Part-4-1A-Auditing-Computer-Based-IS-Risk-Based-Audit-Approach

1/35

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

36 Terms

The Risk-Based Audit Approach

is a four-step approach to internal control evaluation that provides a logical framework for carrying out an audit.

provides auditors with a clear understanding of the errors and irregularities that can occur and the related risks and exposures.

This understanding provides a basis for developing recommendations to management on how the AIS control system should be improved.

Four steps of Risk-Based Audit Approach

Determine the threats (errors and irregularities) facing the accounting information system

Four steps of Risk-Based Audit Approach

Identify control procedures implemented to minimize each threat by preventing or detecting such errors and irregularities.

Four steps of Risk-Based Audit Approach

Evaluate the control procedures

Four steps of Risk-Based Audit Approach

Evaluate weakness (errors and irregularities not covered by control procedures) to determine their effect on the nature, timing, or extent of auditing procedures and client suggestions.

The Information System Audits

The purpose of an information system audit is to review and evaluate the internal controls that protect the system.

Security provisions protect computer equipment, programs, communications, and data from unauthorized access, modification, or destruction

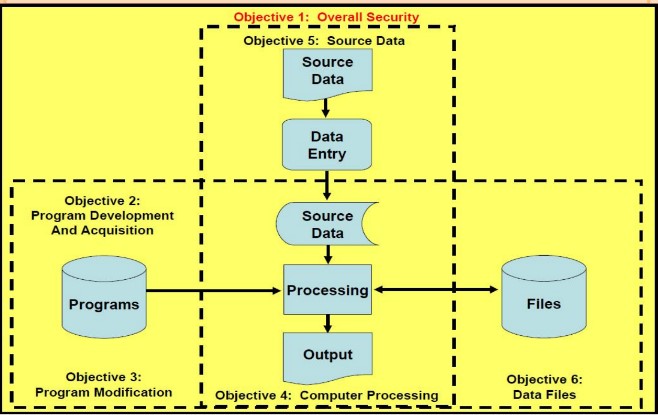

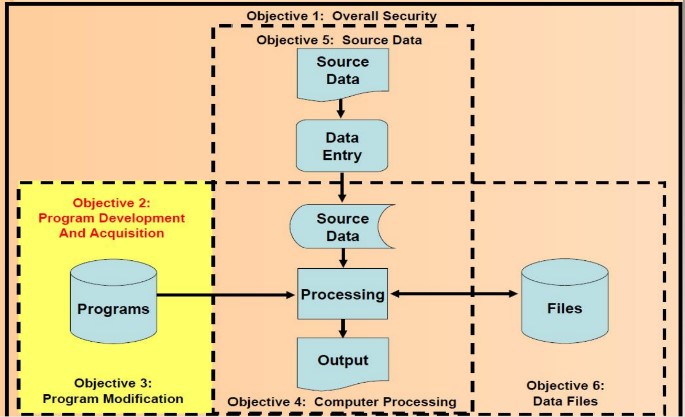

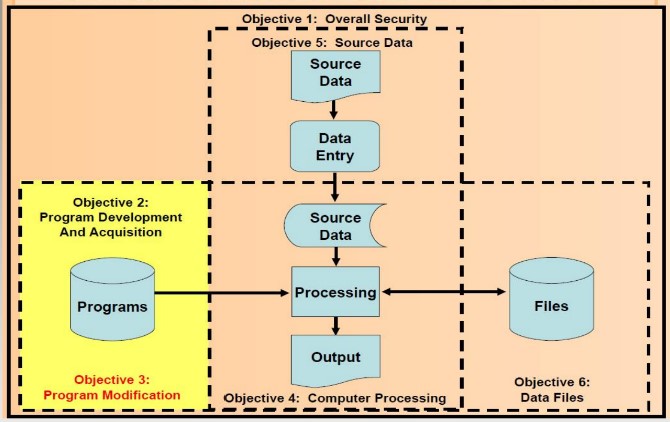

When performing an information system audit, auditors should ascertain that the following objectives are met:

Program development and acquisition are performed in accordance with the management’s general and specific authorization

When performing an information system audit, auditors should ascertain that the following objectives are met:

Program modifications have management’s authorization and approval

When performing an information system audit, auditors should ascertain that the following objectives are met:

Processing of transactions, files, reports, and other computer records is accurate and complete.

When performing an information system audit, auditors should ascertain that the following objectives are met:

Source data that are inaccurate or improperly authorized are identified and handled according to prescribed managerial policies.

When performing an information system audit, auditors should ascertain that the following objectives are met:

Computer data files are accurate, complete and confidential.

When performing an information system audit, auditors should ascertain that the following objectives are met:

Overall Security

Program Development and Acquisition

Program Modification

Computer Processing

Source Data

Data Files

Each description includes an audit plan to accomplish the objective, as well as the techniques and procedures to carry out the plan.

