Production and costs

1/26

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

27 Terms

Production

taking resources and turning them into a finished good or service

productivity

the output produced from a certain amount of input

methods of improving productivity

Improve skills and education of workers

Increase specialisation and division of labour

Use new technology to increase output

Reduce wasted resources

short run

the period of time when at least one factor of production is still fixed

long run

the period of time when all factors of production are variable

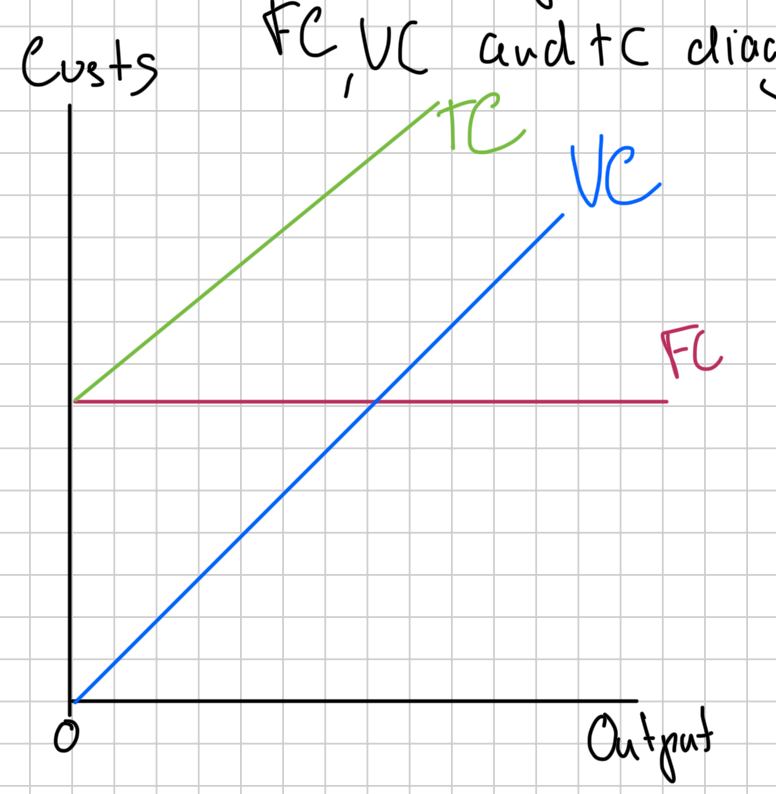

variable costs

costs that change as output changes

fixed costs

costs that do not change as output changes

total costs

the full amount of costs for a firm

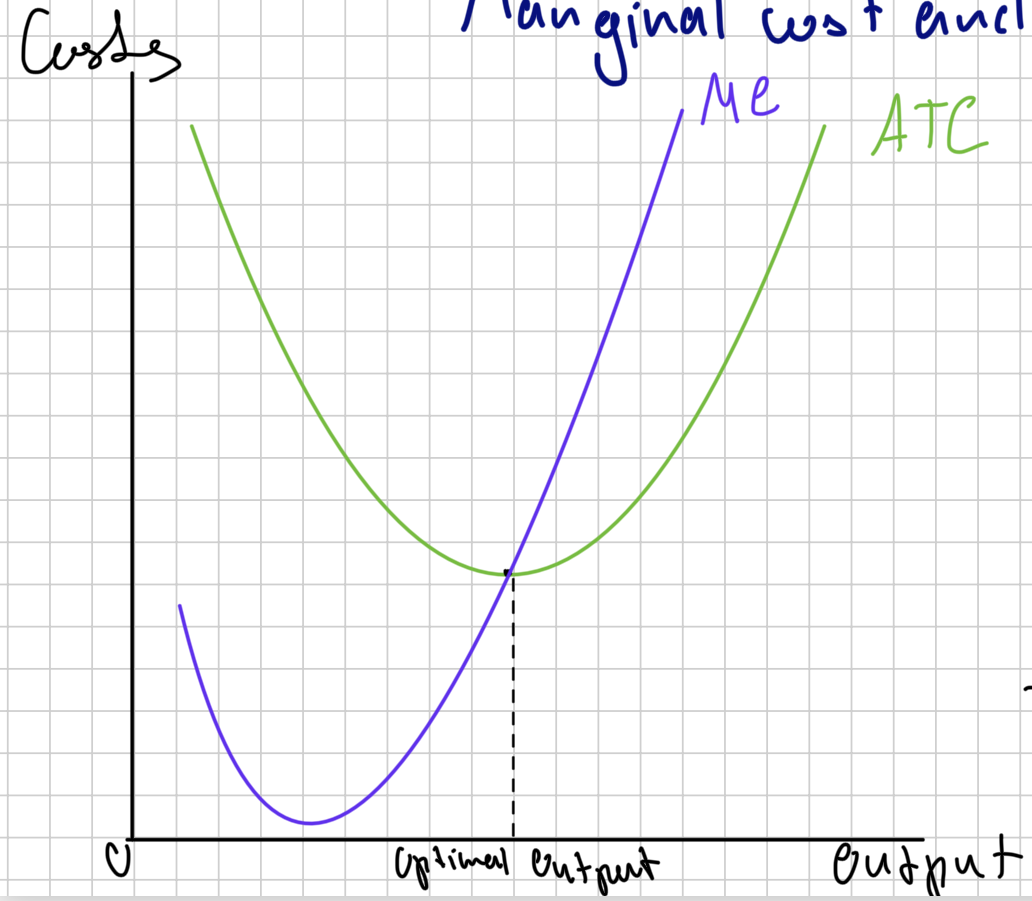

marginal costs

the additional cost of producing one more product

Sales revenue

the money earned from selling products

total sales revenue

the total money from all products sold

average sales revenue

money earned per product

marginal revenue

the additional revenue earned from selling one more product

FC, VC and TC diagram

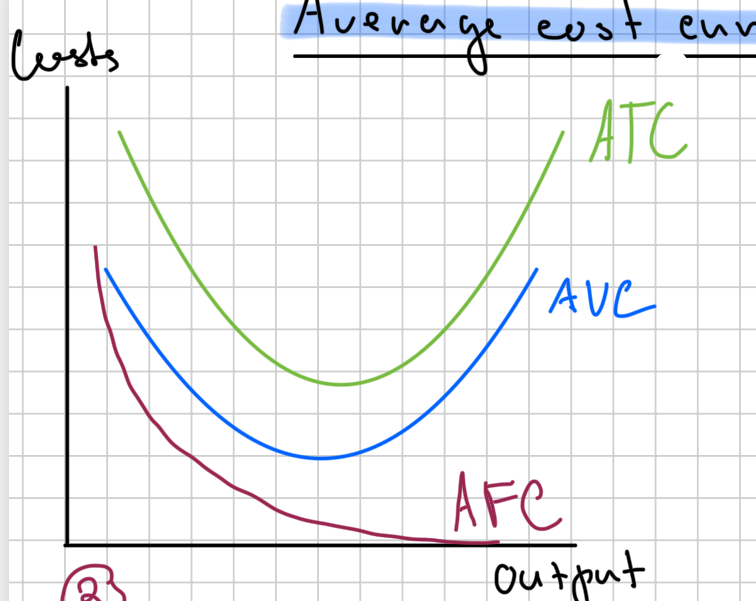

Average cost diagram

