CFA Volume 2 (Financial Statement Analysis)

1/424

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

425 Terms

Central focus of financial analysis

Evaluating the company's ability to:

1) Earn a return on its capital that is at least equal to the cost of that capital

2) To profitably grow its operations

3) To generate enough cash to meet obligations and pursue opportunities

Primary role of Financial Statement Analysis

Use financial reports prepared by companies to evaluate their past, current, and potential performance and financial position for the purpose of making investment, credit, and economic decisions.

Role of equity analyst

Evaluate potential investments in a company's securities as a basis for deciding whether a prospective investment is attractive.

Steps of Financial Statement Analysis

1) State the objective and context

2) Gather data

3) Process the data

4) Analyze and interpret the data

5) Report the conclusions or recommendations

6) Update the analysis

Data Processing Stage of FSA

Make any appropriate adjustments to the statements, calculate ratios, and prepare exhibits such as graphs and common-size balance sheets.

Financial Reporting

The role of financial reporting is to provide information about the performance of a company, its financial position, and changes in financial position that is useful to a wide range of users in making economic decisions.

Follow-Up Phase of FSA

Involves gathering information and repeating the analysis to determine whether it is necessary to update reports and recommendations.

IFRS is developed by

The International Accounting Standards Board (IASB)

IFRS Definition of Income

Increases in economic benefits from increases in assets, enhancement of assets, and decreases in liabilities.

Analyze and Interpret Stage of FSA

Use the data to answer the questions stated in the first step. Decide what conclusions or recommendations the information supports.

Role of credit analyst

Evaluate the creditworthiness of a company to decide whether (and on what terms) a debt investment should be made or what credit ratings should be assigned.

Accruals Concept

1) Revenue is recorded when earned, not when customer pays

2) Expenses are recorded on the income statement in the same period that related revenues are earned ("matching")

3) Expenses not directly tied to revenues should be reported on the income statement in the same period as their use

4) Impacts the balance sheet and income statement, not statement of cash flows

Examples: goods sold on credit = accounts receivables, PP&E and intangibles recorded in B/S and expensed to I/S to match against revenues

Components of Assets

1) Noncurrent Assets

2) Current Assets

IFRS recommends that management commentary addresses:

Key relationships, resources, and risks, as well as the nature of the business, management's objectives, the company's past performance, and the performance measures used.

Components of Liabilities

1) Noncurrent Liabilities

2) Current Liabilities

Components of Equity

1) Contributed Capital

2) Accumulative Other Comprehensive Income

3) Retained Earnings

Income Statement

Also known as Profit and Loss Statement, Statement of Operations, Statement of Earnings.

Dynamic: spans the period between balance sheets.

Shows performance.

Resets to 0 at beginning of each year, with period always between the B/S dates.

Statement of Other Comprehensive Income

Reflects total gains/losses for shareholders. The items in OCI reflect changes in the company’s equity that are not considered to be profit or loss.

Total Comprehensive Income = Net Income + Other Comprehensive Income

Cash Flow Statement

Covers the same time period as the income statement.

Reconciles the change in balance sheet cash (how much the company generated and spent).

Made up of CFO, CFI, and CFF.

Components of Statement of Stockholders' Equity

1) Preferred Stock

2) Common Stock

3) Additional Paid-In Capital

4) Retained Earnings

5) Treasury Stock

6) Accumulative OCI

7) Noncontrolling Interest

Taxable Income (Calculation)

Tax Payable + Deferred Tax Liabilities - Deferred Tax Assets

Components of Standard Auditor's Opinion

1) Responsibility of management to prepare accounts; independence of auditors

2) Properly prepared in accordance with relevant GAAP; reasonable assurance that the statements are free from material misstatement

3) Accounting principles and estimates chosen are reasonable

Under US GAAP, the auditor is required to state an opinion on the company's internal controls under the Sarbanes-Oxley Act.

US GAAP is based on _______________, while IFRS is based on _____________.

Rules, Principles

Internal Controls

Directly affect the firm's financial reporting quality. Weak internal controls provide an opportunity for low-quality or even fraudulent financial reporting.

Long-Term Contracts

When products are delivered over the course of multiple years.

IFRS Requirements for classification:

1) customer receives and benefits from product delivery (immediate use), or

2) assets have no alternative use

Revenue Calculation for Long-Term Contracts

= Contracted Selling Price x (Cost to Date / Estimated Total)

Potentially Dilutive Securities

1) Stock Options

2) Warrants

3) Convertible Debt

4) Convertible Preferred Stock

Dilutive securities decrease EPS if exercised or converted to common stock.

