Looks like no one added any tags here yet for you.

Financial Transactions

[Term]

Events that have an economic impact on a business, such as:

📦 Sale of merchandise

🛒 Purchase of inventory

💰 Payment of salaries and utilities

A business experiences thousands of transactions in a year, requiring a system to organize and track them.

Why is a system needed to track financial transactions?

📖 General journal

📚 Ledger of accounts

two most common components of a financial transaction tracking system

Account

{Term]

The basic component of an accounting system; tracks assets, liabilities, equity, revenue, and expenses.

A. The first statement is true. The second statement is false.physical forms may accounts be kept?

I. The account is the central place used to collect information about transactions affecting a particular financial statement item.

II. There is no need to separate accounts for every asset, liability, owner’s equity revenue and expense.

A. The first statement is true. The second statement is false.

B. The first statement is false. The second statement is true.

C. Both statements are true.

D. Both statements are false.

✅ A) Cash accounts, rent-expense accounts, and accounts receivable

Explanation: Examples of accounts include cash accounts, accounts receivable, retained earnings, cash sales, credit sales, rent-expense, and salary-expense accounts.

What are examples of different types of accounts?

A) Cash accounts, rent-expense accounts, and accounts receivable

B) Owner’s equity, assets, and liabilities

C) Accounts for savings and investments only

D) Income tax and depreciation accounts only

Loose-leaf folder 📂

Notebook 📖

Computer files 💻

Physical forms accounts may be kept in [3]

Accounts are kept in a ledger of accounts. 📒

Where are accounts kept?

📑 In the same order as they appear on financial statements:

Current assets

Noncurrent assets

Current liabilities

Noncurrent liabilities

Owner’s equity

Revenues

Expenses

How are accounts organized in the ledger? [7]

🔍 Analyzing – Understanding what happened and its effect on the business

✍ Recording – Entering data into the system

📂 Classifying – Grouping similar activities together

📊 Summarizing – Explaining the results

📝 Reporting – Issuing financial statements

📈 Interpreting – Evaluating how different data relate to each other

What are the six steps of the Accounting Process?

Analyzing

[Step in the Accounting Process]

looking at what happened and how the business was affected.

Recording

[Step in the Accounting Process]

Putting the information into the accounting system.

Classifying

[Step in the Accounting Process]

Grouping all the same activities (e.g. all purchases) together

Summarizing

[Step in the Accounting Process]

Explaining the results

Reporting

[Step in the Accounting Process]

Issuing the statements that tell the results of the previous functions.

Interpreting

[Step in the Accounting Process]

Examining the statements to determine how the various pieces of information they contain relate to each other

