Microeconomics Theme 1 <3

5.0(1)

Studied by 3 peopleCard Sorting

1/111

Earn XP

Description and Tags

Last updated 6:15 PM on 11/13/22

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

112 Terms

1

New cards

Ceteris paribus

all other things remaining constant

2

New cards

positive statement

a statement with facts and is value free scientific approach.

3

New cards

normative statement

statement with opinion and value judgement and is a nonscientific approach

4

New cards

The basic economic problem

how to allocate scarce resources given unlimited want

5

New cards

3 economic agents

1. Households

2. Firms

3. Government

2. Firms

3. Government

6

New cards

3 key questions

1. What to produce?

2. How to produce it?

3. Who to produce for?

2. How to produce it?

3. Who to produce for?

7

New cards

Difference between renewable and nonrenewable resources

nonrenewable resources are finite whereas renewable resources can replenish themselves and are infinite

8

New cards

Rational consumer

wish to maximise their satisfaction or utility

9

New cards

Rational Producers

wish to maximise profits by producing at the lowest cost

10

New cards

Rational Government

wish to improve the economic and social welfare

11

New cards

opportunity cost

the value of the next best alternative forgone when a choice is made

12

New cards

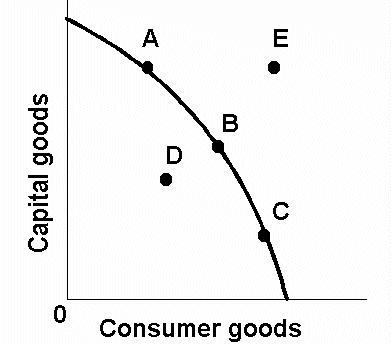

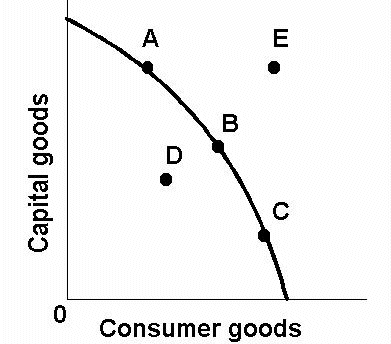

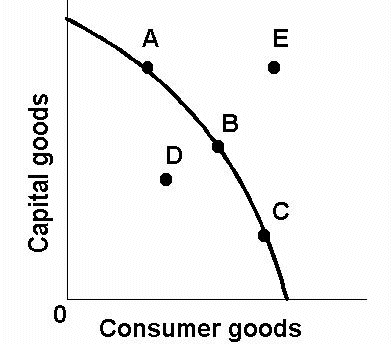

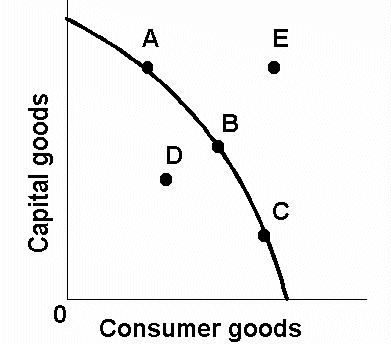

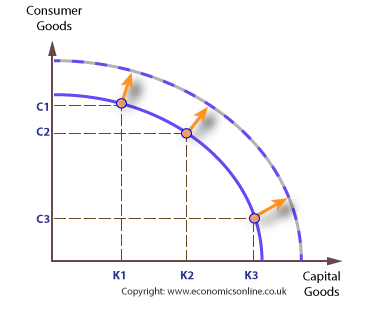

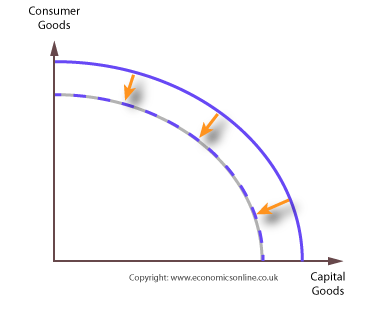

Production Possibility Frontier (PPF)

the maximum potential output combination of two goods an economy can achieve when all its resources are fully and efficiently employed

