ACCT 201B - Chapter 9: Flexible budgets, Standard Costs, and Variance Analysis

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

18 Terms

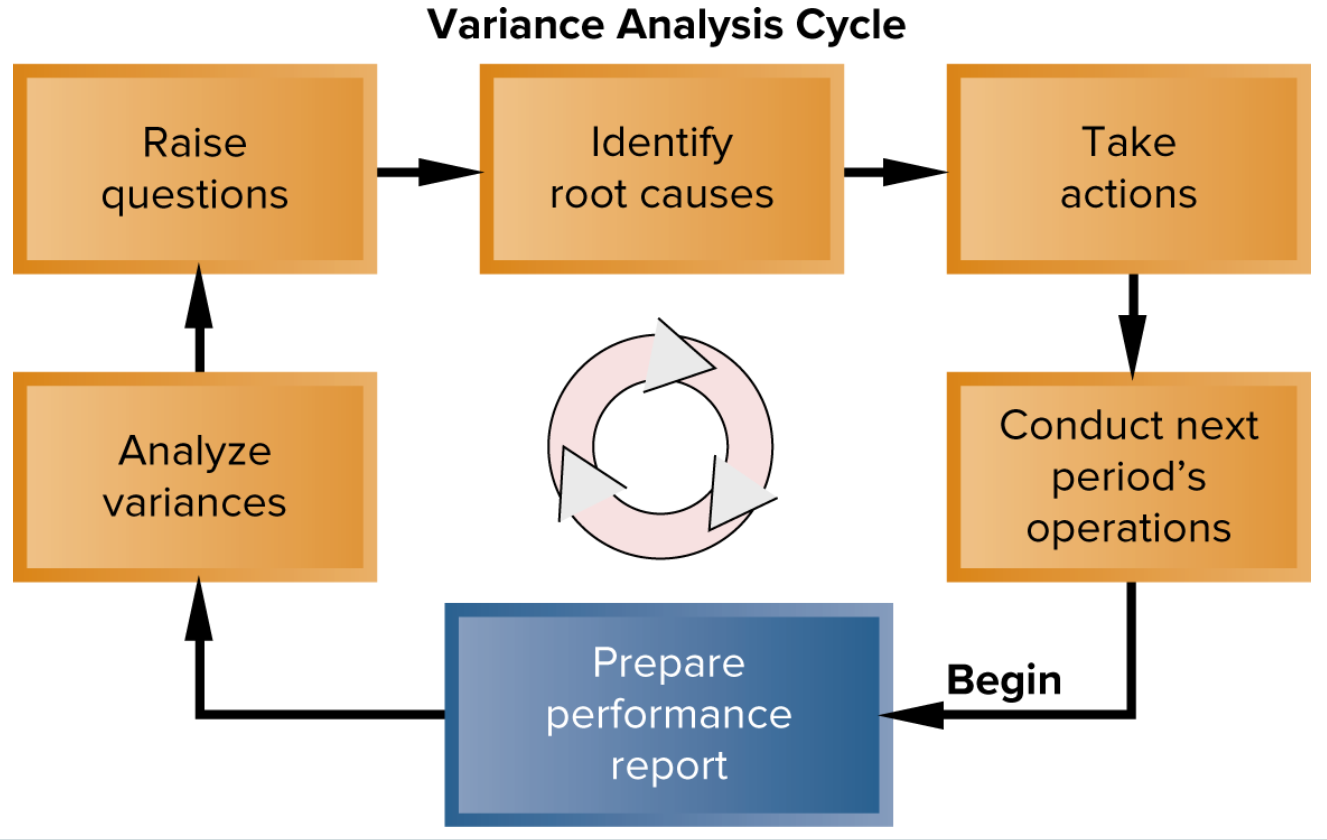

Variance Analysis Cycle

evaluates and improves performance

planning budget

prepared before the period begins and is valid for only the planned level of activity

static planning budget

used for planning but is inappropriate when evaluating how well costs are controlled

flexible budget

shows what costs and revenues should have been given the actual level of activity

revenue variance

the difference between the actual revenue and what the revenue should have been, given the actual level of activity

spending variance

the difference between the actual amount of the cost and how much a cost should of been

cost driver

any factor that directly causes changes in the cost of activities

standard

benchmark for measuring performance

standard quantity per unit

defines the amount of direct materials that should be used for each unit of finished product, includes allowance for normal inefficiencies like scrap and spoilage

standard hours per unit

defines amount of direct labor hours that should be used to produce one unit of finished goods

price variance

difference between the actual amount paid for an input and the standard amount that should have been paid, multiplied by actual amount of input purchased

quantity variance

the difference between how much of an input was actually used and how much should have been used and is stated in terms of dollar using standard price of the input

standard rate per unit

defines that a company expects to pay for variable overhead equals the variable portion of the predetermined overhead rate

