Class 8 - Supply

1/26

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

27 Terms

Four types of suppliers

Dealers (art galleries, antique shops, brokers)

2. Auction houses.

3. Art fairs.

4. Artist’s studios.

Dealers: Art Galleries

emerged during the 2nd half

of the 19th century in cities like London and Paris

art movements such as Realism, Impressionism and Post-Impressionism, usually refused in the official salon

The main retail venues for art were:

The official salon(s)

The alternative salon(s) (e.g., Pavillon du Réalisme 1855; Salon des Refusés 1863, 1873, 1875)

Self-staging movements

New commercial galleries (from the 19th century onwards, first established in France and London)

Academies

First Academy of Fine Arts: Florence in the 16th century – meant to improve social capital and skills of those involved in artistic production à only a small minority of painters, sculptors, and other artists were accepted to the academies (acceptance could also take social class and status into account)

In France and England, academies were also established (late 17th and 18th centuries) and were managed by the King, who took charge of the hierarchisation of artistic production

The “Salon” system (Taylor, 20224: 7-8, 20)

French Académie royale de peinture et de sculpture (1648) was an attempt to circumvent the power of guilds through the protection of the king

Royal Academy in London, 1768; National Academy of Design in New York, 1825.

Dominant model of art commerce 1850s up to the early 20th century

art unions (Kunstverein) w/ purpose-built facility - (kunsthalle)

Salon system generated fame + low commissions

model became extremely conservative due to the role played by incumbent academic painters (art académique, art pompier)

It was dominated by a hierarchy of themes:

o History, religion, mythology, orientalism (most favoured)

o Genre, portraits, landscapes (especially national landscapes)

Exhibitions were opened to all artists after 1789 in France, but not all could be accepted (space constraints)

Manet, Le déjeuner sur l’herbe

refused by the official salon and therefore part of the first Salon des Refusés (May 1863), which was supported by the king; people partly attended this salon in large numbers to muck the paintings which were not admitted to the official salon due to what was seen as technical deficiencies (lack of depth, etc.) and lack of taste (the depiction of nude in a non-mythological setting)

Beginnings of galleries

A new generation of dealers emerged applying an entrepreneurial approach to building artists’ careers who were not accepted at the salons. They supported them financially in exchange for a monopoly.

The Salon model declined after WWI and totally collapsed after WWII, replaced by the private art gallery system

Salon vs contemp. art fair

However, the contemporary art fair (launched in the late 1960s) can be considered almost a revival of the Salon system. But instead of a jury of artists, who juried other artists, the art fair jury has dealers jurying other dealers

Origin of art galleries in a variety of 19th-century shops

Antique dealers moving to the primary market

Home furnishing shops presenting new paintings as part of the offer

3. Bookshops (antique and new)

Art supply stores (canvases, easels, tube paints, varnishes, etc.)

5. Stationery shops (already sold engraving and lithographs, along with music sheets and maps)

Many artists accumulate debt with these stores (especially art supply stores and stationery shops), which accept artworks in barter arrangements displaying them for sale.

Success of contemp. galleries

The success of contemporary art galleries is related to their capacity to promote their artists, aiming to increase and institutionalize their reputation, ultimately inscribing their names in the history of art.

spend more than half their budget on promotion

Exhibitions in the gallery

o Exhibitions in museums and contemporary art centres (Kunsthalle) at home and abroad

o Production of catalogues and monographs, preferably by external curators/experts

o Participation in major art fairs, signalling to customers that the works have both

