accounting midterm #2

1/190

Earn XP

Description and Tags

sessions 8-16

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

191 Terms

start of session 8 information - statement of cashflows

wonderful

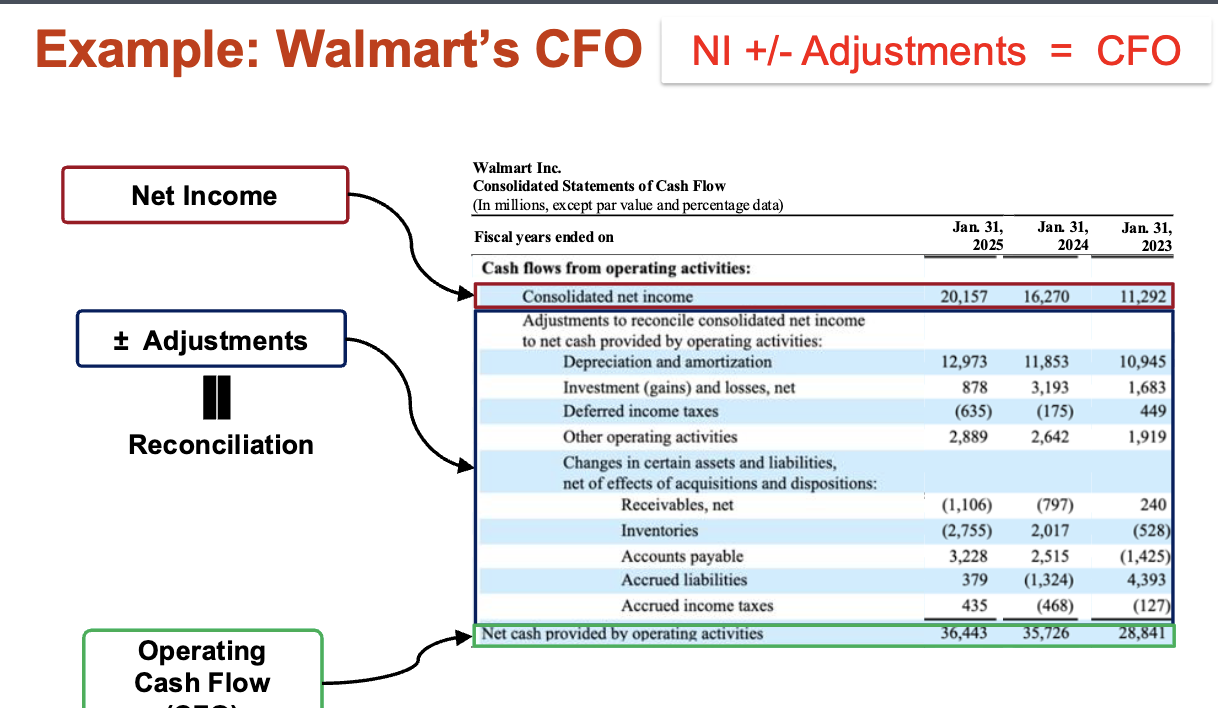

what is CFO

cash flow from operating activities

how to figure out CFO

2 methods: direct and indirect

indirect method for CFO (how to and benefits)

start with net income (which comes from income statement)

makes adjustments to figure out CFO

helps users see why NI is different from operating cash flow (because of those adjustments that are made).

example of CFO using indirect method

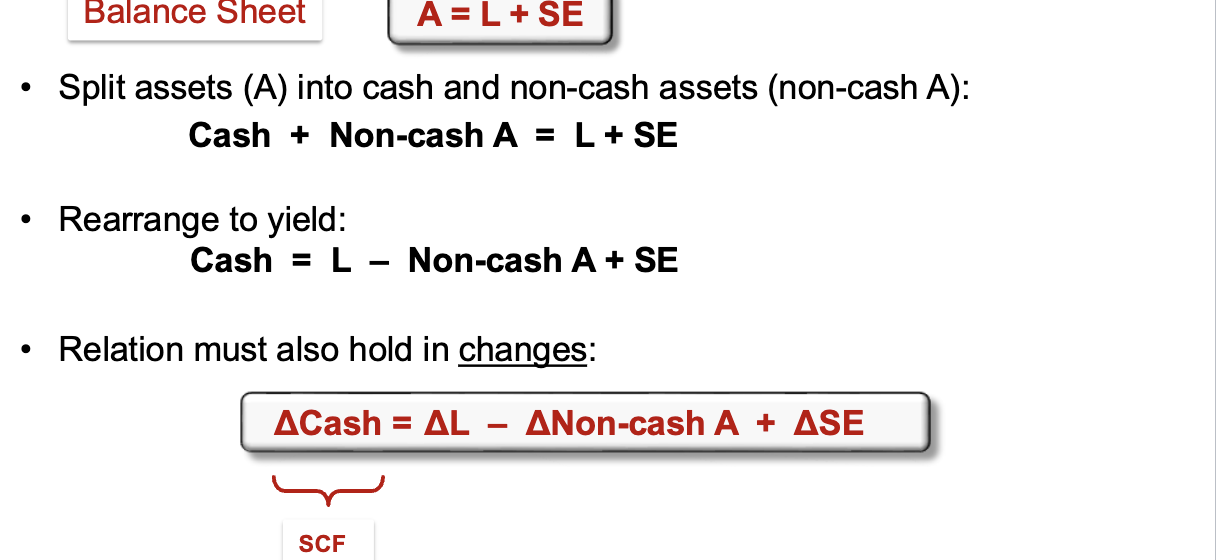

link between balance sheet and SCF - logic

(from IB memory):