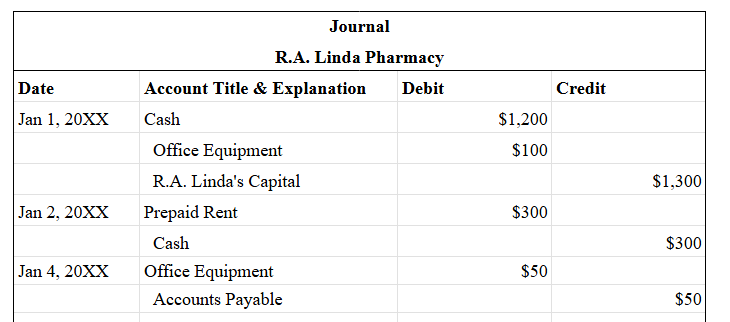

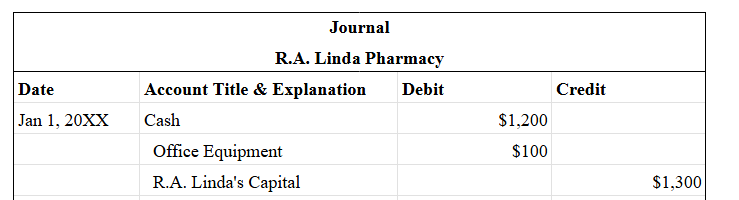

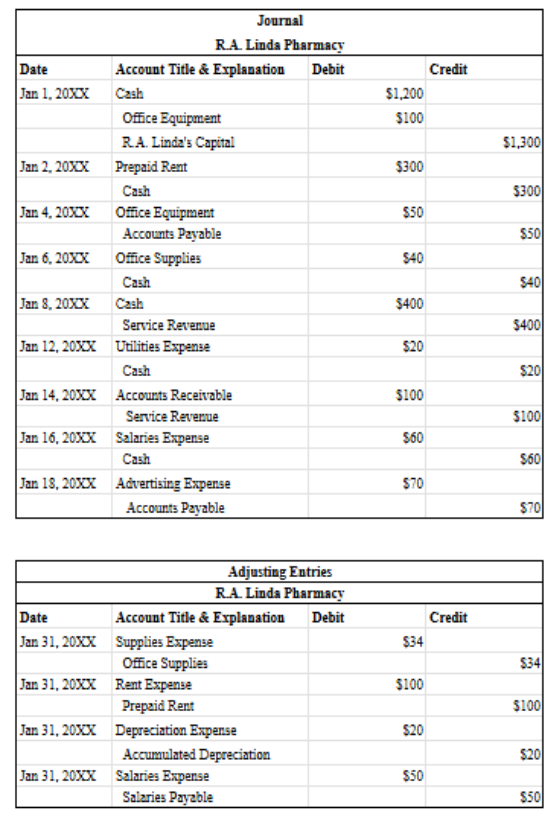

Journal

[Term]

A record of the original entry for every transaction.

📅 Date of transaction

🏦 Account titles

💰 Amounts involved

📝 Brief explanation

📄 Ledger page reference

Journals include the following [5]

❌ False – They are recorded chronologically.

✅ True

I. All transactions are recorded randomly in the journal.

II. The ledger records transactions based on the type of account.

A. The first statement is true. The second statement is false.

B. The first statement is false. The second statement is true.

C. Both statements are true.

D. Both statements are false.

Journalizing

It is the term for the process of recording transactions in the journal.

Journal Example (just read)

Jan. 1 Rose A. Linda invested $1,200 cash and $100 of office equipment to open R.A. Linda Consulting

Jan 2… Paid rent three months in advance $300

Jan 4… Purchased office equipment on account $50.

Analysis and Recording

Steps in Journalizing [2]

Analysis

[Step in Journalizing]

determine the accounts involved

determine what account is to be debited and credited

Recording

[Steps on Journalizing]

write the date

write the account and amount of debit entry write a brief and concise explanation

write the account and amount of credit entry

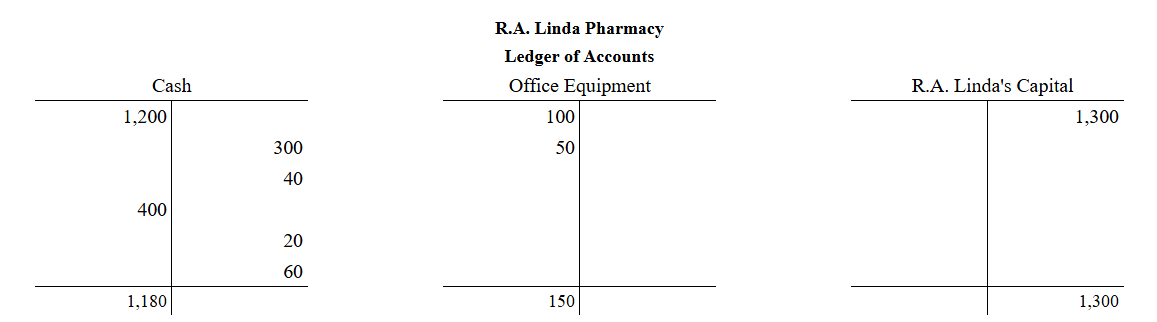

➡ Posting

What is the process of transferring journal entries to a ledger called?

Classifies transactions by type of account

Groups all cash transactions together

Organizes entries from the journal

What does the ledger do? [3]

Posting Example (just read)

✅ Transact the debit entry to the debit side of the ledger

✅ Transfer the credit entry to the credit side of the ledger

✅ Cross-index records by writing their page in the Folio column

Steps in Posting in a Ledger [3]

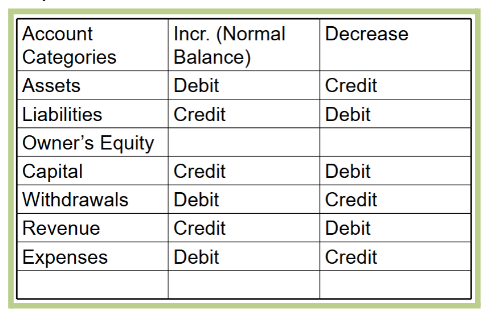

➡ Debit/Credit Method

What is another name for the double-entry method?

