1.2.1, 1.2.2, 1.2.3 demand + supply

1/10

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

11 Terms

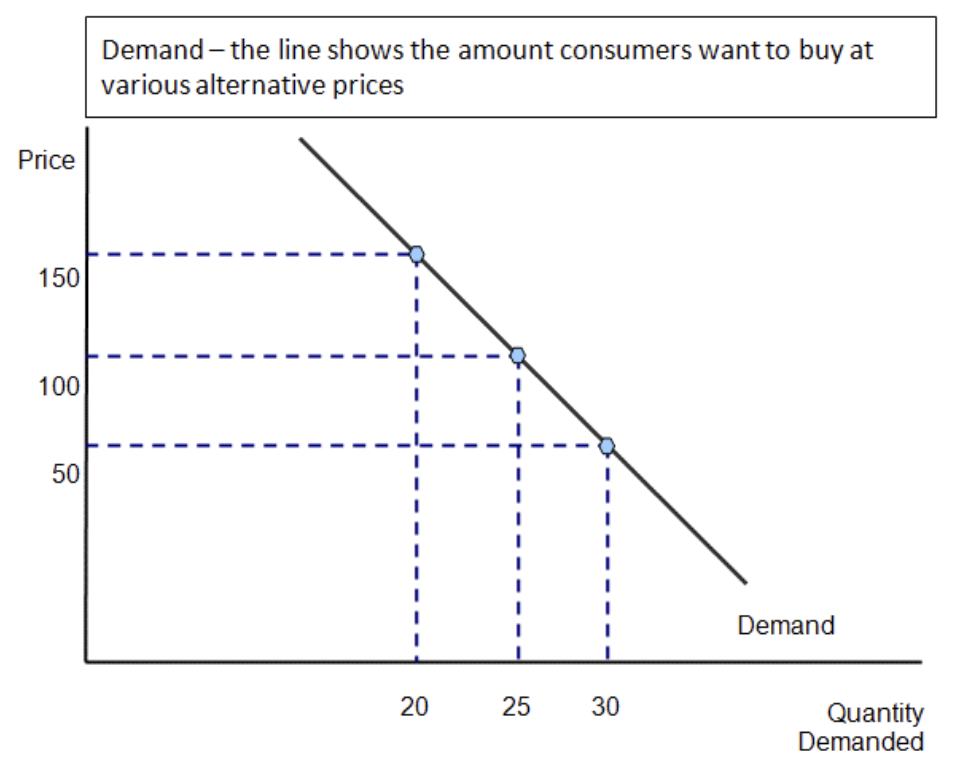

demand (or effective demand) definition

the quantity that customers are willing and able to buy at a given price in a given period of time

the basic law of demand

that demand varies inversely with price – lower prices make products more affordable for customers.

the two types of effects of a price change

income + substitutional

income effects of a price change

A fall in price increases the purchasing power of customers

This allows customers to buy more with a given budget

For normal goods, demand rises with an increase in incomes

substitution effects of a price change

A fall in the price of good X makes it relatively cheaper compared to substitutes

Some customers will switch to good X leading to higher demand

Much depends on whether products are close substitutes

non-price factors that could increase/decrease demands for products/services

Competitions (substitution products)

Prices of contemporary products (a products that is used together with another products)

changes to consumer income

trends in consumer fashion - tastes and preferences changes

advertising and branding

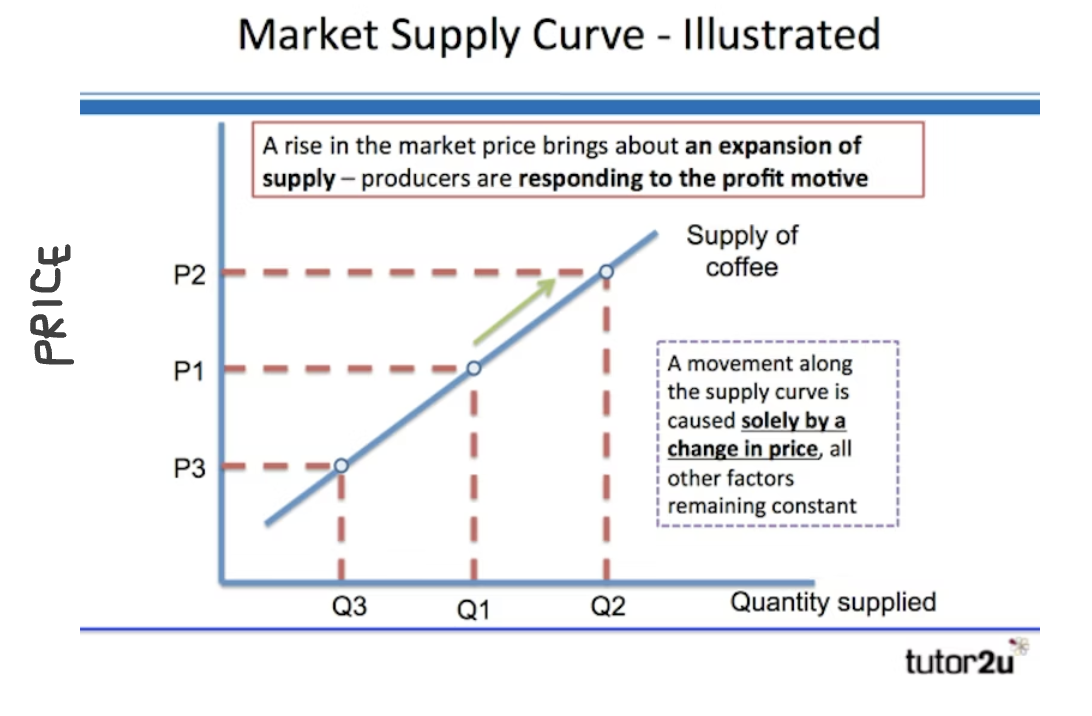

supply definition

the amount producers are willing and able to produce at a given price in a given time period.

market supply curve

The higher the price, the more producers are willing to supply — because profits increase

non-price factors that affect demand

A rise in cost of production

New technology is introduced for production

Indirect taxes (e.g., VAT) are increased

External shocks (e.g., pandemic, a surge in oil prices) take place

the market equilibrium definition

this is when the supply in a market is equal to the demand

summary of changes in equilibrium prices

Demand increases

price: Higher, quantity: Higher

Demand decreases

price: Lower, quantity: Lower

Supply increases

price: Lower, quantity: Higher

Supply decreases

price: Higher, quantity: Lower