Invenotry and COGS (ACC 2101)

1/52

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

53 Terms

Inventory

Items a company intends for sale to customers in the ordinary course of business. Also, merchandise inventory

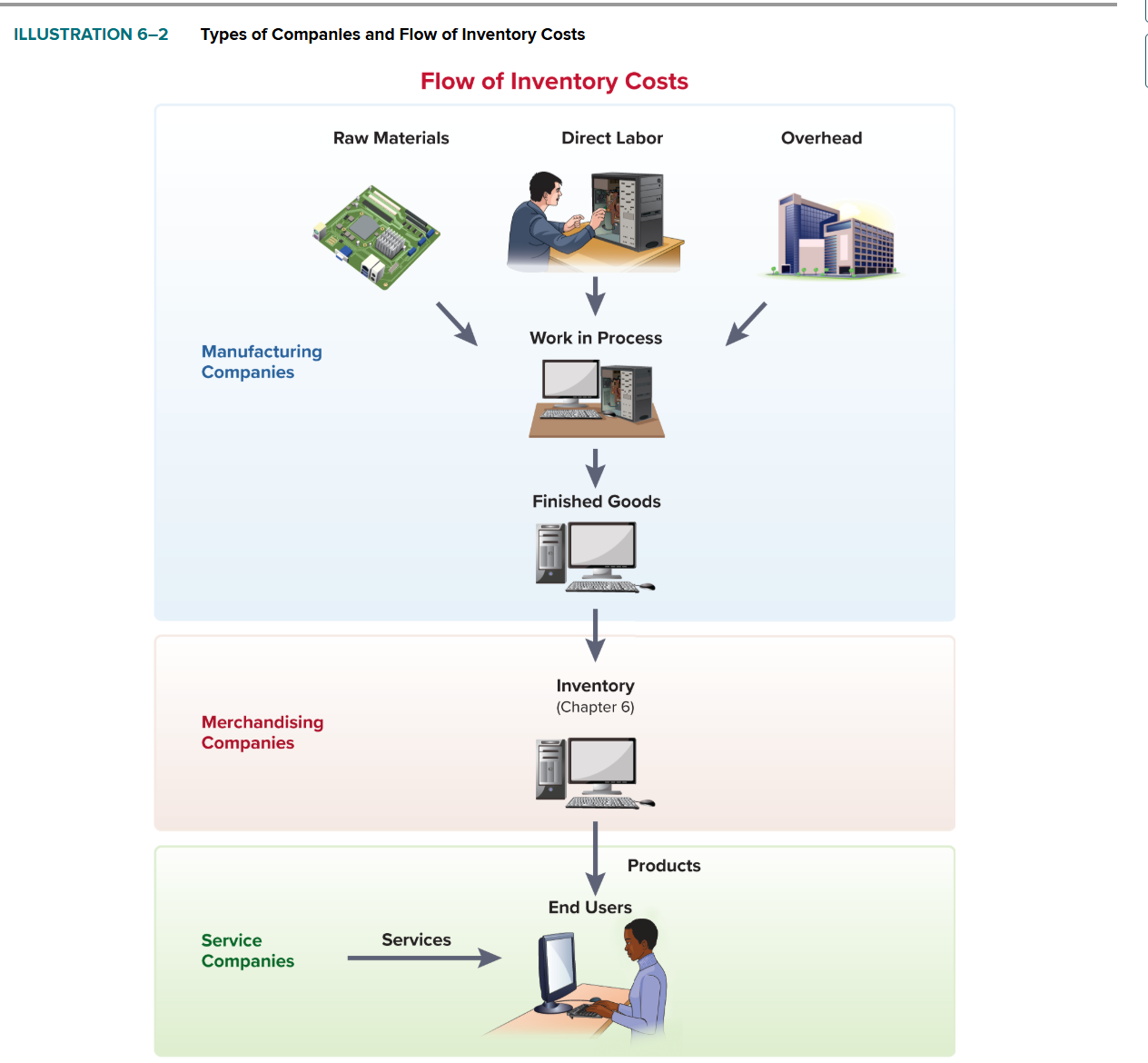

Manufacturing Companies

Companies that sell the inventories they produce rather than sourcing their goods from another supplier

Raw Materials Inventory

Components that will be part of the finished product

Work in Process Inventory

Products that haven’t been fully produced yet

Overhead

The total costs including raw materials, labor, and indirect manufacturing goods

Merchandising Companies

Companies that act as a middleman of storing and moving goods from the manufacturer to the consumer

Wholesalers

They simply sell inventories/goods to retailers and other professionals, but they do not directly sell their products to the public. Ex: Sysco suppling food to resteraunts, schools, etc.

Retailers

They purchase inventory from manufacturers and wholesalers in order to directly sell this inventory to the general public. Ex: Amazon, McDonalds, Costco, Lowes, etc.

What are the steps of the inventory process?

Inventory Flow Raw materials → Production (labor + overhead) → Finished goods → Merchandising company → End user

Key Players

Manufacturers – produce goods from raw materials

Merchandising companies (wholesalers & retailers) – buy finished goods and sell them