the SCF shows the change in cash, and that number is included in the assets section of the B/S

link between balance sheet and SCF - equation

change in cash = change in liability - change in non cash assets + change in SE

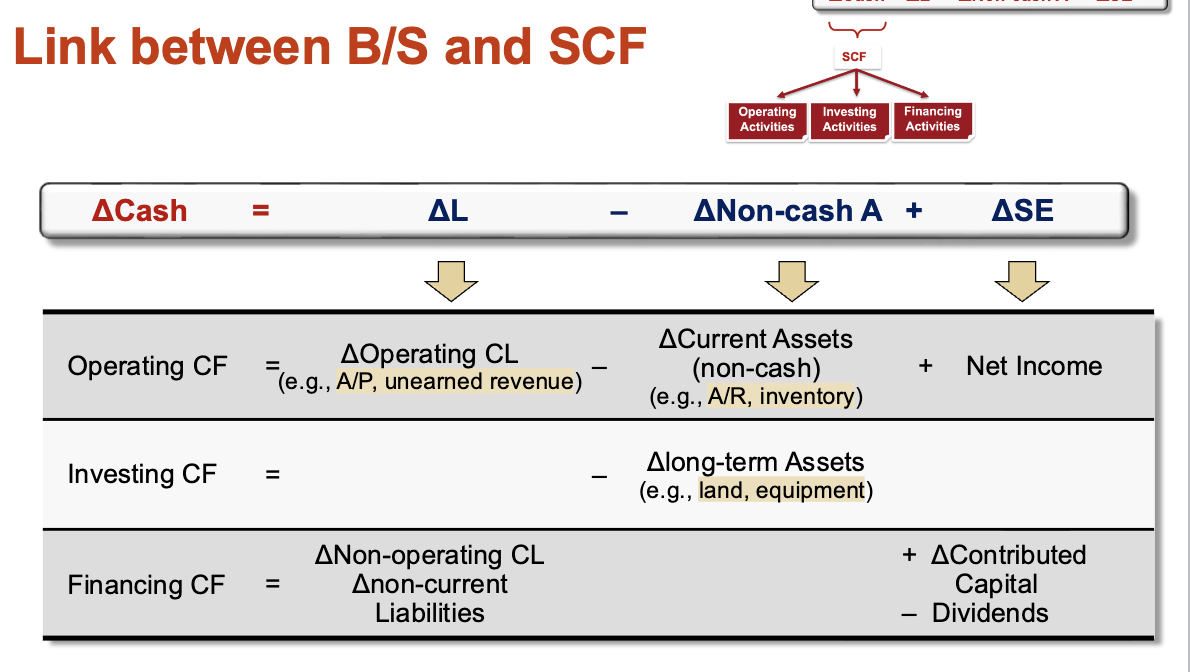

what is the financial statment that’s split into three sections

SCF (operating, financing and investingt)

what does operating cash flow consist of

change in Operating Current Liabilities - Current Non Cash Assets + Net Income

examples of change in operating current liabilities

A/P, unearned rev

examples of change in change in current non cash assets

A/R, inventory

investing cash flow involvs

Change in Liabilities - change in Long-term Assets + change in SE

what does Financing CF consist of

Change in Non operating CL and Non current Liabilities - Change ing Noncash Assets + Change in SE

connection to B/s from SCF table

is net income purely operating related?

NO. it includes:

core operating activities income

expenses and income from non-operating activities, taxes and interest

Operating Income (Operating Profit/EBIT): Measures profit strictly from core business activities (selling goods/services) after deducting operating expenses like rent, payroll, and COGS. It ignores how a company is financed or its tax burden.

Net Income (Bottom Line): Takes the operating income and further adjusts it for non-operational items, interest, and taxes.

is net income purely cash-based?

no. why? it includes

non cash expenses

non operating gains and losses

examples of

non cash expenses

non operating gains and losses

Non-cash expense (e.g., depreciation — reduce NI but do not reduce cash)

• Non-operating gains/losses (e.g., gain on sale of PP&E — included in NI but related to CFI

operating income vs net income

Operating Income (Operating Profit/EBIT): Measures profit strictly from core business activities (selling goods/services) after deducting operating expenses like rent, payroll, and COGS. It ignores how a company is financed or its tax burden.

