ACCT 230 Exam 2 Study Guide

1/32

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

33 Terms

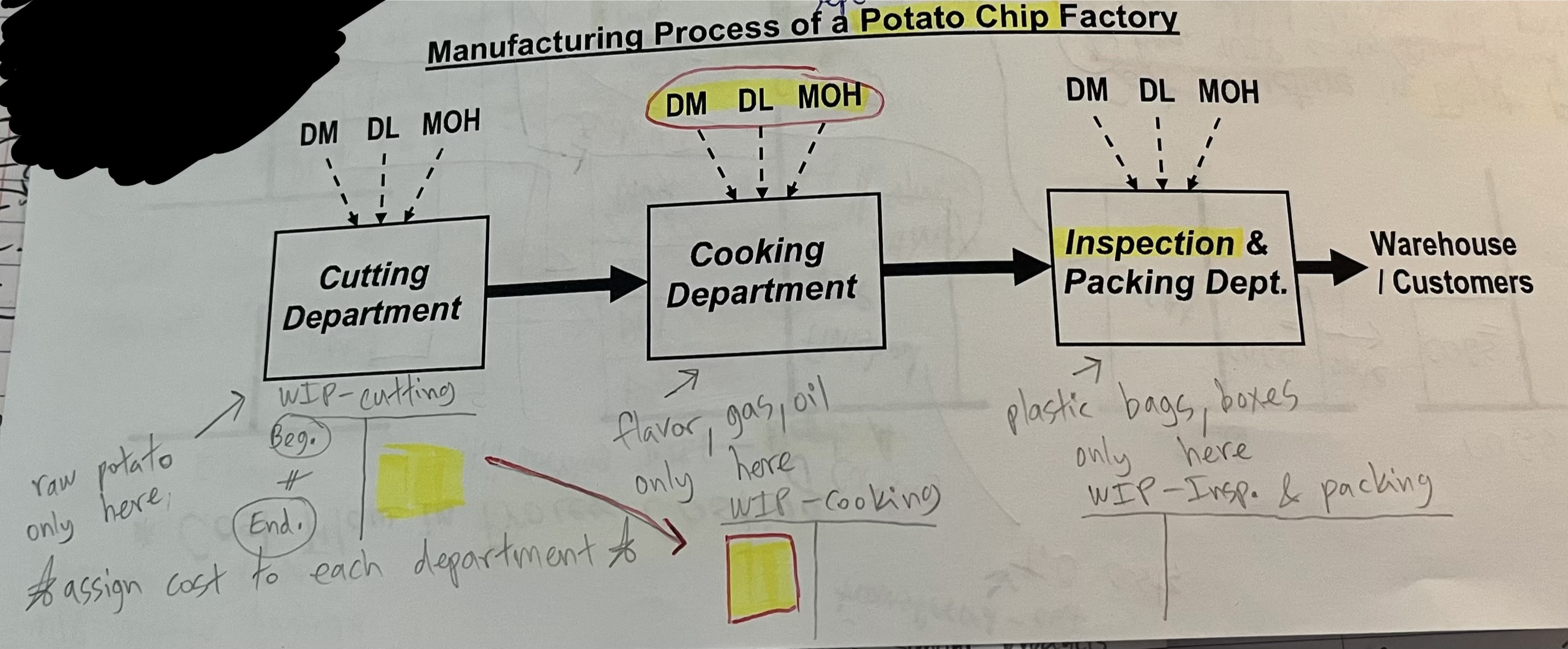

Key characteristics of Process Costing: 1. A large # of

homogenous products pass through a series of similar processes (=manufacturing department)

Key characteristics of Process Costing: 2. In each process,

materials, labor, & overhead inputs may be needed.

cost objective

JO: individual jobs, product batch

process: dept.

Key characteristics of Process Costing: 3. Manufacturing costs are

accumulated by a process for a period of time.

Key characteristics of Process Costing: 4. There is a

“Work-in-Process” account for each process.

# of WIP

JO: only one

process: seperate WIP for each dept.

Key characteristics of Process Costing: 5. Cost flows and the associated journal entries

are similar to job-order costing.