Antidilutive securities increase EPS if exercised or converted to common stock.

International Organization of Securities Commissions (IOSCO)

Regulates significant portion of the world's financial capital markets and assists in attaining the goal of uniform regulation as well as cross-border cooperation in combating violations of securities and derivatives laws.

Three core objectives of securities regulation:

1) Protecting investors

2) Ensuring that markets are fair, efficient, and transparent

3) Reducing systemic risk

Securities Exchange Act of 1934

A federal law dealing with securities regulation that established the Securities and Exchange Commission to regulate and oversee the securities industry.

Securities Act of 1933

The first major federal law regulating the securities industry. It requires firms issuing new stock in a public offering to file a registration statement with the SEC.

Today, this is 10-K (annual report) and 10-Q (quarterly report).

Sarbanes-Oxley Act of 2002

Created the Public Company Accounting Oversight Board (PCAOB) to oversee auditors - addresses auditor independence, strengthens corporate responsibility for financial reports, and requires management to report on the effectiveness of the company's internal control over financial reporting (including obtaining external auditor confirmation of the effectiveness of internal control).

Operating Segment

10%+ of the combined operating segment's revenue, assets, or profits. And defined as a component of a company that:

1) Engages in activities that may generate revenue and create expenses

2) Whose results are regularly reviewed by the company's senior management

2) For which discrete financial information is available

Management Commentary or Management's Discussion and Analysis (MD&A)

In the US, the SEC requires listed companies to provide an MD&A and specifies the content. Management must highlight any favorable or unfavorable trends and identify significant events and uncertainties that affect the company's liquidity, capital resources, and results of operations.

Audit Report

Provides a basis for the independent auditor to express an opinion on whether the information in the audited financial statements presents fairly the financial position, performance, and cash flows of the company in accordance with a specified set of accounting standards.

Investors analyze income statements to evaluate

A company's growth, profitability, and risks, and often use income statement figures in valuation.

Unearned Revenue (or Deferred Revenue)

If a company receives cash in advance but delivers the product or service later, the company would record a liability when the cash is initially received.

Three common expense recognition models

1) The matching principle (a company recognizes expenses (e.g., COGS) when associates revenues are recognized, and thus, expenses and revenues are matched)

2) Expensing as incurred

3) Capitalization with subsequent depreciation or amortization

Period Costs

Expenditures that less directly match revenues — are generally expensed as incurred (either when the company makes the expenditure in cash or incurs the liability to pay).

Identifiable Intangible Assets

Nonmonetary assets that lack physical substance, which can be acquired separately.

Nonoperating Expenses

= Operating Profit - Pretax Profit

Depreciation and amortization are ____________ expenses, and therefore apart from their effect on taxable income and taxes payable, they have no impact on the __________________ statement.

Non-cash, cash flow statement

Interest Coverage Ratios

Solvency indicators measuring the extent to which a company's earnings (or cash flow) in a period covered its interest costs. Entire amount of interest expenditure, both capitalized portion and expensed portion, should be used to calculate these ratios.

Maintaining a minimum interest coverage ratio is a common financial covenant in lending agreements.

Key difference between capitalized and expensed interest

Capitalized interest appears as part of investing cash outflows, whereas expensed interest reduces operating or financing cash flow under IFRS and operating cash flow under US GAAP.

Accounting standards for internal development costs

Companies must capitalize costs after a product's feasibility is established (e.g., software development costs).

Objective of Common-Size Analaysis

Assess over a period of time a company's performance relative to its own past performance or to that of another company.

Common-Size Analysis of Income Statement

Can be performed by stating each line item on the income statement as a percentage of revenue.

US GAAP Reporting of Unusual or Infrequent Items

Material items that are unusual or infrequent and that are both as of reporting period beginning after 15 December 2015 are shown as part of a company's continuing operations but are presented separately.

Difference between Economic Goodwill and Accounting Goodwill

Economic goodwill is based on the economic performance of the entity, whereas accounting goodwill is based on accounting standards and is reported only in the case of acquisitions.

Financial Instrument (IFRS)

Contract that gives rise to a financial asset of one entity, and a financial liability or equity instrument of another entity.