13

New cards

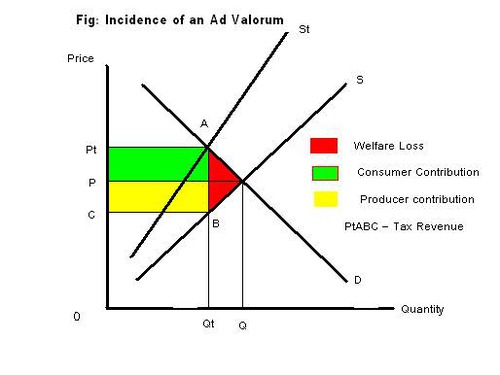

factors causing an outward shift in ppf

increase in quality or quantity of factors of production

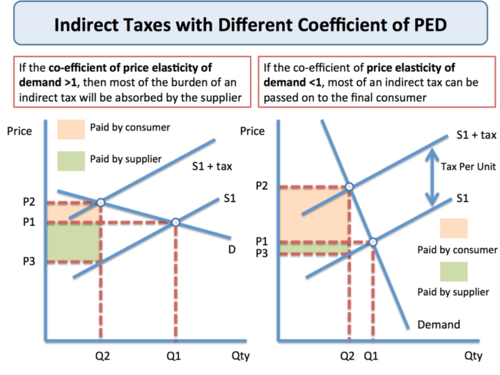

14

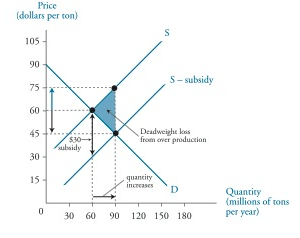

New cards

factors causing an inward shift in ppf

decrease in quality or quantity of factors of production

15

New cards

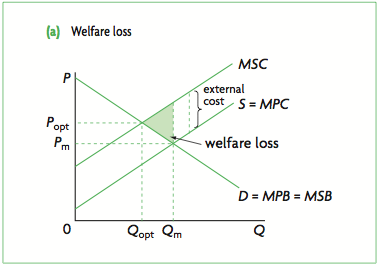

Efficient allocation of resources

B

16

New cards

inefficient allocation of resources (we could produce more given FoP at no OC)

D

17

New cards

unattainable (given current FoP)

E

18

New cards

maximum productive potential of an economy

A/B/C

19

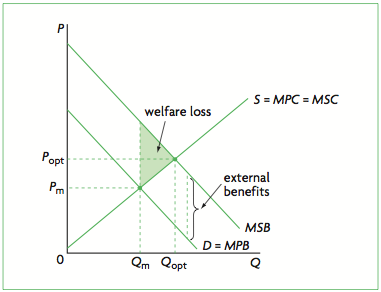

New cards

economic growth on ppf

outward shift

20

New cards

economic decline on ppf

inward shift

21

New cards

division of labour

splitting the production process into different parts to increase output

22

New cards

specialisation

the process of becoming particularly skilled in a task

23

New cards

Adam smith concept of division of labour

a worker will be able to make 20 pins a day if he worked alone but if 10 workers who are specialised in different parts of production then they'll produce 48000 pins a day

24

New cards

4 Advantages of division of labour

1. Increased productivity

2. Lower cost per unit

3. Workers can concentrate on one task

4. Increased output

2. Lower cost per unit

3. Workers can concentrate on one task

4. Increased output

25

New cards

3 Disadvantages of division of labour

1. Work can become tedious

2. Workers can get bored and leave

3. All stages of production will become co reliant on each other so if one stage breaks down the others are affected as well

2. Workers can get bored and leave

3. All stages of production will become co reliant on each other so if one stage breaks down the others are affected as well

26

New cards

4 Functions of money

1. Medium of exchange

2. Store of value

3. Measure of value

4. Standard of deferred payment

2. Store of value

3. Measure of value

4. Standard of deferred payment

27

New cards

free market economy

an economy in which decisions on the three key economic questions and the problem of scarcity is determined by the market force (demand and supply)

28

New cards

command economy

a centrally planned economy in which the role of the state is to be a social planner and the decisions on the three key economic questions and the problem of scarcity is determined by the government

29

New cards

mixed economy

a mixture of free market economy and command economy

30

New cards

Adam Smith and the free market

he thought when individuals follow their own self interest they indirectly promote the good of society then the free market producers would respond to changes in consumer wants in a way that reduces waste and the governments role should be limited to proving public goods

