eco topic 2 - Micro and macro economic

1/29

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

30 Terms

Microeconomic

Microeconomics is the study of the behaviour and decisions of households and firms and the performance of individual markets

Changes in earnings in a particular occupation

Macroeconomics

Macroeconomics is the study of the whole economy, examining national and global economic performance.

National Economic Growth

Decision Makers: Microeconomics

In microeconomics, the main decision makers are consumers, workers, firms and governments.

Decision Makers: Macroeconomics

In macroeconomics, the decision makers are considered at an Large scale The focus is on the government, which makes decisions about taxation and government spending, and the central bank, which makes decisions about interest rates and the money supply.

Resources allocation in a market economy

Consumers and firms decide through the price mechanism

price mechanism

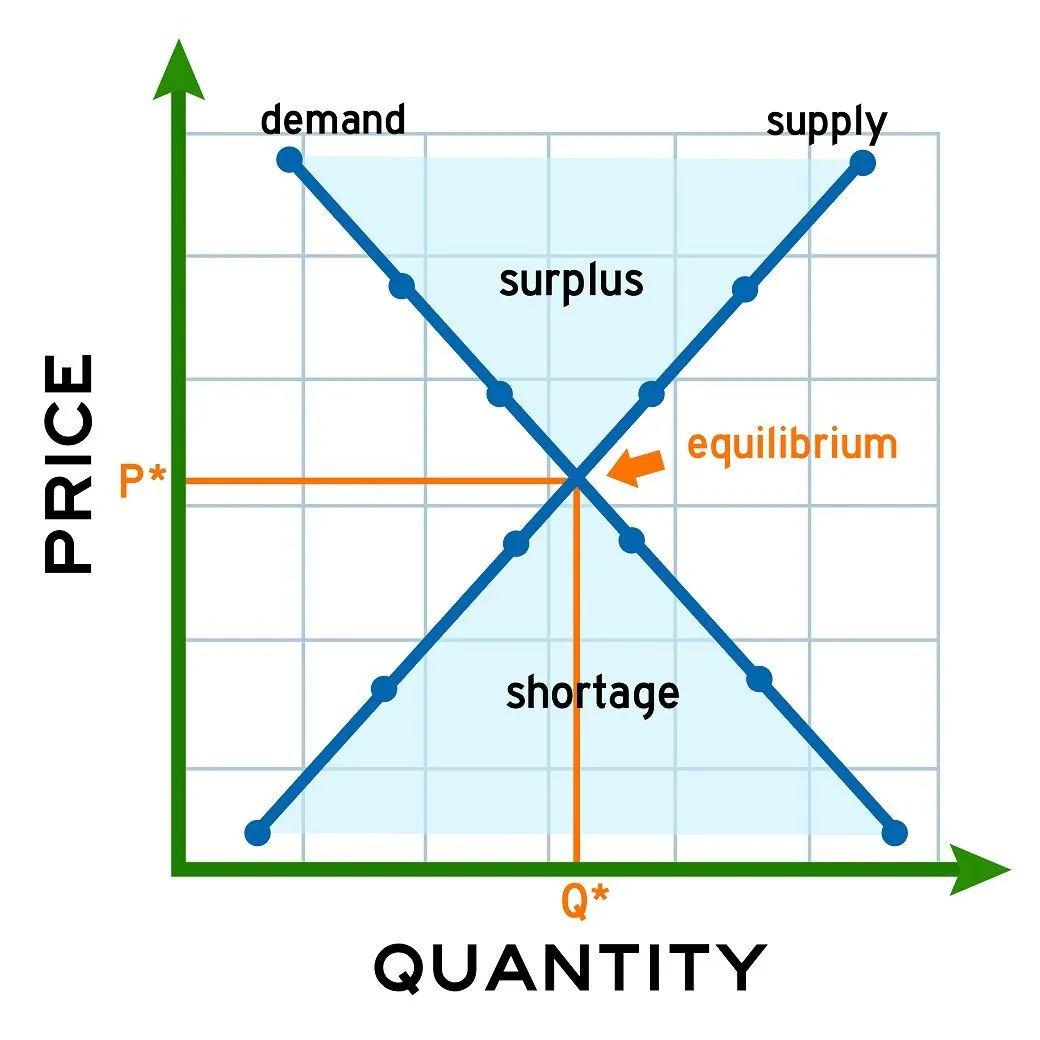

Market Equilibrium

Market equilibrium is the position in a market where demand is equal to supply.

