ACC 301 Exam 2 Study Guide

1/39

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

40 Terms

Which of the following is not one of the steps for recognizing revenue?

Estimate the total transactions price of the contract based on the sum of the stand-alone selling prices of the goods and services in the contract.

Which of the following is not an indicator the control of a good has passed from the seller to the buyer?

Buyer has scheduled delivery

Which of the following is an indicator that revenue for a service can be recognized over time?

The seller in enhancing an asset that the buyer controls as the service is performed

Which of the following is not an indicator that revenue for a service can be recognized over time?

The seller has significant experience with the customer and anticipates fulfillment of the contract

Which of the following is consistent with goods and services being distinct for purposes of identifying separate performance obligations?

All the choices are correct

Which of the following is a separate performance obligation?

An extended warranty

A company enters into a contract that includes a fixed fee of $300,000 and a bonus of $100,000 if the company can achieve a specified goal. The company estimates a 60% likelihood of achieving this goal. Under the expected value method of estimating variable consideration, the transaction price is:

$360,000

Lewis is selling a product with some of the transaction price depending on the outcome of a future event. There is a 75% chance that the event will result in $100,000 of consideration to Lewis, and a 25% chance that the event will result in $40,000 of consideration to Lewis. Which of the following is not an appropriate estimate of the amount of uncertain consideration for purposes of Lewis estimating the transaction price?

$70,000

Bad Debts:

Must be recognized as an expense.

Allocation of the transaction price to performance obligations:

Is based on relative standalone selling prices

Fung wrote a contract that involves two performance obligations. Product A has a stand-alone selling price of $50, and product B has a stand-alone selling price of $100. The price for the combined product is $120. How much of the transaction price would be allocated to the performance obligation for delivering product A?

$40

Jada wrote a contract that involves two separate performance obligations. Jada cannot estimate the stand-alone selling price of product A. Product B has a stand-alone selling price of $100. The price for the combined product is $120. How much of the transaction price would be allocated to the performance obligation for delivering product A? $120-100=$20

$20

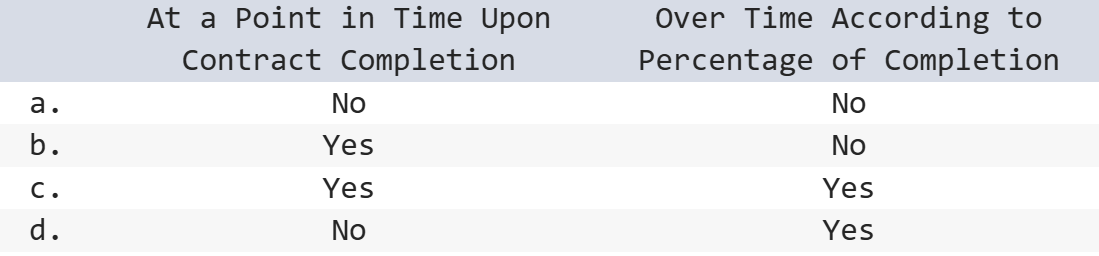

For profitable long-term contracts, income is recognized in each year when revenue is recognized:

Option D

When accounting for a long-term construction contract for which revenue is recognized over time according to the percentage of completion, gross profit is recognized in any year and is debited to:

Construction in Progress (CIP)

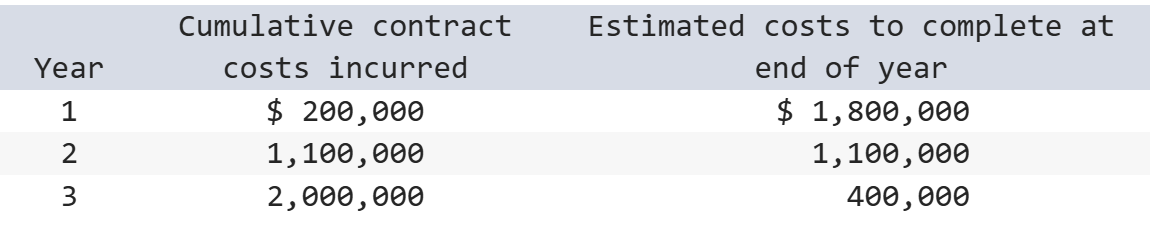

Hollywood Construction Company recognizes revenue over time according to percentage of completion for its long-term construction contracts. During Year 1, Hollywood began work on a $3,000,000 fixed-fee construction contract, which was completed in Year 4. The accounting records disclosed the following data at year-end. For Year 3, Hollywood should have recognized gross profit on this contract of:

As of end of Year 2, revenue recognized to date is ($1,100,000 ÷ ($1,100,000 + 1,100,000)) × $3,000,000 = $1,500,000, and cost of construction recognized to date is $1,100,000, so gross profit recognized to date is $400,000. As of end of Year 3, revenue recognized to date is ($2,000,000 ÷ ($2,000,000 + 400,000)) × $3,000,000 = $2,500,000, and cost of construction recognized to date is $2,000,000, so gross profit recognized to date is $500,000.