Amortized Cost of a Financial Asset (or Liability)

Amount at which it was initially recognized

- any principal repayments

+/- Amortization of discount or premium

- Impairments

Three measurement categories for financial assets

1) Held-for-trading / Fair Value through profit and loss

2) Available-for-sale / Fair Value through other comprehensive income

3) Held-to-Maturity / Cost or Amortized Cost

Common-Size Analysis of Balance Sheet

Can be performed by stating each balance sheet item as a percentage of total assets.

Payments to investors are made with

Cash

Key difference between direct and indirect method

Direct method uses the major categories of gross cash receipts and payments, and the indirect method reconciles net income to net cash flows.

Classification of Interest Received (IFRS)

Operating or investing

Classification of Interest Received (US GAAP)

Operating

Classification of Interest Paid (IFRS)

Operating or financing

Classification of Interest Paid (US GAAP)

Operating

Classification of Dividends Received (IFRS)

Operating or investing

Classification of Dividends Received (US GAAP)

Operating

Classification of Dividends Paid (IFRS)

Operating or financing

Classification of Dividends Paid (US GAAP)

Financing

Classification of Bank Overdrafts (IFRS)

Considered part of cash equivalents

Classification of Bank Overdrafts (US GAAP)

Not considered part of cash and cash equivalents and classified as financing

Classification of Taxes Paid (IFRS)

Generally operating, but a portion can be allocated to investing or financing if it can be specifically identified with these categories

Classification of Taxes Paid (US GAAP)

Operating

For a mature company, it is expected and desired that operating cash flow exceeds _________.

Net income

Two approaches to common-size analysis of cash flow statement

1) Expressing each line item of cash inflow (outflow) as a percentage of total inflows (outflows) or cash

2) Expressing each line item as a percentage of net revenue

Free Cash Flow

Essentially the measure of the excess of operating cash flow over capital expenditures.

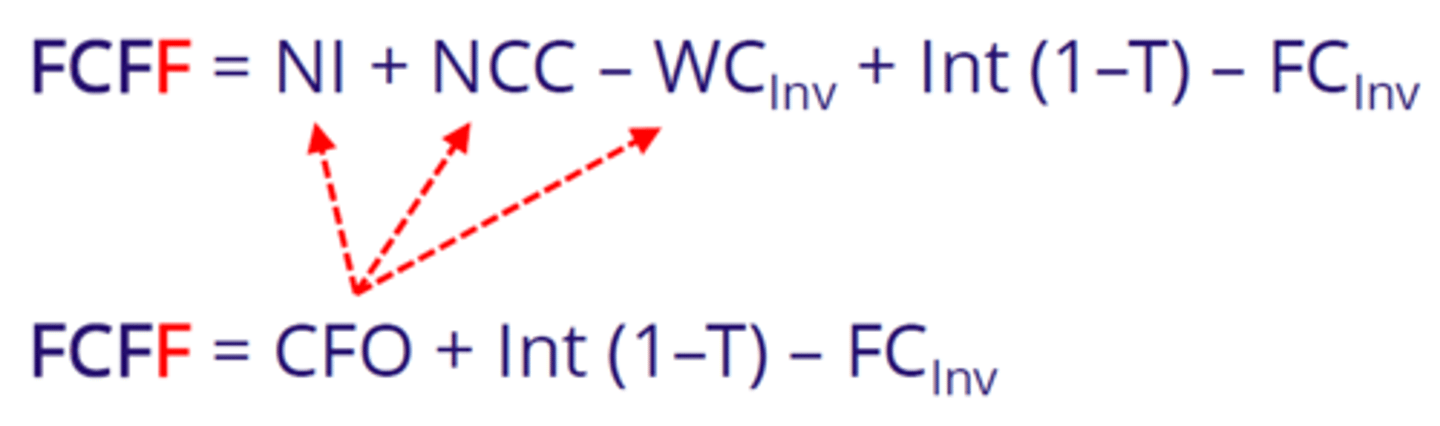

Free Cash Flow to the Firm (FCFF)

The cash available to both debt and equity holders.

= CFO

+ Interest Expense (1 - Tax Rate)

- Net Fixed Capital Investment (CFI) (Capex)

Depreciation and amortization do not have to be added when calculating FCFF from CFO.

