Market Efficiency & Elasticity

1/61

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

62 Terms

Market Efficiency

Producing the goods & services that society wants at the lowest possible cost.

Efficient Outcome

It is not possible to make someone better off without making someone else worse off.

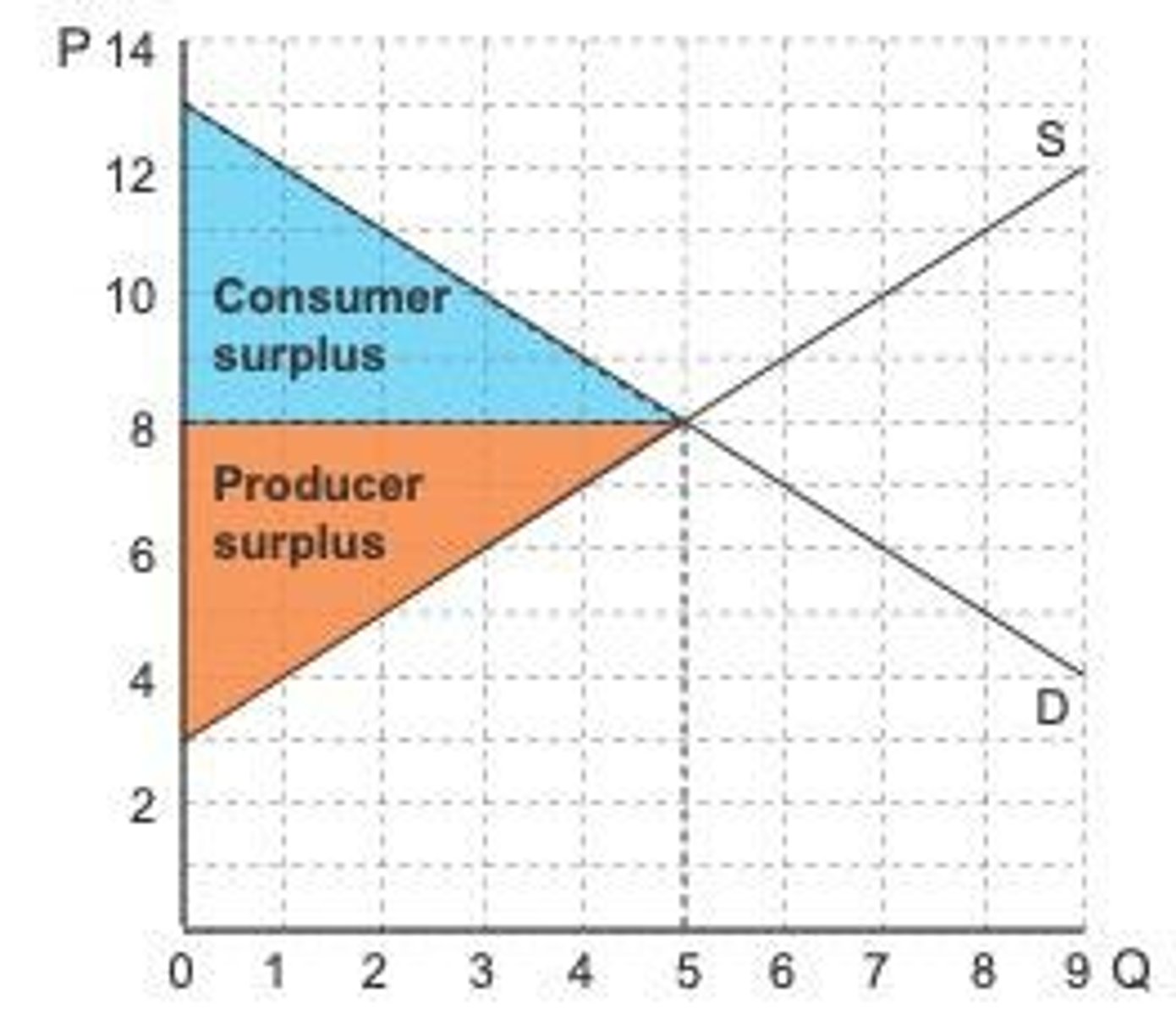

Consumer Surplus

The difference between what a consumer is willing to pay and what they actually pay.

Producer Surplus

The difference between what producers are willing to accept for a good versus what they actually receive.

