Econ Unit 3 (Profit, Production, Costs, Markets & Perfect Competition)

1/93

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

94 Terms

marginal utility turns negative

total utility begins to decrease when

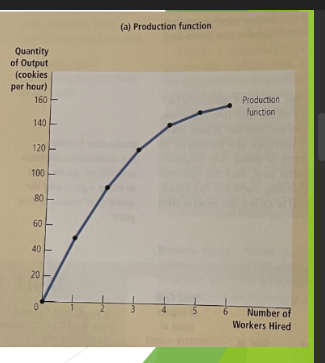

production function

shows the relationship between the quantity of inputs used to make a good and the quantity of output for that good

land, labor, capital, entrepreneurship, sometimes technology

factors of production

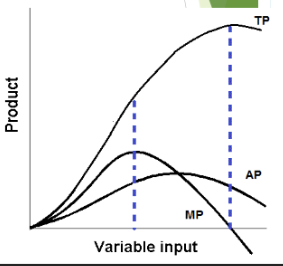

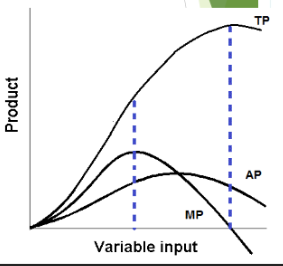

total product

the total amount of final output produced by a firm using given inputs in a given period of time

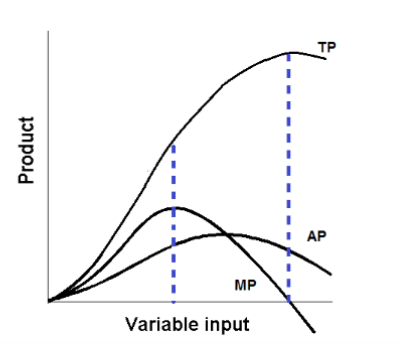

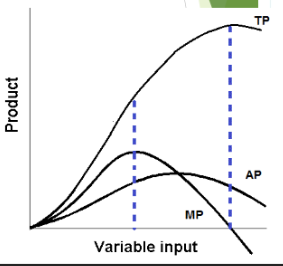

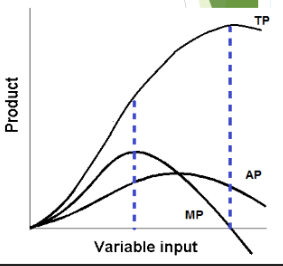

marginal product

increase in the quantity of output that arises from one additional unit of that input (ex: the additional number of strawberries harvested by a farmer who plants additional seeds OR the additional revenue a bowling alley receives if it builds extra lanes)

marginal product = 0

total product is maximized when

MP of capital

the additional output that results from adding one unit of _____ (additional pizza oven)

MP of labor

the additional output resulting from hiring another worker

MP of land

the additional output gained from adding another unit of ____ (a farmer who purchased a field next to their existing property)

MP of raw materials

a rechargeable battery manufacturer who purchased a cache of lithium or cobalt

law of diminishing marginal returns

as you add more of a single input (like labor or capital) to a fixed production process, the resulting increase in output will eventually get smaller. While initial investments usually boost production significantly, you will eventually reach a point where each new unit of input yields less additional "marginal" product, and could eventually lead to a decrease in total output

average product = total product / units of variable factor input

the average of the total product per unit of input

increasing at an increasing rate

if MP is increasing, TP is

decreasing

If MP is negative, TP is

crosses AP curve

the AP is maximized when MP

pulls AP up

when MP is higher than AP, it

pulls AP down

when MP is less than AP, it

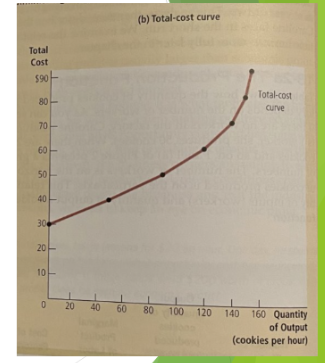

total cost curve

gets steeper as the amount produced rises. when the kitchen is crowded with lots of workers, producing an additional pizza requires a lot of additional labor and is therefore very costly

marginal cost

a representation of the costs incurred when additional units of a product are produced

short-run production costs

the period of time during which at least some factors of production are fixed, labor is typically variable

long-run production costs

the period of time during which all factors are variable, all costs are variable in this time

explicit costs

out-of-pocket costs, payments that are actually made, wages that a firm pays its employees or rent that a firm pays for its office

implicit costs

represent the opportunity cost of using resources already owned by the firm

economic profit

TR-TC, includes both explicit and implicit costs

TR-TC

economic profit

accounting profit

a cash concept, TR-explicit costs = the difference between dollars brought in and dollars paid out

economic profit

even though a business pays income taxes based on its accounting profit, whether or not it is economically successful depends on its ____________

