Investment appraisal

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

20 Terms

Investment appraisal

qualitative technique used in evaluating viability or attractiveness of investment

methods of investment appraisal

Payback Period : Method that estimates the length of

time required for an investment project to pay back

its initial cost outlay.

The average rate of return : Method that measures

the annual net return on an investment as a

percentage of its capital cost.

Net present value : The difference in the summation

of present values of future cash inflows or returns

and the original cost of investment.

Payback Period definition

Payback Period calculates how long a business will

take to recover its principal investment amount

from its net cash flows.

Formula of payback period :

initial investment cost / annual cash flow investment

A construction company plan to invest $200,000 in

new cement-mixing machine and estimates that it

will generate about $50,000 in annual cash flow.

Calculate payback period.

200,000 / 50,000 = 4 years

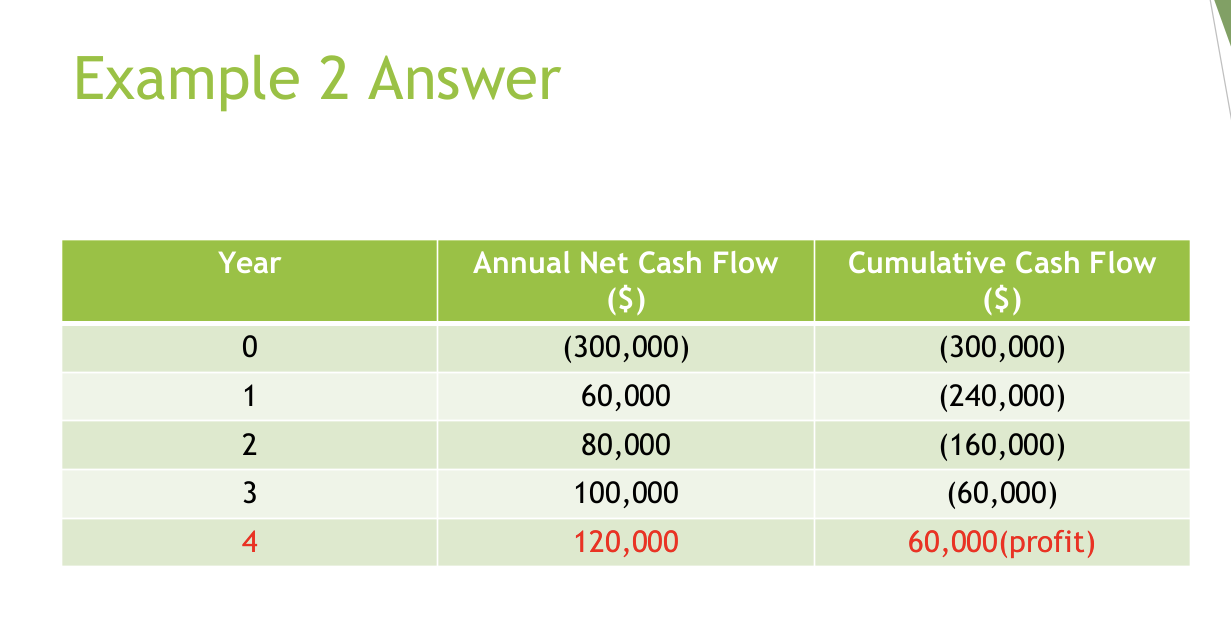

Another construction engineer aims to invest $300,000 in a

new timber-cutting machine. The machine is expected to

generate the following cash flows in the first 4 years :

$60,000, $80,000, $100,000, and $120,000. Calculate

payback period.

payback period = extra cash inflow required / annual cash flow in year 4 × 12 months

payback period = 60,000/120,000 × 12 months

Advantages of payback period

It is simple and fast to calculate.

It is a useful method in rapidly changing industries such as technology.

It helps firms with cash-flow problems.

It is less prone to the inaccuracies of long-term forecasting.

Business managers can easily comprehend and use the results obtained.

Disadvantages of the payback period

It does not consider the cash earned after the payback period which could

influence major investment decisions.

It ignores the overall profitability of an investment project by focusing only

on how fast it will payback.

The annual cash flows could be affected by unexpected external changes in

demand which could negatively affect the payback period.