At the equilibrium price, the quantity demanded equals the quantity supplied. There is no shortage and no surplus, and there is no tendency for the price to change.

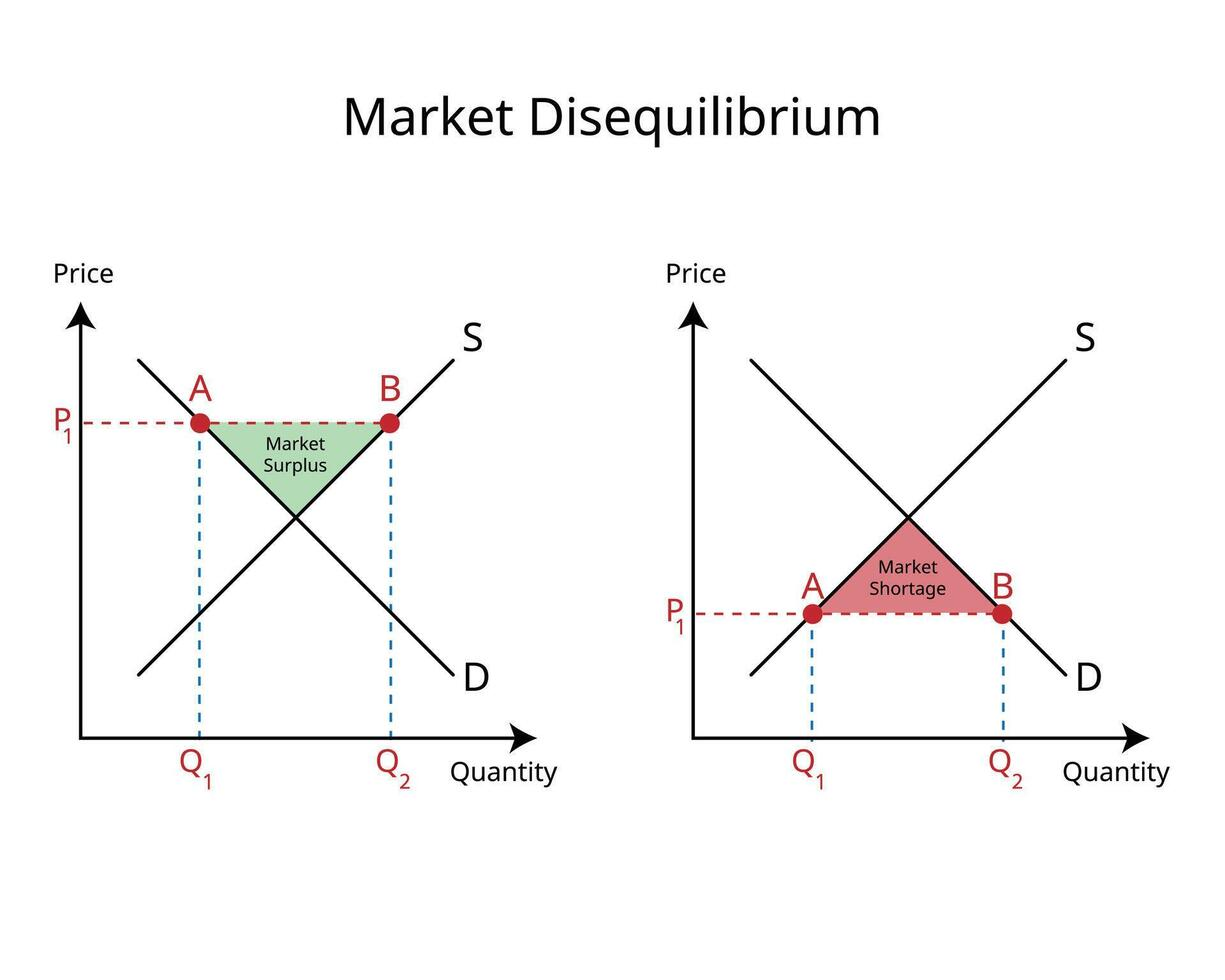

Market Disequilibrium

Market disequilibrium is a situation in which demand is not equal to supply in a market.

It occurs when there is either excess demand (a shortage) or excess supply (a surplus), causing a tendency for the price to change.

The 3 Economic Questions: Explained Market

What to produce: Goods and services demanded by consumers are produced

How to produce it: Firms choose the method of production that minimises costs and maximises profit.

For Whom to produce it: Firms choose the method of production that minimises costs and maximises profit.

A market system is an economic system where resources are allocated through the interaction of buyers and sellers. Buyers create demand for goods and services, while sellers supply them in exchange for money, with prices determined by supply and demand.

Scarce resources—such as land, labour, and capital—are directed by price signals. Rising prices from high demand encourage more production, while falling prices reduce supply, shifting resources elsewhere.

Thus, the market system coordinates choices and allocates resources efficiently according to consumers’ preferences.

Define: Demand

Demand is the quantity of a products that consumers are: willing to buy, able to buy over a period of time at a specific price

Demand Curve: not curve

A demand curves shows

-

Movement along the demand curve

Happens when there is a change in quantity demanded occurs when the price of the good changes ; causing a movement along the existing demand curve- Differernt from shift of the entire curve

Extension: A movement from point A to Point B whows an extension of demand When price falls quatinty demadn increases, beacuse conusmer a willingn and able to buy more of the good

Contraction: A movement fom point B to point A shows a contraction of demand. When prices rise Quantitiy demanded decreceases. Consumers are willing to and able to buy less of the goodn