quotation and liquidity in the system

• Galleries dedicate more than half of their budget to promoting their artists

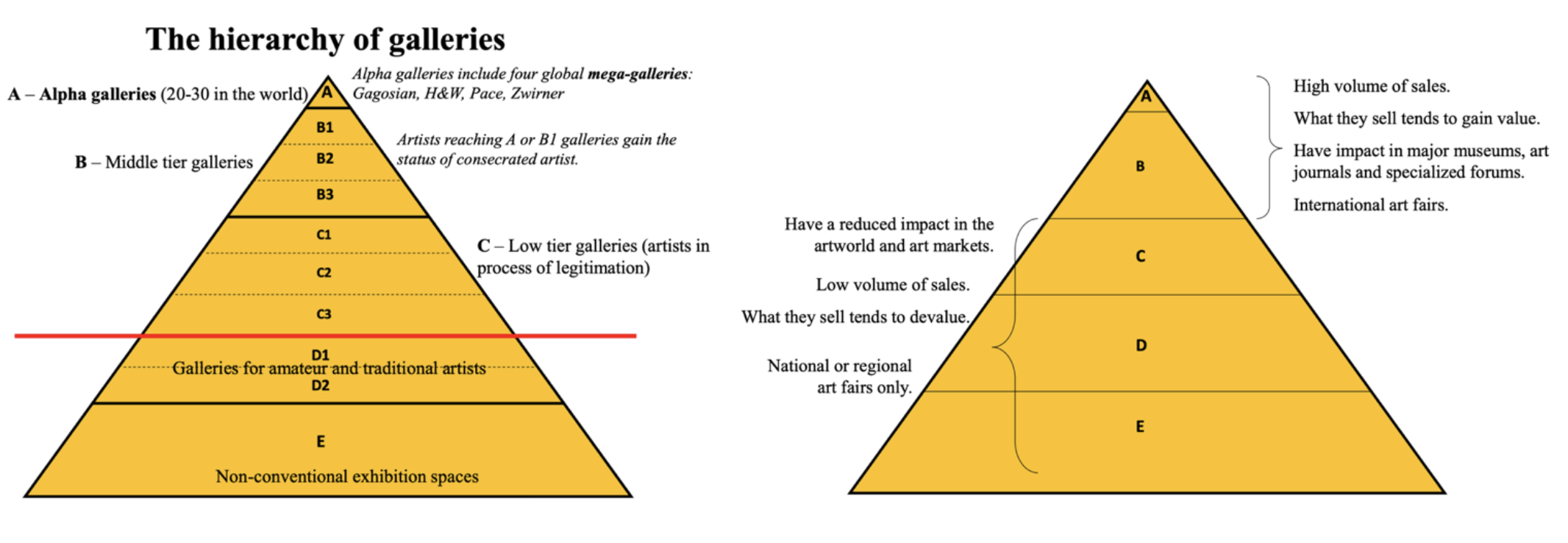

Hierarchy of galleries- Mega galleries

Mega-galleries: Gagosian has 22 galleries, Hauser & Wirth 18, David Zwirner 11, and Pace

8

• Multiple locations, large scale (15.000-20.000 m2), hundred(s) of employees (150-300),

top-quality artists, museum level shows. à Blur the line between gallery and museum

• Represent c.30-50 living artists and estates of deceased artists (primary and secondary

market)

• Must be present in New York, London, and Hong Kong, and eventually also in Paris and

Seoul. And then Shanghai, Tokyo, Los Angeles, Geneva, Rome …

Hierarchy of galleries- Alpha Galleries

White Cube, Lisson, Taddaeus Ropac, Marian Goodman, Perrotin, Galeria Continua,

Marlborough, Mendes Wood DM, Gladstone, Karsten Greve, Templon, etc.

• The biggest ones also represent living artists and estates of deceased artists (primary and

secondary market).

• Present in New York, London, Hong Kong, Paris, Seoul. And also: Shanghai, Tokyo, Los

Angeles, Geneva, Berlin, Rome, Beijing, Zurich, Miami, Vienna, São Paulo, Mexico City,

Athens, Salzburg, Venice, Brussels, (San Gimignano),

Chelsea-type galleries

In the 1990s many galleries moved from Soho to this area in Manhattan (near MoMA and

Whitney Museum) attracted by lower rents and warehouse architecture (freight lifts, truck

accessibility) – now rents reach $20,000 per month for a modest-sized, non-street-level

gallery.

• They occupy the upper floors of industrial warehouses and office buildings. Most work only

in the primary market.

• Concentration of galleries creates synergies. Often several galleries share the same building

and floor, bringing collectors and visitors up the stairs to the upper floors.

• Only alpha galleries can afford prime street-front shops

Dealers: Antique Shops

These companies are usually very heavily indebted to be able to buy goods. This indebtedness, however, is not problematic, since time tends to add value to the pieces, not only because it makes them even older, as the available supply tends to reduce (either because museum purchases remove them from the market, or because the pieces are becoming increasingly rare due to destruction and accidents).

• Consequently, assets tend to appreciate over time, which reassures creditors

Auction Houses

Sotheby’s and Christie’s

SEE TERMINOLOGY

Auction

(public sale to the best bid)

English

ascending

Dutch

descending

Sealed bid

(proposals arrive in advance; open only at the day of auction)

Bid

(increases by 5%-10%)

Lot

(isolated object or group [#])

Estimates

(low and high)

Hammer price

(bid price, excludes buyer’s fee or “premium” and taxes such as VAT on commission, droit de suite , etc.)

Buyer’s premium

(15%-30%)

Seller’s fee

(0-20%)

Reserve Price

(usually corresponds to the low estimate)

Guarantee

(price guaranteed to the proprietor)

“Grand Slam” art fairs

Over 200 contemporary art fairs with international ambitions, but the “Grand Slam” fairs:

o Define the core of the sector’s turnover (c. 50–70% of galleries’ turnover)

o Indicate the artists with the highest value and liquidity

o Set the agenda of the major actors of the art markets (gallery owners, collectors,

curators and directors of museums and Kunsthallen)

• The “Grand Slam” fairs are located in New York, London, Paris, Basel, Miami, Hong Kong and Maastricht.

• These fairs usually belong to large real estate groups and media and events groups.

• The circuit consists of:

o Art Basel: Basel (June), Miami (December), Hong Kong (March) and Paris (October)

o Frieze: Frieze London [post-2000] & Frieze Masters [pre-2000] (October), New York (May), Los Angeles (February), Seoul (September)

o TEFAF: Maastricht (March) & New York (May)

o Armory Show: New York (September)