Key characteristics of Process Costing: 6. The departmental “production cost report”

is the key document for tracking manufacturing activities and costs in each process.

key documents

JO: job cost sheets

process: production cost report

Key characteristics of Process Costing: 7. Unit costs are computed by

dividing the departmental costs of the period by the output of the period. → Averaging-out approach

averaging-out approach: process, JO → costing approach

averaging out: individual seperative costing

Type of production system suitable for Process Costing: What are the examples of manufacturers that may adopt process costing?

Manufacturing Process of a Potato Chip Factory

can start cooking only when receive from cutting dept.

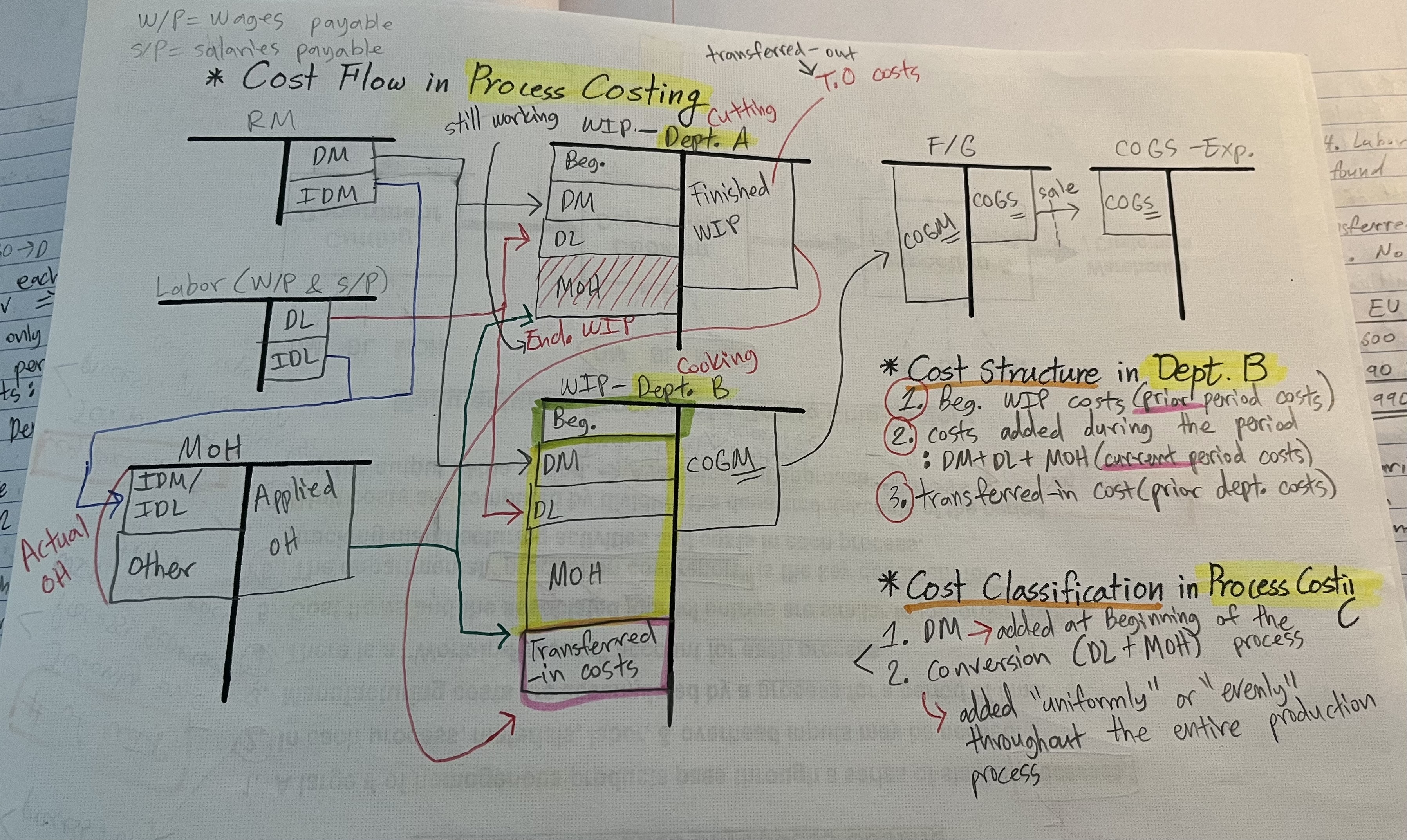

Cost flow under process costing in a T-account system

beg. inv. not = to end. inv. → inv. changing

beg. inv. → leftover from last period

transferred-in costs: from previous dept.

