FAR

1/70

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

71 Terms

Return on Equity Formula

Net income/average total equity

Bottom up EBITDA approach

Net Income + I + T + D + A

Top Down EBITDA approach

Revenue - COGS - OpEx (ex D&A)

Primary emphasis in accounting and reporting for governmental funds is on?

Source, use, and balance of current financial resources

Nongovernmental not for profit organizations are required to provide which of the following 3 statements?

Statement of cash flows, statement of activities, statement of financial position

Form 8-k

Material events and corporate changes

Form 6k

Semi annual report

Asset impairment test

Undiscounted future cash flows<carrying amount

Functional Expenses for non profit

Activities that relate to the mission and purpose of the non profit organizations such as management and general fundraising

Natural classification expenses for non profits

Typical accounting expenses like salaries, rent, depreciation, etc

Sequence of account displays for statement of financial position for non profit

See picture

Net assets with donor restrictions requirments

Information must be reported within the section net assets with donor restrictions or in the notes of the financial statement.

Quanatative disclosures for non profit

These are numbers and amounts reported in the financial statements or footnotes. They answer “how much” questions.

For nonprofits, key quantitative disclosures include:

Assets, liabilities, and net assets (with subtotals for “with donor restrictions” and “without donor restrictions”).

Liquidity disclosures:

The total amount of financial assets available to meet cash needs for general expenditures within one year.

Nature of restrictions: dollar amounts of donor-restricted assets.

Endowment balances: amounts with and without restrictions.

Obligations: amounts of debt, leases, and other commitments.

📌 Example:

Financial assets available within one year = $1,200,000

Less: Restricted by donors ($500,000)

Less: Designated by board ($200,000)

= $500,000 available for operations

Qualitative disclosures for non profit

These are narrative explanations that describe policies, circumstances, and risks. They answer “how” and “why.”

For nonprofits, key qualitative disclosures include:

Liquidity and financial resource management: policies for managing financial assets to meet obligations.

Board designations: whether net assets without restrictions have been earmarked for specific purposes.

Donor-imposed restrictions: description of time, purpose, or perpetual restrictions.

Endowment policies: spending policy, investment strategy.

Risk management: how the nonprofit ensures cash availability (lines of credit, reserve policies, etc.).

📌 Example:

“The Organization maintains a policy of structuring its financial assets to be available as general expenditures, liabilities, and other obligations come due. The Organization has a line of credit available to manage liquidity needs and maintains an operating reserve equivalent to three months of expenses.”

For nonprofits how are prior year adjustments recorded in statement of activities?

Via reclassification of beginning year net assets

Where are OCI items reported for non profits?

Operating income in statement of activities

How are revenues broken down on non profit statement of activities.

Broken down by whether net assets have or don’t have donor restrictions

What happens when donor restrictions are satisfied for nonprofit on statement of activities?

There is a reclassification on the statement of activities from donor restrictions to without donor restrictions. If a donor restricted asset is received and satisfied in the same year it is reported as revenue without donor restrictions as long as done on a consistent basis.

For non profit organizations all expenses(except investment expenses) are reported as decreases to what on statement of activities?

Net assets without donor restrictions

For non profit organizations how are investment expenses reported on statement of activities?

They are netted separately against investment revenue, and the net is reported by whether it is restricted vs non restricted

support services for a non profit organization are?

Anything that is not a program service ie. fundraising, membership development administration/ general expenses.

Endowment vs quasi endowment funds

Definition: Endowment funds are established with the intent to provide long-term financial support, where the principal is kept intact and only the income is used. Quasi-endowment funds, also known as board-designated endowments, are created by the organization itself and can utilize both principal and income at its discretion.

How is unconditional gift to nonprofit for use of fixed asset reported

An unconditional gift-in-kind for the use of a long-lived asset is recognized at fair value as a donation without donor restrictions and an equal expense in the period used, which has no net effect on net assets

Resources provided with a conditional pledge

Resources provided in conjunction with a conditional pledge represent a refundable advance that is recorded as a liability and is not a portion of net assets. There is no value to classify.

Unconditional promises with pay “overtime” requirements

Unconditional promises to pay over a period of time are generally classified as with donor restrictions as to time until collection.

Use of direct cash flow method rule for profit vs non profit

for profit entities must reconcile direct to indirect method cash flow in footnotes. Non profit entities do not have to do this.

operating cash flows for non profit example

investing cash flows for non profit examples

Also includes buying and selling of fixed assets(But not if the asset was donated and then sold. Non profit has to buy on its own and sell

financing cash flows for non profit examples

Significant non cash transactions should be disclosed of in cash flow statement for both non profit and for profits

TRUE

cash flow statement includes cash equivalents?