Net Income (Bottom Line): Takes the operating income and further adjusts it for non-operational items, interest, and taxes.

how to make CFO: indirect method

1) start with net come

2) make adjustments across the three groups

3) sum all adjsutments and calculate the CFO

3 groups of adjustments for CFO’s made with indirect method

1) non cash expenses

2) non operating gains and losses in NI

3) changes in operating working capital

non cash expenses details (for CFO indirect method adjustments)? do you add or deduct

example: depreication expenses

ALWAYS add back depreciation exp

2) non operating gains and losses in NI details? do you add or deduct

exmaples: gains/losses form sale of PPE or long term investments

deduct: non-operating gains

add: non operating losses

3) changes in operating working capital

exmaples: current assest and liabilities

changes in operating assets = inventory, A/R

changes in operating liabilities = A/P, unearned rev

operating cf equation

CFI

cash flow from investing activities

what is the equation of CFI (direct method)

changes in long term assets (land, equipment)

increase vs decrease in long term assets for CFI

increase: purchase = cash outflow

decrease: sale = cash inflow

steps for CFI direct method

list purchase and sale of each long term asset

add them to get CFI

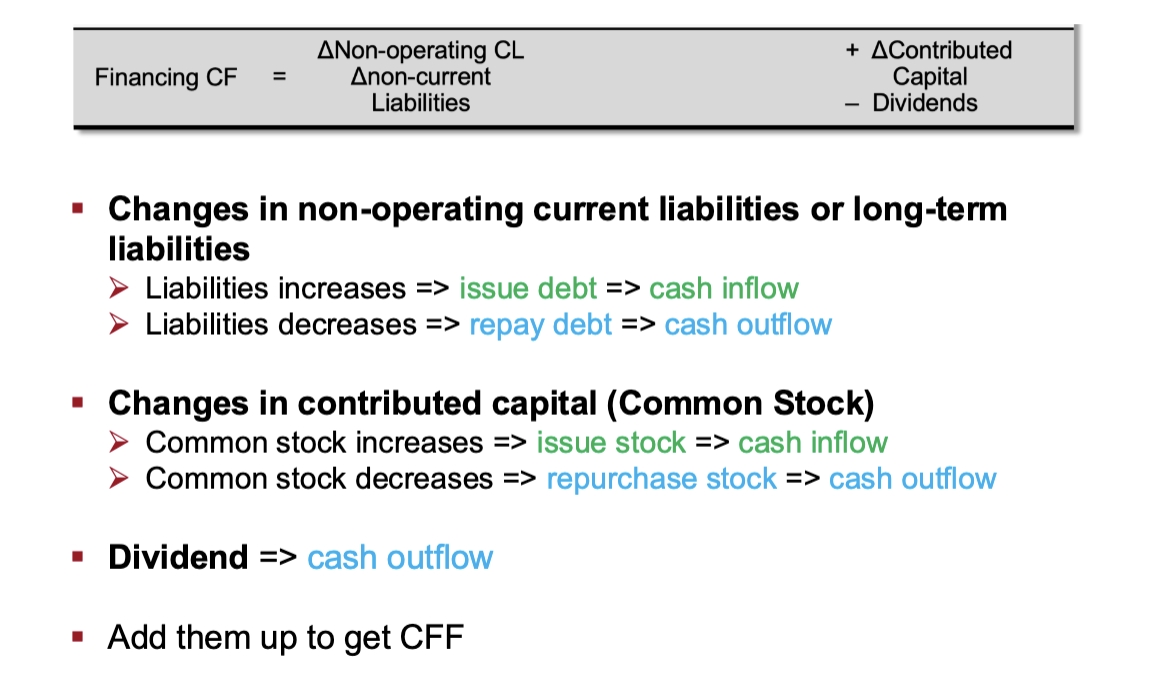

CFF

cash flow for financing activities

euqation for CFF (direct method)

changes in non operating current liabilities or long term liabilities + change in contributed capital - dividends

changes in no operating current liabilities or long term liabilities: increase/decrease

what is contributed capital

common stock!

changes in contributed : increase/decrease for CFF

changes in dividends for CFF: increase/decrease

dividend = cash outflow

how to get CFF

add everything up

end of session 8 / start of session 10

session 10 : prepping SCF using direct/indirect method

goal for session 10 (outside of flashcards)

learn to prep SCF using direct and indirect method, and t-accounts

what does the direct vs indirect method report differeintly for cash flows

The direct method reports actual cash inflows/outflows (e.g., cash from customers, payments to suppliers)

The indirect method reconciles net income to cash flow by adjusting for non-cash items

focus of the direct vs indirect method for Cash Flows

direct = providing high transparency into operational liquidity

indirect =focusing on the quality of earnings

shows the WHYYY of the CFO

more popular for financial analysis

how to find value of dividends

net income - retained earnings = dividends

what must you do with all non-cash expenses

they are always POSITIVE adjustments

operating assets include

changes in:

A/R

Inventory

Prepaid Expense

operating liabilities include

changes in

A/P

Wages Payable

Unearned Rev

why do you deduct the increase in A/R and the increase in Prepaid expenses if they experience an increase over time?