Total Surplus

The sum of consumer surplus and producer surplus in a market.

Deadweight Loss

The loss of economic efficiency that occurs when the equilibrium outcome is not achievable or not achieved.

Price Ceiling

A maximum price set by the government that can be charged for a good or service.

Price Floor

A minimum price set by the government that must be paid for a good or service.

Marginal Benefit Curve

A demand curve that reflects the maximum price a consumer is prepared to pay for a good.

Net Gain

The difference between the total benefit received and the total cost incurred.

Consumer Surplus

The difference between what consumers are willing to pay for a good or service and what they actually pay.

Marginal Benefit

The additional satisfaction or utility that a consumer receives from consuming one more unit of a good or service.

Willingness to Pay

The maximum amount that a consumer is willing to spend on a good or service.

Producer Surplus

The difference between what producers are willing to accept for a good or service and what they actually receive.

Supply Curve

A graphical representation that shows the relationship between the price of a good and the quantity supplied.

Marginal Cost Curve

A curve that reflects the minimum price a producer is prepared to receive for a good, representing the cost of producing one more unit.

Total Revenue

The total amount of money a firm receives from selling its goods, calculated as price multiplied by quantity sold.

Net Gain

The difference between total revenue and total costs, indicating profit.

Market Efficiency

A situation in which resources are allocated in a way that maximizes total surplus, which is the sum of consumer and producer surplus.

Economic Welfare

The overall well-being of individuals in an economy, often measured by the levels of consumer and producer surplus.

Allocation Method

The process by which goods and services are distributed among consumers.

First-Come, First-Served

An allocation method where goods are distributed based on the order in which consumers arrive.

Sharing Equally

An allocation method where goods are divided equally among consumers.

Contest

An allocation method where goods are distributed based on competition among consumers.

Market Price

The price at which a good or service is sold in a competitive market.