TR - explicit costs

accounting profit

fixed inputs

can’t easily be increased or decreased in a short period of time, fixed inputs define the firm’s maximum output capacity

variable inputs

can easily be increased or decreased in a short period of time

optimal output rule

a business’s profit is maximized when it produces a quantity of output where the marginal revenue = marginal cost

MR = MC

optimal output rule

total cost - fixed cost

variable costs

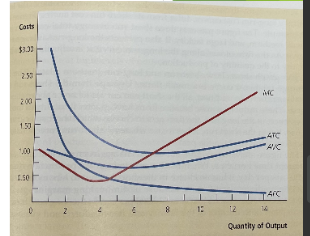

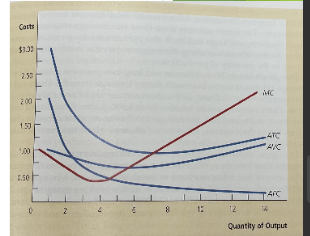

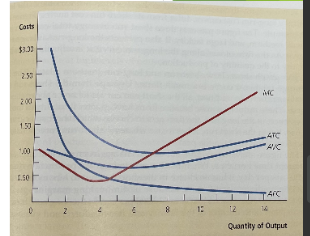

average total cost

the total cost per unit of output, inclusive of both fixed and variable costs, is the per-unit cost of producing a product

total cost / quantity of output

average total cost

average variable cost

the variable cost per unit incurred by a business across a given period

total variable cost / quantity of output

average variable cost

average fixed cost

the fixed costs incurred by a company that remain constant irrespective of output, expressed on a per-unit basis

total fixed cost / production output

average fixed cost

costs fall

when workers are more productive,

diminishing marginal returns

when MC shifts up, this is when the firm is experiencing

ATC decreases

when MC is lower than ATC,

MC and ATC cross

ATC is at its lowest when

ATC rises

When MC is higher than ATC,

marginal cost

there is no relationship between average fixed cost and

downward

average fixed cost always trends

lower fixed cost per unit of output

as production volume increases, the same fixed cost is spread across a larger number of units, resulting in a

quantity increases

total fixed cost does not change as

quantity increases

total variable cost increases as (labor costs go up)

TFC

the gap between TC and TVC is

total fixed costs

TC does not begin at zero because even with no output there are still (rent)

TFC

The TC curve intersects the vertical axis at the level of

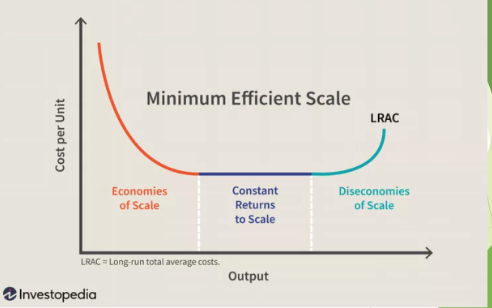

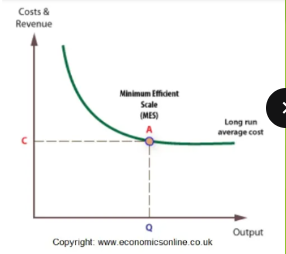

minimum efficient scale

economies of scale

when long-run average total cost declines as a quantity of output increases, happens because higher production levels allows specialization among workers

increasing returns to scale

means that a company increases all its inputs (like labor and capital) by a certain percentage, the resulting output increases by a proportionally larger percentage

lower average costs per unit produced

increasing returns to scale: producing at a larger scale leads to greater efficiency and

constant returns to scale

when long-run average total cost stays the same as the quantity of output changes

diseconomies of scale

when long-run average total cost rises as the quantity of output increases

coordination problems

diseconomies of scale can happen because of

minimum efficient scale

the lowest point on a cost curve at which a company can produce its product at a competitive price, smallest output level at which long-run average total cost is minimized

economies of scale

at the MES point, the company can achieve the ___________ necessary for it to compete effectively in its industry

minimum efficient scale will be

the higher a firm’s fixed costs are, the higher its

long-run average total cost

if a firm is experiencing economies of scale, what will decrease as output increases

market

a group of buyers and sellers of a particular good or service

competitive market

many buyers and sellers, not controlled by any one person or firm, a narrow range of prices are established that buyers and sellers act upon