For A/R

remember this is a CFO, so we;re only concerned about the cash. A/R isn’t technically cash, you’re not recieveing cash for anything (at least not yet, so that’s BAD for the CFO). Revenue and NI increases, but not cash. so it’s a deduction.

if you don’t do this, net income is TOO HIGH and it would account for cash that you don;t have

For Prepaid Expenses:

prepaid expenses means that even though the expenses aren’t recorded yet, you still paid CASH for it. so it decreases cash. if not, NET INCOME STAYS TOO HIGH

why do we add the increase in wages payable on the CFO

because the expense has been recorded, but technically you haven’t traded any cash for it yet. if you were to deduct it, the NI would be too low, because you technically still have that cash!

why do we add the increase in unearned revenue on the CFO

because with unearned revenue, you haven’t actually executed any action/service but you still got the cash. so, it makes sense to add it. otherwise, the NI would be too low

what does a NEGATIVE valye for A/R mean on the CFO

that there’s an increase in A/R

what does a POSITIVE valye for A/P mean on the CFO

that there’s an increase in A/P

what else do you have to learn how to do for session 10

reading and analyze the SCF and what it means

use the information to asses financial condition of a corporation

Session 10 SCF a User’s Perpsective to practice

end of session 10 / beginning of session 11 (accounts recieveables)

what are assets ordered in on the b/S

in order of liquidity

what does accrual accounting mean

revenue is recognized before cash is recieved from customers

reasons to extend credit to customers, what is the risk,

boost sales

customers dont always pay their bills

and why analyze A/R

What is the firm’s credit policy?

- Does the firm have a lot of bad debt?

- How efficient is the company in collecting receivables?

what is bad debt

debt that is not going to be payed

Bad debt expense is an operating expense incurred when customer credit accounts become uncollectible, reducing net income.