Dept. A has own, Dept. B has transfer from A

Cost flow under process costing in a T-account system: Where are the costs assigned? Individual products or departments?

In process costing, each department (process) accumulates its costs in a WIP account. When the work is finished in a process, the units and their associated costs are transferred to the next department by debiting the WIP account of the department receiving the units and crediting the WIP account of the transferring department

Cost flow under process costing in a T-account system: What kinds of costs are accumulated in each department (e.g., what costs will be added to the debit side of WIP account for the 1st and 2nd departments)? → See your notes on the slide (i.e., the cost flow chart).

DM, DL, MOH is accumulated in each dept.

Debit side of WIP account for 1st dept.:

Beg. WIP costs, DM, DL, MOH, End. WIP

Debit side of WIP account for 2nd dept.:

Beg. WIP costs, DM, DL, MOH, Transferred-in costs

What is the key source document used in process costing?

Production Cost Report

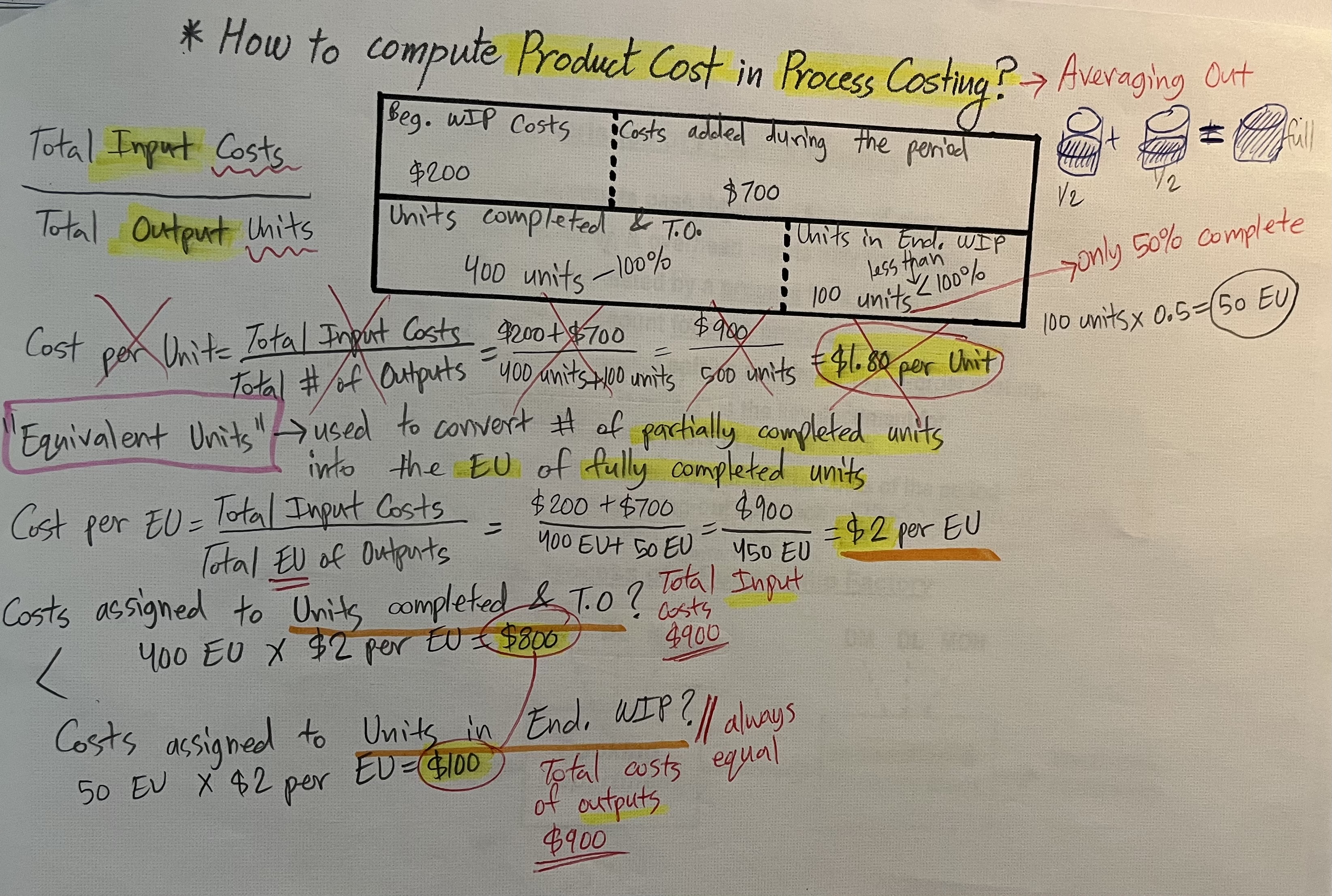