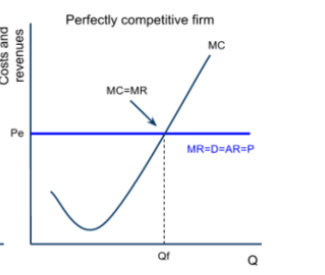

perfect competition

products are the same, numerous buyers and sellers so that each has no influence over price, buyers and sellers are price takers, all firms charge about the same price, free entry into and out of the market

must accept the price for its output

a perfectly competitive firm can sell any number of units at exactly the same price,

quantity to produce

a perfectly competitive firm will determine its total revenue, total costs, and level of profits by deciding the

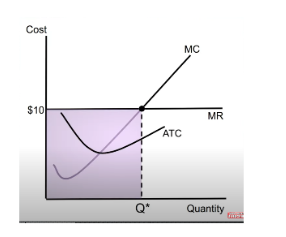

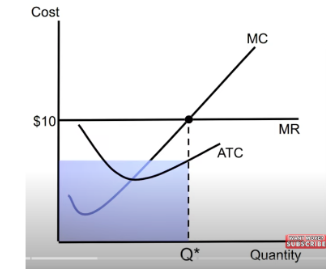

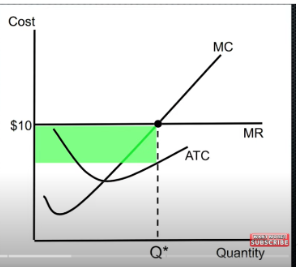

profit = total revenue - total cost

price equation 1

profit = quantity(price-average total cost)

profit equation 2

the supply curve

for a perfectly competitive firm, marginal costs curve is

the demand curve

for a perfectly competitive firm, marginal revenue curve is

a firm produces where MR = MC

profit maximization rule

it can sell however much it wants

why is the firm’s demand curve perfectly elastic

price x quantity

total revenue =

ATC x quantity

total cost =

profit

difference between TR & TC is

short-run shutdown

not producing anything during a specific time period because of market conditions

short-run shutdown

still has to pay fixed costs

short-run shutdown

if a farmer decides to not plant for one season, the fixed cost of land is a sunk cost

short-run shutdown

the farmer should ignore the sunk costs when deciding how much to produce

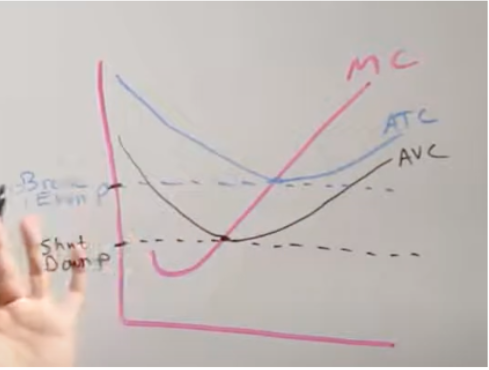

lowest point on ATC, lowest point on AVC

break even point/price = ______________, shut down point/price = ___________

short-run shutdown

loses all revenue from the sale of its product

short-run shutdown

saves the variable costs of making its products

price < AVC

shut down if

P > ATC

if a price is greater than average total cost, then a firm is making economic profits

long-run exit

will save variable AND fixed costs

long-run exit

revenue it would receive from producing is less than total costs

MC = MR

in a short-run market supply with a fixed number of firms, for any given price, each firm supplies a quantity of output so that its

QS

to derive market supply curve, we add the ______ by each firm in the market

the same cost curves

in a long run market supply with entry and exit we will assume all current and potential firms had

profit is positive

if price is above ATC, (encourages new firms to enter)

profit is negative

if price is less than ATC, (encourages some firms to exit)

the quantity produced by each existing firm will decrease

Assume that all firms in a perfectly competitive market currently earn positive economic profits. What will happen in the long run if all firms face constant returns to scale in production