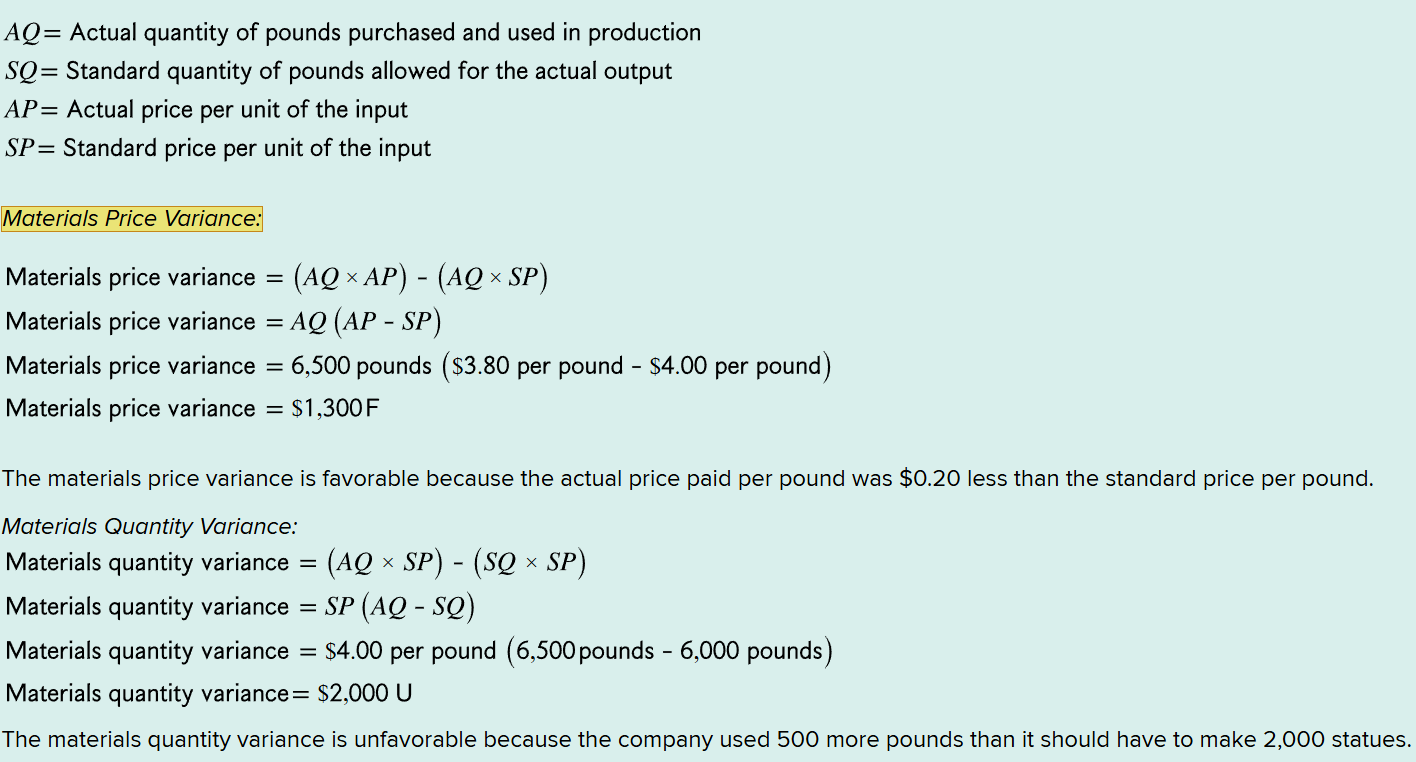

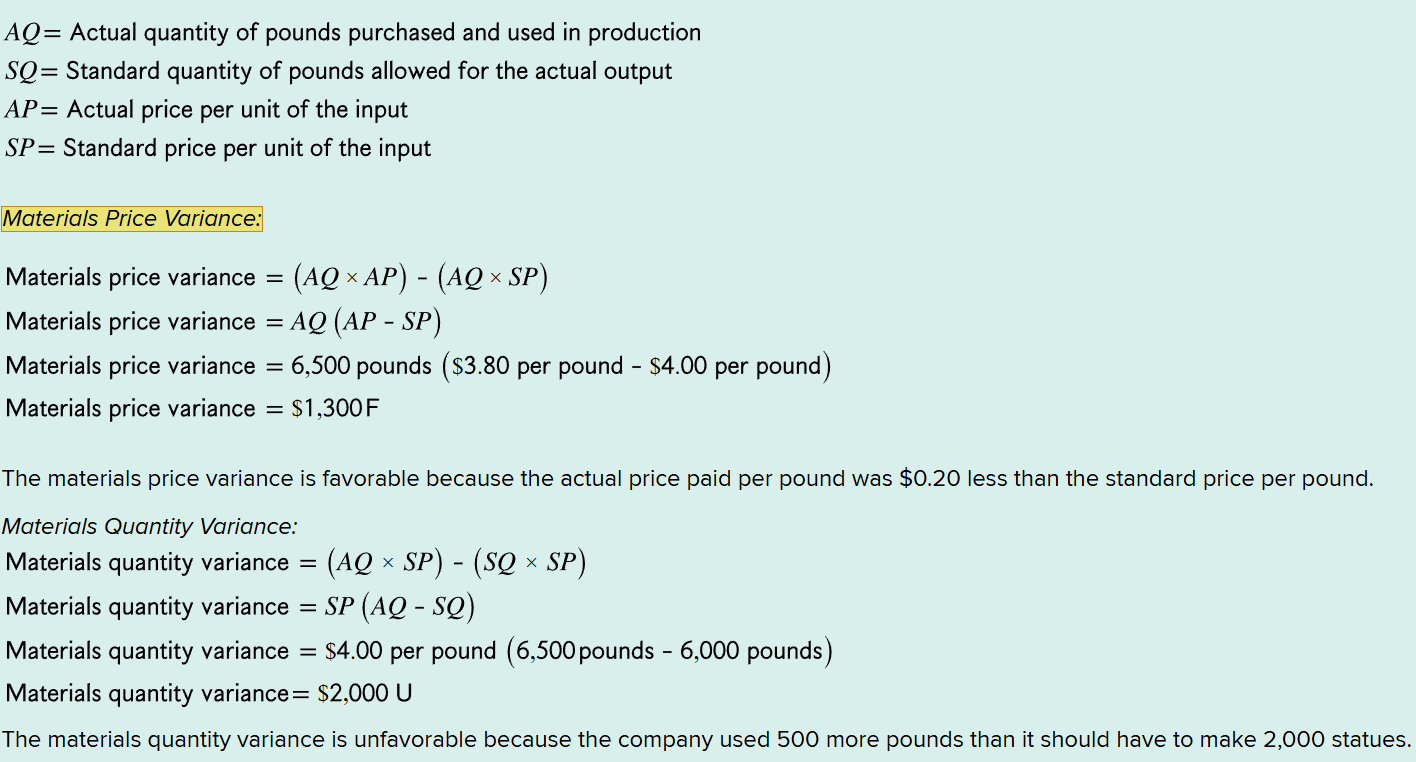

materials quantity variance

measures the difference between the actual quantity of materials used in production and the standard quantity of materials allowed for the actual output, multiplied by the standard price per unit of materials