📌 Debit = Value received

📌 Credit = Value parted with

What do debit and credit represent?

✅ C) The recording function of accounting based on the debit/credit method

What does bookkeeping refer to?

A) Decision-making in accounting

B) The process of posting entries in the journal

C) The recording function of accounting based on the debit/credit method ✅

D) Financial statement analysis

📌 Assets = Liabilities + Owner’s Equity

What equation must always be used as a check in the debit/credit method?

✅ True

❌ False – The credit entry must be posted on the credit side.

I. Every account has two sides: the left side (debit) and the right side (credit).

II. When posting in the ledger, the credit entry should be posted on the debit side.

A. The first statement is true. The second statement is false.

B. The first statement is false. The second statement is true.

C. Both statements are true.

D. Both statements are false.

➡ T accounts

➡ Balance column account

What are the two ways to structure accounts?

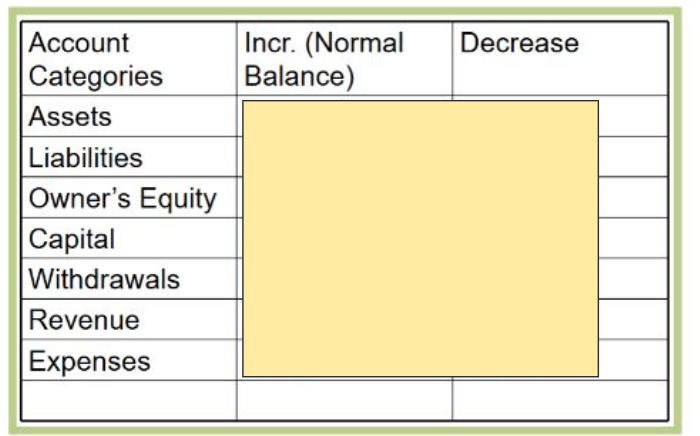

Asset Increase = debit on the left side

liability or owner’s equity increases = credit on the right side

Asset Decrease = credit on the right side

liability or owner’s equity decreases = debit on the left side

Rules Governing the Recording of Transactions in the Debit/Credit Method [4]

Fill in the Table: Rules Governing the Recording of Transactions in the Debit/Credit Method

Each transaction must be recorded separately.

The transaction must be recorded so that assets=liabilities+owner’s equity.

Dual Entry Accounting - Each transaction will affect at least two accounts. transaction may affect more than two accounts, but it must always affect at least two.

Each transaction must be recorded such that debits equal credits.

4 Basic Rules in Recording Transactions

❌ False – Revenue increases owner’s equity, so it is recorded as a credit on the right side.

I. Revenue decreases owner’s equity, so it is recorded as a debit.

II. A transaction may affect more than two accounts, but it must always affect at least two.

A. The first statement is true. The second statement is false.

B. The first statement is false. The second statement is true.

C. Both statements are true.

D. Both statements are false.

dual-entry accounting

Term for each transaction affecting at least two accounts

Account affected

Category

Increase or Decrease

Rules of Debit and Credit

Appearance of T accounts

5 Steps of Transaction Analysis

Cash increases by $1,000: Debit

Accounts payable increase by 1,000: Credit

Owner’s equity increased by 500: Credit

Rent expense of 850: Debit

Revenue of 250: Credit

Accounts receivable decrease by 400: Credit

Notes payable increase by 5000: Credit

Owner’s withdrawal of 100: Debit

Fixed asset increase by 5,000: Debit

Inventory increase by 500: Debit

Indicate whether each of the following would be a debit or credit

Cash increases by $1,000:

Accounts payable increase by 1,000:

Owner’s equity increased by 500:

Rent expense of 850:

Revenue of 250:

Accounts receivable decrease by 400:

Notes payable increase by 5000:

Owner’s withdrawal of 100:

Fixed asset increase by 5,000:

