AP Economics

1/48

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

49 Terms

Why is money demand curve downward sloping?

opportunity costs of holding money rises as interest rate increases (opportunity of missing out on a higher interest rate)

What is crowding out and how does it impact the economy?

When the governments borrowing (i.e. deficit spending), SHIFTS Demand for loanable funds rightwards

-negative economic impact: interest rates rise, deterring private investment spending on physical capital

1/rr (money multiplier) * ALL reserves/funds =

MS addition (STATING THE BANKING SYSTEM DOESN’T WANT EXCESSIVE RESERVE, not prolonged)

M1

Currency in circulation, checkable bank deposits, traveler’s checks

MOST LIQUID

M2

ALL OF M1 + savings, certificates of deposits, money market funds, and other less liquid money (GIFTCARDS AS WELL)

Economists use _____ as a model to show how savers and borrowers come together to determine the equilibrium rate of interest

market for loanable funds

Bank Reserves

The currency kept in a bank’s vault + deposits with the FED

Interest Rate

The price, calculated as a percentage of an amount borrowed, charged by lenders to borrowers of the use of their savings for one year

Budget balance

The difference between tax revenue and government spending

Budget surplus

the difference between tax revenue and government spending when tax revenue exceeds government spending

Budget deficit

The difference between tax revenue and government spending when government spending exceeds tax revenue

National savings

private savings + budget balance

Investment spending identity =

national savings + capital inflow

Capital inflow =

Total inflow of foreign funds - total outflow of domestic funds to other countries

Financial markets

Households invest their current savings and their accumulated savings, or wealth, by purchasing financial assets

Financial asset

Paper claim that entitles the buyer to future income from the seller

Physical asset

claim on a tangible object that gives the owner the right to dispose of the object as he or she wishes

liability

A requirement to pay money in the future

TASKS OF THE FINANCIAL SYSTEM

1) Reducing transaction costs (expenses of negotiating and executing a deal)

2) Reducing risk

3) Financial risk (uncertainty about future outcomes that involve financial losses and gains)

Money

any asset that can easily be used to purchase goods and services

Medium of exchange

an asset that individuals acquire for the purpose of trading for goods and services rather than for their own goods and services rather than consumption

Store of value

holding purchasing power

EXAMPLE: Metal coins make a better store of value due to their durability, compared to grains and ice cream cones

Unit of account

A measure used to set prices and makes calculations

EXAMPLE: price comparisons among products

Commodity money

good used as a medium of exchange that has intrinsic value in other uses

Commodity-backed money

A medium of exchange with no intrinsic value whose ultimate value is guaranteed by a promise that can be converted into valuable goods

Fiat money

A medium of exchange whose value derives entirely from its official status as a means of payment

Bond prices and interest rates relationship

negative/inverse

Reserve ration

The fraction of bank deposits that a bank holds as reserves

REQUIRED-smallest FED requires bank to hold

Bank run

When many of a bank’s depositors try to withdraw their funds due to fears of a bank failure

FOUR FEATURES of bank regulation

-Deposit insurance (FDIC guarantees up to 250,00 per account if bank can’t meet obligations)

-Capital requirements (Making banks hold more capital means losses incurred when loans go bad accrue against the bank’s assets rather than government insurers)

-Reserve Requirements (Rules set by the FED that determine the require reserve ratio for banks)

-Discount Windows (Allows banks to quickly borrow money from the FED in an emergency)

Monetary base

sum of currency in circulation and bank reserves

Central bank

An institution that oversees and regulates the banking system and controls the monetary base

Commercial bank vs. investment bank

COMMERCIAL- accepts deposits and is covered by deposit insurance

INVESTMENT- trades in financial assets and is not covered by deposit insurance

Four basic function of the FED

1) Provide financial services to depository institutions

2) Regulate banks and other financial institutions

3) Maintain financial system stability

4) Conduct monetary policy

Federal funds rate

-set by supply and demand in the federal funds market

-greatly influenced by FED’s actions

-Banks borrow additional reserves from other banks

INCREASE MONEY SUPPLY (monetary policy)

decrease reserve req. - increase MS in banks, more loans, decreased interest rates, more money to consumers + increased investment spending

decrease discount rate -allows more banks to borrow from the FED, increased MS

buys treasury bills- money supply increase by allotting more money to the banks, decrease interest rates

DECREASE MONEY SUPPLY (monetary policy)

increase reserve req.- banks have less funds/decreased MS, increased interest rates, less money to consumers + decreased investment spending

increase discount rates- prevents banks from borrowing from FED (financial barrier), decreased MS

sells treasury bills- decreased money supply by taking away money from banks, increased interest rates