only caused by changesa in prces of the good no TRIPA

Price chages cause movements along the curve. Non price factors cause tye shift of the entrie curve

Shifts in the demand curve: Increase

Increase in demand

There will be an increase in Demand because conusmers are willing to buy more at every price lelve resulting in the entrire demand curve shifting to the Right.

Shifts in the demand curve: Decrease

when TRIPA change(Not price). There will be a decrease in demand meaning consumers are willing to demand less at every price level. The Demand cruve will shift to the left

Shift in the demand curve: Causes- TRIPA

Taste changes in favour of the product

Related goods: Complementary, substitute

Income

Population change

Advertising

Define: Supply

Supply is the willingness and ability to sell a product.

Market Supply

Market supply is the total quantity of a good or service supplied by all producers in the market.

Individual Supply

Individual supply is the amount a single producer is willing and able to sell at a specific price.

Factors affect supply: TSTCO

Technology

Substitues

Taxes

C

O

weather

PED- Price elasticity of demand

PED/ price elasticity of demand measures the responsiveness of changes in quantity demanded of a product to a change in its price

Law of demand

As price increase, quantity demanded decreases

Price elastic Demand

When demand varies significantly with price changes, Consumers are highly responsive to price movements

Price inelastic Demand

When demand remain realtivelt constant regardless of price changes, consumers are less responsive to price movements

PED Formula

change in quantity demand / change in price

all results are negative: common pracitce to ignore negative

Elastic demand

PED > 1

Demand curve: flat

Inelastic Demand

PED < 1

demand curve: relatively steep

Unitary Demand

PED = 1

meaning the percentage change in quantity demanded exactly equals the percentage change

e.g. : price increase by 10% demand decrease by 10%.

means revenue stays whether pirces go up or not

Charaestics of price elasticity

Availability of substitutes

luxury