Yes

Biscuitworks Charities, a not-for-profit organization, received a contribution of crypto assets with donor restrictions that stipulated those assets be used for the construction of a new research facility. Biscuitworks Charities converted them to cash within two days. How would Biscuitworks Charities classify this receipt on its statement of cash flows?

Financing activities

The Limerack not-for-profit corporation routinely invests idle cash without donor restriction in short-term treasury bills with an original maturity of less than three months. How would proceeds from the sale of these short-term treasury bills be classified?

A. | Operating activity | |

B. | Investing activity | |

C. | Financing activity | |

D. | Not required to be reported |

Not required to be reported(considered cash for cash transaction)

The Mariguild Corporation, a not-for-profit organization, received a donor-restricted donation for the construction of a research facility and issued bonds for the construction of a general administration building in Year 1. How would the Mariguild Corporation most likely treat these transactions as it prepares its Year 1 statement of cash flow?

A. | Combine both donor-restricted funds and debt proceeds in the financing activities classification. | |

B. | Separate donor-restricted contributions and debt proceeds within the financing activities classification. | |

C. | Exclusively show only donor-restricted contributions for capital projects within the financing activities classification. | |

D. | Exclusively show only debt proceeds within the financing activities classification. |

Choice "B" is correct. Cash flows from financing activities may be segregated on the face of the financial statements between major classes of gross cash receipts and payments, such as proceeds from donor-restricted contributions and proceeds from long-term borrowing. Mariguild would most likely follow this practice.

Dividend and interest income are operating cash flows for both non profits and for profits?

TRUE

Attributes of Contributions for non profits

For non profits what is the difference between restricted contributions and conditional contributions?

Conditional contributions cannot be recognized as revenue until met

Gain vs revenue treatment for non profits when they receive contributions.

It’s only classified as revenue if the donation is part/for the entity’s normal course of action.

Unconditional promises to give/ conditional promises

Follow same treatment as normal contributuons

Multi-Year Pledge treatment

Allowance for uncollectable pledges

Similar treatment to for profits, but no expense is recognized(revenue is directly decreased

Split interest agreements for non-profits

Assets and liabilities from split interest agreements need to be separately stated in statement of financial postilion as well as contributions in statement of activities. Estimated based on net present value of payments and must be classified as donor restricted.

Donated Services Treatment

Donated collection items(art wrok statues, etc) rules

Do not have to be recorded by non profit if:

the time item is part of a collection used for public viewing, exhibition, education, or research. It must also be preserved and protected by the organization. Finally, the organization must have a policy that states proceeds from the sale of the donated items be reinvested in other collection items or used to support the direct care of existing collections.

If these conditions are met the organization must recognize revenue and record item as an asset and depreciate it over its useful life.

The policy has to apply to all collection assets(can’t pick and choose)

In rare cases if the asset has an extraordinarily long useful life it may not be depreciated if the asset has historical, aesthetic, cultural value and the owner has the ability and intent to preserve it.

Donated Materials treatment

Also, if org is not going to keep materials (ie pass through to beneficaires) it is not recorded on books unless it is a substantial amount.

If donations are then sold at a higher value then when received. The gain is recorded as an additional contribution

Disclosure of non financial asset contributions

Unconditional contriubtions without restrictions promised to be paid at a certain time in the future.

Recorded at net present value(if time length permits) recorded as contributions with donor restrictions

Journal entries for unconditional pledges “without restrictions” to be paid in a certain amount of time

For one’s with restrictions the entry is different

Journal entries for unconditional pledges “without restrictions” to be paid in a certain amount of time

Contributions wheref fundraising appeals are given to donors (calenders, coffe mugs, etc)are recorded at?

Contribution received- fair value of what was given out

revenue treatment for revenue earned by non profit

Educational non-profit special revenue rules with tution

Health Care non profit revenue rules

revenue for services is recorded at gross amount

operating revenues can also include gift shop, criteria, parking revenue if they are conducted normally

Then certain things are deducted from the revenue(not expensed) which include:

contratural adjustments from third parties

policy discounts

adiministrative adjustments

credit losses ONLY associated with services billed prior to organiations assesement that the patient can pay

charitable services(pro bono work)

credit loss rules for non profits in health care

Altruistic University, a not-for-profit research university, conducts cancer research as part of its normal ongoing activities and regularly receives contributions to support these efforts. Experimental Pharmaceuticals Corporation, a large for profit corporation that markets drugs for cancer treatment, provides resources to Altruistic University to perform clinical trial research on an experimental drug to treat cancer. Resources are provided on the condition that Altruistic University comply with strict specifications governing the manner in which the research is conducted and the frequency and the character of outcome reports. Altruistic University should account for the resources provided by Experimental Pharmaceuticals as:

A. | A contribution that increases board-designated restricted net assets (for future research expenditures). | |

B. | A contribution that increases net assets with donor restrictions and is reclassified as an increase to net assets without donor restrictions upon satisfaction of research and reporting restrictions. | |

C. | A contribution that increases net assets without donor restrictions provided the restrictions are met in the current year and the university uniformly applies this method of recognition to all similar transactions. | |

D. | An exchange transaction that increases net assets without donor restrictions. |

Choice "D" is correct. This is an exchange transaction, which increases net assets without donor restrictions. The results of the clinical trials performed by Altruistic University have a commercial value to Experimental Pharmaceuticals Corporation. Resources have been provided in exchange for research results and do not constitute a contribution.

Recipient accounting for non profit rules that effect accounting treatment

Recipient Accounting for Non-profit when not financially interrelated and without variance power

Dr. Asset at fair value

Cr. refundable advance(liability)

Recipient accounting when not financially interrelated but has variance power

Recipient accounting when they are financially interrelated

Transfer accounting (benefciary side) when recipient is not financially interrelated and has no beneficial interest

Transfer accounting (benefciary side) when benifciary is not financially interrelated and has beneficial interest

Transfer accounting (benefciary side) when beneficiary is financially interrelated

Financial instrument treatment for non-profits

Rules for derivatives for non-profits

Endowment found/ endowment earnings treatment

Original amount gifted is usually classified s net assets with donor restrictions

The investment income on the endowment will either be classified as with or without donor restrictions depending on the request of the donor