$100,000

Sandlewood Construction Incorporated recognizes revenue over time according to percentage of completion for its long-term construction contracts. In Year 1, Sandlewood began work on a $10,000,000 construction contract, which was completed in Year 2. The accounting records disclosed the following data at the end of Year 1:

Costs incurred | $ 5,400,000 |

|---|---|

Estimated cost to complete | 3,600,000 |

Progress billings | 4,100,000 |

Cash collections | 3,200,000 |

How much gross profit should Sandlewood have recognized in Year 1?

$600,000

As of year-end Year 1, revenue recognized to date is ($5,400,000 ÷ ($5,400,000 + 3,600,000)) × $10,000,000 = $6,000,000, and cost of construction recognized to date is $5,400,000, so gross profit recognized to date is

CrayFry, offers an extended warranty for one of its products, the CrayFrier. The warranty normally has a price of $25, but CrayFry offers it for $20 when purchased at the same time as the fryer. CrayFry anticipates a 60% chance that a customer will purchase the extended warranty along with the fryer. Assume CrayFry sells to 1,000 fryers with the extended warranty discount offer. What is the total stand-alone selling price that CrayFry would use for the extended warranty discount option for purposes of allocating revenue among the performance obligations in those 1,000 fryer contracts?

$3,000

The $5 discount has a 60% chance of being taken by a customer, so the stand-alone selling price associated with 1,000 warranties is $3,000 (computed as $5 × 60% × 1,000 fryers).

Which of the following does not apply to a seller who is an agent?

Has control over goods or services

TVLand sells home entertainment systems and also offers a complementary installation service. The same service is offered by other vendors for $50 on average, and TVLand typically charges approximately 40% more than other vendors for similar services on a stand-alone basis. Using the adjusted market assessment approach, the stand-alone selling price of the installation service is:

$70

Under the adjusted market assessment approach, TVLand would base its estimate of the stand-alone selling price of the installation service on the prices charged by other vendors for the same service, adjusted as necessary. Because TVLand typically charges 40% more than competitors, it would estimate the stand-alone price of the assembly service to be $50 × 140% =

TVLand sells home entertainment systems and also offers a complementary installation service. TVLand estimates that it incurs $40 in labor and materials to complete one installation, with an average of 25% profit based on cost. Using the expected cost plus margin approach, the stand-alone selling price of the installation service is:

$50

Under the expected cost plus margin approach, TVLand would base its estimate of the stand-alone selling price of the installation service on the $40 cost it incurs, plus its normal margin of 25% × $40 = $10. Therefore, TVLand would estimate the stand-alone selling price of the installation service to be $40 + $10 =

Which of the following might be classified as a cash equivalent?

30-day Treasury Bill

A company uses the gross method to account for cash discounts offered to its customers. If payment is made before the discount period expires, which of the following is correct?

Sales discounts is debited for the amount of discounts taken by customers.

Allister Company does not use the allowance method to account for bad debts and instead any bad debts that do arise are written off as bad debt expense. What problem might this create if bad debts are material?

Receivables likely will be overstated

because not accruing bad debts will result in the receivables being stated at an amount that is greater than the amount expected to be collected.

The Reingold Hat Company uses the allowance method to account for bad debts. During the year, the company recorded $800,000 in credit sales. At the end of the year, account balances were: Accounts receivable, $120,000; Allowance for uncollectible accounts, $3,000 (credit). If bad debt expense is estimated to be 3% of credit sales, the appropriate adjusting entry will include a debit to bad debt expense of:

$24,000

$800,000 × 3% =

Enchill Company accrues bad debt expense during the year at an amount equal to 3% of credit sales. At the end of the year, a journal entry adjusts the allowance for uncollectible accounts to a desired amount based on an aging of accounts receivable. At the beginning of the year, the allowance account had a credit balance of $18,000. During the year, credit sales totaled $480,000 and receivables of $14,000 were written off. The year-end aging indicated that a $21,000 allowance for uncollectible accounts was required. Enchill's bad debt expense for the year would be:

$17,000

Focusing on the allowance account, $18,000 − 14,000 + total bad debt expense = $21,000, so bad debt expense = $17,000.