Inventory increase by 500:

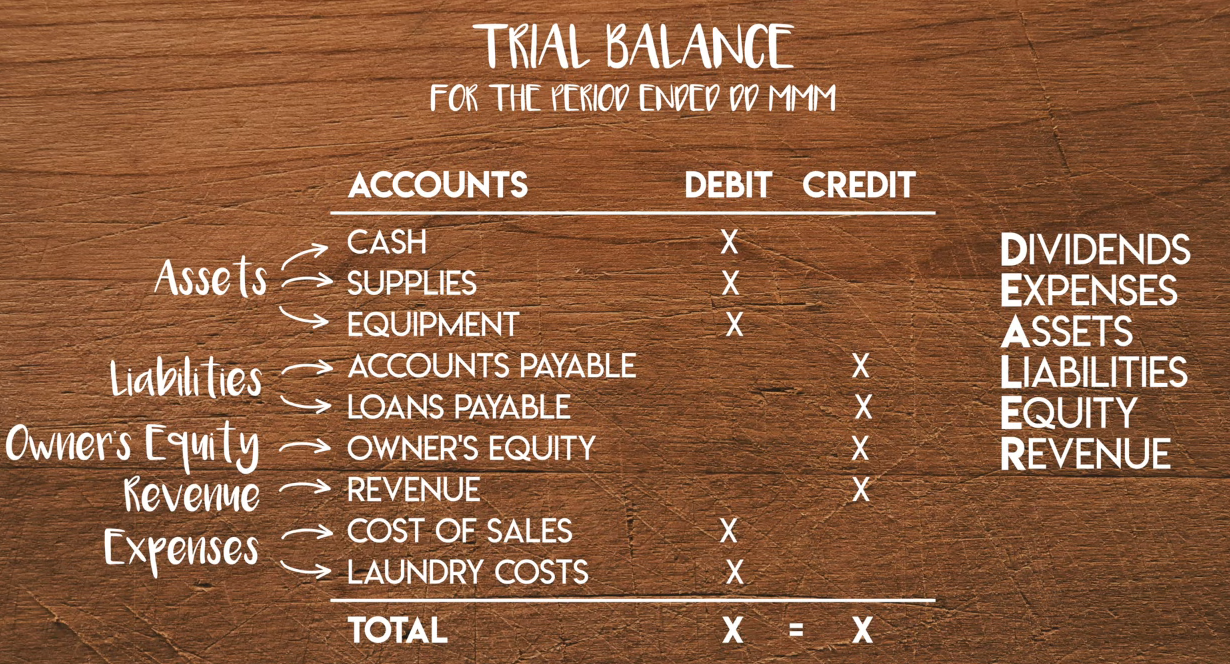

Trial Balance

[Term]

A list of all accounts and their debit or credit balances, arranged in the order they appear in the ledger.

✅ To check for errors

✅ To organize data for financial statements

Why is the trial balance prepared? [2]

Trial Balance Format

Cash Bases of Accounting

[Term]

Revenue is recorded when cash is received, and expenses are recorded when cash is paid, regardless of when they are earned or consumed.

Accrual Basis of Accounting

[Term]

Revenue is recorded when earned, and expenses are recorded when incurred, regardless of when cash is received or paid.

Cash: April 25 (when cash is received)

Accrual: April 10 (when service is provided)

Cash: August 8

Accrual: expenses are recognized as the vials are consumed.

Sample: Record the following as the Case and Accrual Basis

On April 10, a pharmacist dispenses prescription medication to a charge patient who pays the total bill on April 25.

assume that on August 8, a pharmacist pays $500 for prescription containers that will be used in August, September and October.

B) It allows better comparison between pharmacies

❌ False – Inventory is recognized as an asset.

✅ True

Questions Practice

Why is the accrual basis of accounting recommended for pharmacies?

A) It is easier to implement

B) It allows better comparison between pharmacies or industry averages

C) It recognizes inventories as expenses

D) It ignores prepaid expenses

True or False: Under the accrual basis, inventory is recognized as an expense rather than an asset.