aka uncollectible accounts

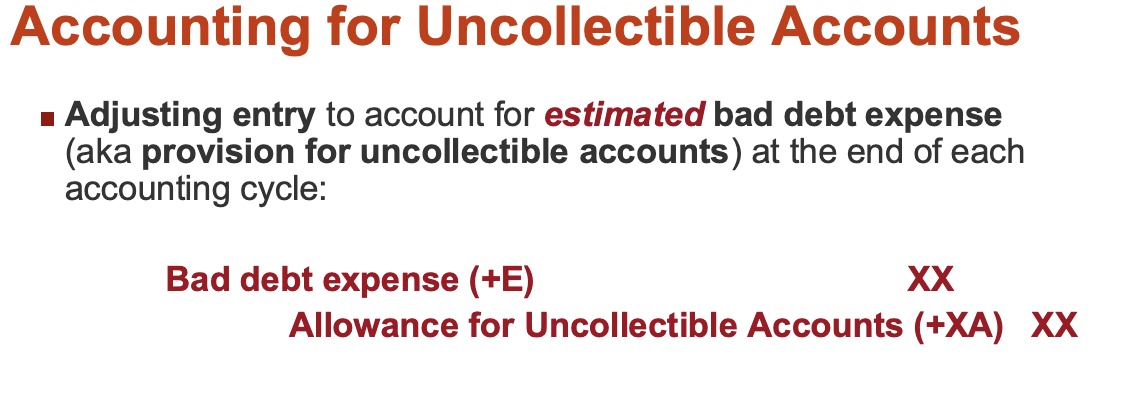

what does GAAP require companies to do due to risk of uncollectibale accounts

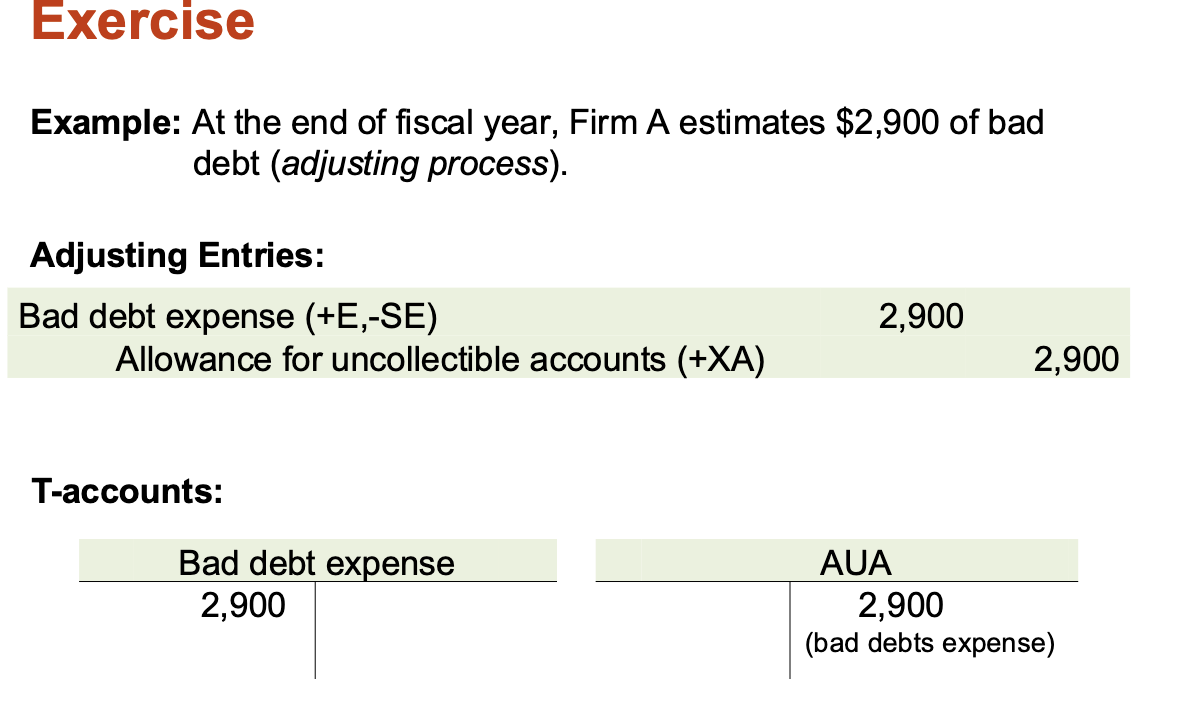

estimate the amount of uncollectible accounts at the end of each accounting cycle (adjusting process)

HOW DO companies estimate the amount of uncollectible accounts at the end of each accounting cycle (adjusting process)

companies anticiapte that some of their credit sales will NOT be collected

they dont wait till the customer fails to pay, they js guess how much it’s gonna be and record it as an expense

matching principal

when companies anticipate their uncollectable accounts/bad debt and they dont wait till the customer fails to pay, they js guess how much it’s gonna be and record it as an expense

what is the adjusting entry for depreciation

Gross Cost of PPE - Accumulated Dep = net PPE

what is established when adjusting for depreciation AND bad debt

a reserve is established

for depreciation it’s contra-asset (X)

for bad debt, it’s…

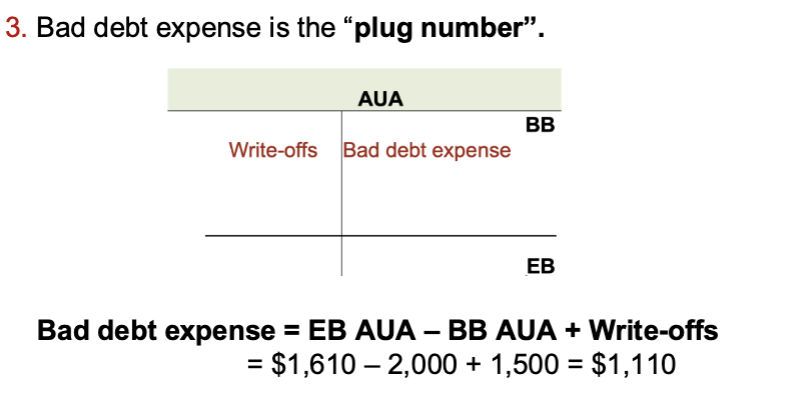

what is the reserve for bad debt

AUA (±XA)

