Lecture 17 - Interpretation of financial statements

1/113

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

114 Terms

What are the main components of an annual report?

Primary financial statements accounting policies notes and non-financial information

What key questions does analysis answer?

How the business performed what risks exist and what future performance may be

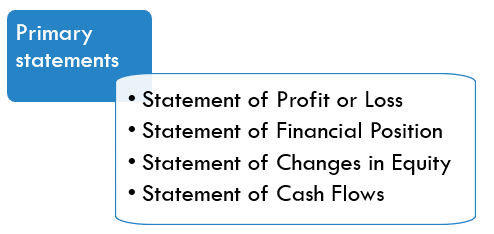

What are the primary financial statements?

Statement of profit or loss

Statement of financial position

Statement of changes in equity

Statement of cash flows

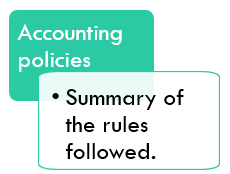

What are accounting policies?

A summary of the rules and methods used in preparing financial statements

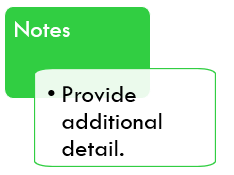

What are notes to the accounts?

Additional detailed explanations supporting the financial statements

What are the main components of an annual report?

Financial statements accounting policies notes and non-financial information

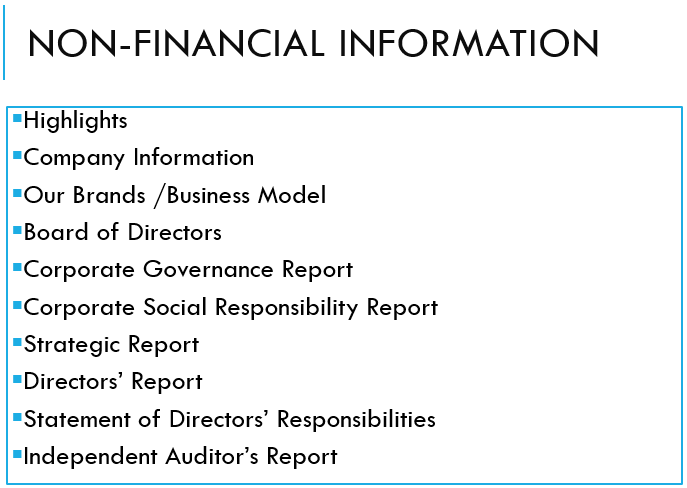

What is non-financial information?

Information about governance strategy and business operations

Why is non-financial information useful?

It provides context beyond the numbers

What assets are often excluded from financial statements?

Intangible assets without measurable cost

Give examples of excluded assets?

Brand value

Internally generated goodwill

Staff expertise

Why are these assets excluded?

They do not have a reliable historical cost

(And can’t be measured reliably)

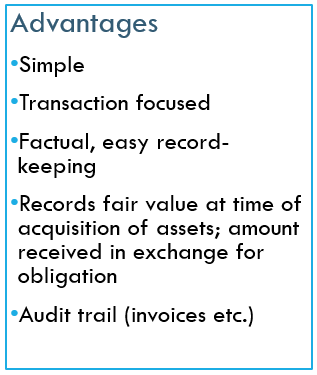

What is historic cost accounting?

Recording assets at their original purchase value

What is an advantage of historic cost accounting?

It is simple objective and verifiable

What is another advantage?

It provides a clear audit trail

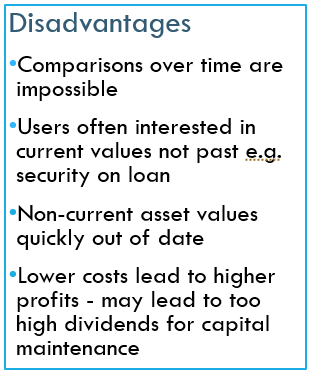

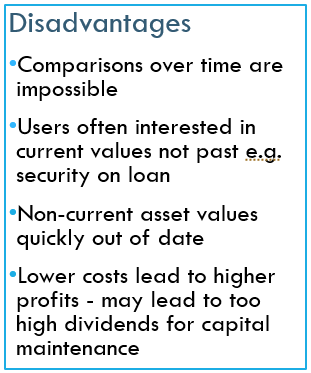

What is a disadvantage of historic cost accounting?