End users – final consumers

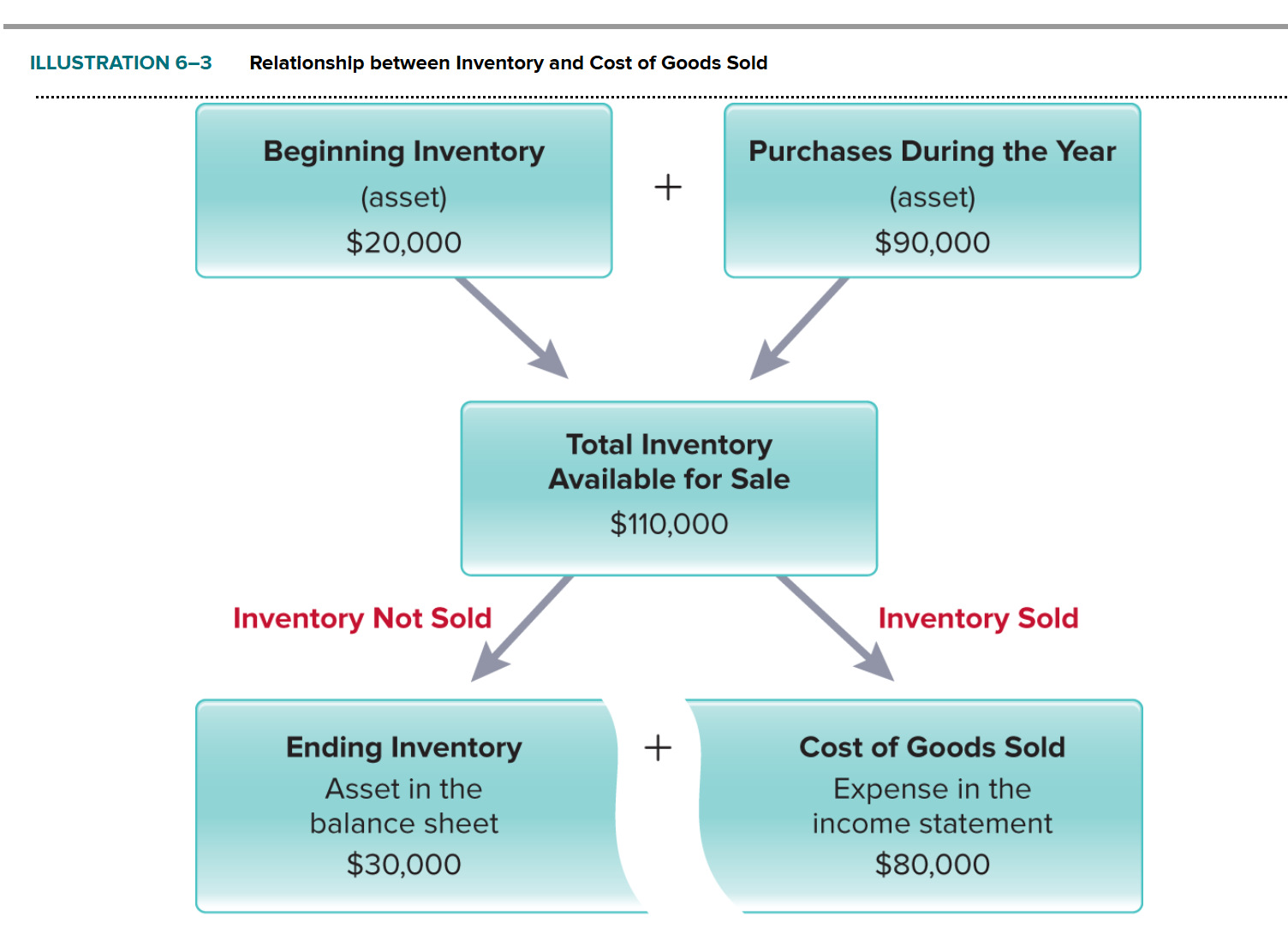

Cost of goods sold (COGS)

Cost of the inventory that was sold during the period. Also, cost of sales, cost of revenues, or cost of products sold

Cost of goods sold (COGS) Formula

Beginning Inventory + Purchases - Ending Inventory

Total Costs of Inventory Formula

Beginning Inventory + Purchases

What is Ending Inventory?

It is the amount of inventory that hasn’t been sold yet

Why is inventory reported in the balance sheet?

B/c it’s a current asset and represents the cost of inventory that has not been sold yet at the end of the period.

Why is Cost of Goods Sold (COGS) in the income statement?

B/c it is an expense that represents the cost of inventory sold during the period.

A company has $500,000 worth of goods available for sale. By year-end, $380,000 worth has been sold. What amount appears on the balance sheet, and what appears on the income statement?

Balance Sheet: $500,000 - $380,000= $120,000. What’s leftover?

Income Statement: $380,000. How many goods/services have actually been sold?

