Microeconomics Final

1/30

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

31 Terms

Cournot game

FIrms compete by setting quantities

How to find reaction functions for firms that compete by setting quantity

Find profit [R - C where R is P(total quantity)*Qi] and set its derivative to zero.

Cournot with a cartel

Find total monopoly profit and take partial derivatives for each quantity set equal to zero. Solve a system of equations.

Incentive for cournot cartel firms to cheat

Check their individual reaction functions in a non-cartel context. What is the best response at the monopoly quantity? Could they do better than the monopoly case?

Deadweight loss with 3rd degree price discrimination

Triangle with points MR = MC, D = MC, and the point on the demand curve with profit maximizing p and q

Finding price and quantity in third degree price discrimination

set MR = MC for each market

How do you relate producer-price and consumer-price after a tax?

Pc - t = Pp

(producer price - consumer price) times change in quantity times ½ is

how to find deadweight loss

When a production function is linear what should you immediately recognize if finding conditional demand??

Labor and capital are perfect substitutes, so pick the least costly one (highest MPL to $ ratio)

Conditional factor demand

For a given level of output, we are finding the demand for the cost minimizing quantity of factors (labor, capital). To find, set MPL/MPK equal to w/r.

Testing returns to scale

If f(2k, 2l) = 2f(k,l) → constant returns to scale

f(2k, 2l) < 2f(k,l) → decreasing returns to scale

f(2k, 2l) > 2f(k,l) → increasing returns to scale

Future value in exactly n period from now

FV=PV×(1+r)n

Present value - how much a sum of money to be received in the future (Future Value, or FV) is worth in today's terms, accounting for the interest rate r

𝑃𝑉 = 𝐹𝑉n/(1 + 𝑟)𝑛

Monopoly/oligopoly barriers to entry

Government franchises

Patents

Economies of scale and other cost advantages

Ownership of a scarce factor of production

Why are monopolies/oligopolies not efficient?

P > MC

Tying and foreclosure contracts were made illegal by ____

Clayton Act of 1914

In 1890, Congress passed the Sherman Act, which

declared ____

– contract or conspiracy to restrain trade among states or nations

illegal

– attempt to monopolize illegal.

The rule of reason is _____

a criterion introduced by the

Supreme Court in 1911 to determine whether a particular

action was illegal (“unreasonable”) or legal

(“reasonable”) within the terms of the Sherman Act.

A per se rule is ____

a rule enunciated by the courts

declaring a particular action or outcome to be a per se

(intrinsic) violation of antitrust law, whether the result is

reasonable or not. Ex. price fixing is illegal whether the resulting

price is reasonable or not.

Profit maximizing condition in short run production

MPL = w/p or MPK = r/p (derived from differentiating profit equation)

How to find short run supply curve

After solving for the derived demand of labor (capital) which is a function of price, subsitute that function in to get quantity as a function of price

What is another way to say, find L that maximizes the firm’s profit?

Find the derived demand for L.