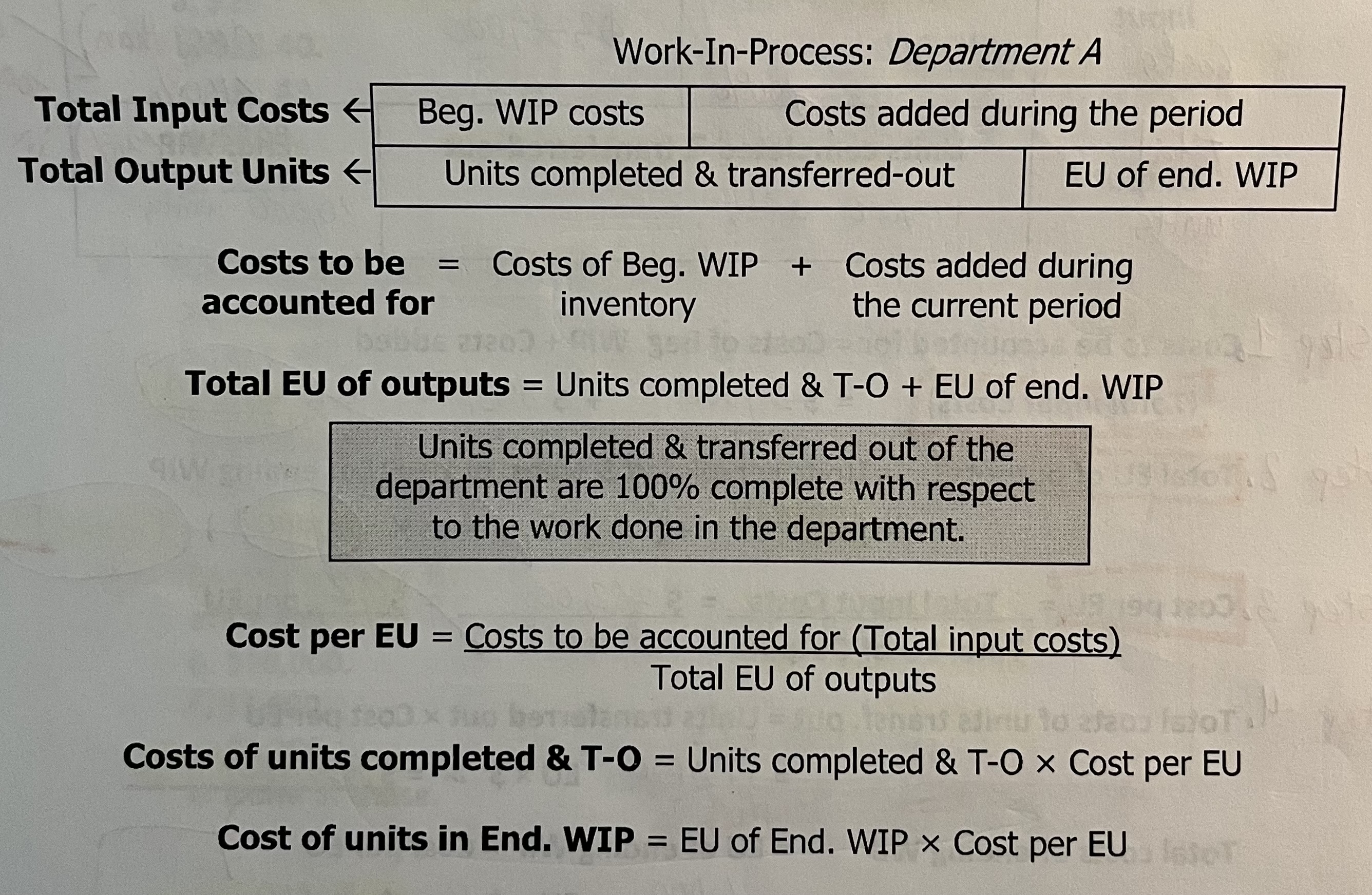

How to compute product cost using the “weighted-average” method?

find EU (equivalent units)

find Cost per EU

find Costs assigned to Units completed & T.O. (transferred out)

find Costs assigned to Units in End. WIP

What is the “Weighted-Average” costing method? How the beginning WIP costs (i.e., past period costs) are treated under this method? See the handout!

The weighted-average method does not track prior period output and costs separately from current period output and costs. It simply combines the costs in beginning WIP inventories (prior-period costs) with the costs added during the current period (current-period costs). These combined input costs are treated as if they were incurred during the current period.

Pros & cons of the weighted-average method? See the handout!

The weighted-average method may not provide accurate “period” performance measures because it combines the performance of the current period with that of a prior period. But, it saves considerable time and effort in product costing because of its simplicity.

What is the costing procedure used by the weighted-average method?

For each category of cost in each processing department, the following calculations are made:

(1) How to determine Total Input Costs (Costs to be accounted for)?

Beg. WIP costs + Costs added during the period

(2) How to determine Total EU of Outputs?

Units completed and transferred-out + EU of end. WIP

Units completed & transferred out of the department are 100% complete with respect to the work done in the department.

“equivalent units” → used to convert # of partially completed units into the EU of fully completed units

(3) How to compute Cost per EU?

Costs to be accounted for (Total input costs) / Total EU of outputs

(4) How to calculate Total Costs of Units Completed & Transferred-Out?

Units completed & T-O × Cost per EU

(5) How to calculate Total Costs of Ending WIP Units?

EU of End. WIP × Cost per EU

In terms of the flow of physical units, the numbers of total inputs (i.e., Units in Beg. WIP + Units Started) and total outputs (i.e., Units Completed & Transferred-Out + Units in End. WIP)

should always equal!