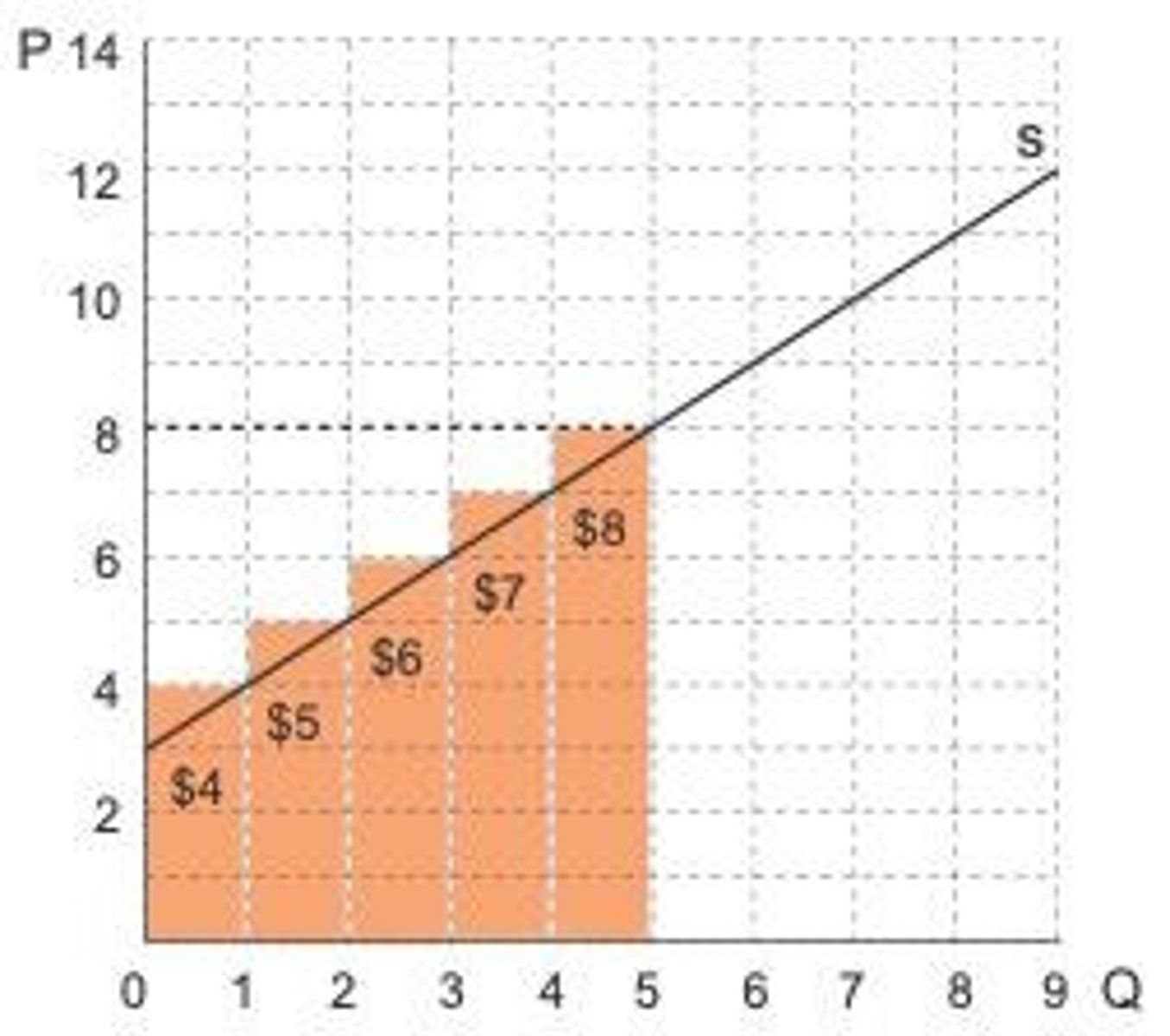

Consumer Surplus Calculation

For James, if he pays $42 for 7 pizzas and his total benefit is $63, his consumer surplus is $21.

Increase in Producer Surplus

If the price rises, there will be an increase in producer surplus because producers will sell more at a higher price.

Supply Curve

The supply curve shows the minimum price that firms must receive to supply a certain quantity of a good.

Producer Surplus Condition

Producer surplus will be positive when the price exceeds marginal cost.

Total Surplus

Total surplus is a measure of the economic welfare that a market creates for consumers and producers.

Total Surplus Formula

Total surplus = consumer surplus + producer surplus.

Economic Efficiency

Economic efficiency occurs when total surplus is maximised.

Equilibrium Price & Quantity

Total surplus equals a maximum only at the equilibrium output.

Deadweight Loss

When total surplus is reduced because of either under or overproduction, it is referred to as a deadweight loss.

Government Intervention

When governments intervene in markets they may decrease economic efficiency.

Market Restrictions

Examples include market restrictions, price ceilings, price floors, taxes, and subsidies.