estimated amount of uncollectible recivables

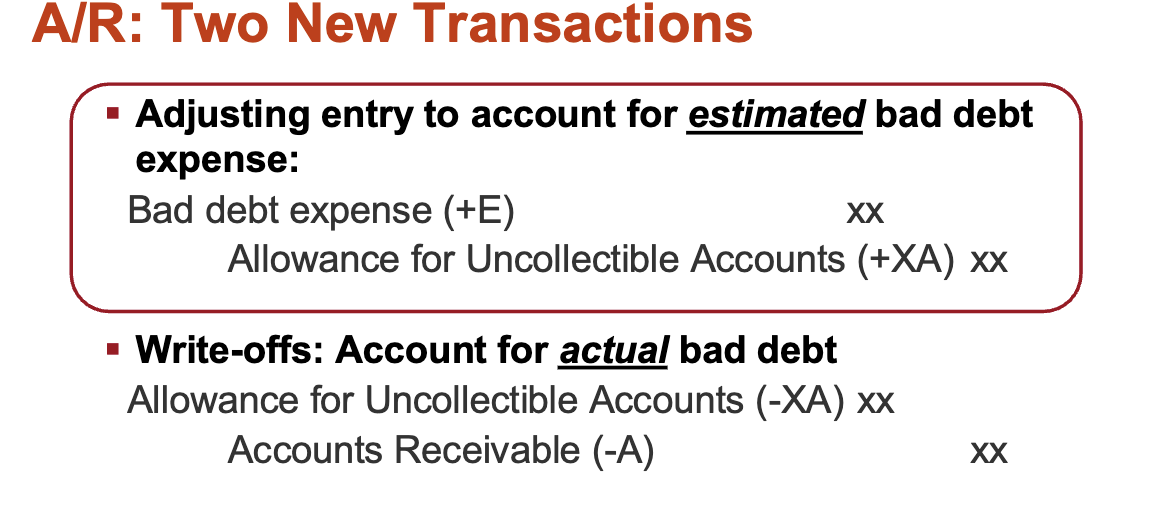

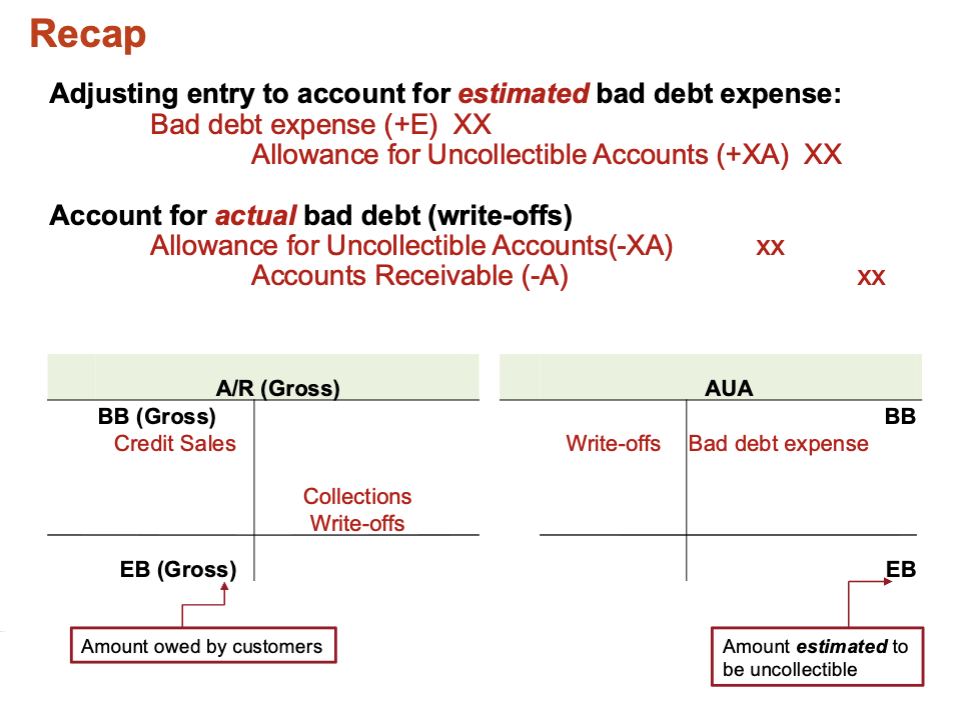

journal entry for bad debt

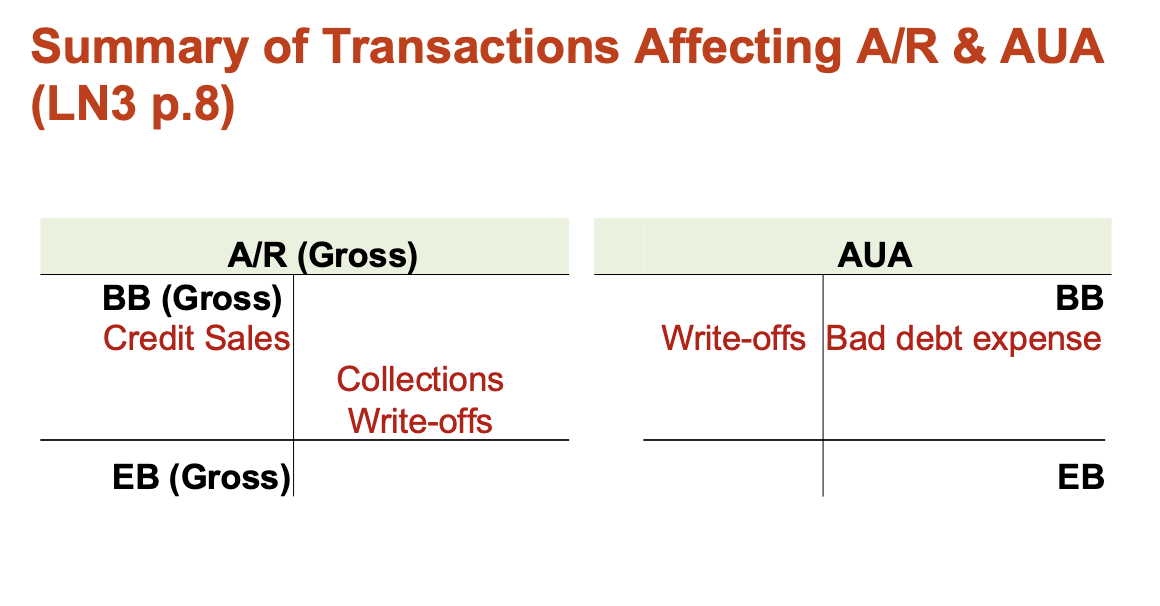

balance sheet stuff for AUA

A/R gross - AUA = A/R net

on balance sheet, what to look out for when it comes to A/R

it’ll say A/R and then “net allowance of $x". that amount = the amount of AUA/bad debt. if you add those, you’ll get gross A/R

