ECO 202 Module 3: Interaction of Supply and Demand

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

perfectly competitive market (model)

market with:

many buyers and sellers

all firms selling identical products

no barriers to new firms entering the market

market demand

the demand by all consumers of a given good or service

demand schedule

table that shows the relationship between the price of a product and the quantity of the product demanded

demand curve

a curve that shows the relationship between the price of a product and the quantity of the product demanded

affected by factors other than price

quantity demanded

amount of a good or service that a consumer is willing and able to purchase at a given price

affected by changes in price

law of demand

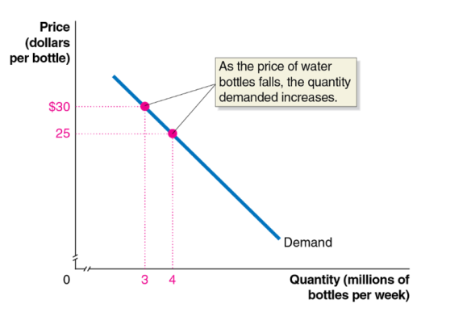

a rule that states, holding everything else constant, when the price of a product falls, the quantity demanded of the product will increase, and when the price of a product rises, the quantity demanded of the product will decrease

when the price of a good falls…

1) consumers substitute toward the good whose price has fallen

2) consumers have more purchasing power, which is like an increase in income

substitution effect

the change in the quantity demanded of a good that results from a change in price, making the good more or less expensive relative to other goods, holidng constant the effect of the price change on consumer purchasing power

income effect

the change in the quantity demanded of a good that results from the change in the good’s price on a consumer’s purchasing power, holding all other factors constant

purchasing power

the quantity of goods a consumer can buy with a fixed amount of income

ceteris paribus (“all else equal'“) condition

the requirement that when analyzing the relationship between two variables - such as price and quanitity demanded - other variables must be held constant

shifting the demand curve

a change in something other than price that affects demand causes the entire demand curve to shift

shift to the right is an increase in demand, shift to the left is a decrease in demand

when the demand curve shifts, quantity demanded will change, even if the price doesn’t change

quantity demanded changes at every possible price

variables that shift market demand

income: an increase in income increases demand if the product is normal, and decreases demand if the product is inferior

prices of related goods: an increase in the price of related goods increases demand if products are substitutes, and decreases demand if products are complements

tastes

population and demographics

expected future prices

natural disasters and pandemics

normal good

a good for which the demand increases as income rises and decreases as income falls

ex) new clothes, resaurant meals, vacations

inferior good

a good for which the demand increases as income falls and decreases as income rises

ex) second-hand clothes, instant noodles

substitutes

goods and services that can be used for the same purpose

ex) Big Mac and Whopper, Ford F150 and Dodge Ram, reusable water bottles and bottle spring water

complements

goods and services that are used together

ex) Big Mac and McDonald’s fries, left shoes and right shoes, resuable water bottles and gym memberships

changes in tastes

if consumers’ tastes change, they may buy more or less of the product

ex) influencers successfully advertise reusable water bottles, changing tastes, and increasing demand

changes in demographics

demographics are the characteristics of a population with respect to age, race, and gender

ex) an increase in the elderly population increases the demand for medical care

changes in expectations about future prices

consumers decide which products to buy and when to buy them

future products are substitutes for current products

an expected increase in the price tomorrow increases demand today

an expected decrease in the price tomorrow decreases demand today

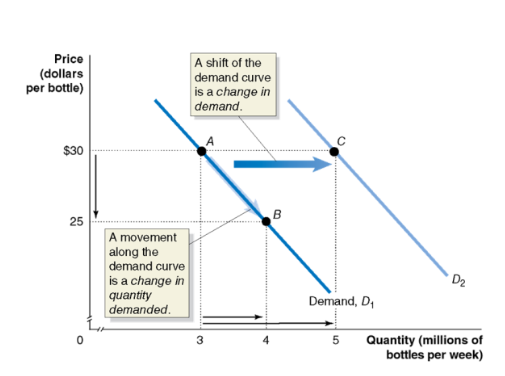

change in demand vs change in quantity demanded

a change in the price of the product being examined causes a movement along the demand curve — this is a change in quantity demanded

any other change affecting demand causes the entire demand curve to shift — this is a change in demand

market supply

the decisions of (generally) firms about how much of a product to provide at various prices

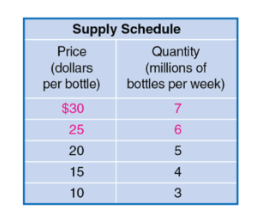

supply schedule

a table that shows the relationship between the price of a product and the quantity of a product supplied

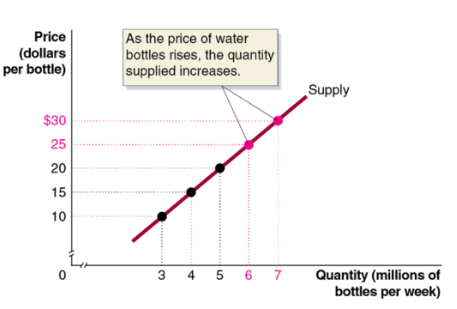

supply curve

a curve that shows the relationship between the price of a product and the quantity of a product supplied

quantity supplied

the amount of a good or service that a firm is willing and able to supply at a given price

law of supply

a rule that states that, holding everything else constant, increases in price cause increases in the quantity supplied, and decreases in price cause decreases in the quantity supplied

