(1AA3) Chapter 6: PPE and Intangible Assets

1/29

Earn XP

Description and Tags

Final Exam review

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

30 Terms

Acquisition Cost

The cost at which an asset is reported on the balance sheet

Used in calculating the depreciation expense

Cost principle

When a business buys an asset, the cost they record isn’t just the purchase price.

It includes everything necessary to prepare the asset for use.

Subsequent expenditures

Any expenditures once an asset is put to use

Includes:

Revenue expenditures

Capital expenditures

Revenue Expenditures

Expenditures that are necessary to keep the asset in good running condition

Classified as operating expenses on the income statement

What is an immediate expense?

Maintenance or repair → expensed right away.

Capital expenditure

Increase the useful life of an asset

Increase an asset's capacity

Improve the performance of an asset 0

Added to the cost of the asset

Capitalizing a revenue expenditure will:

Understate expenses

Overstate net income

Overstate assets

Lump Sum purchases

Businesses buy more than one asset in a single transaction with a single quoted price

For example, a business acquires a building for $5 million

This $5 million covers the cost of the land and building of the asset

However, on the Balance Sheet, we can't have an account called Land and Building

Depreciation

The systematic allocation of an asset's cost over its useful life

Not meant to reflect the drop in an asset’s value

Depreciation - cost

Acquistion cost of an asset

Salvage Value (or residual value)

What the company expects to recover from the sale of an asset at the end of its useful life

Useful life

Number of years for which a business expects to use the asset

Depreciation cost

Cost - Salvage Value

Accumulated Depreication (AD)

The sum of depreciation

Expense over the years since the asset was acquired

At the end of its useful life, AD = depreciable cost

Book value

Cost - Accumulated Depreciation

3 Depreciation methods

Straight line method (SLM)

Double diminishing balance / doubling declining balance (DDB)

Units of activity

Straight line method (SLM)

Depreciation expense is the same every year

Straight line method (SLM) - Formula

SLM annual depreciation expense = (cost – salvage value) / useful life

Double declining balance (DDB)

Accelerated depreciation method

Yields the highest depreciation expense in the earliest years of an asset’s useful life

Lower depreciation expense in later years

Double declining balance (DDB) - Formula

DDB annual depreciation expense = beginning book value x depreciation rate

Depreciation rate = 2/ useful life

Units of activity

Need to have a measure of activity, such as:

Mileage for vehicles

Need to have an estimate of the total activity

For example, need to know the total mileage for a vehicle over its useful life

Units of activity - Formula

Units of activity annual depreciation expense =

(cost – salvage value) x (units of activity / total units of activity)

Sale of Long term assets

Record depreciation expense on the day of the assets sale

Record gains or losses on the sale of the asset

Record the journal entry

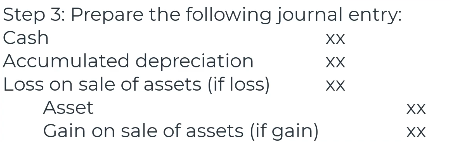

Sale of Long term assets - Journal Entry

Does depreciation reflect asset market value?

No, it allocates cost over useful life.

Can a fully depreciated asset still be used?

Yes, but no more depreciation recorded.

What do you record when disposing fully depreciated asset with no proceeds?

Remove asset and accumulated depreciation. No gain/loss.

When is an asset impaired?

When carrying amount > recoverable amount.

Recoverable amount

Higher of fair value (less cost to sell) or value in use.

What measures profitability?

Return on Assets (ROA)

shows how efficiently a company uses its assets to generate profit.