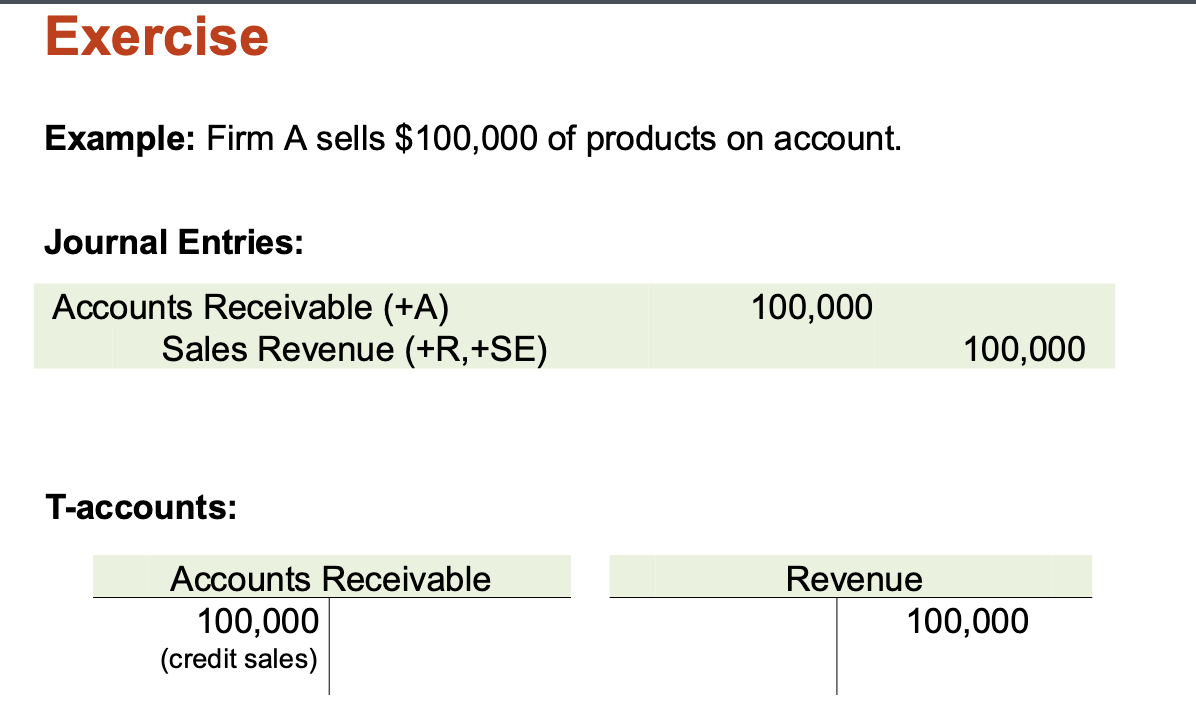

if a company sells products on account, what is the journal entry

A/R(+A) xx

Sales Rev (+R, +SE) xx

what do you make t-accounts for

for EACH account involved in the journal entry

so the entry talks about A/R and Revenue:

journal entry and t-accounts for bad debt for adjusting process

write off

when you remove an amount from A/R and reduce the AUA

why do you write things off

when a specific account is deemed to actually be uncollectible (not just estimating that it is)

write off = the account for actual bad debt

when do write offs happen

When the firm receives notice that one of its customers

declare bankruptcy.

- Companies have specific policies to determine when to

classify an unpaid receivable as uncollectible (in the FOOTNOTES)

journal entry for write-offs

do write offs affect the income statement?

no

The “hit” to earnings already happened earlier when the company estimated bad debt expense.

That estimate reduced net income before

The write-off is just confirming: “yep, this specific customer won’t pay”

👉 So at the time of write-off:

No new expense

No impact on net income

Intuition:

The income statement cares about estimates of losses, not the exact timing of when accounts go bad.

do write off affect net A/R reported on B/S

👉 No, net A/R stays the same.

Why?

A write-off does two things at the same time:

Decreases Accounts Receivable (gross)

Decreases Allowance for Uncollectible Accounts

Same amount.

Example:

Before write-off:

A/R = 1,000

Allowance = (100)

Net A/R = 900

Write off $50:

After write-off:

A/R = 950

Allowance = (50)

Net A/R = 900 ✅ (unchanged)

🧠 Intuition:

You already expected not to collect that money, so removing it doesn’t change the “true” value.

write offs affect on I/S and net A/R

Write-offs do NOT affect net income

→ because expense was already recorded earlierWrite-offs do NOT affect net A/R

→ because both A/R and allowance go down equally

What does affect the income statement?