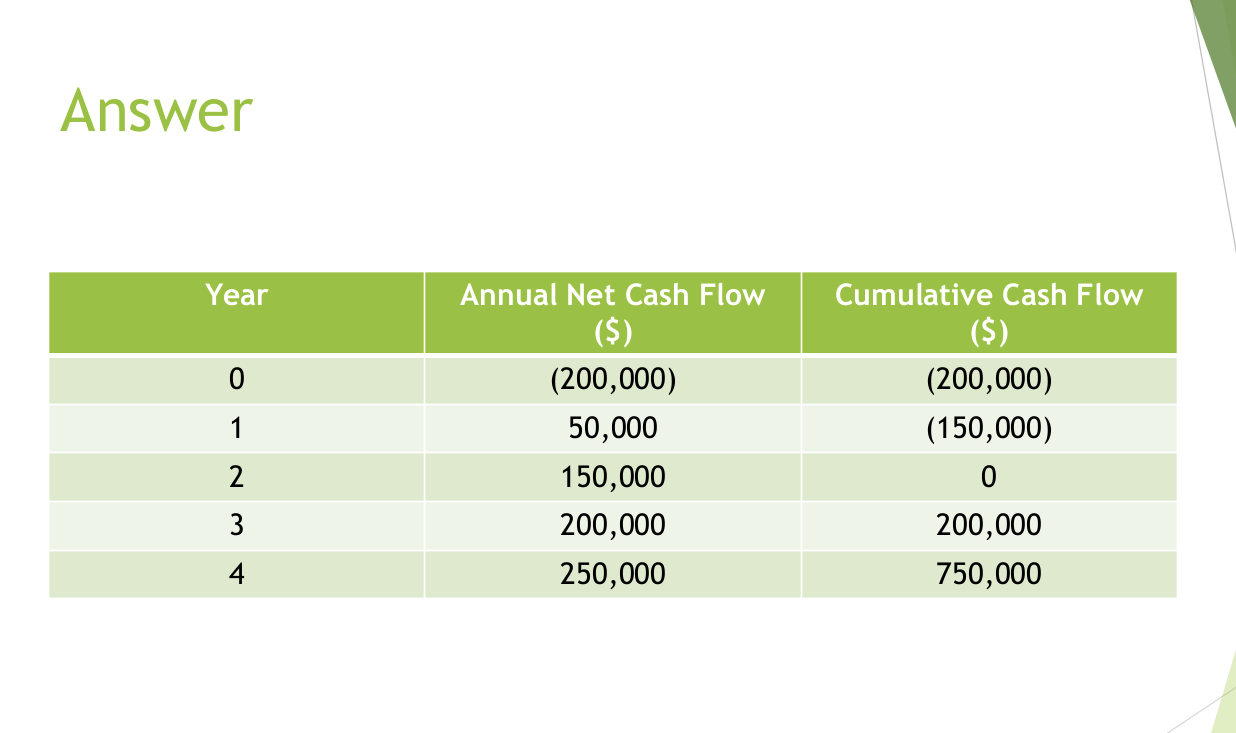

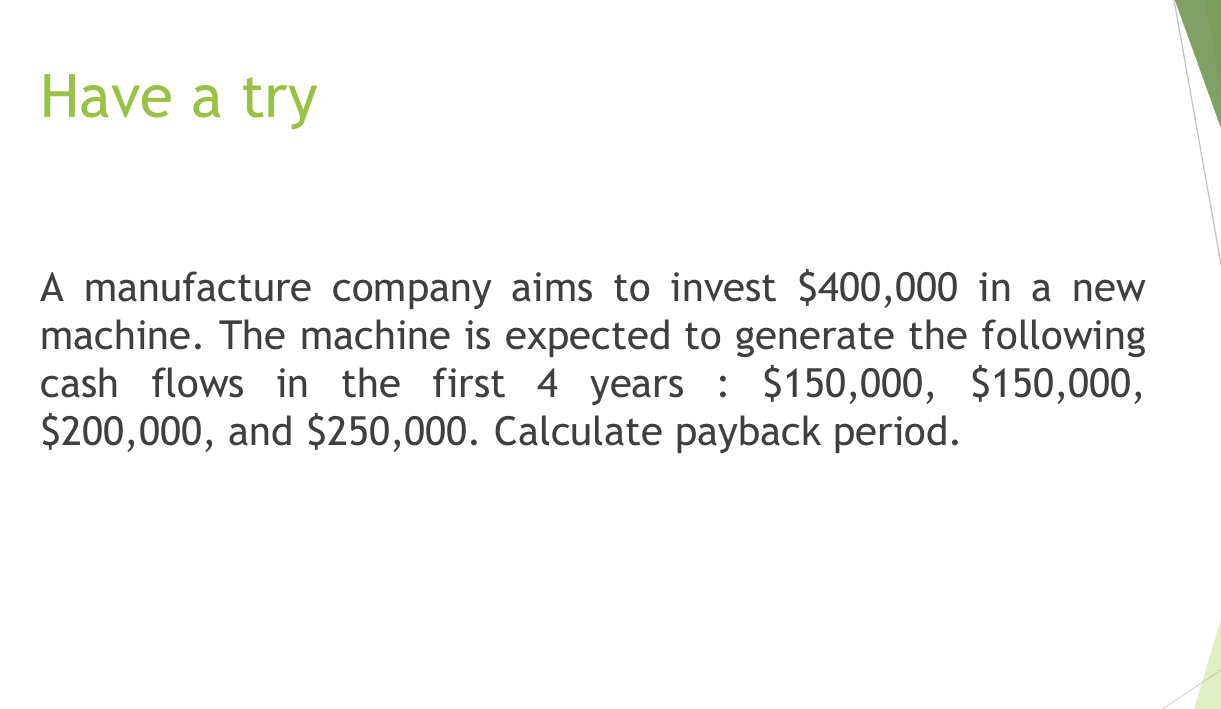

A building engineer aims to invest $200,000 in a new

timber-cutting machine. The machine is expected to

generate the following cash flows in the first 4 years :

$50,000, $150,000, $200,000, and $250,000. Calculate

payback period.

payback period = 200,000 / 200,000 × 12 months

payback period = 1 × 12 months = 12 months

payback period = 2 years 12 months = 3 years

ARR definition

Measures the annual

net return on an investment as a percentage of its capital.

It assesses the profitability per annum generated by a

project over a period of time.

ARR formula

ARR = years of usage (total returns-capital cost) / capital cost x 100

A business considers purchasing a new commercial

photocopier at a cost of $150,000. It expects the following

revenue streams for the next 5 years : $30,000, $50,000,

$75,000, $90,000, and $100,000.

Calculate ARR.

Step 1 : Calculate total returns.

Total returns = $30,000 + $50,000 + $75,000 + $90,000 + $100,000

= $345,000

Step 2 : Calculate Net Return per Annum.

Net Return per Annum = Total returns – Capital Cost / 5 years

Net Return per Annum = $345,000 - $150,000 / 5 years

= $39,000

Step 3 : Calculate ARR.

Net Return per Annum

ARR = ---------------------------- x 100

Capital Cost

$39,000

ARR = ----------- x 100 = 26 %

$150,000

ADVANTAGES OF THE ARR

The ARR shows the profitability of an investment project over a

given period of time.

Unlike the payback period, it makes use of all the cash flows in a

business.

It allows for easy comparisons with other competing projects, for

better allocation of investment funds.

A business can use its own criterion rate and check this with the

ARR for a project, to assess the viability of the venture.

DISADVANTAGES OF THE ARR

A-Since it considers a longer time period or useful life of the

project, there are likely to be forecasting errors.

-It does not consider the timing of cash inflows.

-The effects on the time value of money are not considered.

A Car Rental considers purchasing a new mini bus at a

cost of $350,000. It expects the following revenue streams

for the next 4 years : $150,000, $250,000, $200,000, and

$250,000.

Calculate ARR.

Total returns = $150,000 + $250,000 + $200,000 + $250,000

= $850,000

Net return per annum = $850,000 - $350,000 / 4 years

= $125,000

ARR = $125,000 / $350,000 x 100

= 35.71 %

Net present Value

The difference in the summation of present

values of future cash inflows or returns and the original cost of

investment.

Present value is today’s value of an amount of money available in

the future.

For example, $100 invested at the beginning of the year in a bank

account offering 10% interest would be worth $110 at the end of

the year.