CVP Analysis

Cost Volume Profit Analysis

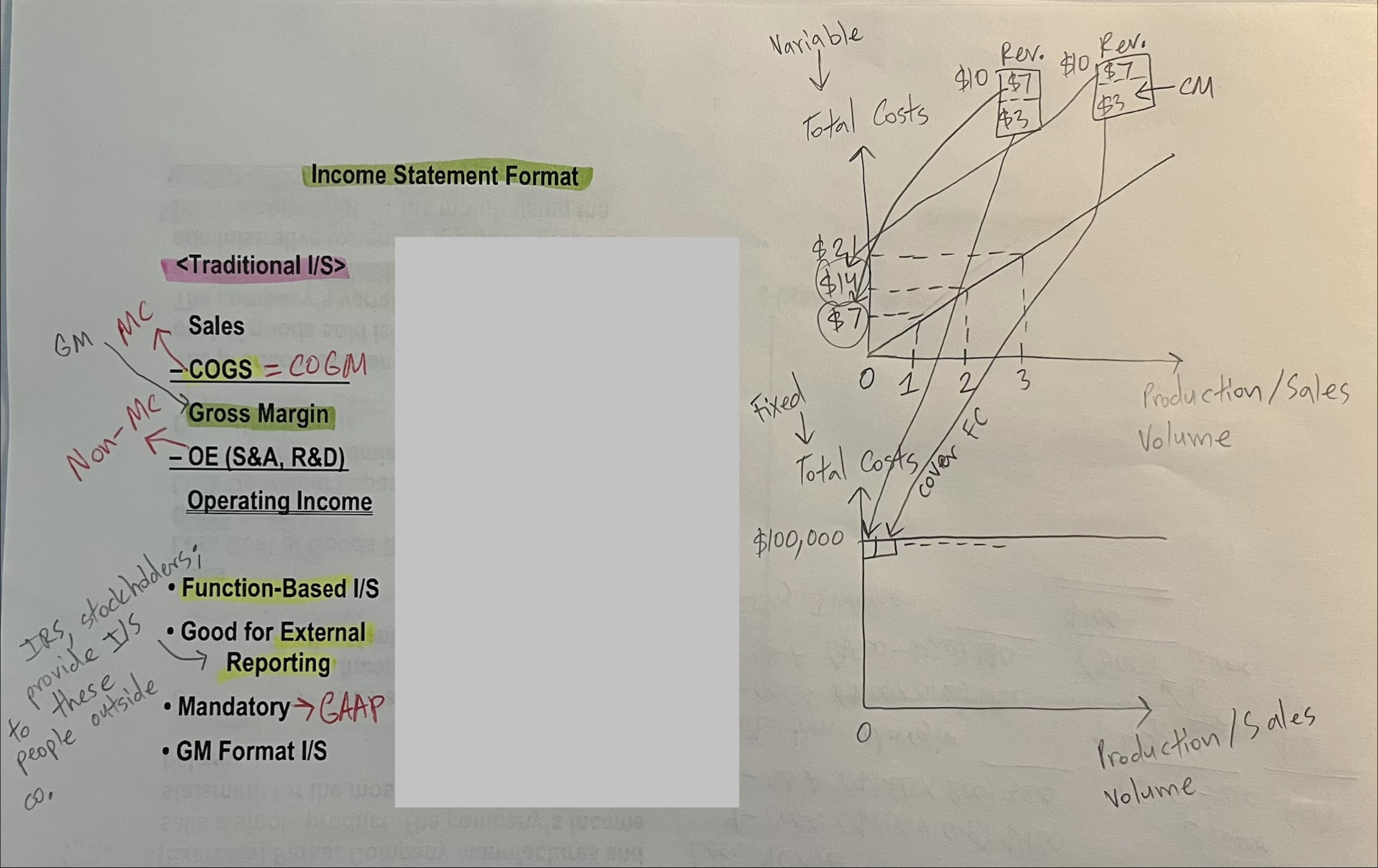

Traditional income statement

costs are organized and classified according to function (i.e., manufacturing vs. non-manufacturing).

→ Function-based; Good for external reporting; Mandatory (follows GAAP); GM (gross margin) format I/S