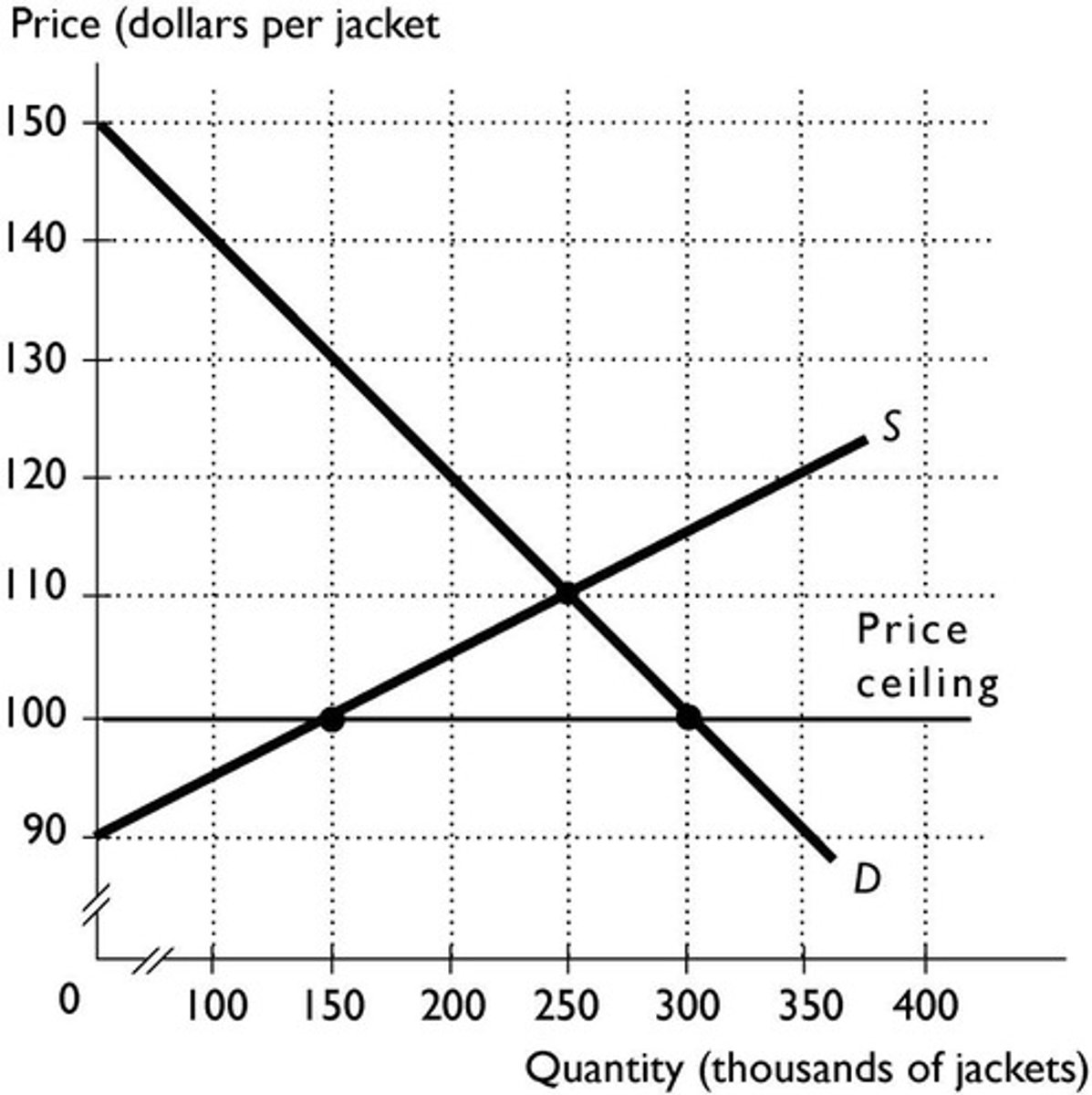

Price Ceiling Definition

A price ceiling is a legislated maximum price that sellers are allowed to charge in the market.

Price Ceiling Purpose

A price ceiling is designed to benefit consumers by keeping the price below the market clearing or equilibrium price.

Price Ceiling Effect

A price ceiling results in a shortage because the quantity demanded exceeds the quantity supplied.

Price Ceiling Impact

A price ceiling will create a deadweight loss - total surplus is decreased because quantity has fallen.

Price Floor Definition

A price floor is a legislated minimum price that sellers are allowed to charge in the market.

Price Floor

A minimum price that is set above the equilibrium price.

Surplus

A situation that results when the quantity supplied exceeds the quantity demanded.

Consumer Surplus

The benefit consumers receive when they pay less than what they are willing to pay.

Producer Surplus

The benefit producers receive when they sell at a higher price than the minimum they would accept.

Marginal Benefit

The additional benefit received from consuming one more unit of a good or service.

Marginal Cost

The additional cost incurred from producing one more unit of a good or service.

Shortage

A situation that occurs when the quantity demanded exceeds the quantity supplied.

Black Market

An illegal market in which the price exceeds a legally imposed price ceiling.

Price Ceiling

A maximum price that is set below the equilibrium price.

Market Efficiency

Occurs when the sum of consumer surplus and producer surplus is maximized.

Tax

A financial charge imposed by the government on goods and services to raise revenue.

Total Surplus

The total benefit to society, calculated as the sum of consumer surplus and producer surplus.

Price Elasticity

A measure of how much the quantity demanded or supplied responds to changes in price.

Price Inelastic

A situation where the quantity demanded or supplied is relatively unresponsive to price changes.

Equity Grounds

Justifications for economic policies based on fairness and income distribution.

Government Intervention

Actions taken by the government to affect the economy, such as setting price floors or ceilings.

Quantity Supplied

The total amount of a good that producers are willing and able to sell at a given price.

Quantity Demanded

The total amount of a good that consumers are willing and able to purchase at a given price.

Consumer surplus effect from tax

Buyers pay more & consume less - consumer surplus decreases.

Producer surplus effect from tax

Sellers receive less & sell less - producer surplus decreases.

Subsidy definition

A subsidy is a grant paid by the government to a producer with the purpose of reducing costs and increasing output.