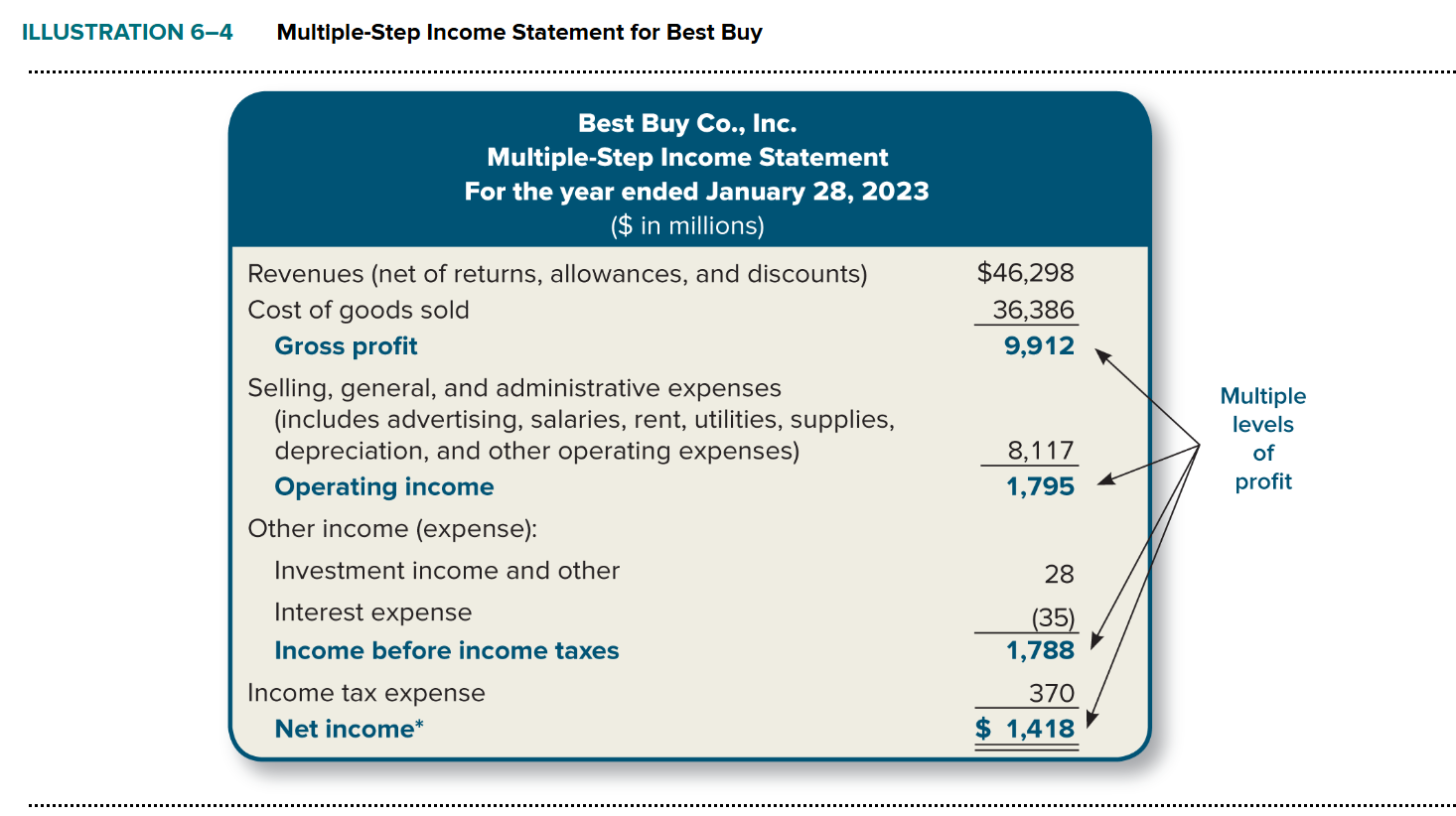

Multiple-step income statement

An income statement that reports multiple levels of income (or profitability).

Gross profit

The difference between net sales and cost of goods sold

SG&A

Selling, General, and Administrative expenses

Operating income

Gross Profit − SG&A Expenses = Operating Income

Income Before Taxes

Operating Income + Other Income/Expense = Income Before Taxes

Net Income

Income Before Taxes − Income Tax Expense OR Revenues - Expenses

Specific identification method

Inventory costing method that matches or identifies each unit of inventory with its actual cost.

First-in, first-out method (FIFO)

Inventory costing method that assumes the first units purchased (the first in) are the first ones sold (the first out)

Trivia Company reports a gross profit of $100, income tax expense of $15, selling, general, and administrative expenses of $35, nonoperating revenues of $10, and nonoperating expenses of $15. What is the company’s operating income?

A. $45

B. $30

C. $50

D. $65

D. $65

Last-in, first-out method (LIFO)

Inventory costing method that assumes the last units purchased (the last in) are the first ones sold (the first out).

Weighted-average cost method

It assumes that all your inventory gets "mixed together" into one big pool, and every single unit is treated as having the same average cost — regardless of when it was purchased or what you actually paid for it.

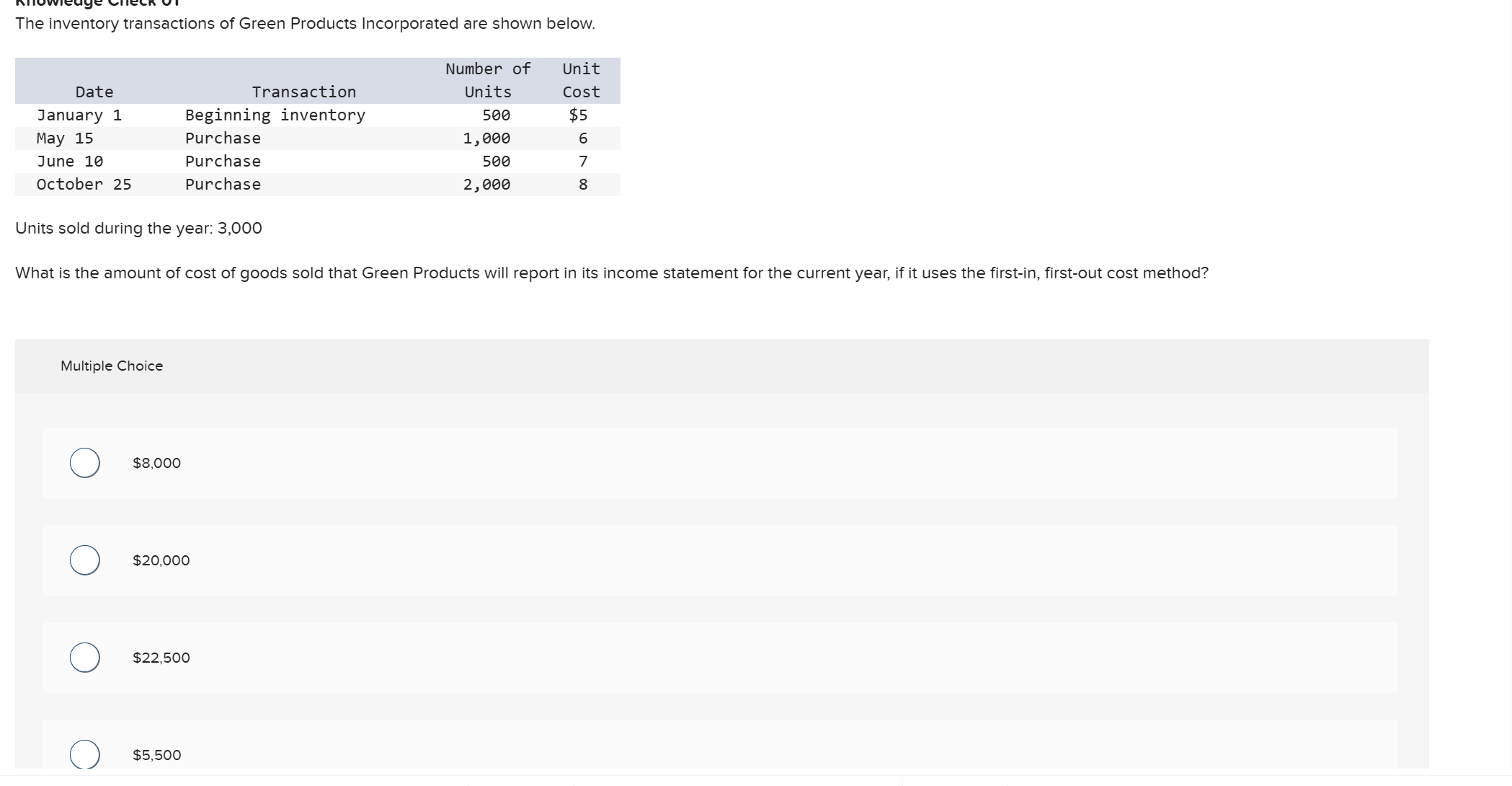

How to find the COGS using the FIFO (first in first out) method in the income statement for the current year?

