Econometrics T1

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

23 Terms

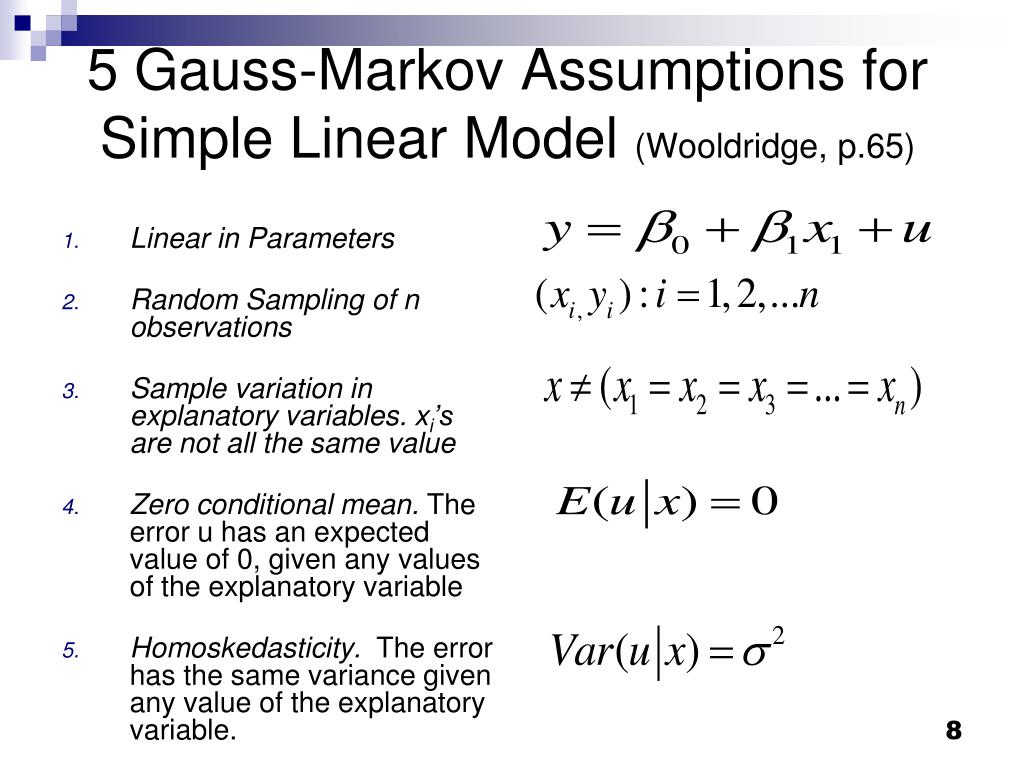

Gaus Markov assumptions