Information System coponents and audit objectives

Accidental or intentional damage to system assets

Unauthorized access, disclosure, or modification of data and programs

Theft.

Interruption of crucial business activities.

OBJECTIVE 1: OVERALL SECURITY

Types of security errors and fraud faced by companies:

OBJECTIVE 1: OVERALL SECURITY

Control procedures to minimize security errors and fraud

Inspecting computer sites.

Interviewing personnel.

Reviewing policies and procedures.

Examining access logs, insurance policies, and the disaster recovery plan.

OBJECTIVE 1: OVERALL SECURITY

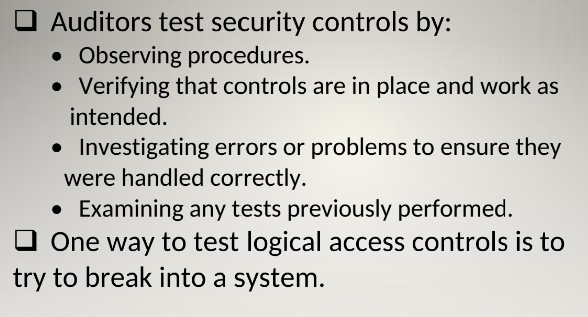

Audit Procedures: Systems Review

OBJECTIVE 1: OVERALL SECURITY

Audit Procedures: Tests of Controls

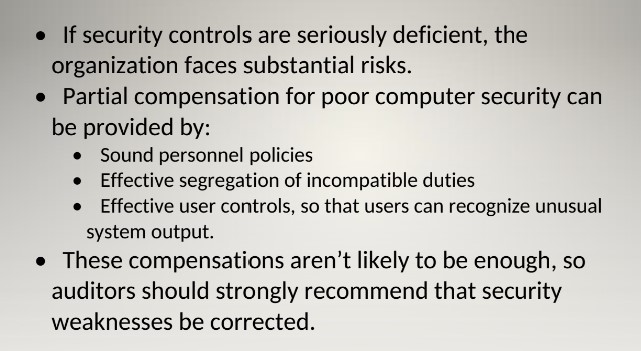

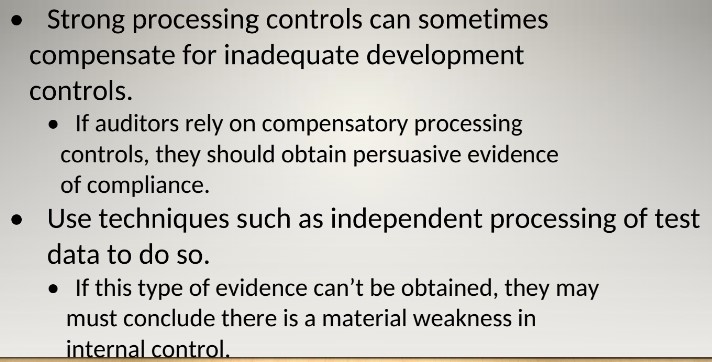

OBJECTIVE 1: OVERALL SECURITY

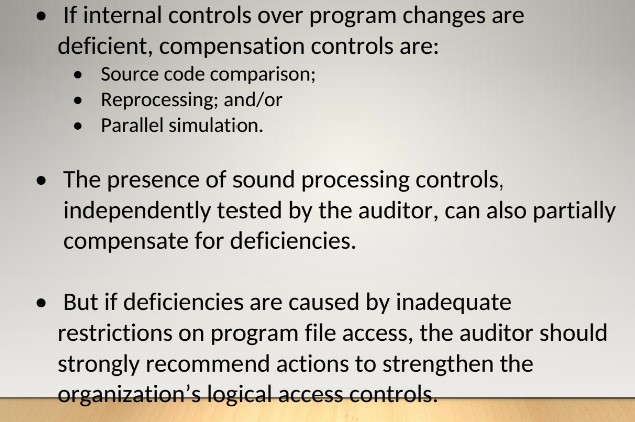

Compensating Controls

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Two things can go wrong in program development:

Inadvertent errors due to careless programming or misunderstanding specifications; or

Deliberate insertion of unauthorized instructions into the programs.

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Types of errors and fraud:

The preceding problems can be controlled by requiring:

Management and user authorization and approval

Thorough testing

Proper documentation

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Control procedures:

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Audit Procedures: Systems Review

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Audit Procedures: Tests of Controls