shifting the supply curve

a change in something other than price that affects supply causes the entire supply curve to shift

a shift to the right is an increase in supply and a shift to the left is a decrease in supply

as the supply curve shifts, the quantity supplied will change, even if the price doesn’t change

the quantity supplied changes at every possible price

variable that shift market supply

price of inputs

technological change

prices of related goods in production

number of firms in the market

expected future prices

natural disasters and pandemics

inputs

anything used in the production of a good or service

an increase in the price of an input decreases the profitability of selling the good, causing a decrease in supply

a decrease in the price of an input increases the profitability of selling the good, causing an increase in supply

technological change

positive or negative change in the ability of a firm to produce a given level of output with a given quantity of inputs

a new, more efficient way of producing water bottles would increase their supply

governmental restrictions on how much workers are allowed to work might decrease the supply of water bottles

prices of related goods in production

many firms can produce and sell alternative products: substitutes in productions

ex) farmer can plant either corn or soybeans. if the price of soybeans rises, that farmer will plant (supply) less corn

sometimes two products are necessarily produced together: complements in production

ex) cattle provide both beef and leather. an increase in the price of beef encourages cattle farming, which increases the supply of leather

number of firms and expected future prices

more firms in the market will result in more products available at a given price (greater supply). fewer firms mean supply decreases

if a firm anticipates that the price of its product will be higher in the future, it might decrease its supply today in order to increase it later

change in supply vs change in quantity supplied

a change in the price of the product being examined causes movement along the supply curve — this is a change in quantity supplied

any other change affecting supply causes the entire supply curve to shift — this is a change in supply

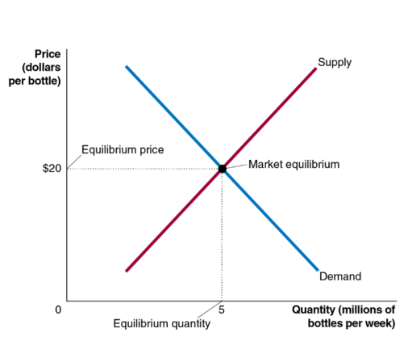

market equilibrium

situation in which quantity demanded equals quantity supplied

at a price of $20, consumers want to buy 5 million water bottles per week and producers want to sell 5 million water bottles per week

equilibrium price is $20 and equilibrium quantity is 5 million, we do not expect the price to change

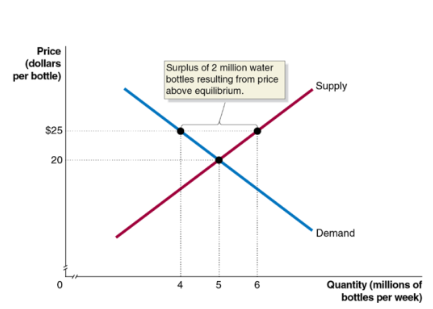

surplus

a situation where quantity supplied is greater than quantity demanded

at a price of $25, consumers want to buy 4 million water bottls and producers want to sell 6 million water bottles

this gives us a surplus of 2 million water bottles

prediction: sellers will compete among themselves, driving the price down

shortage

a situation in which the quantity demanded is greater than the quantity supplied

at a price of $10, consumers want to buy 7 million water bottles and producers want to sell 3 million

this gives us a shortage of 4 million water bottles

prediction: sellers will realize they can increase the price and still sell as many water bottles, so the price will rise

demand and supply both count

price is determined by the interaction of buyers and sellers

neither group can dictate price in a competitive market

however, changes in supply and/or demand will affect the price and quantity traded

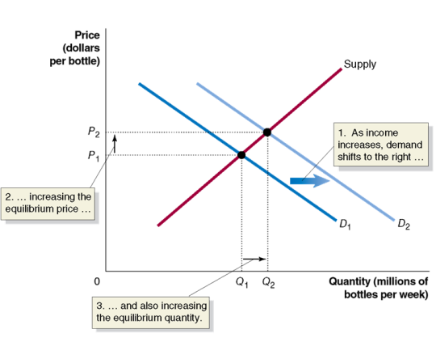

effect of an increase in demand on equilibrium

suppose income increases, water bottles are a normal good, so as income rises:

demand shifs to the right

equilibrium price rises

equilibrium quantity rises

effect of an increase in supply on equilbirum

suppose a new producer enters the market, so more water bottles can be supplied at any given price

supply increases - shifts to the right

equilibrium price falls

equilibrium quantity rises

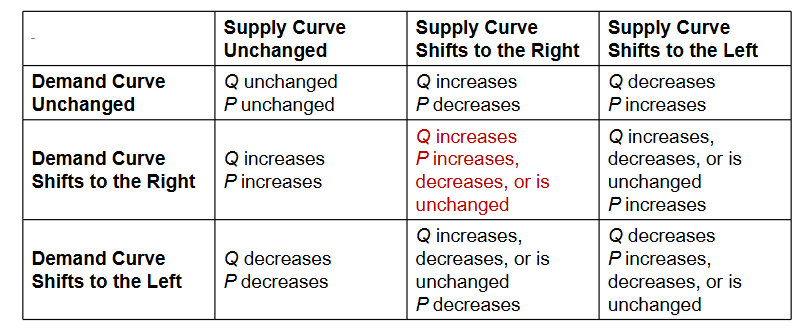

how shifts in demand and supply affect equilibirum price and quantity

when both curves move, we need to know the relative size of the changes to know the effects on equilibirum price and quantity