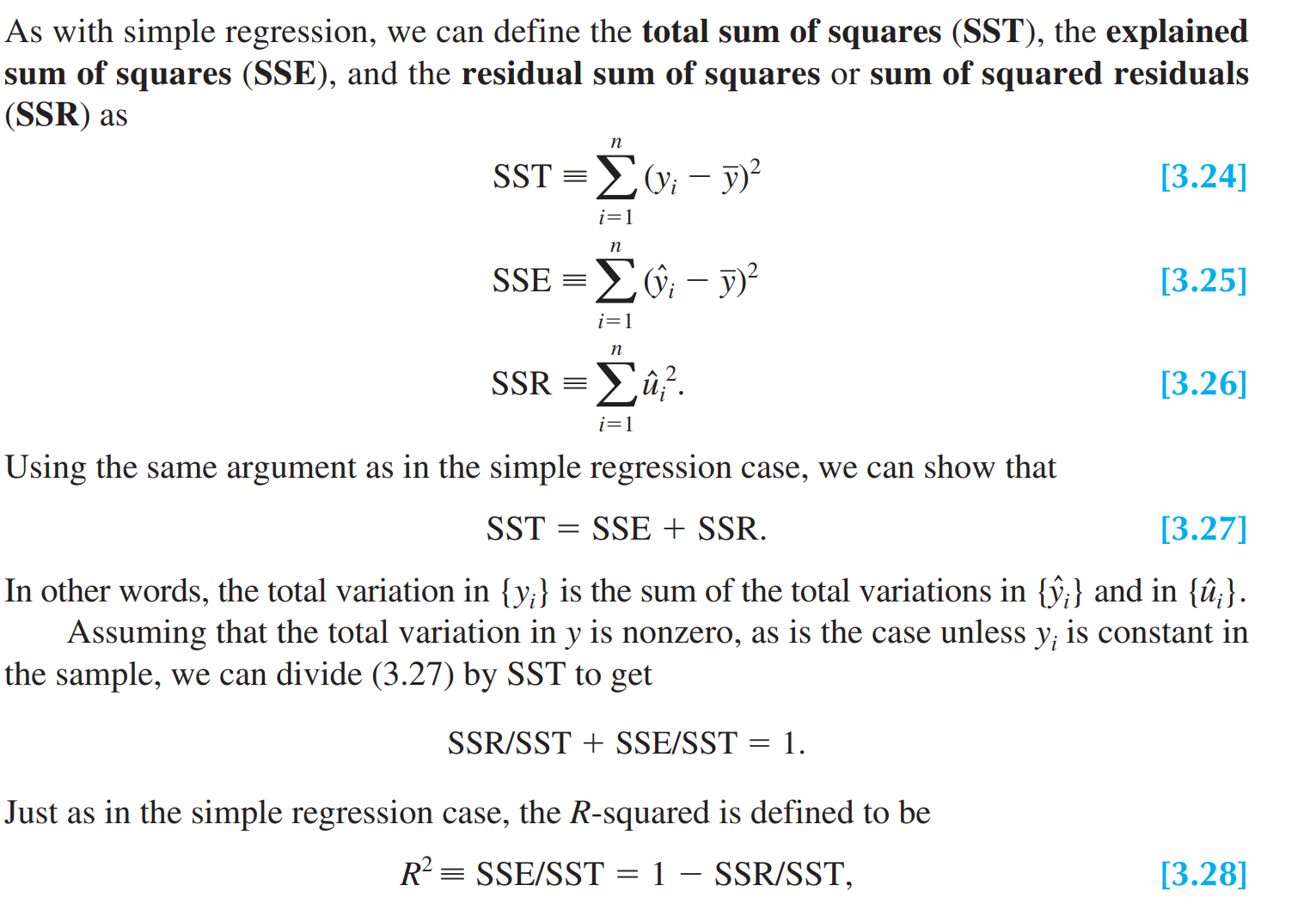

formulae for SST, SSR, SSE, R², and relationships

omitted variable bias

leads to invalid t and f tests, calculate bias to check?