Discount rate

Banks borrow from the FED

Benefit + cost to holding money

BENEFIT: convenience, liquid → easily converted into goods and services)

OPPORTUNITY COSTS: earns no interests

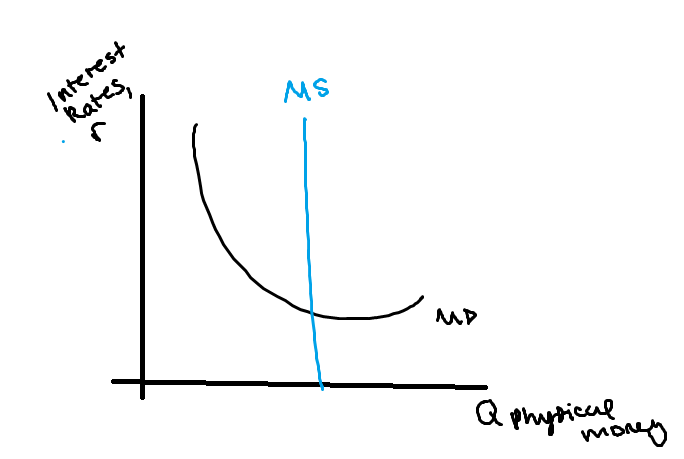

Money demand (SPECIFICALLY PHYSICAL CASH)

WHAT CHANGES MD? (for physical cash)

1) Changes in aggregate price level

HIGHER PRICES = INCREASED MD

LOWER PRICES = DECREASED MD

2) Changes in real GDP (consumer confidence)

INCREASE IN GDP = INCREASED MD

DECREASE IN GDP = DECREASED MD

3) Changes in banking tech.

MORE ACCESSIBILITY TO PHYSICAL CASH/PAYMENT= DECREASE

LESS ACCESSIBILITY TO PHYSICAL CASH/PAYMENT = INCREASE

4) Changes in banking institutions

AFTER interest checking was legal, MD shifted right

MS is set by

FED… (Specifically for money demand graph)

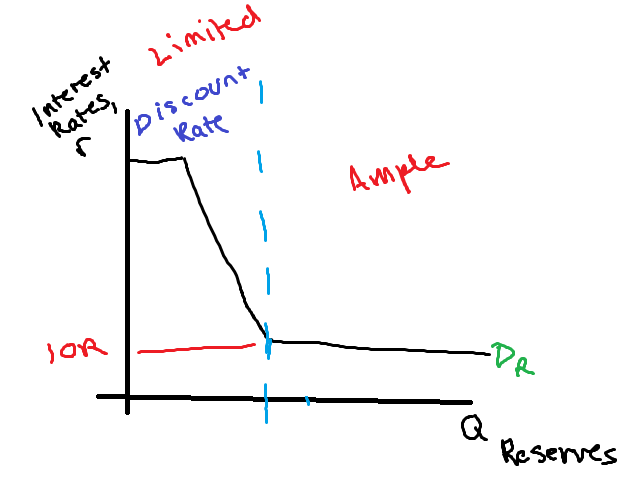

Reserves graph

Changing the IOR

Lowering IOR- banks loan out more of their excessive reserves = INCREASED MS

Raising IOR- causes banks to hold more in reserves = DECREASED MS

Loanable funds market

brings together those who want to lend and those who want to borrow money

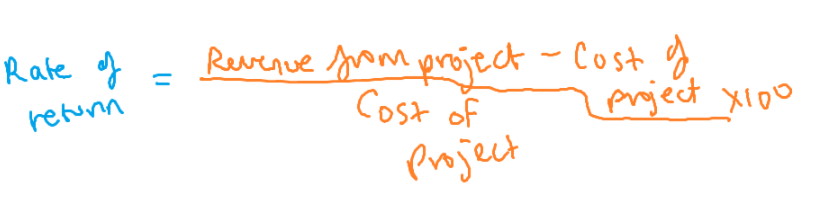

Rate of return

FACTORS THAT CAUSE DEMAND FOR LOANABLE FUNDS TO SHIFT

1) CHANGES IN PERCEIVED BUSINESS OPPORTUNITIES

increase in opportunities = borrow more

lessen in opportunities = borrow less

2) CHANGES IN GOVERNMENT BORROWING

increase in government borrowing = Dlf increase

decrease in government borrowing = Dlf decreases

Factors that cause the supply of loanable funds to shift

1) CHANGES IN PRIVATE SAVING

Household saves more = Slf increases

Households save less = Slf decreases

2)CHANGES IN CAPITAL INFLOWS

funds into country = right

funds out country = left

Fisher effect

An increase in expected inflation drives the nominal interest rate upward by the same percentage, leaving the expected real interest rate unchanged