Multiply the # of units and the costs, and then sum up everything.

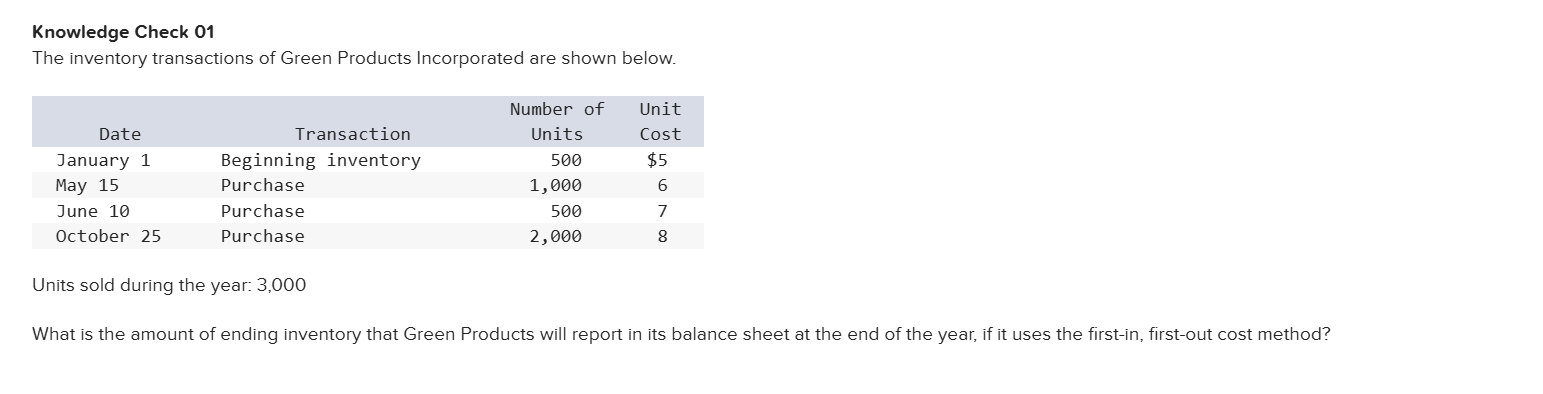

What is the amount of ending inventory that Green Products will report in its balance sheet at the end of the year, if it uses the first-in, first-out cost method?

Step 1: Find total units available

500 + 1,000 + 500 + 2,000 = 4,000 units

Step 2: Find ending inventory units

4,000 − 3,000 sold = 1,000 units remaining

Step 3: Under FIFO, remaining units come from the most recent layer (October 25)

Layer | Units Remaining | Unit Cost | Total |

|---|---|---|---|

October 25 | 1,000 | $8 | $8,000 |

The answer is $8,000.

Quick tip: Notice that COGS + Ending Inventory should always equal the total cost of goods available for sale. You can use this as a check:

Total available = (500×$5) + (1,000×$6) + (500×$7) + (2,000×$8) = $2,500 + $6,000 + $3,500 + $16,000 = $28,000