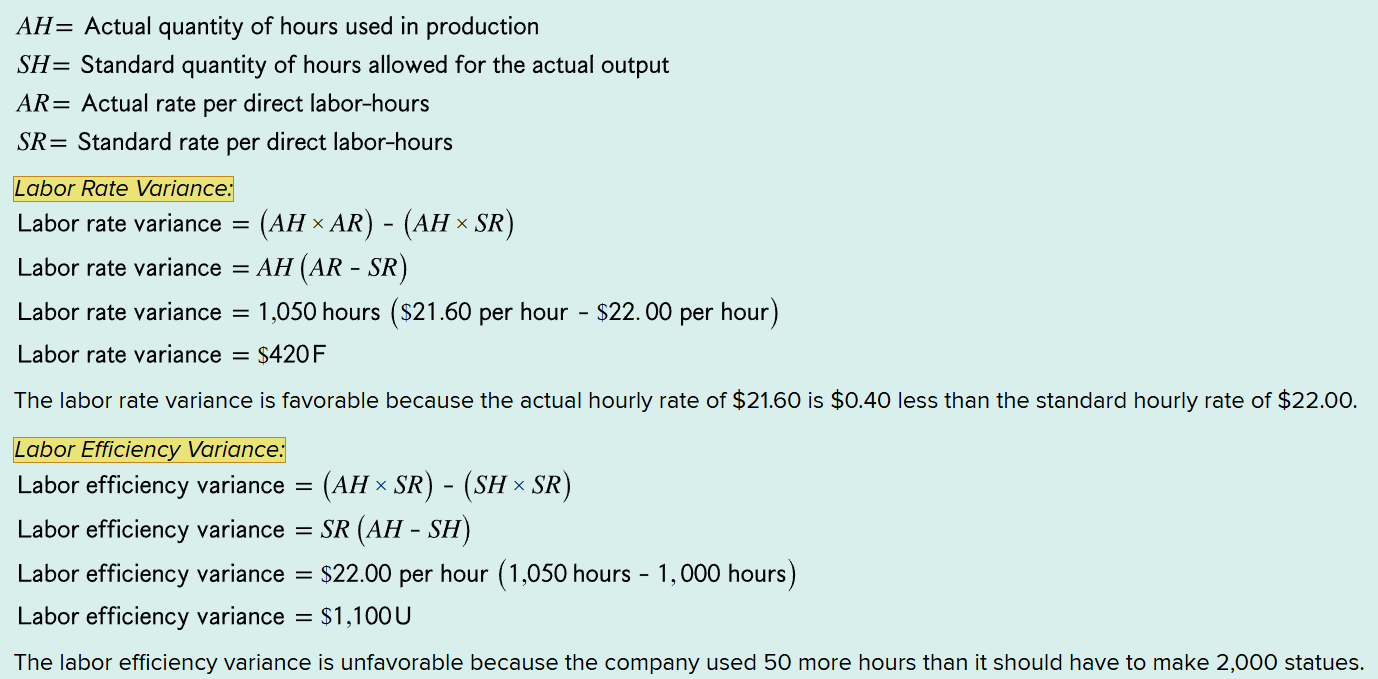

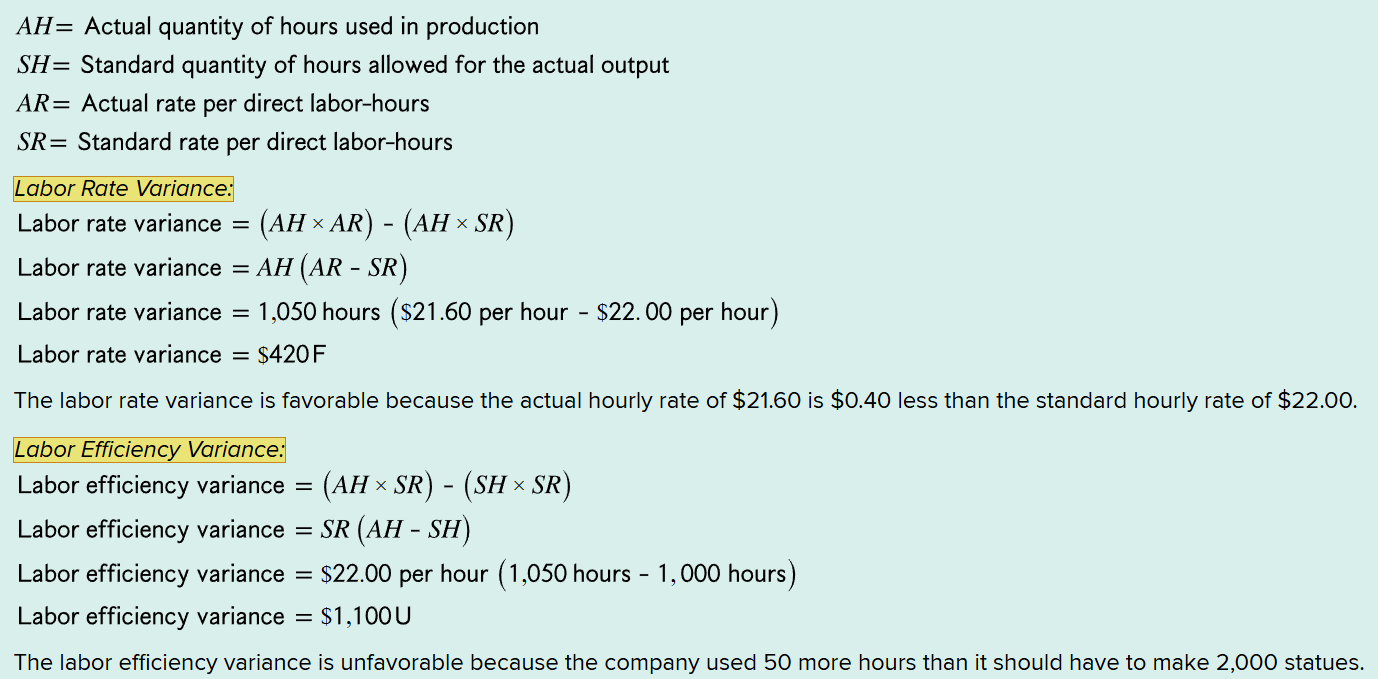

labor rate variance

measures the difference between the actual hourly rate and the standard hourly rate, multiplied by the actual number of hours worked during the period; actual rate > standard rate = unfavorable

labor efficiency variance

measures the difference between the actual labor-hours used and the standard hours allowed for the actual output, multiplied by standard hourly rate; actual hours < standard hours = favorable