31

New cards

Friedrich Hayek and the free market

he thought when the government plans economies it leads to failure, requires force and restricts freedom

32

New cards

Karl Marx

he thought capitalism was inherently unstable because workers were exploited and there would be a revolution and the economy would follow communism

33

New cards

5 characteristics of command economy

1. State ownership of resources

2. Price determined by the state

3. Resources allocated by the state

4. The role of the state is to be a social planner

5. A greater equality of income and wealth

2. Price determined by the state

3. Resources allocated by the state

4. The role of the state is to be a social planner

5. A greater equality of income and wealth

34

New cards

5 characteristics of free market economy

1. Private ownership of resources

2. Producers aim to maximise profits

3. Consumers aim to maximise utility

4. Resources are allocated by the price mechanism

5. The role of the state is to reduce constraints

2. Producers aim to maximise profits

3. Consumers aim to maximise utility

4. Resources are allocated by the price mechanism

5. The role of the state is to reduce constraints

35

New cards

the role of the state in a mixed economy

fix market failure

36

New cards

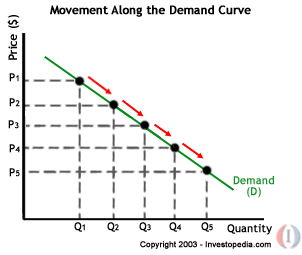

demand

the quantity of a good or service that consumers are willing and able to buy

37

New cards

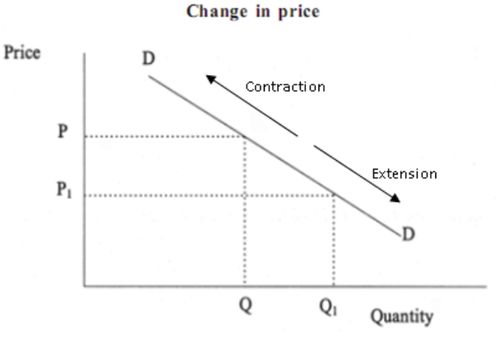

movement along the demand curve

change in price

38

New cards

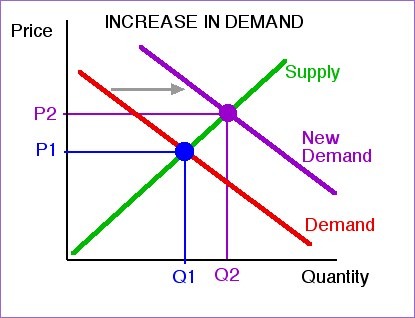

shift in demand curve

Population

Advertisement

Substitutes

Income

Fashion/trends

Interest rates

Complements

Advertisement

Substitutes

Income

Fashion/trends

Interest rates

Complements

39

New cards

diminishing marginal utility

Decreasing satisfaction or usefulness as additional units of a product are acquired

40

New cards

contraction and extension in demand

41

New cards

percentage change formula

change/original x 100

42

New cards

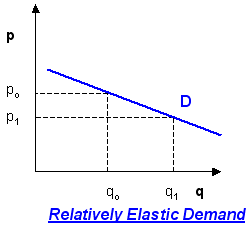

elastic demand

%change in price leads to a more than proportional %change in quantity demanded (more than 1)

43

New cards

inelastic demand

%change in price leads to a less than proportional %change in quantity demanded (less than 1)

44

New cards

price elasticity demanded (PED)

how responsive quantity demanded is to a change in price

45

New cards

PED formula

% change in Qd / % change in P

46

New cards

Determinants of PED

Substitutes

Proportion of income

Luxury/necessity

Addictive

Time period

Proportion of income

Luxury/necessity

Addictive

Time period

47

New cards

Income elasticity demanded (YED)

how responsive quantity demanded is to a change in income

48

New cards

YED formula

% change in Qd / % change in Y

49

New cards

inferior goods

there are other alternatives so when income rises demand falls (negative YED)

more than 1 - income elastic

less than 1 - income inelastic

more than 1 - income elastic

less than 1 - income inelastic

50

New cards

normal good

there are no other alternatives so when income rises demand rises (positive YED)

more than 1 - income elastic (normal luxury)

less than 1 - income inelastic (normal necessity)

more than 1 - income elastic (normal luxury)

less than 1 - income inelastic (normal necessity)