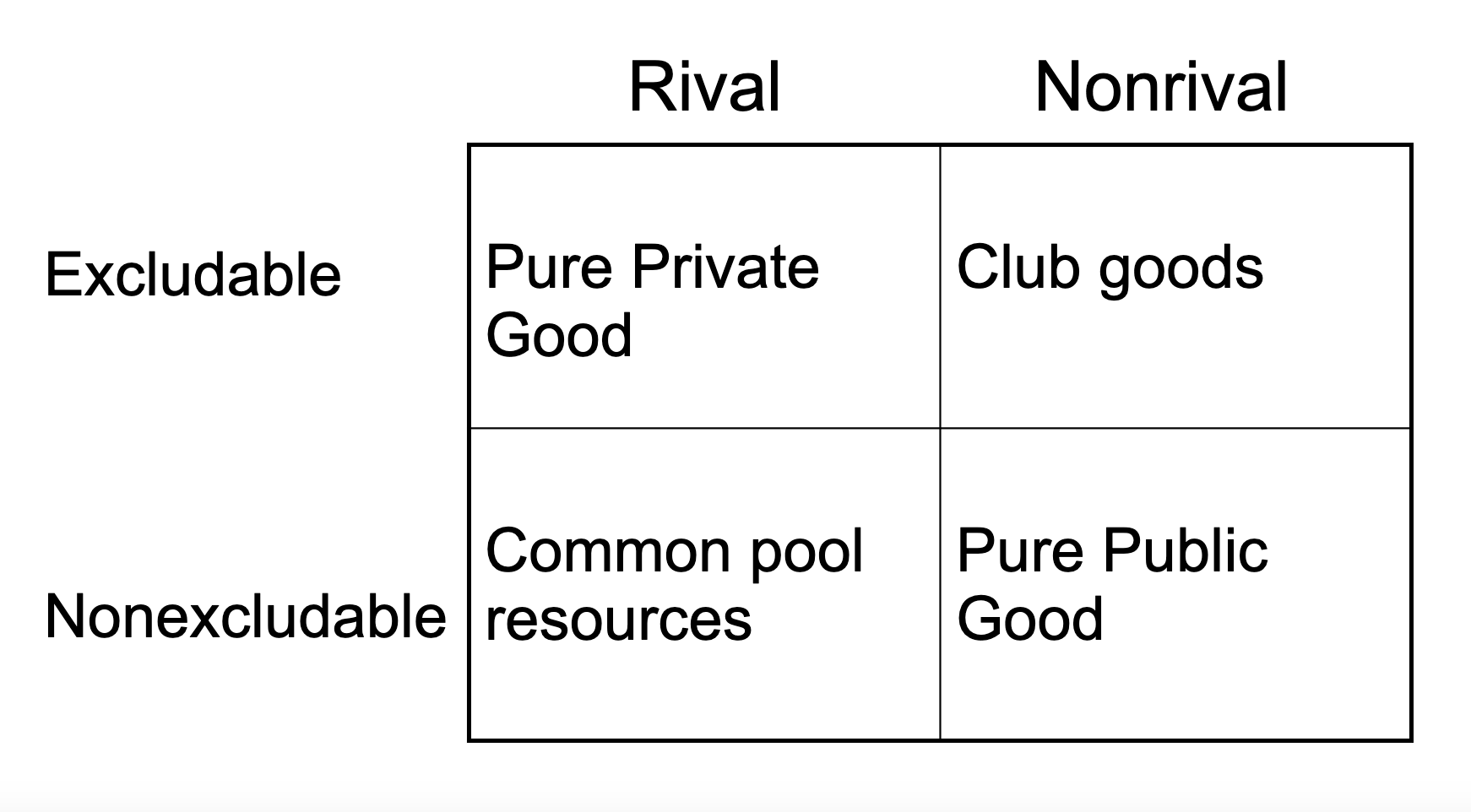

A good is nonexcludable if

once produced, no one can be excluded from enjoying its benefits. ex. security, a road(?). Problem: The private sector will not provide them

Free-rider problem

Because people can enjoy the benefits of nonexcludable goods whether they pay for them or not, they are usually unwilling to pay for them.

A good is non-rival in consumption when

A’s consumption of it does not interfere with B’s consumption of it. ex. security, clean air(?), light, a road (?), information. Congestion affects nonrivalry. The efficient price for a nonrival good is zero, so the private sector should not provide them.

Spectrum of public and private goods

Public goods (social or collective goods)

are goods that are nonrival in consumption and their

benefits are nonexcludable.

drop-in-the-bucket problem

the public good is usually so costly that its provision does

not depend on whether or not any single person

pays.

Sick or high-risk people have a greater

incentive to buy insurance. This problem is called

adverse selection.

Moral Hazard

People act differently when they have insurance compared to when they do not.

Sometimes moral hazard is not serious ex. Lightning strike. The insured has little control over such events. Sometimes moral hazard is serious, ex. Car insurance. Solution: Deductibles and co-payments.

Principal-Agent problem

Usually, the agent has more information about her behavior, talent, or effort level than principal. Examples of agents: Doctors, US gov, CEOs

Solution: Incentive contracts