Asset values may become outdated

What is another disadvantage?

It does not reflect current market value

What is another issue?

It can lead to overstated profits and dividends

Why can profits be overstated?

Lower recorded asset values reduce expenses

Why must financial statements be interpreted carefully?

They contain limitations and may not reflect true performance

What is the purpose of financial statement interpretation?

To assess past performance and predict future performance

Why is a single year’s profit not enough?

It lacks context and comparison

Why should multiple years be analysed?

To identify trends and patterns

What is the risk of analysing one period only?

It may reflect unusual or temporary events

What are the four main analysis techniques?

Vertical analysis

Horizontal analysis

Trend analysis

Ratio analysis

What is vertical analysis?

Analysing financial statement items as a percentage of a base figure

What is the base in the income statement?

Sales

What is the base in the balance sheet?

Total assets or capital

What does vertical analysis show?

Cost structure and financing structure

What is horizontal analysis?

Analysing percentage changes over time

What does horizontal analysis show?

Trends across periods and growth

Why is it useful?

It highlights increases or decreases

What is trend analysis?

Evaluating performance over multiple periods

Why is trend analysis important?

It provides context for interpreting performance

What does it help identify?

Long-term growth decline or stability

Why is a single profit figure not enough?

It lacks context and comparison

What is ratio analysis?

Comparing financial statement items to evaluate performance

What does a ratio represent?

Relationship between two financial variables

What are the main types of financial ratios?

Profitability

Efficiency

Liquidity

Gearing/Leverage

Investor ratios

What is gross profit margin? (profitability ratio)

Gross profit divided by sales multiplied by 100

What does gross profit margin measure?

Profitability of core operations

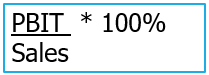

What is operating profit margin?

Operating profit divided by sales multiplied by 100

What does operating margin measure?

Operating efficiency

What is the operating profit percentage/margin?

What does PBIT mean?

Profit before interest tax

What is ROE (ROSF)?

Profit after tax divided by equity

What does ROE measure?

Return to shareholders

What is ROCE?

Profit before interest and tax divided by capital employed

What does ROCE measure?

Overall return on capital used

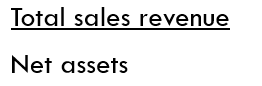

What is asset turnover? (efficiency ratios)

Sales divided by net assets

What does asset turnover measure?

Efficiency of asset use

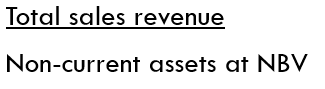

What is non-current asset turnover?

Sales divided by non-current assets

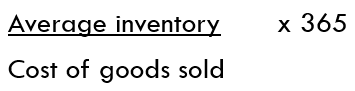

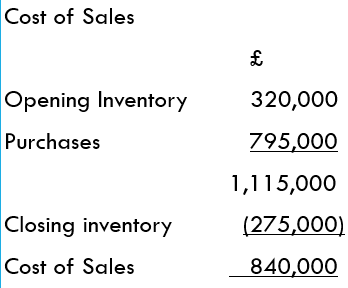

What is inventory holding period?

Average inventory divided by cost of sales multiplied by 365

(the lower the better)

What does it measure?

Number of days inventory is held

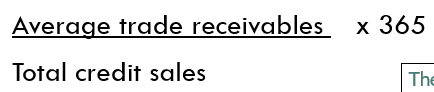

What is receivables collection period?

Average receivables divided by credit sales multiplied by 365

(the lower the better)

What does it measure?

Time taken to collect cash

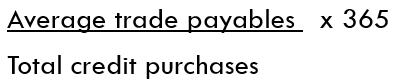

What is payables payment period?

Average payables divided by credit purchases multiplied by 365

(the higher the better)

What does it measure?

Time taken to pay suppliers

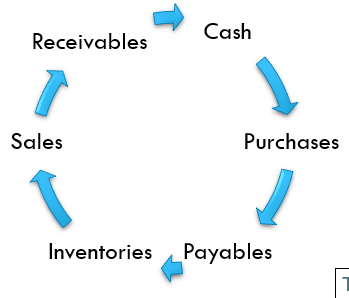

What is the working capital cycle?