51

New cards

Cross Elasticity of Demand (XED)

how responsive quantity demanded of good A is to a change in price of good B

52

New cards

XED formula

%change in Qd of Good A / %change in P of Good B

53

New cards

Joint demand (complements)

two goods are complements so if price increases for one demand would decrease for the other (negative XED)

54

New cards

competitive demand (substitutes)

a good has substitutes so if the price of the good increases the demand for the substitute increases (positive XED)

55

New cards

supply

the quantity of a good the producer is willing and able to sell

56

New cards

movement in supply

change in price

57

New cards

shift in supply

cost of production changes

government subsidy

entry of new things into the market

government subsidy

entry of new things into the market

58

New cards

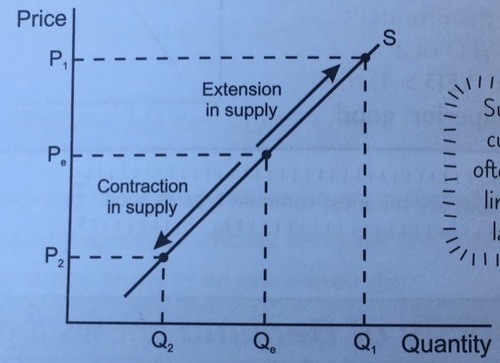

contraction and extension in supply

59

New cards

price elasticity supplied (PES)

how responsive quantity supplied is to a change in price

60

New cards

PES formula

% change in Qs / % change in P

61

New cards

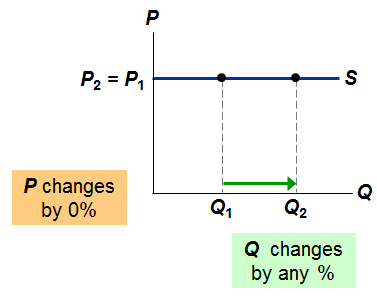

perfectly elastic

infinity

62

New cards

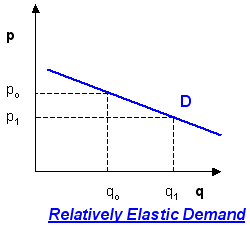

relatively elastic

greater than 1 but less than infinity

63

New cards

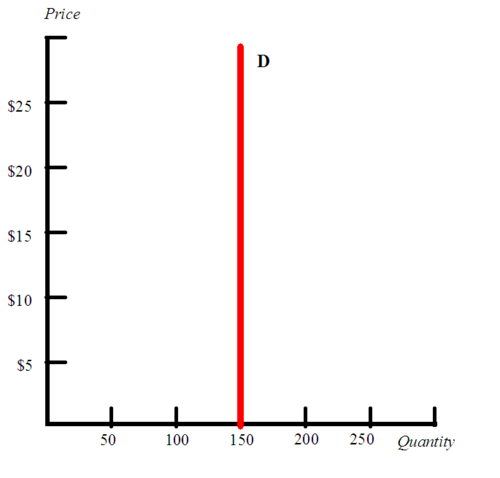

perfectly inelastic

0

64

New cards

relatively inelastic

less than 1 but greater than zero

65

New cards

determinants of PES

Time period

Production time

Factor mobility

Spare capacity

Production time

Factor mobility

Spare capacity

66

New cards

Factors of production

Land

Labour

Capital

Entrepreneurship

Labour

Capital

Entrepreneurship

67

New cards

Price mechanism

signals to producers that the price is too high/too low

incentive to change the price

rations excess demand/supply

successfully allocates scarce resources

incentive to change the price

rations excess demand/supply

successfully allocates scarce resources

68

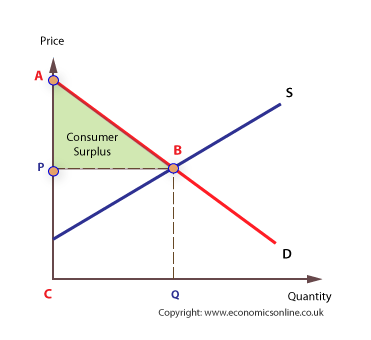

New cards

consumer surplus

difference between how much a consumer is willing and able to pay and the market price