List of Cash Flow Ratios (Performance)

1) Cash flow to revenue

2) Cash return on assets

3) Cash return on equity

4) Cash to income

5) Cash flow per share

List of Cash Flow Ratios (Coverage)

1) Debt coverage

2) Interest coverage

3) Reinvestment

4) Debt payment

5) Dividend payment

6) Investing and financing

List of Inventory Ratios

1) Inventory Turnover

2) Days of Inventory on Hand (DOH)

3) Gross Profit Margin

Criteria for intangibles under IFRS

1) Identifiable (either capable or being separated from the entity or arising from contractual or legal rights)

2) Under the control of the company

3) Expected to generate future economic benefits

4) It is probable that the expected future economic benefits of the asset will flow to the company

5) The cost of the asset can be reliably measured

On the statement of cash flows, costs of internally developing intangible assets are classified as _____________ cash flows, whereas costs of acquiring intangible assets are classified as _____________ cash flows.

Operating, investing

IFRS allows companies to recognize an intangible asset arising from development expenditures if following are met:

1) Demonstration of the technical feasibility of completing the intangible assets

2) The intent to use or sell the product

Free Cash Flow to Equity (FCFE)

Cash available to distribute to equity holders. After payments have been made to debt holders (i.e., this is considered a post-levered measure, unlike FCFF which is before payments to both debt and equity holders).

Net Debt Increase = the change in Balance Sheet debt (“debt principal raised”, change in “bonds issued”)

Positive FCFE means the company has an excess of operating cash flow over amounts needed for capital expenditures and repayment of debt (this cash would be available for distribution to owners).

Three ways intangible assets can be obtained:

1) Purchased

2) Developed Internally

3) Acquired

Treatment of Impairment for Intangible Assets with a Finite Life

Amortized (carrying amount decreases over time) and may become impaired.

Essentially the same as for tangible assets. The amount of the impairment loss will reduce the carrying amount of the asset on the balance sheet and will reduce net income on the income statement.

Treatment of Impairment for Intangible Assets with Indefinite Lives

Not amortized — instead, carried on the balance sheet at historical cost but are tested at least annually for impairment.

Treatment of Impairment for Intangible Assets Held-for-Sale

A long-lived (non-current) asset is reclassified as held for sale rather than held for use when management's intent is to sell it and its sale is highly probable.

At the time of reclassification, assets previously held for use are tested for impairment. If the carrying amount at the time of reclassification exceeds the fair value less costs to sell, an impairment loss is recognized and the asset is written down to fair value less costs to sell. Long-lived assets held for sale cease to be depreciated or amortized.

Derecognition

A company derecognizes an asset (i.e., removes it from the financial statements) when the asset is disposed of or is expected to provide no future benefits from either use or disposal.

A company may dispose of a long-lived operating asset by selling it, exchanging it, abandoning it, or distributing it to existing shareholders.

Calculation for Sale of Long-Lived Asset

The gain or loss on the sale of long-lived assets is computed as the sales proceeds minus the carrying amount of the asset at the time of sale. An asset's carrying amount is typically the net book value (i.e., the historical cost minus accumulated depreciation), unless the asset's carrying amount has been changed to reflect impairment and/or revaluation.

Lessee

Party who uses the asset and pays the consideration.

Lessor

Party who owns the asset, grants the right to use the asset, and receives consideration. Often real estate investment companies or banks.

For a contract to be a lease or contain a lease, it must:

1) Identify a specific underlying asset

2) Give the customer the right to obtain largely all of the economic benefits from the asset over the contract term

3) Give the customer, not the supplier, the ability to direct how and for what objective the underlying asset is used

Advantages of Leasing

1) Less cash needed upfront (require little, if any, down payment)

2) Cost effectiveness: leases are a form of secured borrowing — in the event of non-payment, the lessor simply repossesses the leased asset

3) Convenience and lower risks associated with asset ownership (e.g., obsolescence)

Leases can resemble either

1) The purchase of an asset (finance lease)

2) A rental contract (operating lease)

Lessee Accounting (IFRS)

1) At lease inception, the lessee records a lease payable liability and a right-of-use (ROU) asset on its balance sheet, both equal to the present value or future lease payments (discount rate in the PV calculation is either the rate implicit in the lease or an estimated secured borrowing rate)

2) Lease liability subsequently reduced by each lease payment using effective interest method

3) ROU is subsequently amortized, often on a straight-line basis, over the lease term

Lessee Accounting (US GAAP) — Operating Lease

At operating lease inception, the lessee records a lease payable liability and a corresponding right-of-use asset on its balance sheet that are subsequently reduced by the principal repayment component of the lease payment and amortization, respectively, in the same manner that an IFRS lessee would.