Returns on endowment fund with donor restriction treatment

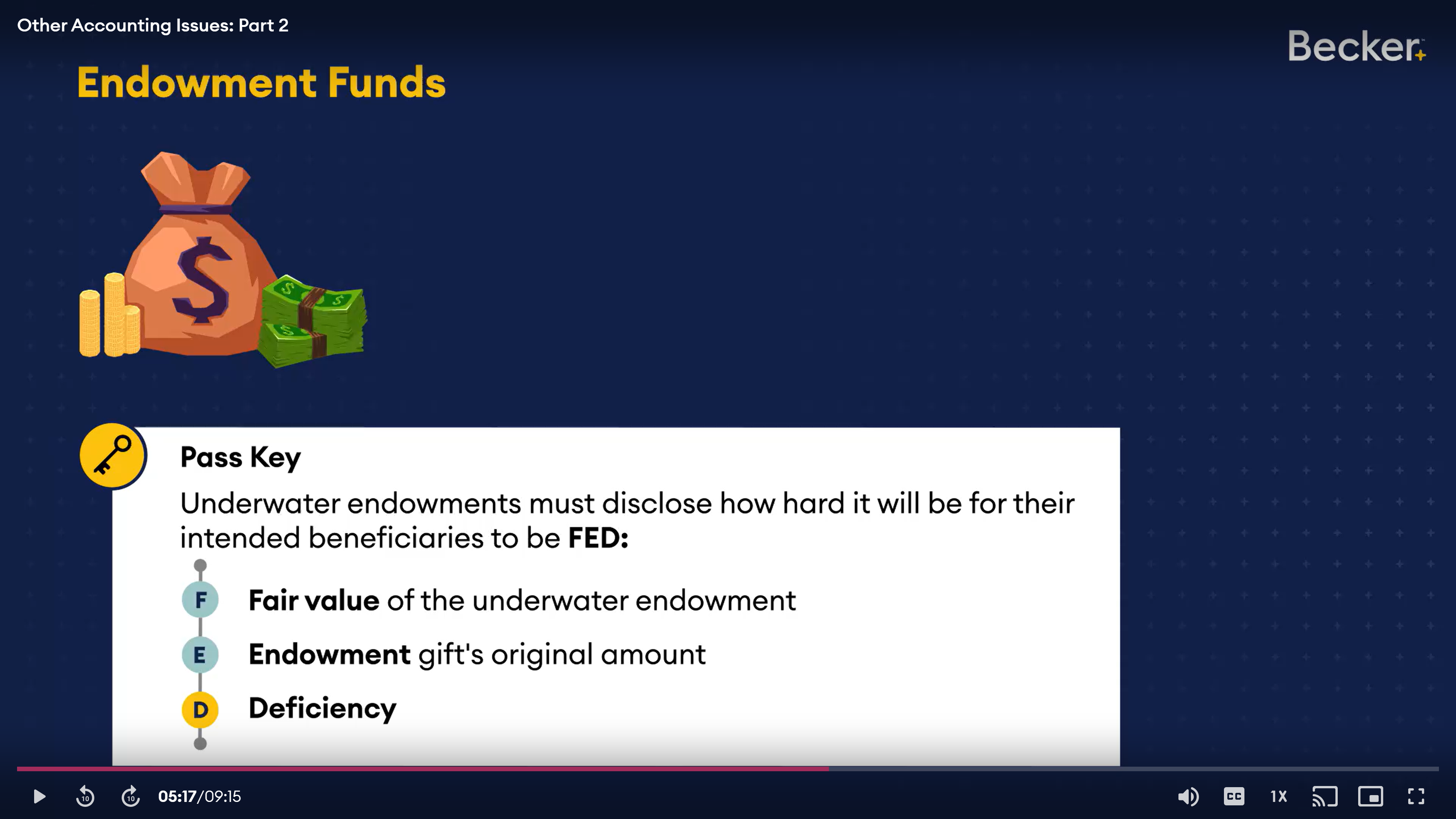

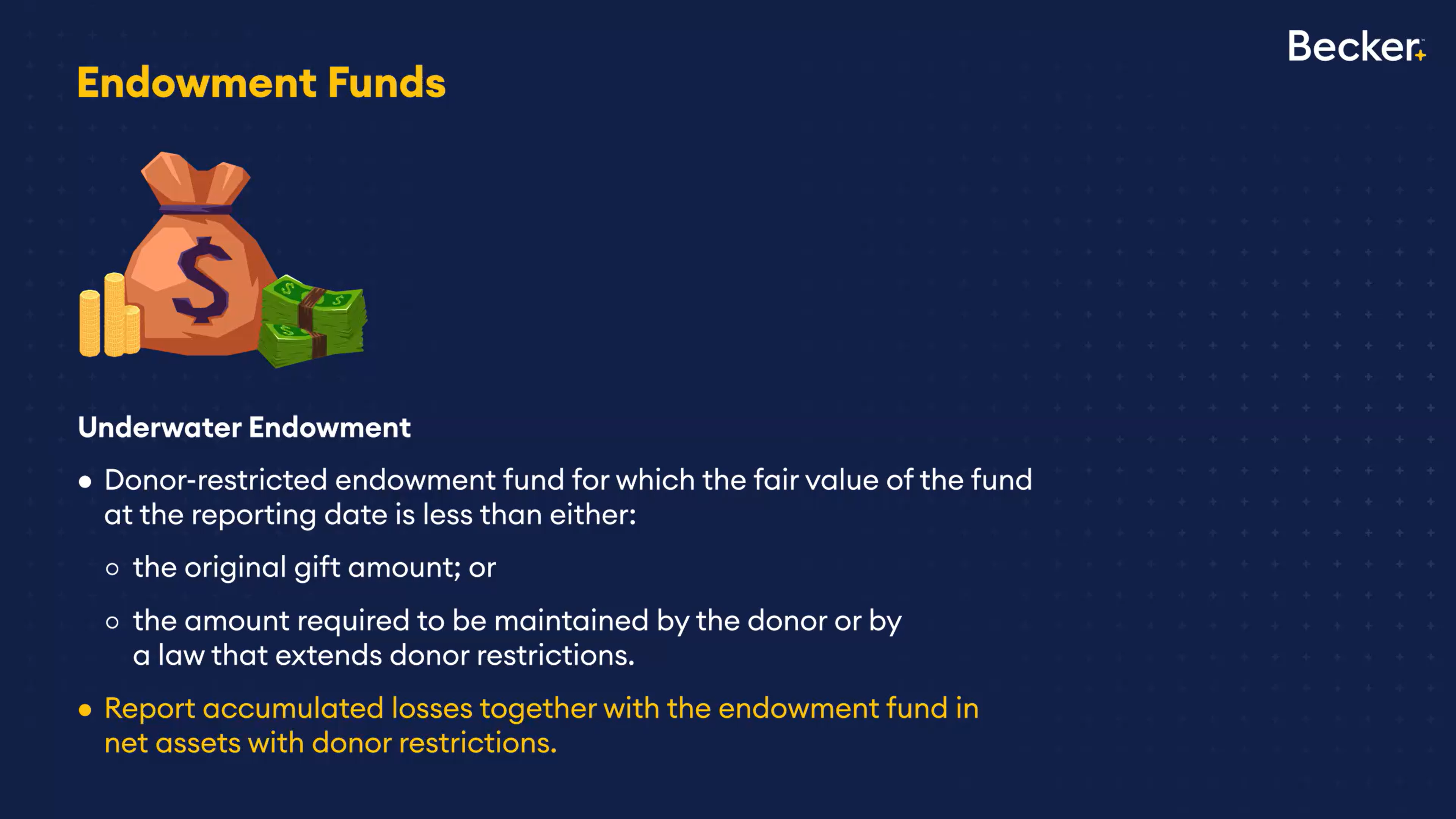

Disclosure rules with endowment with losses(under water endowment)