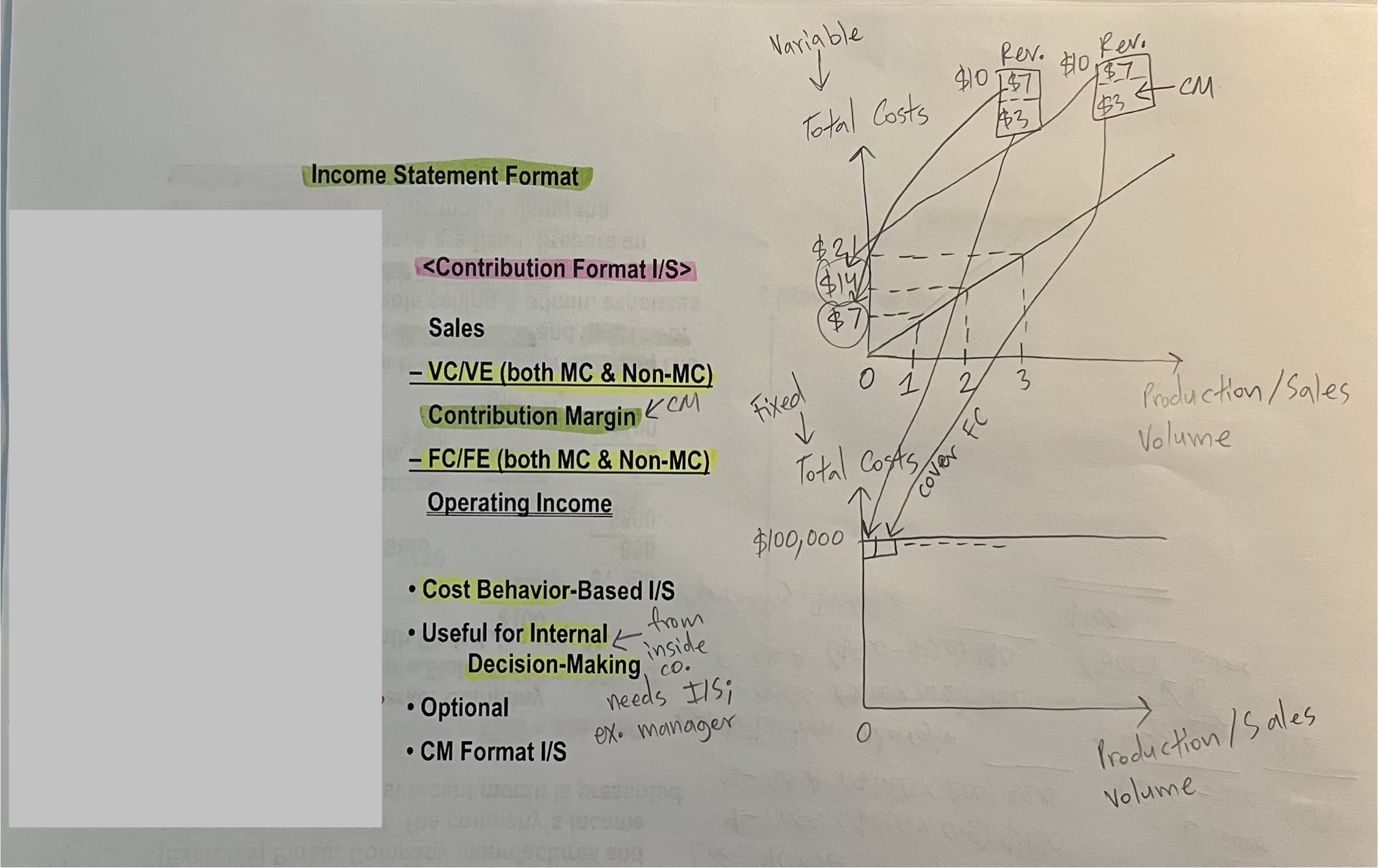

Contribution format income statement

classifies costs by behavior (i.e., variable vs. fixed).

→ Cost behavior-based; Good for internal decision-making (e.g., planning & control); Optional (does not follows GAAP), CM (contribution margin) format I/S