For an operating lease, the lessee's ROU asset amortization expense is the lease payment minus the interest expense. The implication is that the total expense reported on the income statement (interest plus amortization) will equal the lease payment and that the lease liability and the ROU asset will always equal each other because the principal repayment and amortization are calculated in an identical manner.

Lessor Accounting (IFRS and US GAAP) — Finance Lease

1) At finance lease inception, the lessor recognizes a lease receivable asset equal to the present value of future lease payments and de-recognizes the leased asset, simultaneously recognizing any difference as a gain or loss. The discount rate used in the present value calculation is the rate implicit in the lease

2) The lease receivable is subsequently reduced by each lease payment using the effective interest method. Each lease payment is composed of interest income, which is the product of the lease receivable and the discount rate, and principal proceeds, which equals the difference between the interest income and cash receipt

Lessor Accounting (IFRS and US GAAP) — Operating Lease

Because the contract is essentially a rental agreement, the lessor keeps the leased asset on its books and recognizes lease revenue on a straight-line basis. Interest revenue is not recognized because the transaction is not considered a financing.

Grant Date

The day that options are granted to employees.

Service Period

The period between the grant date and vesting date.

Vesting Date

The date that employees can first exercise the stock options (can be immediate or over a future period).

Exercise Date

When employees exercise the options and convert them to stock.

Basic EPS

Basic EPS is the amount of income available to common shareholders divided by the weighted average number of common shares outstanding over a period.

The amount of income available to common shareholders is the amount of net income remaining after preferred dividends (if any) have been paid.

For weighted average of common shares outstanding, must multiply the values by the proportion of the period (if shares are issued on April 1, multiple number of shares by 9/12).

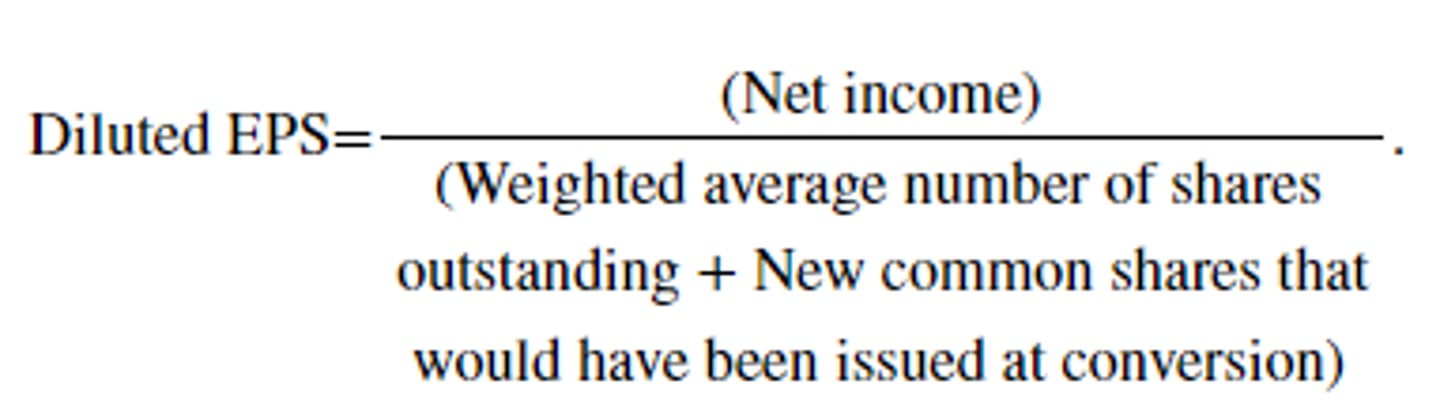

Diluted EPS (Convertible Preferred Stock Outstanding)

Diluted EPS using the if-converted method for convertible preferred stock is equal to net income divided by the weighted average number of shares outstanding from the basic EPS calculation plus the additional shares of common stock that would be issued upon conversion of the preferred.

Diluted EPS (Convertible Debt Outstanding)

Diluted EPS is calculated as if the convertible debt had been converted at the beginning of the period. If the convertible debt had been converted, the debt securities would no longer be outstanding; instead, additional shares of common stock would be outstanding. Also, if such a conversion had taken place, the company would not have paid interest on the convertible debt, so the net income available to common shareholders would increase by the after-tax amount of interest expense on the debt converted.

When instruments can be converted is irrelevant, includes all.