👉 Bad Debt Expense (the estimate)

That is what:

Reduces net income

Increases the allowance

two accounts affected with write offs

AUA and A/R

two accounts affected with write offs - T ACCOUNTS

adjusting entry to account for ESTIMATED VS ACTUAL bad debt

for ESTIMATED VS ACTUAL bad debt, which one affects net income? how about net A/R

for estimated: You’re anticipating losses, so both income and A/R are adjusted early.

for actual: You’re just using the estimate you already made, not creating a new loss. this ends up NOT AFFECTING ANY OF THE STATEMENTS (according to chat, so double check)

2 ways to estimate AUA

percentage of sales and recievables

percentage of sales

estimate AUA based on a

percentage of total sales

percentage of recivables

estimate AUA based on

a percentage of A/R ending balance

AUA equation to memorize

EB AUA = BB AUA + Bad Debt Exp - Write Offs

percentage of recievables steps

get ending balance of gross A/R (add the bad debt and the net income)

estimate how muhc of gross A/R would be collectiable (you’re typically given a percentage). multiply this percentage by the gross A/R

step two yeilds the ending balance of AUA

use the equation and use bad debt exp as the “plug number” (EB AUA = BB AUA + Bad Debt Exp - Write Offs)

percentage of recievables method: other name

BALANCE SHEET METHOD (not confusing at all!)

actual vs estimated bad debt recap slide

end of session 11/ start of session 12 (still about A/R)

yep

more detailed way of percentage of receivables

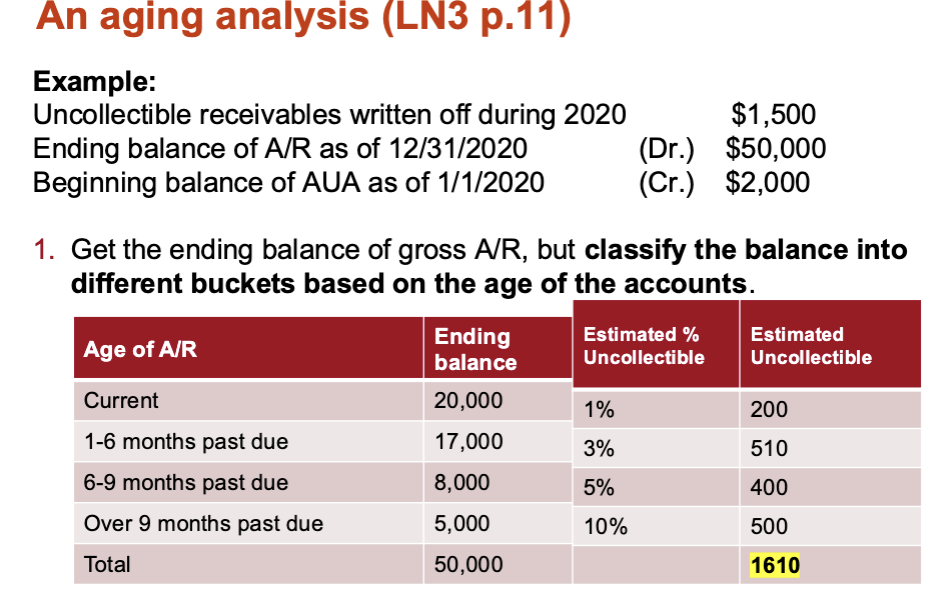

an aging analysis

you’re given all the percntages

what does aging analysis do/ how are recivables classified

receivables are classified based

on age

for aging analysis, what is each balance multipled by?

and each balance is multiplied by its

estimated uncollectible percentage.

what is the total amount of each balance with aging analysis

it is the ending balance for the AUA

step 1 of aging analysis

Get the ending balance of gross A/R, but classify the balance into

different buckets based on the age of the accounts.

step 2 of aging analysis

Estimate the % of uncollectible in each bucket.

Sum of estimated amount of uncollectible accounts for all buckets =

Ending balance of AUA

steo 3 of aging analysis

plug number!

negative reserve example

debt ending balance for AUA

what is a negative reserve

a large amount of unexpected write-offs (i.e.,underestimated bad debt expense last year)

are negative reserves allowed

no, not by GAAP

how to avoid negative reserve and why this works

increase provision (i.e., bad debt expense) in the current year

why:

negative reserve = underestimated bad debt = did not set aside enough

bad debt expense = the provision

increase in provisions because If the reserve is negative, it needs to be brought back up

The only way to increase it is to record more Bad Debt Expense now

negative reserve, its fix and why

Negative reserve = not enough expense recorded before →

Fix = record more expense now to rebuild the allowance

Increase provision because it directly increases ____ and corrects the ____

Increase provision because it directly increases the allowance (THE AUA) and corrects the shortfall