Endowment fund with losses reporting rules

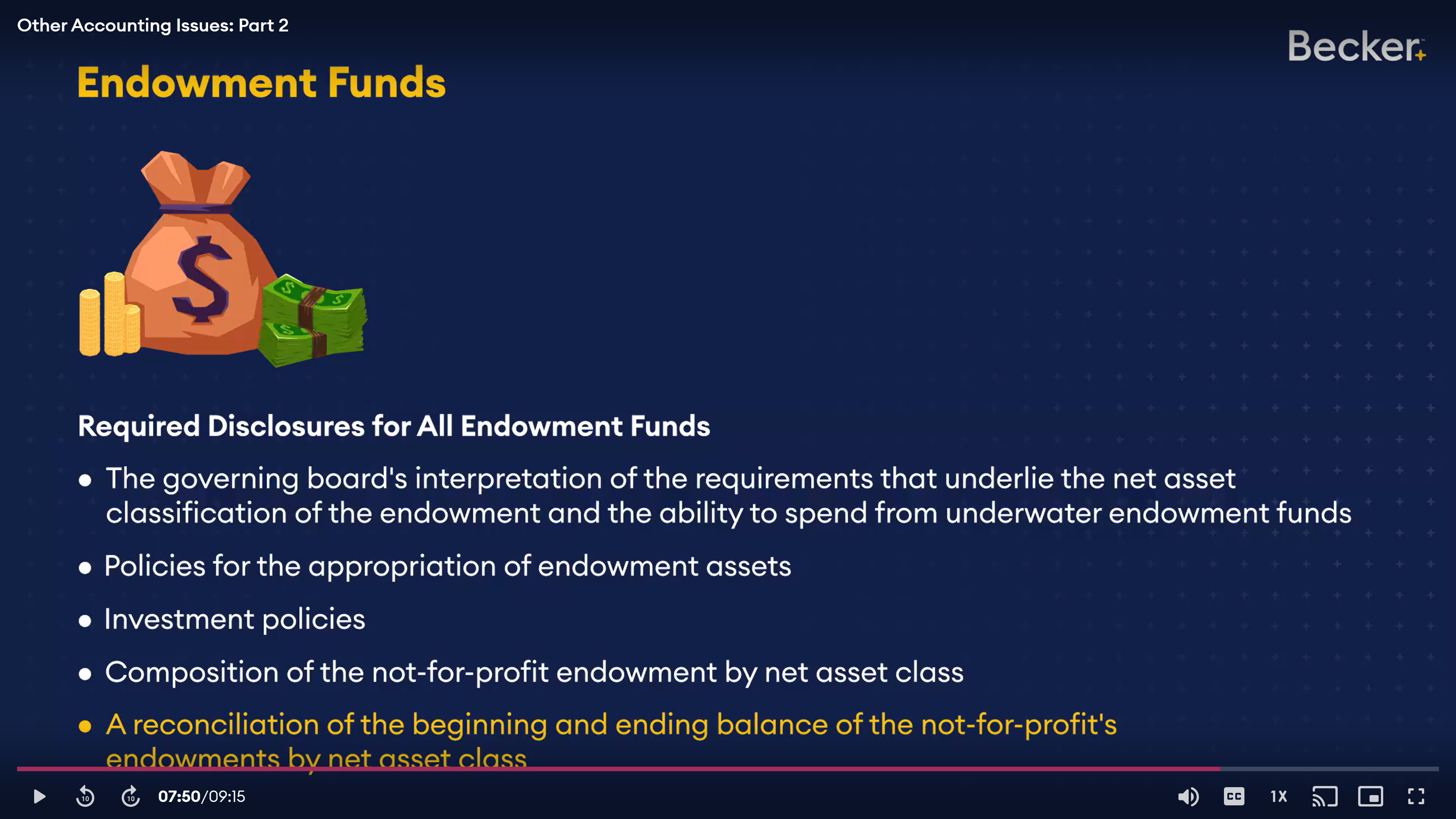

Required disclosures for all endowment funds

Basis rules for assets for non-profits

If acquired by non-profit the asset is recorded at cost

If received via donation- asset is recorded at fair value

depreciation follows GAAP