OBJECTIVE 2: PROGRAM DEVELOPMENT AND ACQUISITION

Compensating Controls

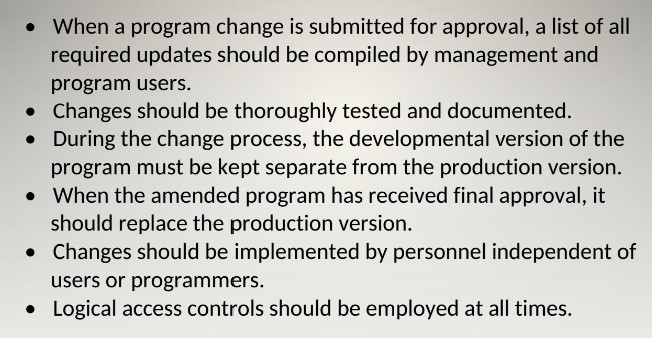

OBJECTIVE 3: PROGRAM MODIFICATION

OBJECTIVE 3 : PROGRAM MODIFICATION

Types of Errors and Fraud

Same that can occur during program development:

Inadvertent programming errors

Unauthorized programming code

OBJECTIVE 3 : PROGRAM MODIFICATION

Control Procedures

OBJECTIVE 3 : PROGRAM MODIFICATION

Audit Procedures: System Review

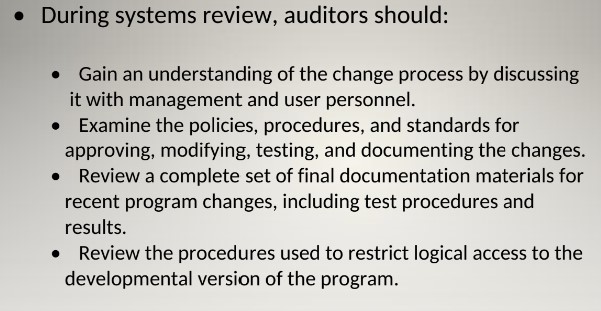

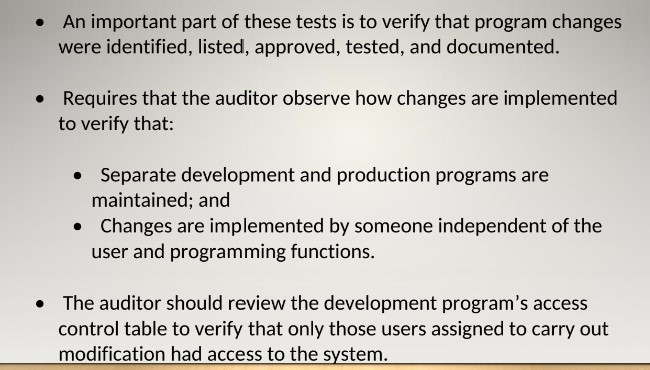

OBJECTIVE 3 : PROGRAM MODIFICATION

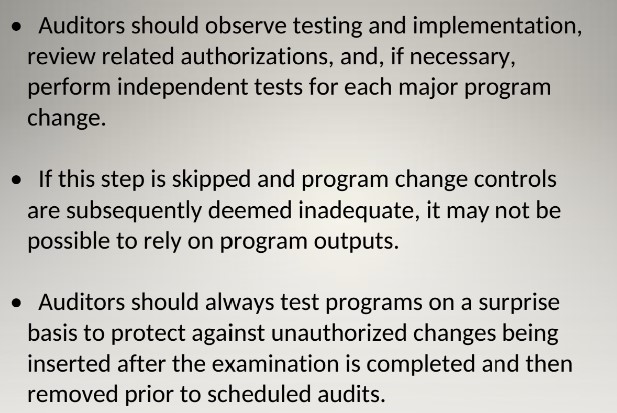

Audit Procedures: Tests of Controls

OBJECTIVE 3 : PROGRAM MODIFICATION

Audit Procedures: Tests of Controls

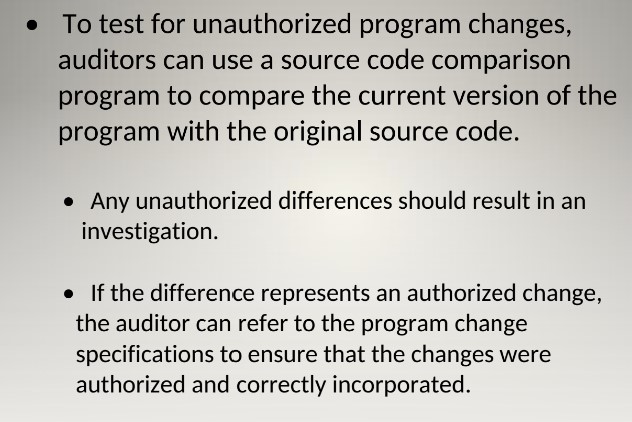

Reprocessing and Parallel simulation

Two additional techniques detect unauthorized program changes:

Reprocessing

On a surprise basis, the auditor uses a verified copy of the source code to reprocess data and compare that output with the company’s data.

Discrepancies are investigated.

Parallel simulation

Like reprocessing except that the auditor writes his own program instead of using verified source code.

Can be used to test a program during the implementation process.

OBJECTIVE 3 : PROGRAM MODIFICATION

Audit Procedures: Tests of Controls

OBJECTIVE 3 : PROGRAM MODIFICATION

Compensating Controls