Unit 1 - AP Macro

1/33

Earn XP

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

Scarcity

we have unlimited wants but limited resources

Because of scarcity choices need to be made

trade-offs + opportunity cost

Consumer Goods

Direct consumption (pizza)

Capital Goods

Indirect Consumption (cheese, knives, bowl)

Factors of Production

Land, Labor, Capital (Human +Physical), Entrepreneurship

Physical Capital

Any human-made resource that is used to create other goods and services.

Human Capital

Any skills or knowledge gained by a worker through education and experience.

Productivity

A measure of efficiency that shows the number of outputs per unit of input.

Price vs Cost

Amount buyer pays for product vs Amount seller pays to make good

Constant Opportunity Cost

Resources are easily adaptable for producing either good. (pizzas and calzones)

3 shifters of PPC

1. Change in resource quantity or quality

2. Change in Technology

3. Change in Trade (allows more consumption)

Per Unit Opportunity Cost

Opportunity Cost / Units Gained

Absolute Advantage

The producer that can produce the most output OR requires the least amount of inputs (resources).

Comparative Advantage

The producer with the lowest opportunity cost.

Output Questions

OOO= Output: Other goes Over

Input Questions

IOU = Other goes Under

Demand

The different quantities of goods that consumers are willing and able to buy at different prices.

Demand Shifters

Change in Disposable Income (DI) Spendable income after taxes and debts are paid

Change in spending (domestic/foreign)

Change in interest rates

Change in population

Change in preferences

Prices don’t shift demand unless price of another good changes.

Substitutes are goods used in place of one another. (coke + pepsi)

Complements are two goods that are bought and used together. (hot dogs + buns)

Supply

The different quantities of a good that sellers are willing and able to sell (produce) at different prices.

Law of Supply

DIRECT (or positive) relationship between price and quantity

Supply Shifters

Prices/Availability of inputs (resources)

Number of Sellers

Technology

Government Action: Laws, Taxes & Subsidies

Expectations of Future Profit

Surplus or Shortage in a Free Market

Prices automatically move towards equilibrium; surplus: producers will lower prices shortage: producers will raise prices

Price Ceiling

Maximum legal price a seller can charge for a product.

Goal: Make affordable by keeping price from reaching Eq.

Result: Shortage —> Black Markets (demand is higher than the quantity)

Price Floor

Minimum legal price a seller can sell a product.

Goal: Keep price high by keeping price from falling to Eq.

price control

Price ceilings and price floors result in a misallocation of resources

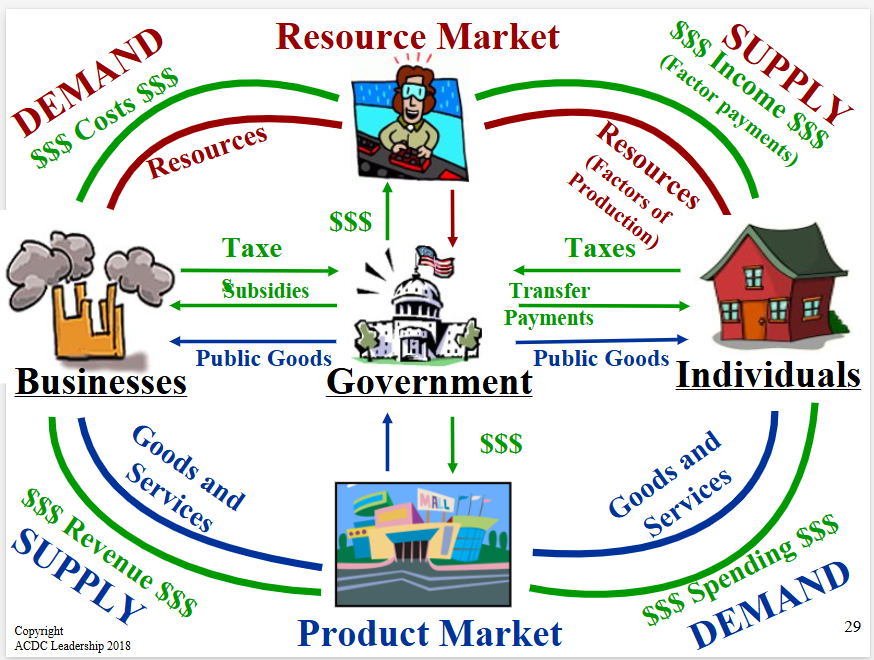

Circular Flow Model

(CFM) The Product Market

The “place” where goods and services produced by businesses are sold to households.

(CFM) The Resource (Factor) Market

The “place” where resources (land, labor, capital, and entrepreneurship) are sold to businesses.

Private Sector

Part of the economy that is run by individuals and businesses.

Public Sector

Part of the economy that is controlled by the government.

Factor Payments

Payment for the factors of production, namely: rent, wages, interest, and profit.

Transfer Payments

When the government redistributes income (ex: welfare, social security)

Subsidies

Government payments to businesses.