COGS $20,000 + Ending Inventory $8,000 = $28,000 ✓

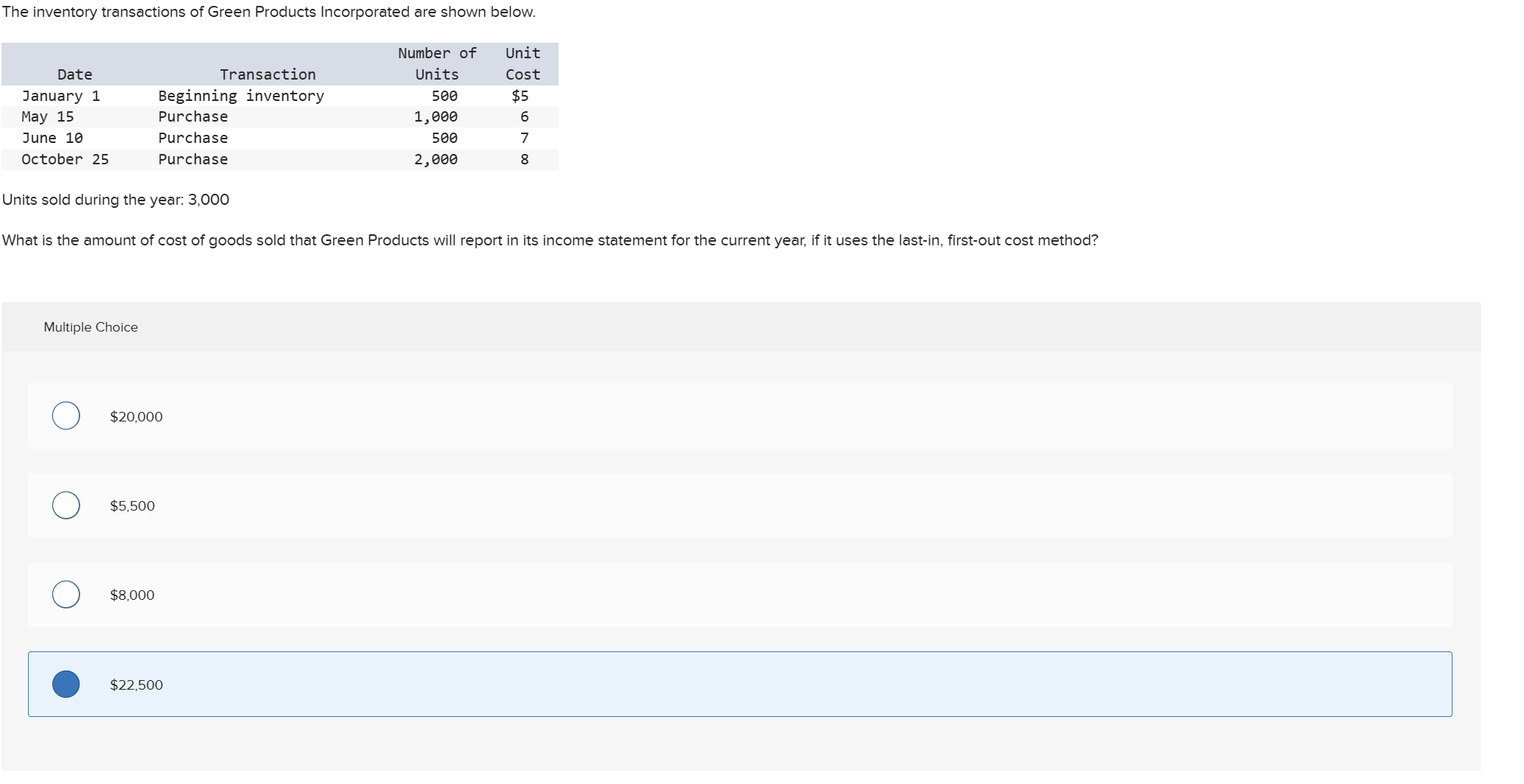

What is the amount of cost of goods sold that Green Products will report in its income statement for the current year, if it uses the last-in, first-out cost method?

Under LIFO (Last-In, First-Out), you sell the newest inventory first. So work through the layers from most recent → oldest:

Layer | Units Used | Unit Cost | Total |

|---|---|---|---|

Oct 25 (newest) | 2,000 | $8 | $16,000 |

June 10 | 500 | $7 | $3,500 |

May 15 | 500 | $6 | $3,000 |

Total | 3,000 | $22,500 |

Note you only need 500 of the 1,000 May 15 units to reach 3,000 total.

The answer is $22,500 ✓ (which matches the selected answer)

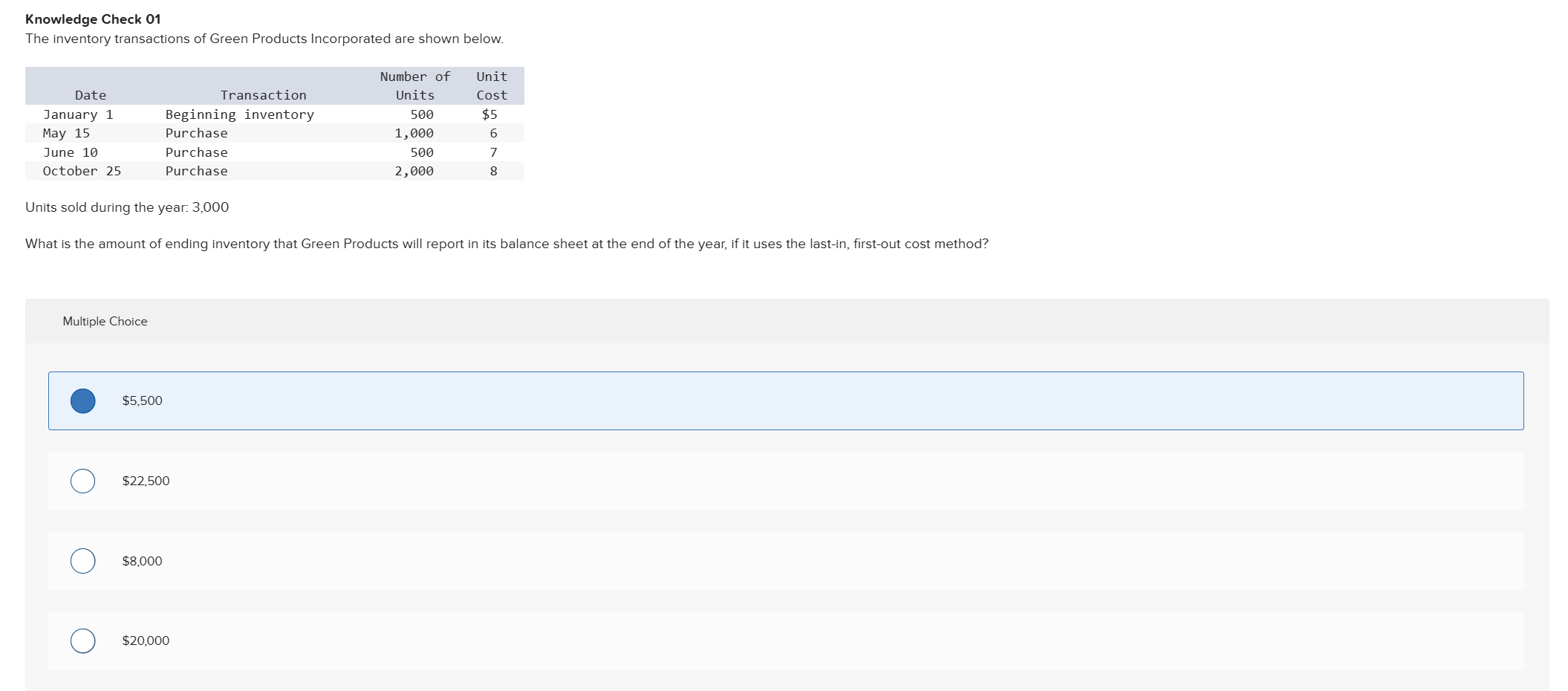

What is the amount of ending inventory that Green Products will report in its balance sheet at the end of the year, if it uses the last-in, first-out cost method?