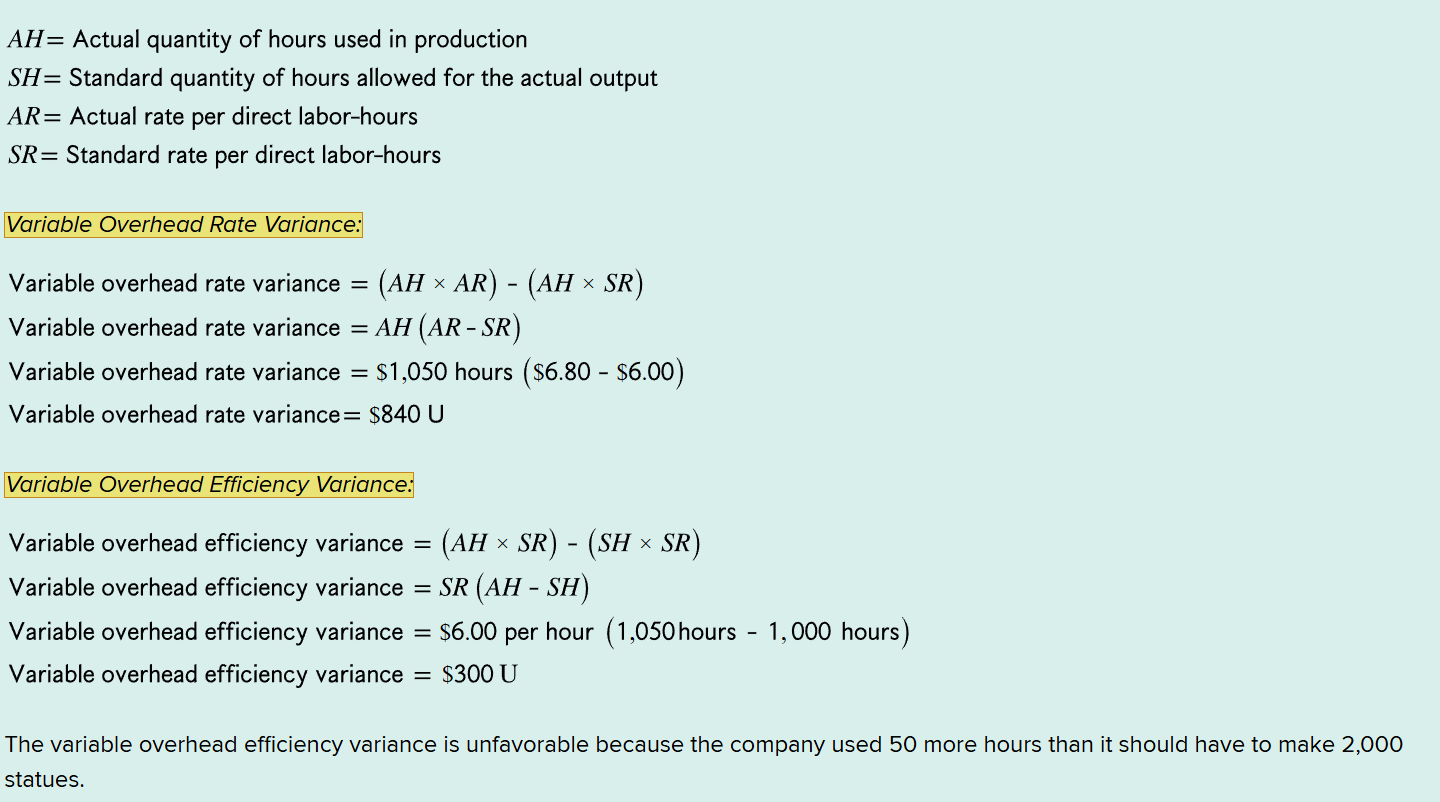

variable overhead rate variance

actual > standard = unfavorable

materials price variance

measures the difference between a direct material’s actual price per unit and its standard price per unit, multiplied by the actual quantity purchased