(10% x $100) + 100 = $110

Discounted Cash-Flow Method

A technique that considers how interest rates affect the

present value of future cash flows.

It uses a discount factor that converts these future cash flows

to their present value today.

Advantages of Net Present Value

The opportunity cost and time value of money is put into

consideration in its calculation.

All cash flows including their timing are included in its

computation.

The discount rate can be changed to suit any expected

changes in economic variables such as interest rate

variations.

Disadvantages of Net Present Values

It is more complicated to calculate than the payback

period or ARR.

It can only be used to compare investment projects with

the same initial cost outlay.

The discount rate greatly influences the final NPV result

obtained, which may be affected by inaccurate interest rate

predictions.

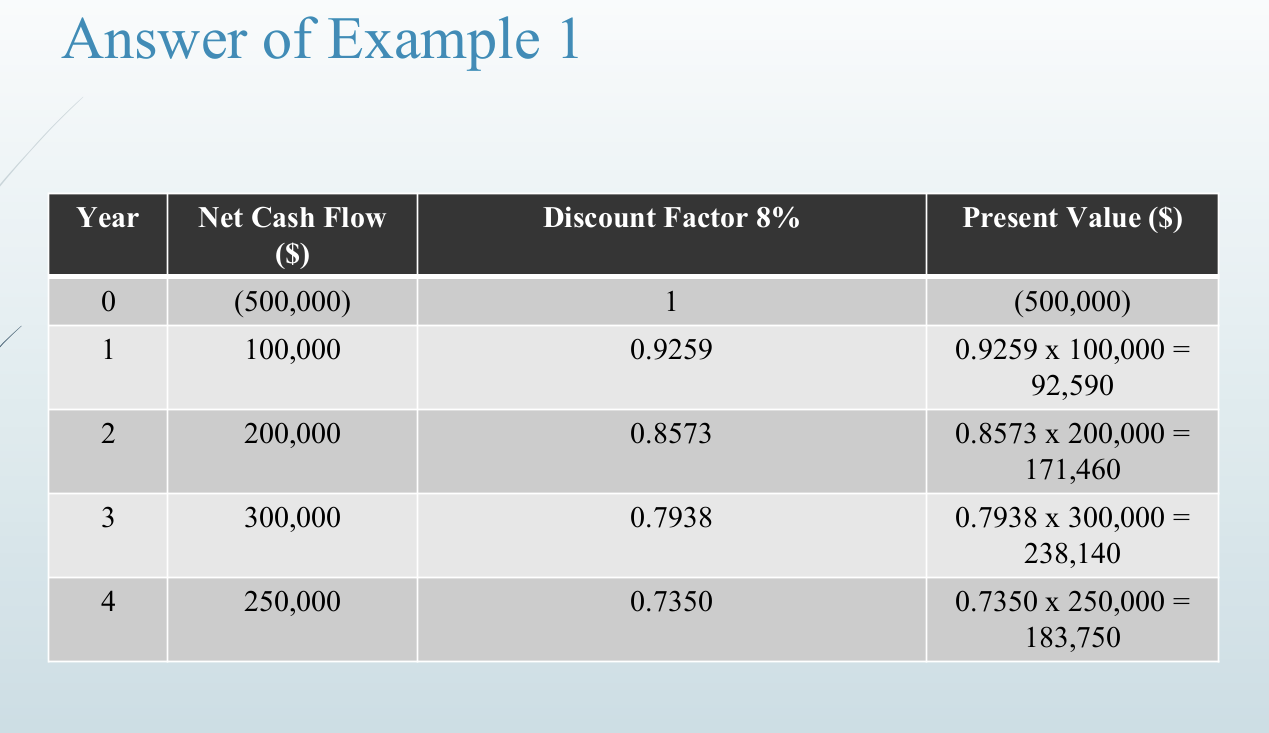

Consider an investment project that costs $500,000 and

produces net cash flow over the next four years as follows,

Year 1 = $100,000

Year 2 = $200,000

Year 3 = $300,000

Year 4 = $250,000

Calculate the Net Present Value at a discount factor 8%.

Net Present Value = Total Present Values – Original Cost

Total Present Values = $92,590 + $171,460 + $238,140 +

$183,750 = $685,940

Original Cost = $500,000

Net Present Value = $685,940 - $500,000 = $185,940