69

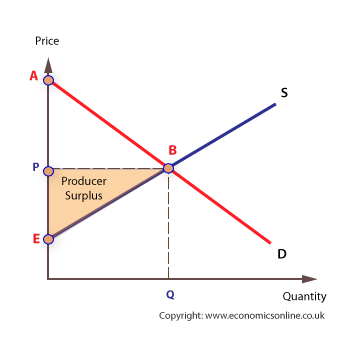

New cards

producer surplus

difference between how much a producer willing and able to sell a good for and the market price

70

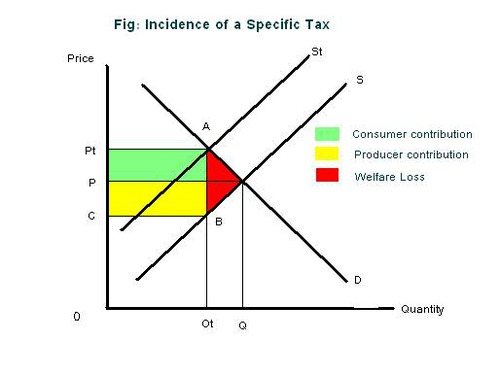

New cards

indirect tax

a tax imposed on goods

71

New cards

ad valorem tax

a percentage tax imposed on good

72

New cards

elastic/inelastic demand in indirect tax

elastic demand more of the incidence of tax is paid by the producer

inelastic demand more of the incidence of tax is paid by the consumer

inelastic demand more of the incidence of tax is paid by the consumer

73

New cards

subsidy

money granted by the government

74

New cards

herd thinking

Making decisions based on what other people do.

75

New cards

habitual thinking

people prefer to carry on behaving as they always have

76

New cards

market failure

the market misallocates resources and isn't operating at the socially optimum level

77

New cards

types of market failure

Negative externality

Positive externality

Public good

Asymmetric information

Positive externality

Public good

Asymmetric information

78

New cards

negative externality

cost to the third party and social costs exceeds private costs

79

New cards

private cost

cost faced by producers directly involved in a transaction

80

New cards

external cost

cost to the third party

81

New cards

social cost

private cost + external cost

82

New cards

marginal private cost (MPC)

the cost of producing an additional unit of output

83

New cards

Marginal External Cost (MEC)

the cost to the third party for producing an additional unit of output

84

New cards

Marginal Social Cost (MSC)

The total cost to society of producing an additional unit of output MSC=MPC+MEC

85

New cards

negative externality causes market failure

social costs exceed private cost

overproduction of the good

misallocation of resources

not operating at the socially optimum level

market failure

overproduction of the good

misallocation of resources

not operating at the socially optimum level

market failure

86

New cards

positive externality

benefit to the third party and social benefits exceed private benefits

87

New cards

private benefit

benefits for consumers directly involved in a transaction

88

New cards

external benefit

benefit to the third party

89

New cards

social benefit

private benefits + external benefits

90

New cards

Marginal Private Benefits (MPB)

benefits to consumers for consuming an additional unit of output

91

New cards

marginal external benefit (MEB)

Benefit to third parties from the consumption of extra unit of output.

92

New cards

marginal social benefits (MSB)

total benefits to the consumer consuming an additional unit of output MSB=MPB+MEB

93

New cards

positive externality causing market failure

social benefits exceed private benefits

under consumption of the good

mis allocation of resources

not operating at the socially optimum level

market failure

under consumption of the good

mis allocation of resources

not operating at the socially optimum level

market failure

94

New cards

public goods

good that are non excludable and non rivalrous

95

New cards

non excludable

can't be confined solely to those who have paid for it and non payers can enjoy the benefits at no financial cost

96

New cards

non rivalrous

each persons enjoyment of a good doesn't stop others enjoyment

97

New cards

free rider problem

difficulty of charging consumers and they will benefit from the product without paying for it

98

New cards

public goods cause market failure

a good is non excludable and non rivalrous

you can't charge people to use it (free rider problem)

firms have to incentive to provide it

under provision of the good

misallocation of resources

market failure

you can't charge people to use it (free rider problem)

firms have to incentive to provide it

under provision of the good

misallocation of resources

market failure

99

New cards

asymmetric information

one party to an economic transaction has more information than the other

100

New cards

asymmetric information causes market failure

information gaps

consumers don't have all the information to make a rational decision

market failure

consumers don't have all the information to make a rational decision

market failure