Under LIFO, those remaining units come from the oldest layers:

Layer | Units Remaining | Unit Cost | Total |

|---|---|---|---|

Jan 1 (Beginning) | 500 | $5 | $2,500 |

May 15 | 500 | $6 | $3,000 |

Total | 1,000 | $5,500 |

The answer is $5,500 ✓

Weighted-average cost method Formula

COGS for sale / # of units avalible for sale

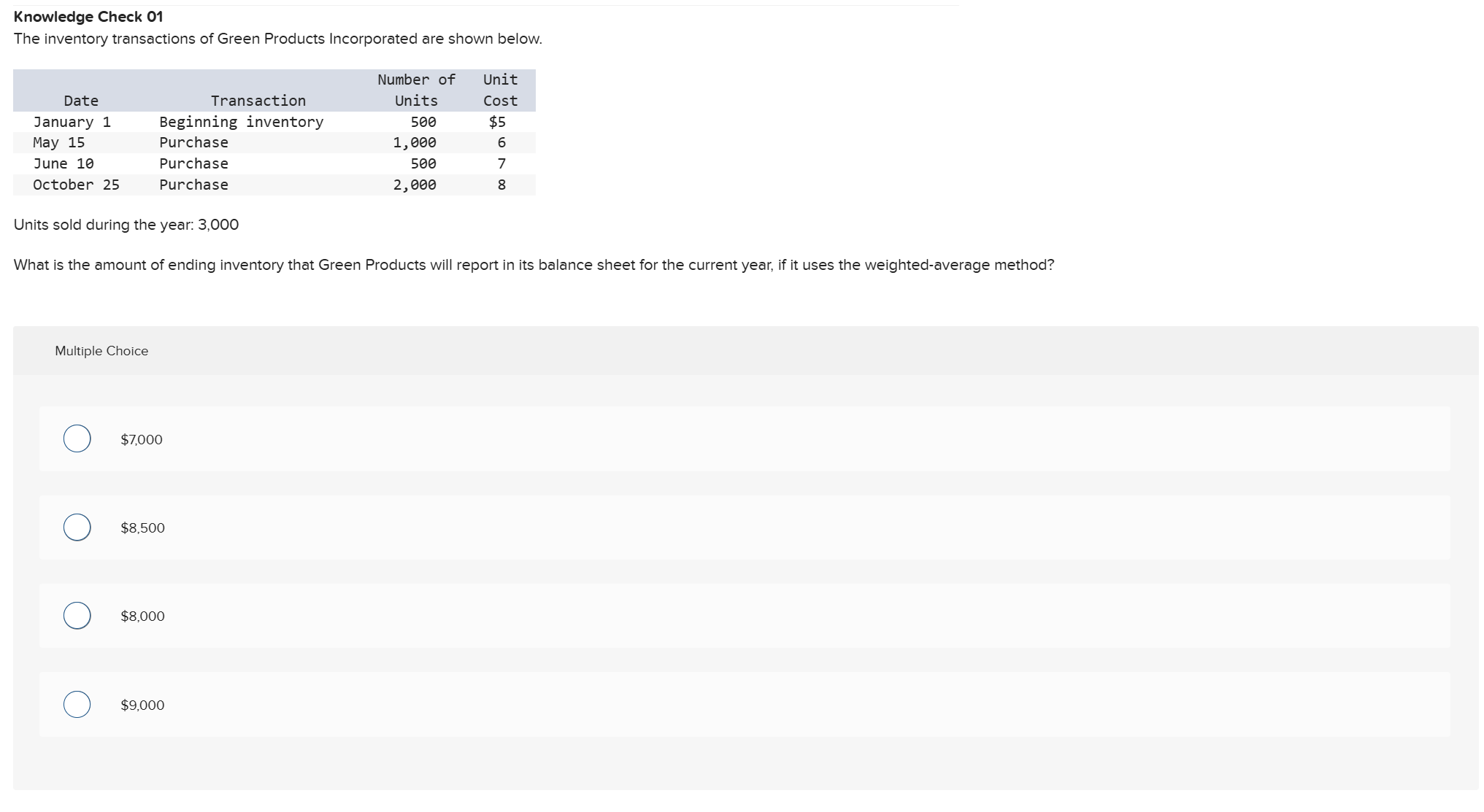

What is the amount of ending inventory that Green Products will report in its balance sheet for the current year, if it uses the weighted-average method?

A. $7,000

B. $8,500

C. $8,000

D. $9,000

Step 1: Calculate total cost of all inventory available

Layer | Units | Unit Cost | Total |

|---|---|---|---|

Jan 1 | 500 | $5 | $2,500 |

May 15 | 1,000 | $6 | $6,000 |

June 10 | 500 | $7 | $3,500 |

Oct 25 | 2,000 | $8 | $16,000 |

Total | 4,000 | $28,000 |

Step 2: Calculate weighted-average cost per unit

$28,000 ÷ 4,000 units = $7.00 per unit

Step 3: Apply to ending inventory units

1,000 remaining units × $7.00 = $7,000

The answer is $7,000.

Accountants often call FIFO the balance-sheet approach because _____

A. the amount of ending inventory appears in the balance sheet

B. the amount it reports for cost of goods sold more realistically matches the current costs of inventory needed to produce current revenues

C. the amount it reports for ending inventory better approximates the current cost of inventory

D. it better approximates actual cost of goods sold for most companies, because most companies' actual physical flow follows FIFO

C. the amount it reports for ending inventory better approximates the current cost of inventory

Which of the following is true of a period of falling inventory costs?

A. LIFO will result in lower tax payments than FIFO.

B. LIFO will report higher cost of goods sold than FIFO.

C. FIFO will report higher ending inventory than LIFO.

D. LIFO will report higher gross profit than FIFO.

D. LIFO will report higher gross profit than FIFO.

Here's the logic for falling prices:

Under LIFO, you sell the newest (cheaper) units first → lower COGS

Lower COGS means higher gross profit

Under FIFO, you sell the oldest (more expensive) units first → higher COGS

Higher COGS means lower gross profit

LIFO conformity rule

IRS rule requiring a company that uses LIFO for tax reporting to also use LIFO for financial reporting.

Perpetual Inventory System

An inventory system that is being continually updated to reflect inventory purchases and sales.