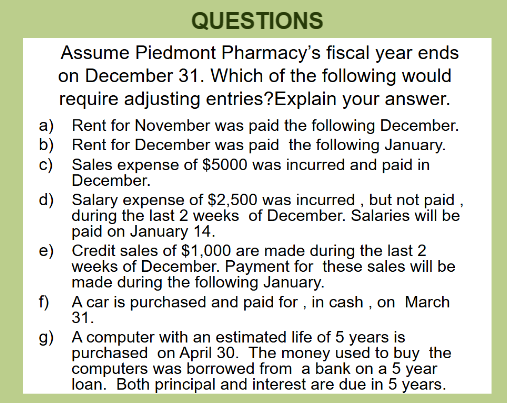

True or False: Adjusting entries are made after transactions are journalized and posted but before financial statements are prepared.

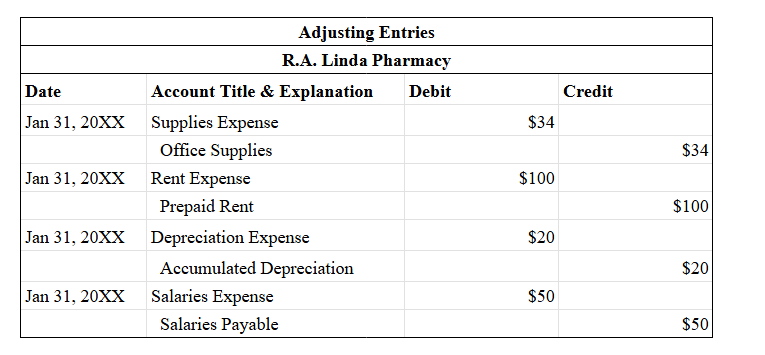

Adjusting Entries

[Term]

Entries made at the end of an accounting period to update accounts for more accurate financial statements.

✅ To properly match/update revenues and expenses in the correct period

✅ To update accounts for depreciation, prepaid, and accrued expenses

From ppt:

Some transactions begun in 1 year and is not concluded until a later one. This causes a problem in accurately matching expenses and revenues in the proper year.

If transaction begins in 1 year and is not concluded until a later one, accountants must adjust the accounting records to indicate what portion of the transaction is a revenue or expense in each of the affected years.

Why are adjusting entries necessary? [2]

For Examples of Adjusting Entries: look at the trans here’s an example from the assignment

Adjustment data as of January 31

a) Supplies on hand $6

b) Rent expired $100

c) Depreciation, office equipment $20

d) Salaries payable $50 to be paid February 15

✅ One balance sheet account

✅ One income statement account

✅ The accounting equation remains balanced

What does each adjusting entry affect? (3)

✅ Prepaid expenses

✅ Supplies

✅ Depreciation

✅ Accrued items

What are examples of accounts that require adjusting entries? [4]

✅ To reflect journal adjustments after the initial trial balance. ✍

✅ Ensures more accuracy than a trial balance alone. 🎯

✅ Used to prepare the 📄 Income Statement, 📜 Statement of Owner’s Equity, and 📊 Balance Sheet.