three components of OLS variance

error variance, SST, R²

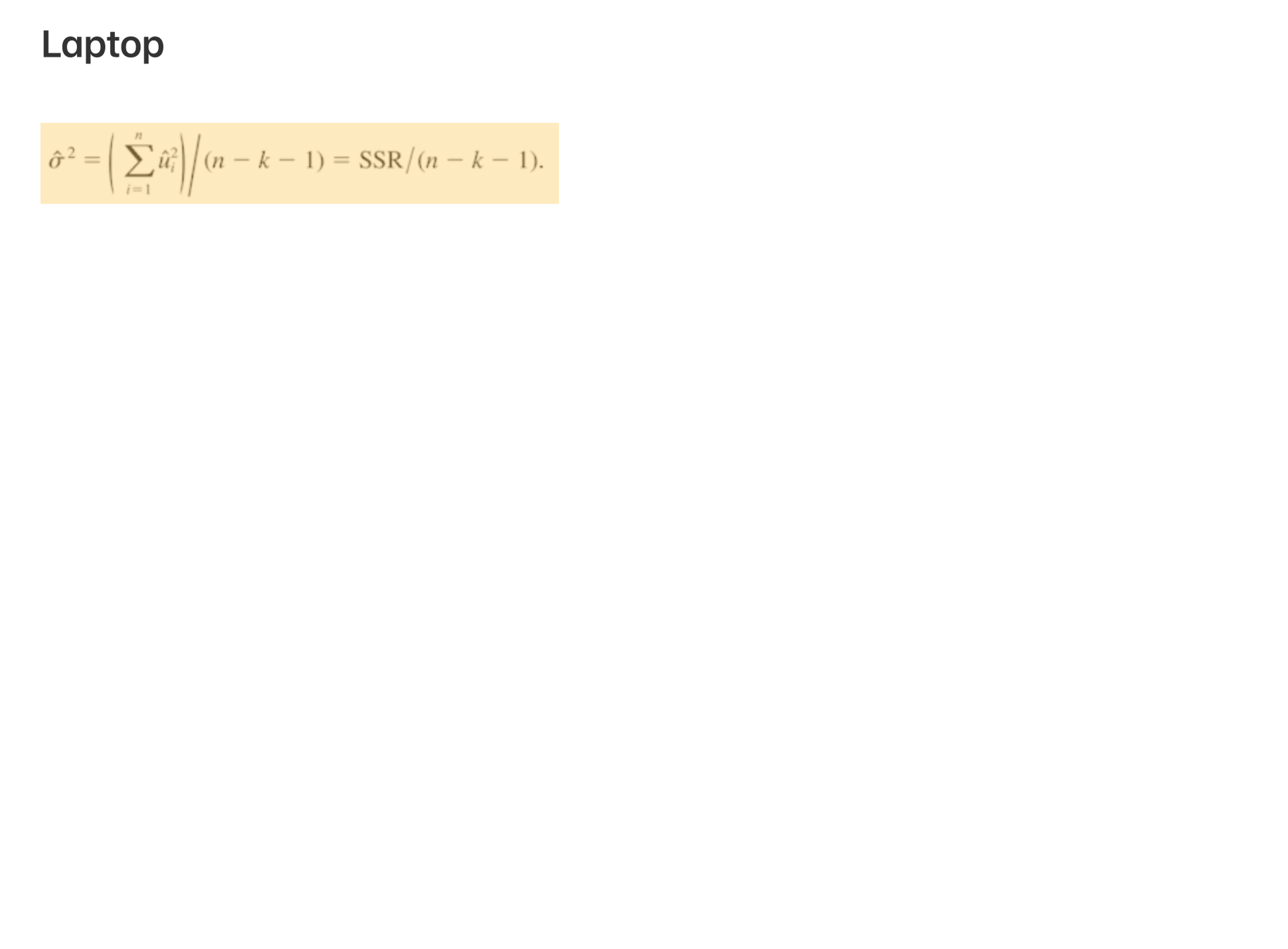

error variance formula

CLM assumption and problem

Gauss markov + normality assumption, problem that it assumes all unobserved factors affect y in a separate additive fashion

t test formula and when to reject

H0 rejected if t>c

CLT

if IID then normally distributed with var= s.d²/n

Frisch-Waugh Theorem (beta hat=…..)

R² formula

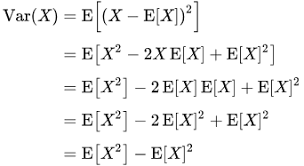

variance formula

law of iterated expectation

t test

F test

Chow test

log form changes

why do we use robust standard errors

control for heteroskedasticity

simultaneity bias

two variables influence each other at the same time, have endogeneity

over specifying

including too many variables especially ones that are not relevant

adjusted R²

use to see if a model with more variables gives better fit, use when lots of variables

consistent OLS estimate

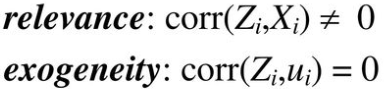

condition to use IV

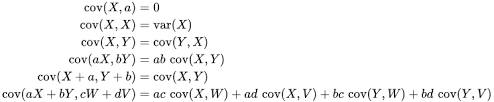

covariance formula