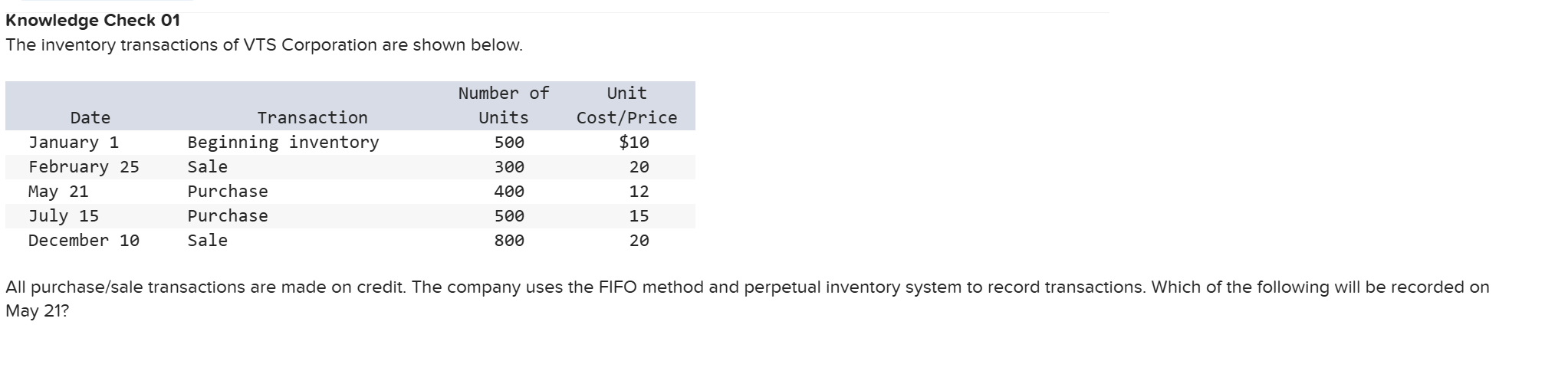

All purchase/sale transactions are made on credit. The company uses the FIFO method and perpetual inventory system to record transactions. Which of the following will be recorded on May 21?

A. Debit to Sales Revenue for $4,800

B. Credit to Cost of Goods Sold for $4,800

C. Credit to Accounts Payable for $4,800

D. Credit to Cash for $4,800

C. Credit to Accounts Payable for $4,800

FOB (Free On Board) Shipping Point

Title passes when the seller ships the inventory

What are Freight charges on incoming changes from suppliers called?

Freight in

Cost of Freight In Formula

Balance of Inventory + Cost of Freight In

A supplier offers a company terms 3/10, n/30 for a $10,000 purchase on account on January 1. The company uses a perpetual inventory system to record transactions. If the company makes the payment on January 10, the entry to record the payment will include a:

A. Debit to Accounts Payable for $9,700

B. Credit to Inventory for $300

C. Credit to Cash for $10,000

D. Debit to Accounts Payable for $300

Payment Within Discount Period (3/10, n/30)

First, decode the terms:

3/10 = 3% discount if paid within 10 days

n/30 = full amount due within 30 days

January 10 is within the 10-day window, so the company takes the discount.

Discount = $10,000 × 3% = $300 Cash paid = $10,000 − $300 = $9,700

The journal entry would be:

Account | Debit | Credit |

|---|---|---|

Accounts Payable | $10,000 | |

Cash | $9,700 | |

Inventory | $300 |

A company that returns items that were previously purchased on account will debit

Accounts Payable

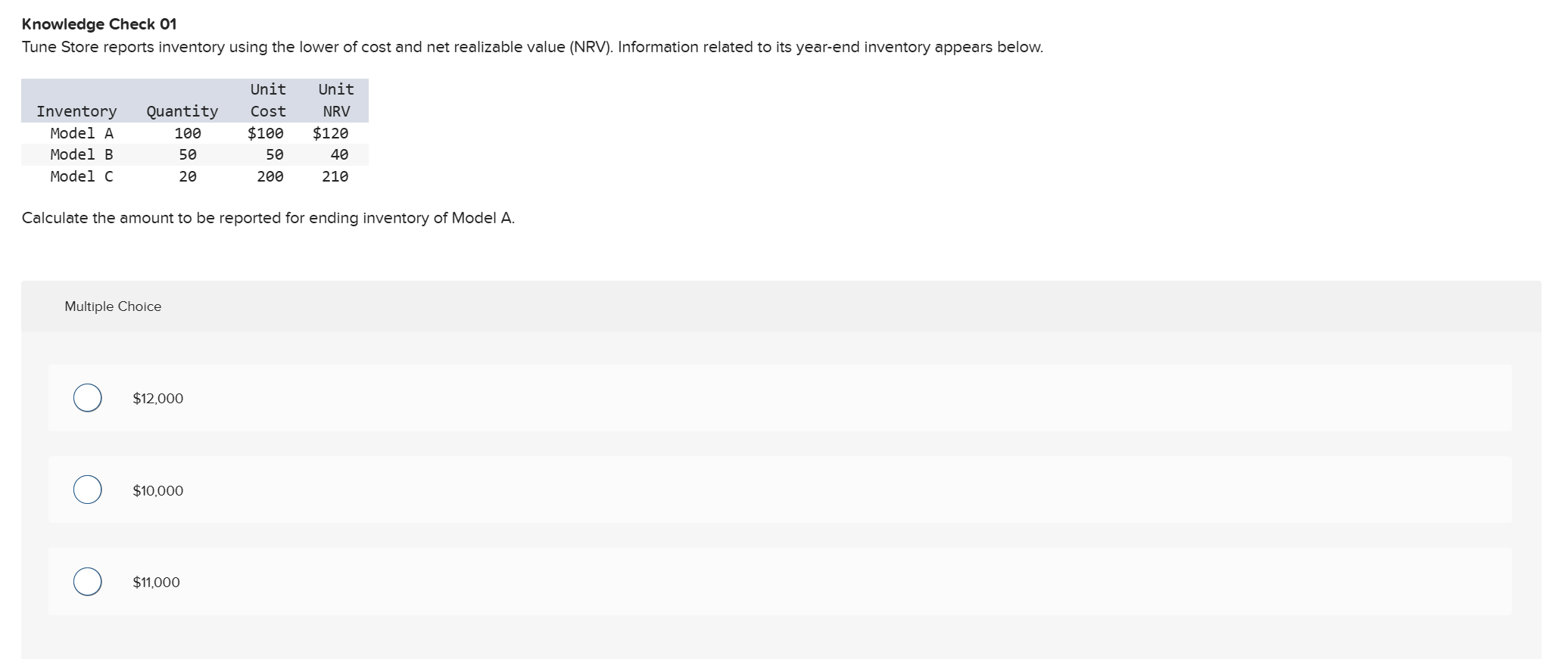

Calculate the amount to be reported for ending inventory of Model A.