Inventory days plus receivables days minus payables days

(the lower the better)

What does the cash conversion cycle look like?

What does it measure?

Time to convert resources into cash

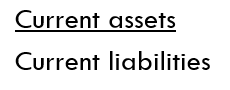

What is the current ratio? (liquidity ratio)

Current assets divided by current liabilities

What does it measure?

Liquidity

(E.g. a typical supermarkets current ratio = 0.65times)

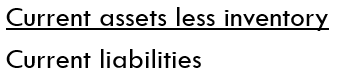

What is the acid test ratio?

Current assets minus inventory divided by current liabilities

What are the determinants of the lequidity ratios?

The’re not as simple as “the higher the better” - there is no right answer here

Why exclude inventory?

It is less liquid

Is a higher liquidity ratio always better?

No there is no single optimal level

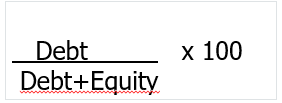

What is gearing ratio?

Debt divided by total capital multiplied by 100

(As a %)

What is the alternative gearing ratio equation?

As a %

What does gearing measure?

Financial risk - if too high, there’s a danger of over-commitment to pay interest

What is interest cover?

Profit before interest and tax divided by interest expense

What does it measure?

Ability to pay interest

What happens if gearing is too high?

Risk of financial distress increases

What is dividend cover? (investor ratio)

Profit after tax divided by dividends

What does it measure?

Ability to sustain dividends

What is dividend yield?

Dividend per share divided by share price

What is earnings per share?

Profit after tax divided by number of shares

What is price earnings ratio?

Share price divided by earnings per share

What does a high PE ratio indicate?

Possible overvaluation or high growth expectations

What does a low PE ratio indicate?

Possible undervaluation

What are yardsticks?

Benchmarks used to compare performance

Why are yardsticks used in analysis?

Past performance

Competitors

Industry averages

Budgets

Why must companies be compared carefully?

Different industries and policies affect results

What are sources of noise in accounting information?

Business cycles accounting policies and estimates

Why analyse earnings over a full business cycle?

To identify normalised performance

What is lack of comparability?

Differences between firms that distort comparisons

Why do accounting policies matter?

They affect reported figures

What should be checked in accounting policies?

Consistency over time

What areas commonly vary?

Depreciation

Inventory valuation

Revaluation

What is retrospective adjustment?

Adjusting past figures after policy changes

What is accounts manipulation?

Adjusting figures to influence results

How can inventory be used to manipulate profit?

Higher closing inventory increases profit

Why is this important?

It can distort performance

Why should exceptional items be considered?

They distort underlying performance

What are exceptional items?

Large unusual transactions affecting profit

Where are exceptional items reported?

In profit or loss before interest

What is adjusted profit?

Profit excluding exceptional items

Why use adjusted profit?

To assess core performance

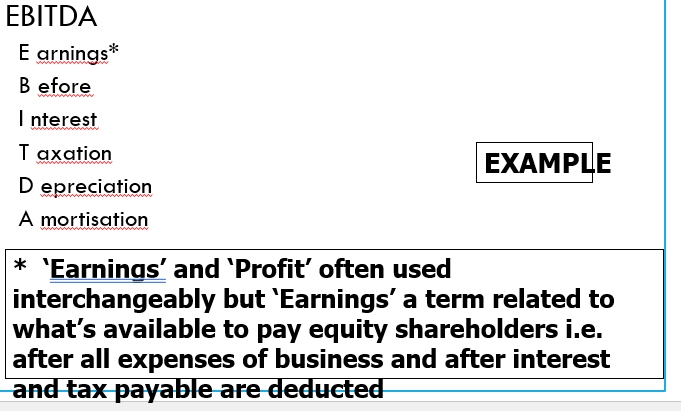

What is EBITDA?

Earnings before interest tax depreciation and amortisation

Depreciation vs Amortisation

Amortisation applies to intangibles whole depreciation applies to tangible

Why use EBITDA?

To compare operating performance