Harmon Sporting Goods received a $60,000, 6-month, 10% note from a customer. Four months after receiving the note, it was discounted at a local bank at a 12% discount rate. The cash proceeds received by Harmon were:

$61,740

Face amount ($60,000) + interest to maturity ($60,000 × 10% × ½ year = $3,000) = maturity value ($63,000). Maturity value ($63,000) − discount ($63,000 × 12% × 212 year = $1,260) =

At the end of June, the Marquess Company factored $200,000 in accounts receivable with Homemark Finance. The transfer is made without recourse. Homemark charges a fee of 3% of receivables factored. During July, $150,000 of the factored receivables are collected. What amount of loss on sale of receivables would Marquess record in June?

$6,000

$200,000 × 3% =

At the end of June, the Marquess Company factored $200,000 in accounts receivable with Homemark Finance. Homemark charges a fee of 3% of receivables factored. During July, $150,000 of the factored receivables are collected. If the transfer were made with recourse but is still accounted for as a sale, what amount of loss on sale of receivables would the company record in June assuming the estimated recourse liability is $2,000?

$8,000

Which of the following is NOT true about accounting for merchandise returns?

The refund liability is credited when a customer makes a return

Lewis Diagnostics sold merchandise to a customer in exchange for a $40,000, four-year, noninterest-bearing note when an equivalent loan would carry 8% interest. Lewis would record sales revenue on the date of sale equal to:

The present value of $40,000 using an 8% interest rate.

Clancy Company accepted a two-year noninterest-bearing note for $1,166,400 on January 1, Year 1. The note was accepted as payment for merchandise with a fair value of $1,000,000. The effective interest rate is 8%.

The cash collection on December 31, Year 2, would be recorded as:

Account Title | Debit | Credit |

|---|---|---|

Discount on notes receivable | 86,400 |

|

Cash | 1,166,400 |

|

Notes receivable |

| 1,166,400 |

Interest revenue |

| 86,400 |

Heinlein Association accepted a two-year interest-bearing note for $1,000,000 on January 1, Year 1. The note was accepted as payment for merchandise with a fair value of $1,000,000. The effective interest rate is 7%. Interest is paid at the end of each year.

The cash collection on December 31, Year 2, would be recorded as:

Account Title | Debit | Credit |

|---|---|---|

Cash | 1,070,000 |

|

Notes receivable |

| 1,000,000 |

Interest revenue |

| 70,000 |

Companies that purchase inventories that are primarily in finished form for resale to customers are known as:

Merchandising Companies

Using a perpetual inventory system, the purchase of inventory on account is recorded with a:

Debit to inventory

Using a perpetual inventory system, the sale of inventory on account is recorded with a:

All of the other answers are recorded with the sale of inventory on account.

In a perpetual inventory system, if merchandise is returned to a supplier:

Inventory is Credited

Sanfillipo, Incorporated, had 800 units of inventory on hand at March 1 of the current year, costing $20 each. Purchases and sales of inventory during the month of March were as follows:

Date | Purchases | Sales | |

|---|---|---|---|

March 8 |

| 600 | units |

March 15 | 400 units @ $22 each |

|

|

March 22 | 400 units @ $24 each |

|

|

March 27 |

| 400 | unit |

Sanfillipo uses the periodic inventory system. According to a physical count, 600 units were on hand at the end of March.

The cost of inventory at the end of March applying the FIFO method is:

(400 units @ $24 each + 200 units @ $22 each)

$14,000

Sanfillipo, Incorporated, had 800 units of inventory on hand at March 1 of the current year, costing $20 each. Purchases and sales of inventory during the month of March were as follows:

Date | Purchases | Sales | |

|---|---|---|---|

March 8 |

| 600 | units |

March 15 | 400 units @ $22 each |

|

|

March 22 | 400 units @ $24 each |

|

|

March 27 |

| 400 | units |

Sanfillipo uses the periodic inventory system. According to a physical count, 600 units were on hand at the end of March.

The cost of inventory at the end of March applying the LIFO method is:

$12,000

600 units @ $20 each

Sanfillipo, Incorporated, had 800 units of inventory on hand at March 1 of the current year, costing $20 each. Purchases and sales of inventory during the month of March were as follows:

Date | Purchases | Sales | |

|---|---|---|---|

March 8 |

| 600 | units |

March 15 | 400 units @ $22 each |

|

|

March 22 | 400 units @ $24 each |

|

|

March 27 |

| 400 | units |

Sanfillipo uses the periodic inventory system. According to a physical count, 600 units were on hand at the end of March.

The cost of inventory at the end of March applying the average cost method is:

$12,900

Average cost of purchases = $21.50 each = [(800 × $20) + (400 × $22) + (400 × $24)] ÷ 1,600 units. Ending inventory = 600 units @ $21.50 each.