Apply the rule: report at the lower of cost or NRV.

Unit Cost = $100

Unit NRV = $120

Lower = $100 (cost)

Since cost is lower, report at cost:

100 units × $100 = $10,000

The answer is $10,000

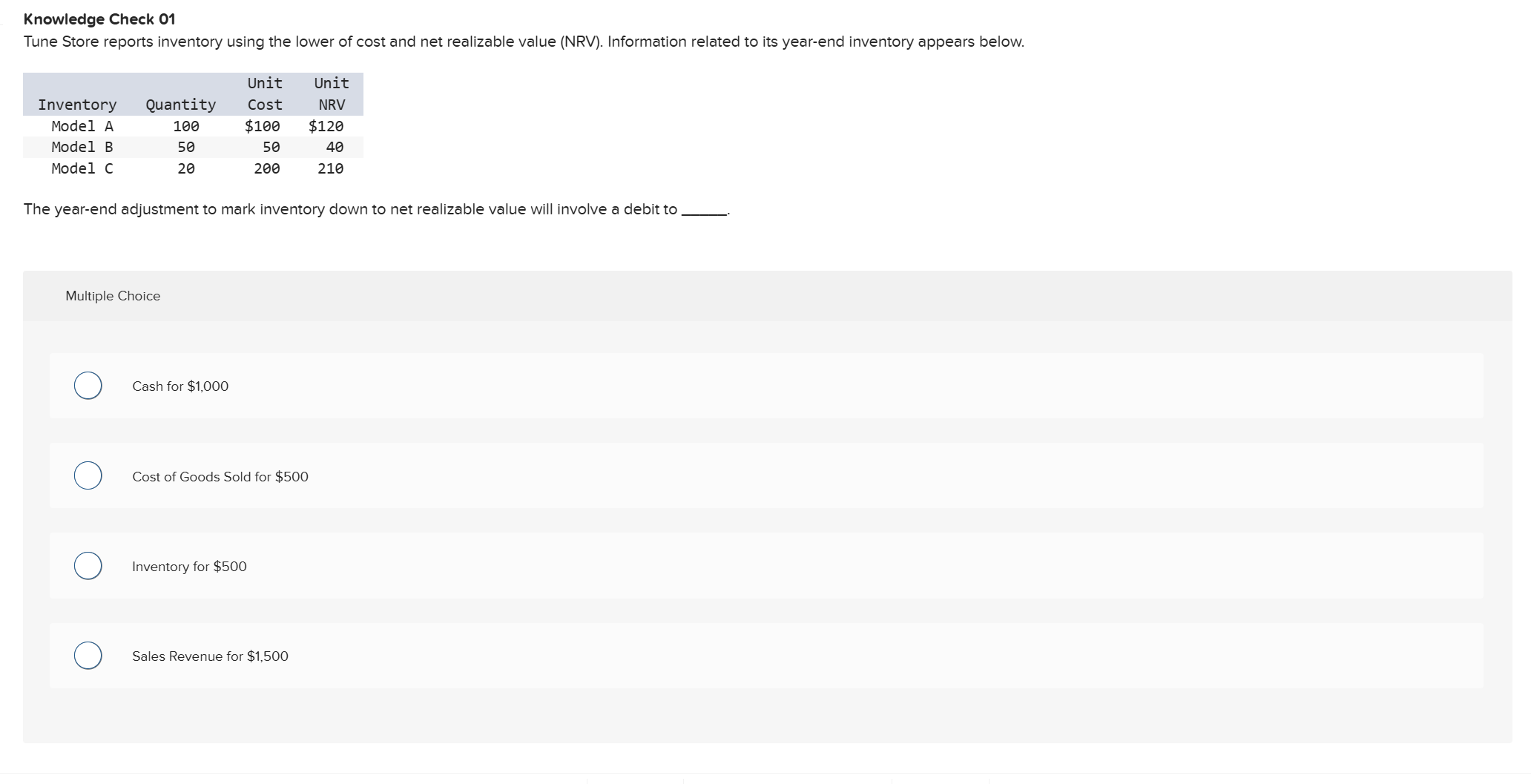

Tune Store reports inventory using the lower of cost and net realizable value (NRV). Information related to its year-end inventory appears below.

Model | Qty | Cost | NRV | Write-down per unit | Total Write-down |

|---|---|---|---|---|---|

Model A | 100 | $100 | $120 | None | $0 |

Model B | 50 | $50 | $40 | $10 | $500 |

Model C | 20 | $200 | $210 | None | $0 |

Only Model B needs a write-down: 50 × $10 = $500

The journal entry is:

Account | Debit | Credit |

|---|---|---|

Cost of Goods Sold | $500 | |

Inventory | $500 |

Inventory turnover ratio Formula

COGS / Average Inventory

Average Inventory Formula

Beginning Amount of Inventory + Ending Amount of Inventory / 2

Average Days in inventory Formula

365 Days / Inventory Turnover Ratio

Gross Profit Ratio Formula

Gross Profit / Net Sales

A company has total sales revenue of $500,000 for the year. Sales discounts, returns, and allowances total $50,000 and the cost of goods sold is $300,000. What is the company's gross profit ratio?

A. 44.44%

B. 40%

C. 60%

D. 33.33%

Step 1: Calculate Net Sales

$500,000 − $50,000 = $450,000

Step 2: Calculate Gross Profit

$450,000 − $300,000 = $150,000

Step 3: Calculate Gross Profit Ratio

$150,000 ÷ $450,000 = 33.33%

What types of inventory do manufacturing businesses hold?

Raw materials

Work In Progress

Finished Goods

What type of inventory do Merchandising businesses have?

Goods

Periodic Inventory System

A periodic system that adjusts the record of sales and purchases at the end of the reporting period