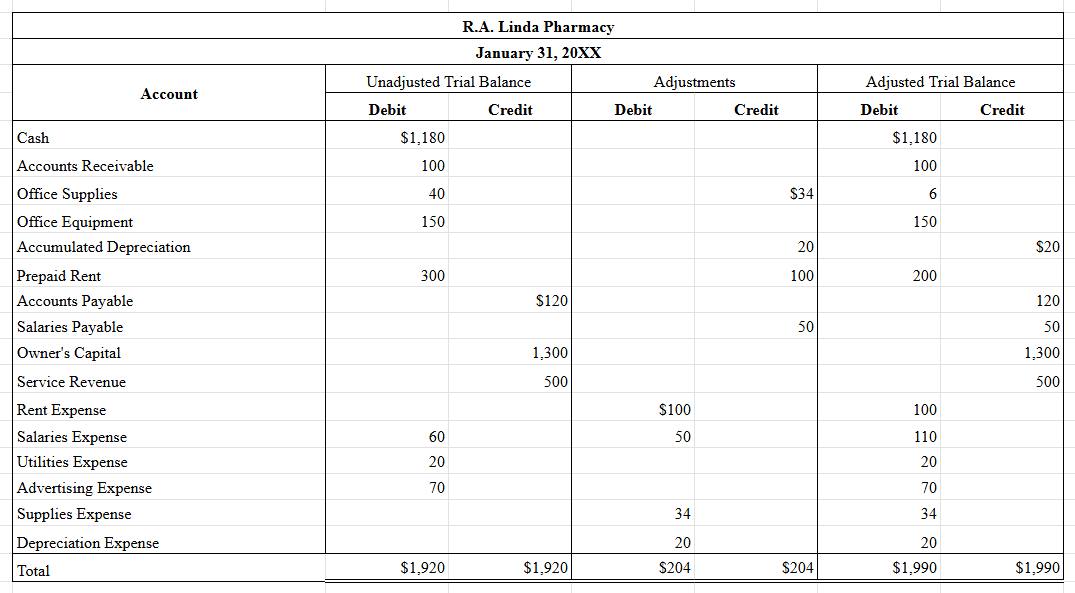

Why is an adjusted trial balance prepared? [3]

Sample of a Full Length Trial Balance. This is a full length one so you can picture it better if you are having a hard time understanding ba’t ganon

Refer to trans and assignment nlng though

Real accounts (Permanent accounts)

[Type of Account in Closing Entries]

Found in the 📊 Balance Sheet (e.g., 💰 Cash, 🏢 Assets, 🏦 Liabilities, 💼 Owner’s Equity).

🔄 Carry over to the next period (Ending balance → Next period’s opening balance).

Balance Sheet Accounts are carried year to year

Nominal accounts (Temporary accounts)

[Type of Account in Closing Entries]

Found in the 📄 Income Statement (e.g., 💵 Revenues, 💸 Expenses, 🤷 Owner Withdrawals).

🔁 Reset to zero at the end of each accounting period.

functional life of one accounting period only in order to permit measurement of net income.

Income Statement Accounts are for one accounting period

✅ B) Income statement accounts reset to zero, while balance sheet accounts carry forward.

What is the key difference between balance sheet accounts and income statement accounts?

A) Balance sheet accounts reset to zero, while income statement accounts carry forward.

B) Income statement accounts reset to zero, while balance sheet accounts carry forward.

C) Both types of accounts reset to zero.

D) Both types of accounts carry forward.

❌ False – They are closed at the end of each accounting period and reset to zero.

❌ False – Adjustments are journalized before preparing the adjusted trial balance.

I. Nominal accounts accumulate balances over multiple accounting periods.

II. The adjusted trial balance is prepared before journalizing adjustments.

A. The first statement is true. The second statement is false.

B. The first statement is false. The second statement is true.

C. Both statements are true.

D. Both statements are false.

Close the revenue account → Transfer balance to Income Summary Account (ISA)

Close each expense account → Transfer balances to ISA

Close the ISA → Transfer balance to the capital account

either capital (for sole proprietorship)or retained earnings (for a corporation)

Close the withdrawal/dividends paid account → Transfer balance to the capital account

owner’s withdrawal account (of a sole proprietorship)

dividends paid account (of a corporation)

Four Closing Entrie

Answer: B – The ISA is temporary and used only for closing.

Since it does not represent a specific item on the financial statements, it does not appear in any of them.

Given that ISA is a nominal account, what is the purpose of the Income Summary Account (ISA)?

A) It appears on the balance sheet.

B) It is a temporary account used only during closing.

C) It holds permanent balances for future accounting periods.

D) It replaces the owner’s equity account.

Transfers net income (or net loss) to the capital account.

A credit balance in ISA = Net Income.

A debit balance in ISA = Net Loss.

Resets income statement accounts to zero for the next period.

From the Trans if you wanna basa:

Closing entries are dated as of the last day of the accounting period. They are journalized and posted on the ledger. Closing entries are made after all other entries have been recorded. Closing process has two effects:

It transfers net income (or net loss) to the capital account. Before it is closed, the ISA contains revenue on the credit side and expenses on the debit side. Hence a credit balance indicates net income and a debit balance indicates net loss.

It establishes zero balance in each of the income statement accounts so they are ready for use in the next accounting period.

Two Effects of the Closing Process

ALL YES

Which of the following accounts must be closed at the end of the accounting period?

Cash

Accounts Receivable

Sales

Rent Expense

Owner’s Withdrawal

Consulting Revenues

YES: B, D, E, G

NO: A,C,F

Practice