marginal cost and average total cost diagram

profit

the money left once all costs are paid

normal profit

the minimum level of profit an entrepreneur has to earn to keep them running this firm

abnormal profit

any profit earned over and above normal profit

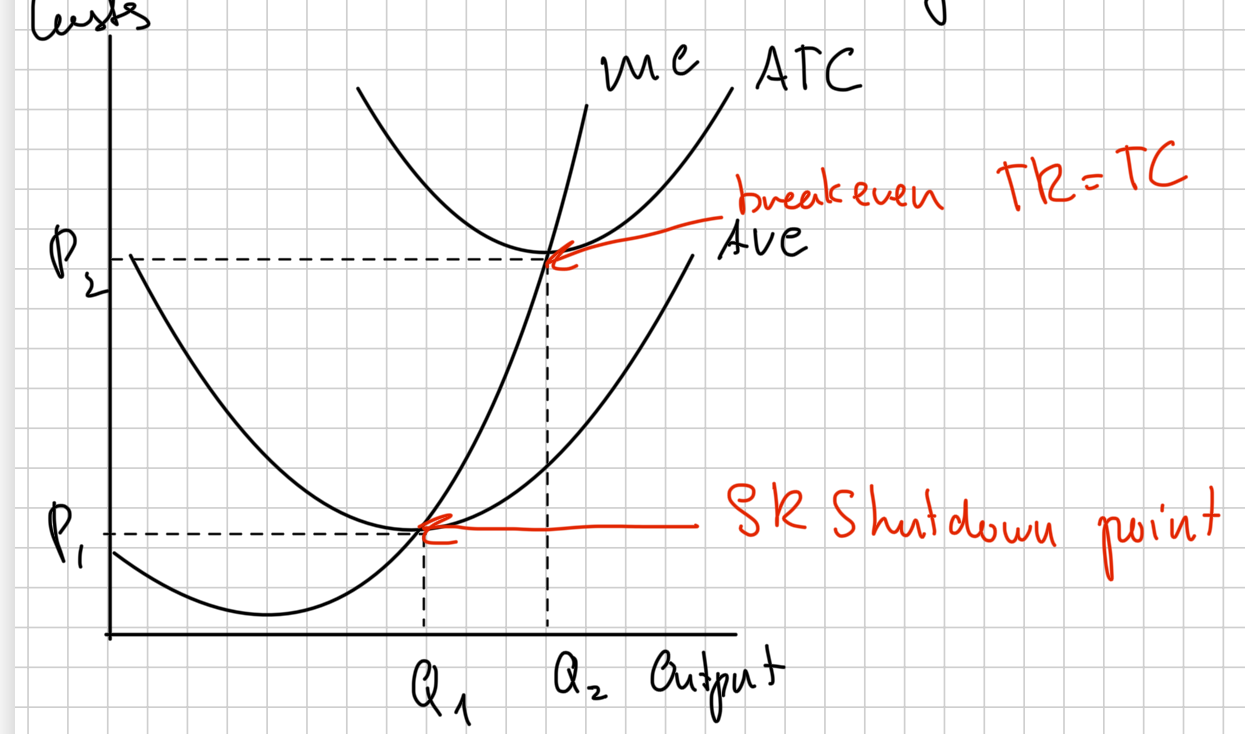

loss

when the total costs of a firm are greater than total revenue

short run shutdown diagram

reasons why loss-making firms keep operating in SR (if they cover vc)

the reason for the losses is likely to improve soon by recession

to keep loyal customers

to keep highly trained workers

to avoid the cost of redundancy

if they have reserves of cash they can use to pay costs

machinery in a factory may be damaged if shut down for long

specialisation

using resources for the activity they are best suited to

division of labour

specialisation of each individual worker

2 methods of dividing labour

by product

by process

optimum output

the output where ATC is at its minimum

law of diminishing returns

if you keep increasing one factor in the production of goods (such as your workforce) while keeping all other factors the same, you'll reach a point beyond which additional increases will result in a progressive decline in output.