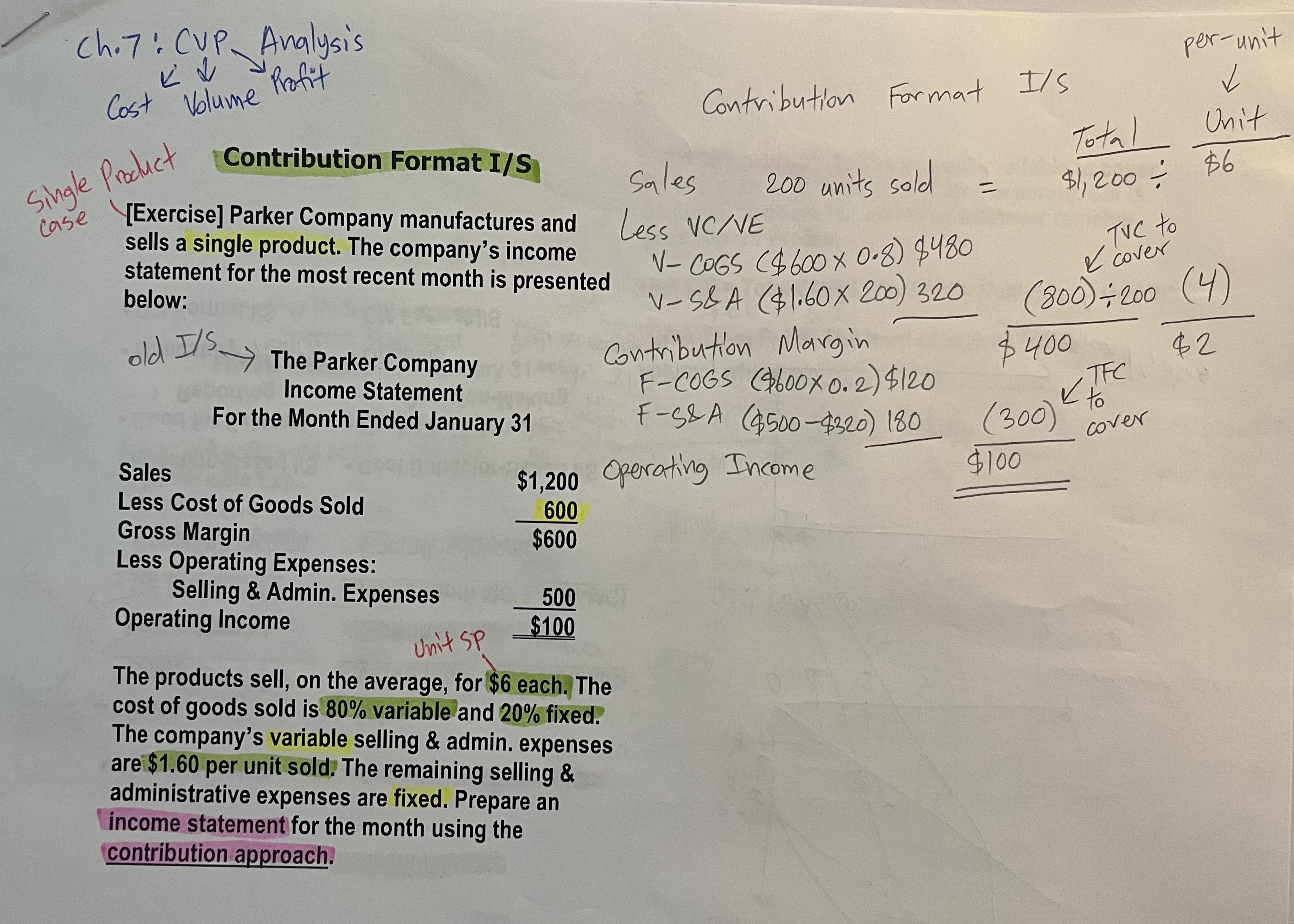

How to prepare a contribution format income statement using a traditional income statement when there is the cost behavior information (i.e., variable/fixed) available for every expense item? → Review the exercise problem in “[Handout] CVP Analysis (1)”!

Sales (=revenue)

Less VC/VE (=variable cost → cover more easily; variable expense)

V-COGS (=variable COGS)

V-S&A

Contribution Margin

F-COGS (=Fixed COGS)

F-S&A

Operating Income (=OI)

What is the Contribution Margin?

Total CM = Total Sales – Total VC;

Used to cover FC first and then to make profits.

CM = Rev – Total VC: The amount available to cover FC and then to provide profits for the period. CM is used first to cover FC, and then whatever remains goes toward Profits.

Unit Selling Price from a contribution format income statement?

Number of Units Sold / Total Sales Revenue

Unit Variable Cost from a contribution format income statement?

Number of Units Produced or Sold / Total Variable Costs

Unit Contribution Margin from a contribution format income statement?

Unit Selling Price−Unit Variable Cost

Units Sold / Total Sales Revenue−Total Variable Costs

Total CM / # Units Sold = Unit Price - Unit VC

Variable Cost Ratio from a contribution format income statement?

Total Sales / Total Variable Costs

Unit Selling Price / Unit Variable Cost

Contribution Margin Ratio from a contribution format income statement?

Sales / Contribution Margin

Unit Selling Price / Unit CM

Unit Selling Price, Unit Variable Cost, Unit Contribution Margin, Variable Cost Ratio, and Contribution Margin Ratio from a contribution format income statement; What are the mathematical relationships among each other?

Selling Price = Variable Cost + Contribution Margin, and the ratios are just percent versions of that split

VC ratio = 1 - CM ratio

CM ratio = 1 - VC ratio