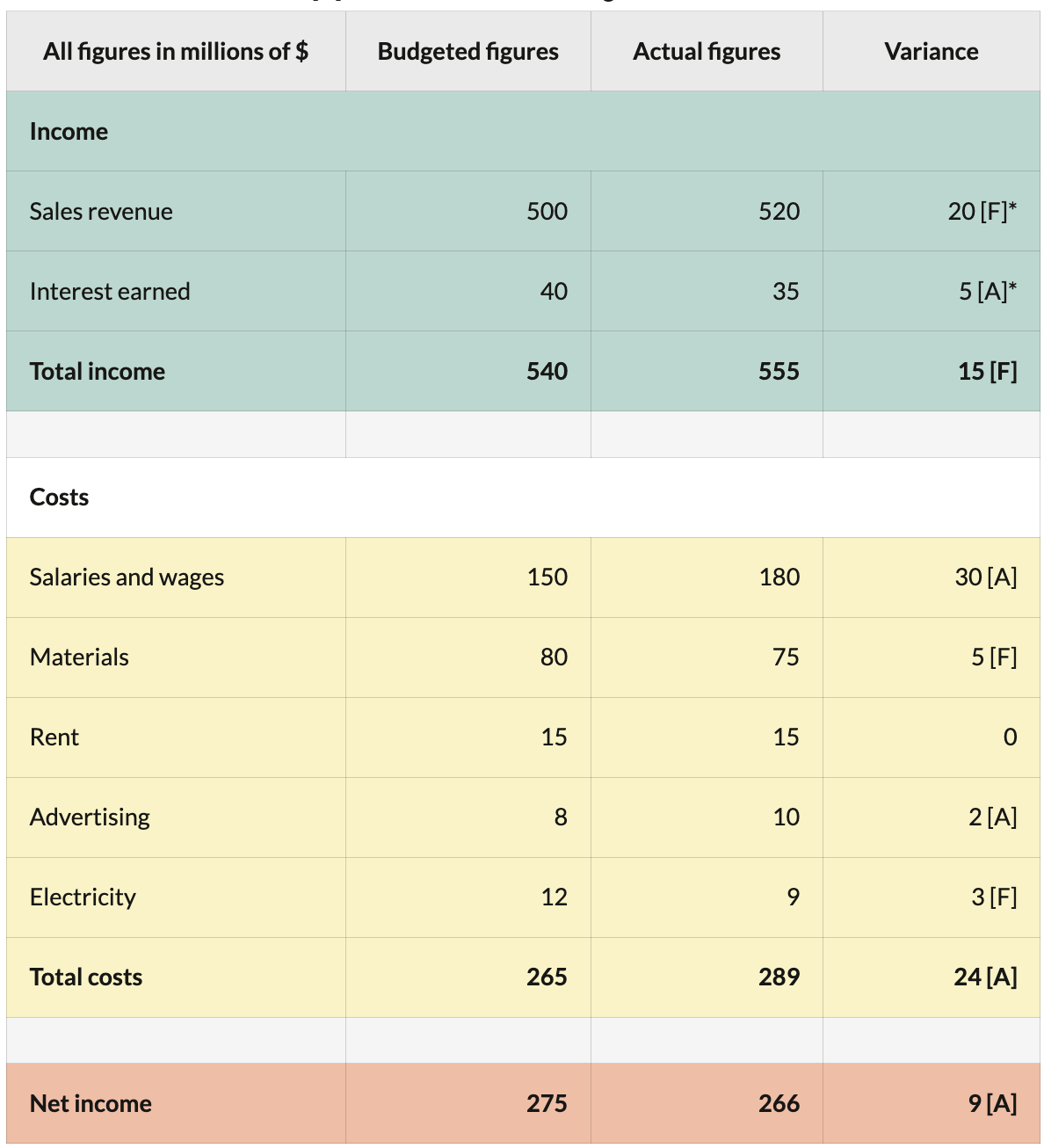

Format of a budget

A budget for a profit centre will include sections for both revenues and costs. A budget for a cost centre will only have a listing of costs.

ROWS:

Income (sales revenue, interest earned…)

Costs (salaries, ads, rent…)

Net income (total income - total costs)

COLUMNS:

Budgeted figures

Actual figures

Variance (Favorable/Adverse)

Variance

Two types of variance:

Favorable [F]: A situation when the actual budget situation is better than the forecast.

Adverse [A]: A situation when the actual budget situation is worse than the forecast.

No variance [0]: This means that the actual budget situation was the same as the forecasted budget.

If the budget is for a cost centre, there will be no variance calculated for income.

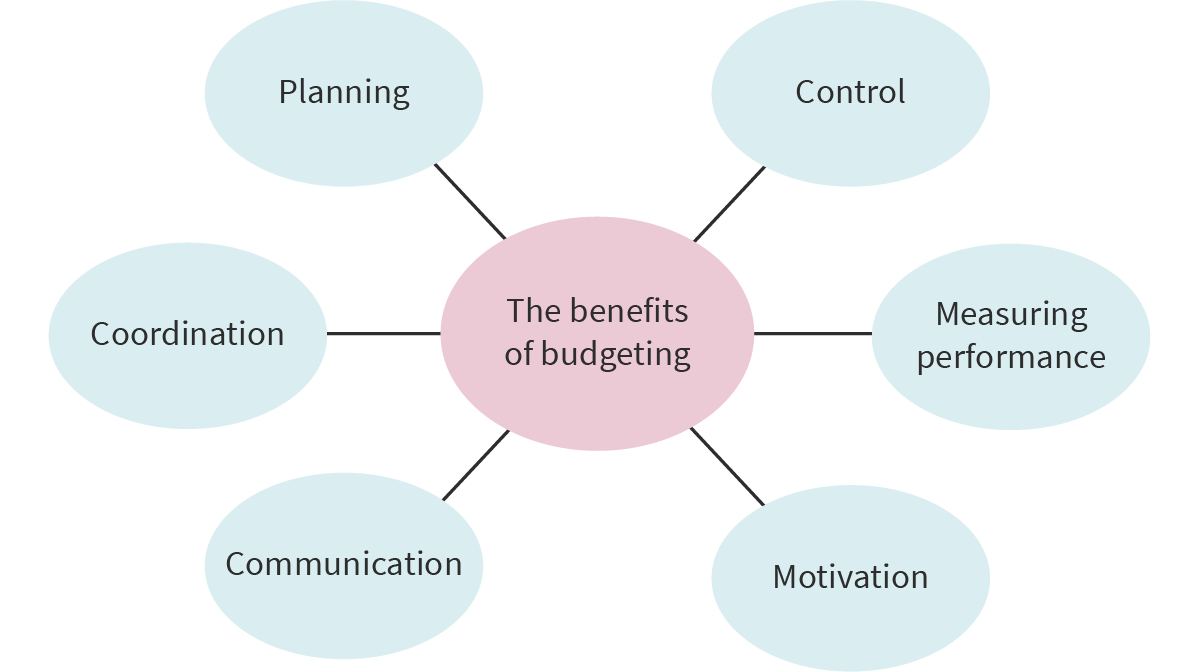

The importance of budgets and variance analysis in decision - making